Hormuz Hit US Salt at Its Most Vulnerable: 25 Years of Supply Neglect Left No Buffer

Hormuz disruption, rising energy costs, and 31% US salt import reliance are tightening North American supply and supporting domestic pricing power.

- Since 28 February 2026, disruption in the Strait of Hormuz has kept Brent crude elevated, with the US Energy Information Administration's May 2026 Short-Term Energy Outlook projecting $106 per barrel through Q2 2026 before declining to $79 in 2027, increasing production costs for vacuum-pan and chemical-grade salt.

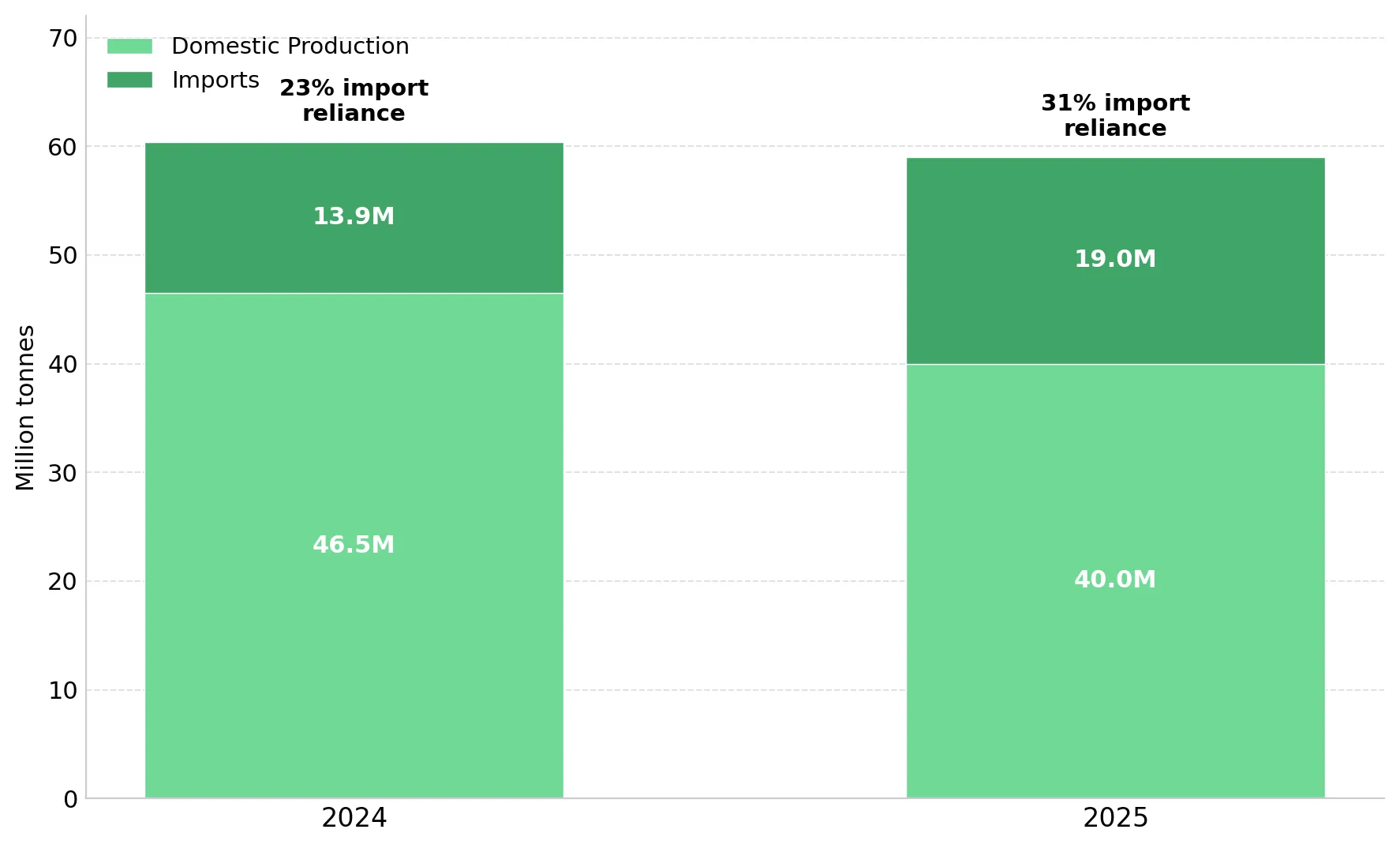

- The US Geological Survey's Mineral Commodity Summaries 2026 reports US salt net import reliance rose to 31% in 2025 from 23% in 2024, with 19 million tonnes of imports supplementing 40 million tonnes of domestic production.

