i-80 Gold's Recapitalisation Brings Mineral Point Forward in the Nevada Buildout

i-80 Gold's recapitalisation dedicates US$50 million to earlier Mineral Point work, advancing a Phase 3 asset central to the Nevada production buildout.

- i-80 Gold's recapitalisation is now complete, with total capital raised exceeding US$1 billion, leaving the company fully funded for Phase 1 and Phase 2 of its Nevada development plan.

- US$50 million of Franco-Nevada royalty financing has been dedicated to Mineral Point infill drilling, engineering, and early-stage permitting in 2026, bringing preparatory activity forward ahead of Phase 3.

- The 2026 Mineral Point work programme covers approximately 131,000 metres of planned drilling, with exploration spend of US$40 million to US$45 million and a further US$5 million allocated to permitting and technical work.

- Mineral Point holds an indicated resource of 3.4 million ounces of gold and 104.3 million ounces of silver, with Mineral Point identified as potentially the largest producing asset in the i-80 Gold portfolio.

- The asset remains formally a Phase 3 project, with a 2027 study, subsequent permitting, and construction still ahead before any production, expected in the early 2030s.

What Has Happened

The completion of i-80 Gold's [TSX:IAU] [NYSE American:IAUX] recapitalisation in March 2026 has reshuffled the timing of preparatory activity across its Nevada asset portfolio. Total capital raised now exceeds US$1 billion, and the company is fully funded for Phase 1 and Phase 2 of its development plan. The most consequential near-term effect involves Phase 3: US$50 million of the Franco-Nevada royalty financing has been designated for Mineral Point infill drilling, engineering, and early-stage permitting in 2026, in support of a study anticipated for 2027. This capital enables work that was not previously funded to begin earlier than a strict Phase 3 designation would imply.

Mineral Point's Role in the Portfolio

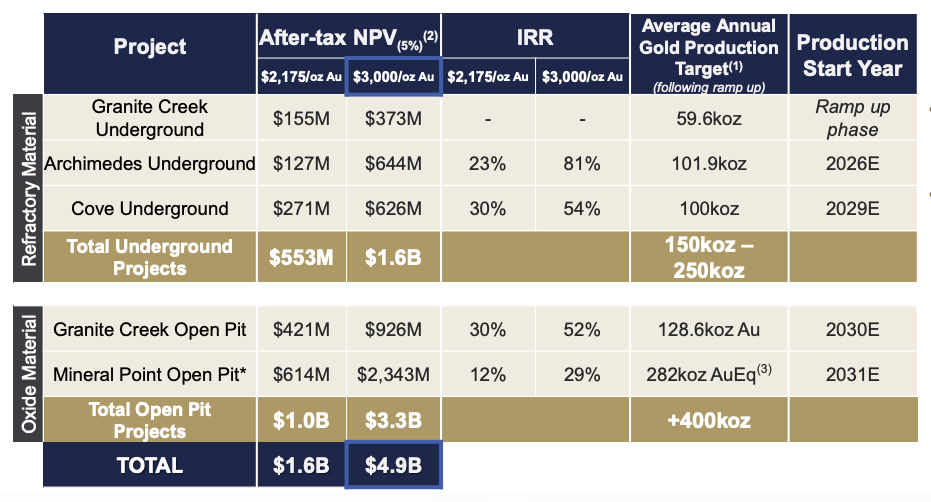

Mineral Point is a large oxide gold and silver deposit at Ruby Hill, Nevada. It sits in the third phase of i-80 Gold's three-phase development sequence, which prioritises underground hard-rock operations at Granite Creek and Archimedes in Phase 1, alongside the Lone Tree autoclave processing facility, and the Cove underground and Granite Creek open pit operations in Phase 2. Mineral Point is identified as potentially the largest producing asset in the portfolio and the most significant step change in company-wide production.

The deposit is planned as an open-pit operation with on-site heap leach processing, distinguishing it from the pressure-oxidation-dependent underground projects that define the earlier phases. That distinction preserves Mineral Point's development independence: its processing route does not rely on Lone Tree infrastructure, meaning its construction and production timeline is governed by permitting, capital, and study completion rather than by upstream processing capacity.

What the New Capital Now Allows

The Franco-Nevada royalty financing totals US$250 million, with US$225 million advanced at closing and a further US$25 million subject to conditions. Of that total, US$50 million is specifically allocated to Mineral Point activities in 2026, covering infill drilling, engineering, and early-stage permitting. The second conditional US$25 million becomes available after the initial US$25 million allocated to Mineral Point has been deployed, creating a staged capital release mechanism tied directly to asset-level progress. The gold prepayment facility is also planned to transition into a corporate revolver to fund later Mineral Point development

Executive Vice President and Chief Operating Officer of i-80 Gold, Paul Chawrun, is direct about what the new capital makes possible:

"What this capital raise provides for us is to do the drilling, get that done sooner, and it hasn't happened yet because it takes a little bit of time, but to start the environmental impact statement process sooner, and then that would allow us to accelerate the timeline for Mineral Point by anywhere from one to two years."

The capital structure carries a further signal around partner interest. Chawrun places Mineral Point drilling centrally in his account of why the royalty arrangement came together:

"It allows us to do a lot of drilling both at Ruby Underground and at the Mineral Point project on the open pit side, and that was something that Franco-Nevada was very excited about, and that is one of the reasons why they were very excited to be our partner in developing this story."

The 2026 Mineral Point Work Programme

The scale of the 2026 programme positions Mineral Point as an active development priority rather than an asset held in reserve. Approximately 131,000 metres of drilling is planned, with core drilling having commenced in June 2025. The exploration budget for Mineral Point in 2026 stands at US$40 million to US$45 million, with a separate US$5 million directed toward permitting and technical work. Evaluation and exploration expense for the Mineral Point open pit is guided at US$45 million to US$50 million, within a wider portfolio-level permitting and technical spend line.

Engineering work covers planning for a large-scale open-pit mine, dewatering requirements specific to the Ruby Hill geology, and the on-site heap leach operation. These workstreams run in parallel with the infill drilling and are designed to support the resource conversion and technical inputs required before the 2027 study can proceed.

Why Management Is Pulling Work Forward

The stated objective of the 2026 drilling campaign is to convert inferred material into measured and indicated categories, improving the technical foundation for a formal study. Chawrun is specific about the sequence:

"We're going to be looking to convert all of that to measured and indicated to eventually get to a prefeasibility study in the early part of 2027."

The connection between earlier capital deployment and a shorter overall timeline runs through the Environmental Impact Statement (EIS). In Nevada, federal environmental review is a multi-year process, and initiating it earlier compresses the gap between study completion and construction readiness. Earlier drilling, combined with earlier initiation of the EIS, could bring the project forward by 1 to 2 years, though this remains contingent on programme execution and regulatory progress.

Construction is scheduled to begin around 2029, with initial production from 2031. These dates remain subject to change depending on the outcome of the 2026 drilling programme and the timing of the formal environmental review.

Why Mineral Point Matters to the Longer-Term Production Profile

The economic rationale for prioritising Mineral Point's earlier preparation reflects the scale of the deposit's eventual contribution. The indicated resource stands at 3.4 million ounces of gold at 0.48 grams per tonne and 104.3 million ounces of silver at 15.0 grams per tonne, with an additional inferred resource of 2.1 million ounces of gold at 0.34 grams per tonne and 91.5 million ounces of silver at 14.6 grams per tonne. The average annual production following ramp-up is projected at approximately 282,000 gold equivalent ounces, at an all-in sustaining cost of US$1,400 per ounce of gold.

Published technical work produces an after-tax net present value at a 5% discount rate (NPV5%) of US$614 million and an internal rate of return (IRR) of 12%, based on gold at US$2,175 per ounce and silver at US$27.25 per ounce. At US$3,000 per ounce for gold and US$35.00 per ounce for silver, the sensitivity table shows an after-tax NPV5% of US$2.343 billion and an IRR of 29%. Mine construction capital is estimated at US$708 million. Mine life is presented as 16.5 years in detailed project metrics and approximately 17 years in summary materials.

These figures are outputs of existing technical work and will be updated when the 2027 study is completed. The resource conversion programme underway in 2026 is designed to improve the quality of the technical inputs for that study.

What Still Has to Be Proved

Mineral Point's Phase 3 classification accurately reflects what the asset still requires before production is possible. A 2027 study remains ahead, and its scope, whether at prefeasibility or feasibility level, has not been consistently characterised. The EIS process has not yet formally commenced. The second conditional US$25 million royalty payment remains subject to conditions. Construction, carrying a capital requirement of US$708 million, lies several years out, and with production targeted for the early 2030s.

The open pit configuration, dewatering requirements, and heap leach design at Mineral Point's scale present engineering and permitting complexity that infill drilling and early engineering work address incrementally. What has changed with the recapitalisation is that those workstreams are now funded and underway, rather than sequenced behind the completion of Phase 1 and Phase 2. The preparatory gap between Phase 3's formal start and its eventual execution has narrowed, but the major gating milestones ahead of construction remain.

Broader Context

The rationale behind pulling Mineral Point preparatory work forward reflects a dynamic that appears across large-asset phased development portfolios: permitting timelines are typically the longest and least controllable variable in mine development, and companies that initiate environmental review earlier can compress total project lead times without accelerating construction capital commitments. i-80 Gold's three-phase structure was designed to sequence capital intensity, with Phase 1 and Phase 2 prioritising near-term production and cash flow before the company's largest capital requirement is engaged. Mineral Point sits at the far end of that spectrum in terms of construction cost, but its permitting and study timelines do not have to be governed by when the earlier phases reach completion.

The Franco-Nevada royalty structure reinforces this. By attaching US$50 million directly to Mineral Point 2026 activity rather than providing general corporate capital, the financing creates a committed programme with its own momentum, distinct from discretionary exploration allocations that might otherwise be redirected in a capital-constrained environment.

What to Watch Next

The 2026 drilling programme is the most immediate data stream to follow. Progress updates and any interim resource disclosures will indicate whether infill drilling is converting inferred material into measured and indicated categories at the grade and volume needed to support a credible 2027 study. Whether the EIS formally commences during 2026 is a parallel signal: starting the EIS process sooner is a direct objective of the capital deployment, but no formal initiation has been confirmed. Any disclosure that environmental review has begun would represent a material development for Mineral Point's timeline.

The 2027 study's scope and label have not been consistently characterised, with references to both prefeasibility and feasibility levels across different disclosures. How the company formally characterises the study on publication will indicate how close Mineral Point is to a construction decision at that point, and whether the study is presented as a step toward a further study or as a direct precursor to financing and permitting decisions.

Subsequent company disclosures should be monitored for consistency on the production timeline. The current production timeline targets 2031, based on a construction start around 2029, itself contingent on permitting and study milestones that are now being accelerated but not yet confirmed. If the 2026 programme delivers on management's stated targets, future guidance may reflect a revised path to production, marking the recapitalisation's sequencing effect and translating into a formally acknowledged, shorter timeline.

FAQs (AI-Generated)

Mineral Point is a large oxide gold and silver open-pit deposit at Ruby Hill, Nevada. It sits in Phase 3 of i-80 Gold's three-phase development sequence, following underground operations and processing infrastructure work in Phases 1 and 2.

US$50 million of the Franco-Nevada royalty financing is dedicated to Mineral Point infill drilling, engineering, and early-stage permitting in 2026. A further US$25 million royalty payment becomes available after the initial allocation is deployed, subject to conditions.

The programme targets approximately 131,000 metres of infill drilling to convert existing inferred resources into measured and indicated categories, providing the technical foundation for a study anticipated in 2027.

No. Mineral Point remains a Phase 3 project. What has changed is that infill drilling, engineering, and early-stage permitting are now funded and underway, advancing preparatory work earlier than the phased sequencing would otherwise allow.

The main watch points are 2026 drilling results and any interim resource update; whether a formal EIS process commences; and how the scope and label of the 2027 study are characterised when it is published.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed