K92 Mining (KNT) - Standout Mid-tier High-Grade Gold Producer

K92 Mining owns and operates the Kainantu Gold Mine in PNG. It is a high-grade, low-cost underground mine in a region known for Tier 1 deposits.

K92 Mining owns and operates the Kainantu Gold Mine in the Eastern Highlands province of Papua New Guinea. The Kainantu Gold Mine is a high-grade, low-cost underground mine in a region known for Tier 1 deposits.

We caught up with John Lewins, CEO of K92 Mining to discuss how things have gone since we last spoke in October, a review of 2020 and what we should be looking for in 2021. Our last interview went into detail about the company business plan, strategy, the team’s success and relevant experience in the field.

Company Overview

K92 is a Gold-Copper producer, operating in Papua New Guinea with one of the highest-grade Gold mines in the world. It was the 4th highest-grade for mining in the last 12-months with over 5Moz. This year they will produce close to 100,000oz. They are also one of the lowest-cost producers in the world. K92 has been growing the business over the last 3-years since January 2018 when they declared commercial production and have increased their production every year: They are cash positive, have almost no debt and they’re looking at expansion which they would be funding from their own cash flow.

TSX Listing & Trebled Share Price

The move from TSX-V to TSX was a logical move to make for K92 Mining. They are already in the GDX and GDXJ, and the TSX opens up new institutional investment for the company. The growth in the share price equates directly to a growth in market cap which is due to the consistent high grades they are hitting at Kora.

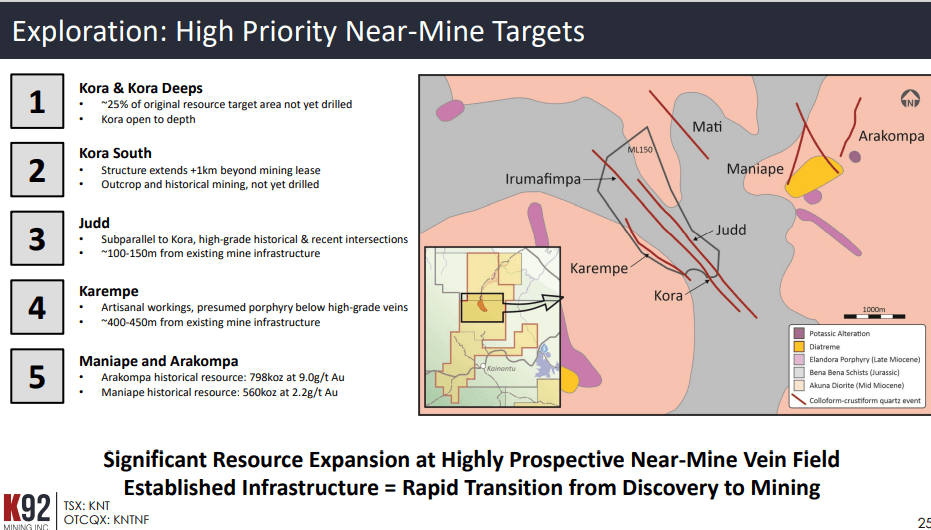

Underground they currently have 5 diamond drill rigs primarily drilling at Kora but also now at Judd. The rigs are focused on 2 things in Kora; the first is to increase the measured and indicated resource, which is part of completing the Feasibility Study on the next phase of expansion and the second is on expanding the resource, primarily to the South but also at depth. When you look at Kora and their drilling continuity, they have almost 100% hits and they release the results from every single hole onto the market.

Kora Deposit in Kainantu: Grades, Plans, & Goals

At Kora and at Judd, K92 is able to consistently achieve low-cost underground mining. Kora has 2 veins, K1 and K2 which average about 20-30m apart so the development underground access is 2 vein systems, each system averaging 3-6m wide, and overall, a resource grade, which is +10g/t. Access is relatively straightforward and is going into the side of a mountain, and actually going up into the deposit, rather than spiralling down, having to go deeper and deeper to get to the resource. They go along the strike, and currently have over 1,000m along strike, a 2-vein system, and over 1,000m vertically. So they have a very concentrated, 1,000m x 1,000m, plus or minus 1.1Moz measured and indicated. 3.7Moz inferred which combined is almost 5Moz and is expanding all the time.

The access is straightforward, geotechnically it is relatively easy mining. Then they recently drilled into Judd which is on the other side of their development, about 50m away from the access to Kora. So the all-in sustaining costs are very low because they now can access all 3 vein systems from just one main development and access routes.

Consistency of Results & Business Plan Development

K92 is constantly planning and developing new ideas. They brought out a PEA earlier in the year, which was to expand to 1Mt per annum. It showed an incredibly robust project and NPV5 of USD$1.5Bn, producing over 300,000oz/year initial 12-year life. That was before any drilling or development started at Judd.

Now at Judd, they have another underground rig coming in next quarter, so will have 6 rigs drilling underground plus the 5 they have on the surface. Kora is expanding to the South and the resource for Kora today would be larger than the current result because they've drilled many holes outside of that envelope of the results. They are looking, in the full Feasibility study, at a project which is probably larger than they allowed for. They have got the twin incline in with the 6x6 pushing 200m and the 5x5 20m behind it. They have a brand-new twin incline system committed to it which they have designed to allow up to 3Mt and perhaps beyond that as there is so much potential there.

Company Financials & Growth Potential

The numbers are great in the K92 quarterly results. They have a good cash position, no debt, and they have options in terms of how they move this forward. The company has significant commitment to capital next year as are committed to putting in the twin incline and opening up the mine. They are bringing in additional drills and setting up underground to continue to expand the resource.

Judd has started to come into the equation. They've also got surface drilling at Karempa, which is another parallel system only 400m away. And they have Blue Lake, which is their main porphyry target where they are drilling at the moment. They started the year with a capacity of 200,000t/pa and are closing the year with a capacity of 400,000t/pa. Next year will be the first year that they will do that 400,000t/pa and that's increased cash flow. The team is aiming for growth and expansion and they are coming out with their Feasibility Study of the next phase of expansion. They will continue to provide that information to the market, continue to drill, continue to deliver and provide the catalysts that the market wants to see.

Focus, Money Allocation, & Single-Asset Risks

A single asset company always has a degree of risk but they need to justify getting another asset and would it be as good as the first asset? The K92 asset has been recognized by PDAC, where they got the Thayer Lindsley Award in 2021 for the best Global discovery in 20 years. That recognition and what that's done for the company in terms of its market capitalisation, cash flow, etc, has provided an opportunity to be able to look for other assets. It is part of the business plan, to look for potential other assets which are accretive to the value of the company and provide opportunities to grow.

2020 Achievements: Could it Have Been Better?

Considering the challenges of this year with Covid-19 and its impact on the world and the mining industry, K92 have achieved such a lot which is a testament to their team of people. They have two great resources now and the team has managed to increase the production by 20% from the previous year despite the environment that they've had over the last 12-months. They completed an expansion and started the development of a twin incline while still generating cash which is a real testament to the team that is K92 Mining.

Scale of Opportunity: 2021 Focus, Plans, & Growth

2020 has been a good year for K92 and they must keep moving forward in 2021. They plan to continue production growth at a similar rate of 20%, which would be impressive. They plan to bring out their guidance in Q1/21, which is the first priority.

Secondly, they will come out with a new Resource, and that Resource, based on the drilling that they've done, looks to be expanding out from their current resource.

Importantly, K92 will have their first Feasibility Study and will be bringing out their first Reserves. There are plans for further exploration and decisions to be made on the drilling programme. So Kora is coming out and they have Judd and also Karempa which is another vein system which they haven’t started drilling yet but is known to have historical Resources.

The aim is for K92 Mining to be developed as a tier-1 asset, which means long Life of Mine (LOM), plus 300,000oz/pa and they believe there is potential to go significantly beyond 300,000oz. The results coming out now are showing that even with the current Feasibility Study, they could push the tonnage up by maybe 50%, which would see a commensurate increase in annual production. If they start to deliver on this, K92 would become an immediate take-over target. That could be very interesting for shareholders. But that said the management see the ability to create a very large cash-machine from these operations in PNG. Nice choices to have to make.

Looking at business development and M&A, K92 is actively looking at a number of opportunities and we would certainly like to see something come to fruition over the next 12-months. So whilst not a top priority because to the successes in PNG, lessons learnt with Centamin's woes in 2020, means that the management team is conscious of single asset risk (although they would argue that they have multiple assets) and single jurisdiction risk is important to mitigate against. They are primarily looking outside of PNG, possibly in Australia or North America. Target-wise they're looking for something that is significant in size to add value to the company which means that they are looking for something at production, or with the potential to produce +100,00oz/year.

K92 is an example of how to build a company well. It's been methodical and relentless. I suspect though that shareholders will want to understand the scale of the opportunity ahead, what the dividend plans are and the timing of an end game if there is one. One to keep an eye on in 2021.

To find out more, go to the K92 Mining website.

Analyst's Notes

Subscribe to Our Channel

Stay Informed