- The European Chemical Industry Council reports 37 million tonnes of European chlor-alkali capacity closures since 2022, while Adani and Reliance are building Indian chlor-alkali plants that could absorb roughly 8 million tonnes per year of salt previously exported into seaborne markets.

- The World Bank's April 2026 Commodity Markets Outlook projects 2026 commodity prices rising 16%, including a 24% increase in energy prices, increasing freight and processing costs for imported salt.

North American Salt Import Deficit & Asian Chlor-Alkali Demand Tighten Global Supply

The US Geological Survey's Mineral Commodity Summaries 2026 reports 42% of US salt demand supports chlor-alkali production used in plastics, water treatment, and pulp and paper manufacturing, while another 37% supports highway de-icing. Together, these end markets leave 79% of US salt demand tied to chemical production and road-safety procurement that remains relatively stable during economic slowdowns.

Asian chlor-alkali expansion could increase industrial salt demand by roughly 10 million tonnes per year by 2028 as production shifts from Europe to lower-cost regions. North America has not commissioned a new underground salt mine since 2001, contributing to 31% net import reliance and an annual supply deficit of 8 to 10 million tonnes.

Strait of Hormuz Disruption & Higher Energy and Freight Costs Raise Salt Import Prices

Since US and Israeli forces struck Iran on 28 February 2026, tanker traffic through the Strait of Hormuz has remained below pre-conflict levels, according to the US Energy Information Administration's May 2026 Short-Term Energy Outlook. The outlook projects Brent crude at $106 per barrel through Q2 2026 before declining to $89 in Q4 and $79 in 2027. Higher oil prices affect salt through chlor-alkali electricity costs and higher freight rates for imported supply.

Rising Energy Costs Increase Chlor-Alkali and Vacuum-Pan Salt Production Costs

The International Energy Agency's Electricity 2026 estimates electricity accounts for more than 40% of chlor-alkali production costs, while each tonne of caustic soda production consumes 1.4 to 1.8 tonnes of salt. Higher natural gas and electricity prices reduce operating rates at higher-cost chlor-alkali plants, while Brent crude above $100 per barrel through mid-2026 increases production costs for vacuum-pan and food-grade salt. The US Geological Survey reports average vacuum-pan salt prices reached approximately $260 per tonne in 2025 versus $54 per tonne for rock salt because of the higher energy cost of evaporation processing.

US Geological Survey trade data shows the US sourced 23% of salt imports from Chile and 6% from Egypt between 2021 and 2024, with shipments requiring more than 14 days of transit. Higher bunker fuel costs and rerouting premiums linked to Red Sea and Persian Gulf disruption have increased delivered import costs, while wider regional price spreads during the 2025 to 2026 winter season improved pricing for producers with shorter shipping routes.

North American Salt Import Reliance & 25 Years Without New Mine Capacity

Even without Hormuz disruption, North America entered 2026 with a multi-year salt supply deficit that imports have filled since at least 2015. Limited mine construction and rising import dependence have increased North America's exposure to higher freight and energy costs, while new greenfield supply remains years from production.

US Salt Imports Rise to 31% as Domestic Supply Lags Stable Demand

The US Geological Survey's Mineral Commodity Summaries 2026 reports US salt production at 40 million tonnes in 2025 against apparent consumption of 57 million tonnes. Imports filled the supply deficit with 19 million tonnes in 2025, up from 13.9 million tonnes in 2024. Net import reliance rose from 23% in 2024 to 31% in 2025, the highest level in the past five years.

The US Geological Survey reports the chemical industry accounts for 42% of US salt sales, with salt brine supplying roughly 90% of chlor-alkali feedstock demand. Highway de-icing accounts for another 37% of demand, supported by state and municipal procurement tied to road-safety liability requirements. Together, chemical feedstock and de-icing account for 79% of US salt demand, making consumption more stable during economic slowdowns than construction-linked commodities such as copper.

Salt Mine Closures & Limited Replacement Supply Tighten North American Capacity

American Rock Salt in New York, commissioned in 2001, remains the last new underground salt mine built in North America. North American salt production capacity has declined over the past 25 years as older mines closed without replacement supply. Cargill's closure of the Avery Island, Louisiana, mine removed approximately 2.5 million tonnes per year of domestic production. The US Geological Survey reported a regional rock salt shortage in New York during early 2025 as winter demand exceeded available supply, highlighting limited spare production capacity in the market.

Below-average snowfall reduced de-icing demand during the 2025 to 2026 winter season, but the National Oceanic and Atmospheric Administration's weak La Niña forecast implies higher salt consumption next winter. State and municipal transportation departments continue purchasing road salt regardless of price because road-safety obligations limit their ability to reduce procurement.

European Chlor-Alkali Closures & Asian Demand Growth Tighten Salt Supply

Asian chlor-alkali expansion is increasing industrial salt demand as North American and European supply remains constrained. Chlor-alkali production is shifting from high-cost Europe to lower-cost Asian plants, but limited availability of salt above 97% purity restricts supply for membrane-cell chemical processing.

37 Million Tonnes of European Chlor-Alkali Capacity Has Closed Since 2022

The European Chemical Industry Council reports 37 million tonnes of European chemical capacity closures since 2022, equal to roughly 9% of regional capacity. Closures announced across 2025 and early 2026 include Fortischem, Spolana, Arkema Jarrie, and Vencorex, while Vynova is closing its Beek facility in the Netherlands and Dow is exiting Schkopau in Germany.

The European Union's Carbon Border Adjustment Mechanism entered its definitive phase on 1 January 2026, increasing compliance costs for importers of chlor-alkali products. European Union Emissions Trading System allowances averaged €72 per tonne in 2025, adding roughly €65 per tonne of caustic soda produced at coal-powered membrane-cell chlor-alkali plants. Higher carbon compliance costs increase the incentive for chlor-alkali producers to shift capacity from Europe to lower-cost Asian markets.

Asian Chlor-Alkali Expansion & Rising Demand for High-Purity Salt

Sixteen chemical plants under construction in India, China, and Indonesia are projected to add 10.2 million tonnes per year of industrial salt demand by 2028. Adani and Reliance are building Indian chlor-alkali plants that could consume roughly 8 million tonnes per year of salt previously exported into Asian seaborne markets, reducing export availability for other buyers.

Membrane-cell chlor-alkali plants require salt purity above 97% to avoid operating disruptions, while most Southeast Asian solar salt averages roughly 94% sodium chloride. Indonesia is targeting salt self-sufficiency by 2027 under Presidential Regulation No. 126/2022, but upgrading lower-purity solar salt to membrane-cell specifications requires significant refining investment. Higher-purity rock salt and vacuum-pan products command higher prices than bulk solar salt because membrane-cell chlor-alkali plants cannot substitute lower-grade feedstock.

Limited North American Salt Projects Increase Scarcity Value for Development-Stage Equities

Few new North American salt projects are advancing toward production, limiting the number of public equities exposed to the regional supply deficit.

Atlas Salt's Newfoundland Project & the US Import Replacement Opportunity

Atlas Salt is a Development-stage Canadian company advancing the Great Atlantic Salt Project in Newfoundland, targeting North American de-icing and chemical-grade salt markets. The project contains 95 million tonnes of probable reserves grading 95.9% sodium chloride under National Instrument 43-101 standards. The 95.9% grade exceeds the threshold for premium de-icing salt and approaches the 97% purity required for membrane-cell chlor-alkali feedstock.

Planned production of 4 million tonnes per year would address a meaningful portion of North America's 8 to 10 million tonne annual salt import deficit. Deep-water port access in Newfoundland enables shipping times of less than three days to the US Eastern Seaboard versus more than 14 days from Chilean and Egyptian suppliers, reducing freight exposure and delivery risk. Newfoundland and Labrador released the project from provincial environmental assessment in April 2024, reducing a major permitting risk for mine development.

The 2025 Updated Feasibility Study reports an after-tax Net Present Value of $920 million using an 8% discount rate. The study models average annual post-tax free cash flow of $188 million and average annual EBITDA of $325 million over a 24.3-year mine life using a base salt price of $81.67 per tonne.

Atlas Salt Trades at a Deep Discount to Salt Producer Valuation Multiples

Atlas Salt trades at an enterprise value of $138.5 million against a $920 million after-tax Net Present Value, implying roughly 0.1x forward Net Asset Value. Operating salt producers trade at materially higher valuation multiples than Atlas Salt. Compass Minerals trades at 9.1x enterprise value to EBITDA, while recent transactions for K+S Americas and US Salt were completed at 12.5x and 16.5x enterprise value to EBITDA respectively.

Atlas Salt trades at a discount because the project still requires construction financing. The 2025 Updated Feasibility Study outlines $589 million in pre-production capital expenditure that remains unfunded, while Endeavour Financial has been engaged as project finance advisor, making project financing the key valuation catalyst.

Nolan Peterson, Chief Executive Officer of Atlas Salt, describes why long-life salt assets may trade differently from conventional mining projects with shorter reserve lives and more volatile cash flows:

“What we bring is stability to the project cash flows. We have a 25-year mine life, an NPV8 profile, and roughly 50 years of resource already defined by drilling, which makes the value decline much slower than a typical mining project.”

Oil Prices, Project Financing & Import Costs Remain Key Salt Market Risks

The investment case depends on continued import dependence, elevated freight costs, and successful project financing. The thesis weakens if Strait of Hormuz shipping normalizes faster than current US Energy Information Administration forecasts or if Brent crude falls below $80 per barrel, reducing freight and chlor-alkali electricity costs. Pre-production financing remains the primary risk for development-stage companies, while near-term catalysts include the US Energy Information Administration's 9 June 2026 Short-Term Energy Outlook, India's monsoon forecast for Gujarat solar salt production, and the World Bank's next Pink Sheet update on commodity and energy costs.

The Investment Thesis for Salt

- North America's 31% net import reliance and 25 years without a new underground salt mine have created a supply deficit that additional industrial demand would tighten further.

- Higher energy and freight costs linked to Hormuz disruption increase imported salt prices, improving pricing and margin potential for domestic producers and permitted projects with deep-water port access.

- Chlor-alkali capacity expansion in Asia could increase industrial salt demand by roughly 10 million tonnes per year by 2028, primarily for feedstock above 97% sodium chloride purity.

- US salt demand remains relatively stable because 79% of consumption supports chemical feedstock and highway de-icing, both tied to industrial operations and government road-safety procurement.

- Development-stage North American salt projects priced at 0.1x forward Net Asset Value carry binary financing-execution risk but expose investors to a 9 to 16x enterprise value to EBITDA re-rating range established by operating salt comparables once financing risk is retired

The salt market entered 2026 with limited spare supply capacity, and the Hormuz energy shock has increased spot prices for imported salt. Institutional investors will focus on whether development-stage salt companies can rerate toward the 9x to 16x enterprise value to EBITDA multiples assigned to operating producers after project financing is secured. Retail investors are effectively buying exposure to a commodity market with a 31% US import deficit, constrained shipping routes, and demand tied to chemical production and road safety. Pre-production financing remains the primary risk, and investors could face capital loss if development-stage projects fail to secure funding or advance into construction.

TL;DR

Disruption in the Strait of Hormuz has increased energy and freight costs, raising prices for imported salt as the US becomes increasingly dependent on foreign supply. North America now relies on imports for 31% of salt demand while no new underground salt mine has been built since 2001, creating a structural supply deficit. At the same time, European chlor-alkali plant closures and expanding Asian chemical capacity are tightening global industrial salt markets, particularly for high-purity feedstock. These conditions improve the long-term pricing environment for domestic salt producers and development-stage projects, though financing risk remains the key challenge for new entrants.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed