Why Precious Metals Producers Offer Asymmetric Upside in a Record-Breaking Rally

Gold at $4,400/oz creates margin expansion for producers with operational leverage and capital discipline execution drives valuation, not exploration upside.

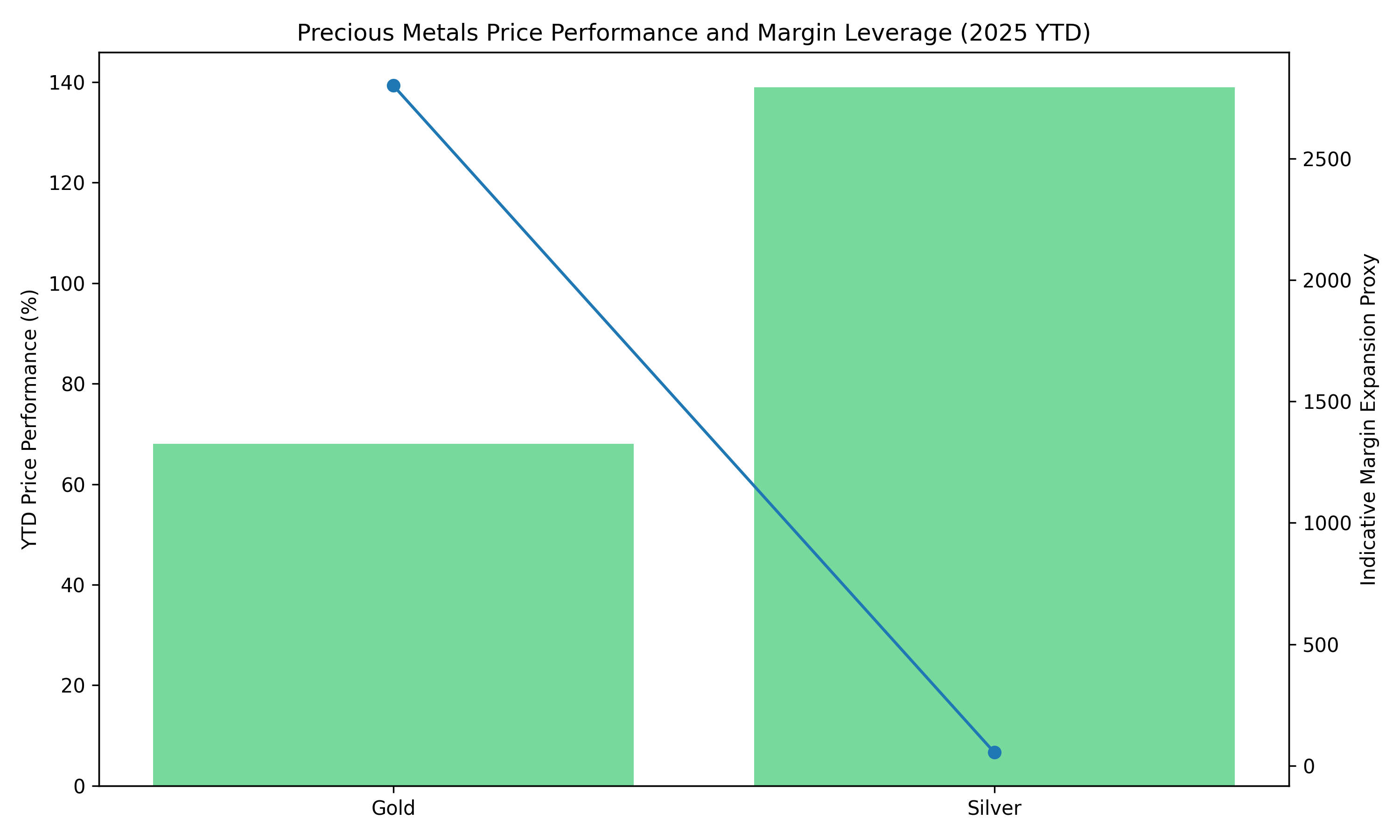

- Gold surpassed $4,400/oz and silver approached $80/oz in late 2025, representing YTD gains of 70% and 140% respectively, driven by monetary policy expectations and safe-haven demand amid geopolitical tensions.

- Investment flows via ETFs and central bank accumulation have replaced traditional jewelry demand as the dominant price drivers, creating sustained support levels despite high absolute prices and thinner end-of-year liquidity.

- Mid-tier and emerging producers with operational leverage, particularly those with declining AISC profiles, processing control, or near-term production growth, stand to capture disproportionate free cash flow at current price levels.

- The narrowing gold-silver ratio and silver's 139% YTD gain elevate the strategic value of silver-levered assets, particularly those with existing infrastructure and near-term production pathways in Nevada and other established jurisdictions.

- Valuation upside in the sector now depends on demonstrated operational delivery, margin expansion, and capital discipline rather than exploration upside alone, as producers and advanced developers with clear cash-flow visibility are structurally advantaged over early-stage stories.

The 2025 Price Surge & How Investors Can Position for Success

Precious metals have entered 2026 trading at historically unprecedented levels. Gold broke through $4,400 per ounce in late December 2025, marking a 68% year-to-date gain, while silver approached $70 per ounce with an even more dramatic 139% advance. The rally confirmed across institutional trading platforms, reflects a convergence of macroeconomic forces: expectations of looser U.S. monetary policy, a weakening dollar, sustained central bank demand, and geopolitical risk premiums that show no signs of abating.

For investors, the question is no longer whether precious metals remain investable at these levels but rather which companies and project types offer the most compelling risk-adjusted exposure. The answer lies not in exploration upside or resource scale alone, but in operational leverage, margin expansion, and demonstrated execution at a time when cash flow visibility commands premium valuations.

Global Trends: Macro Forces Driving Sustained Precious Metals Strength

The current precious metals rally is distinguished from prior cycles by the absence of crisis-level distress. Unlike the COVID-driven surge of 2020 or the financial crisis spike of 2011, the 2025 advance reflected anticipatory positioning rather than panic buying. Markets are pricing in multiple interest rate cuts by the U.S. Federal Reserve, a structural weakening of the dollar, and persistent geopolitical friction across multiple theatres.

Central banks remain net buyers of physical gold, reinforcing a price floor that traditional jewelry demand can no longer provide. Investment demand via exchange-traded funds has surged, with silver-focused products seeing particularly strong inflows. The narrowing gold-silver ratio indicates that silver is being re-priced not merely as an industrial metal but as a monetary asset with inflation-hedging characteristics.

Technical indicators suggest the rally has momentum behind it, though silver in particular shows overbought conditions that could introduce short-term volatility. End-of-year liquidity constraints amplify this risk, but the underlying structural drivers remain intact. For mining equities, this environment creates a tailwind, but not uniformly. Companies with high all-in sustaining costs, complex metallurgy, or permitting bottlenecks face margin compression despite higher prices. By contrast, producers with sub-peer costs, processing control, and near-term production growth profiles capture exponential free cash flow expansion.

Supply Challenges: Why Production Growth Lags Price Performance

One of the most underappreciated aspects of the current rally is the supply-side inertia in precious metals mining. Large-scale gold and silver projects face multi-year permitting timelines, capital intensity that deters speculative development, and jurisdictional risks that reduce the effective pool of investable projects. Even in mining-friendly jurisdictions like Nevada, Western Australia, and parts of Canada, project timelines from discovery to production average 10 to 15 years.

This dynamic creates a structural advantage for companies already in production or within 12 to 24 months of first gold. The processing bottleneck is particularly acute for refractory ores. Companies dependent on toll-milling arrangements face payability discounts and processing costs that absorb much of the margin uplift from higher gold prices. By contrast, companies with owned autoclaves or flotation circuits capture 90%+ recoveries and materially lower AISC profiles.

Silver presents its own supply challenges. Primary silver mines are rare; most silver is mined as a byproduct of base metals operations. The structural deficit in primary silver supply, combined with investment demand that now rivals industrial consumption, has driven the metal's outperformance. Companies with high silver credits benefit disproportionately, as silver byproduct revenue can reduce effective gold production costs to levels that provide margin expansion even at flat gold prices.

Company Case Studies: Eleven Distinct Paths to Value Creation

The investment case for precious metals equities depends on identifying companies where operational improvements, production ramps, or processing upgrades translate directly into free cash flow expansion. The following case studies illustrate how different development stages and jurisdictional contexts create distinct risk-return profiles.

Perseus Mining: Multi-Asset West African Producer with Balance Sheet Firepower

Perseus Mining operates three producing mines in West Africa delivering approximately 500,000 ounces per year at all-in sustaining costs below peer averages. The company recently upsized its corporate facility to $400 million, reflecting institutional confidence rather than financial stress. Combined with a net cash and bullion position exceeding $837 million, Perseus operates from a position of strategic excess liquidity. The Nyanzaga Gold Project in Tanzania, fully permitted and under construction, is forecast to produce over 200,000 ounces per year during peak years at costs that would make it the lowest-cost asset in the portfolio. First gold is targeted for early 2027. At current gold prices, Perseus' margins exceed $1,000 per ounce across the portfolio. The company's five-year outlook targets 515,000 to 535,000 ounces per year with minimal year-to-year volatility, with 93% of planned ounces backed by existing reserves. Shareholder returns via both dividends and share buybacks are funded from operating cash flow, not leverage, creating a sustainable capital allocation framework.

Lee-Anne de Bruin, Chief Financial Officer of Perseus Mining, said:

"With cash and undrawn debt capacity exceeding US$1.2 billion, Perseus is fully funded to deliver on our 5 Year Outlook and pursue future growth opportunities whilst maintaining our commitment to return funds to shareholders via ongoing dividends and share buy backs."

Valuation re-rating depends on continued delivery at existing operations, successful commissioning of Nyanzaga, and disciplined capital returns.

West Red Lake Gold: High-Grade Canadian Underground Ramp-Up

West Red Lake Gold operates the Madsen Mine in Ontario's Red Lake district, transitioning from restart credibility to operational delivery. The company recently upgraded to the OTCQX Best Market, improving liquidity access for U.S. institutional investors. The mine restarted following extensive infrastructure investment, with bulk sample programs demonstrating strong reconciliation between geological models and actual results. Gold recoveries average 95%, validating the processing circuit. Underground waste rock storage is now operational, reducing haulage bottlenecks, and a shaft skipping project is advancing to lower unit costs further. Definition drilling over 150,000 meters has tightened drill spacing from 20 meters to 7 meters, addressing continuity risk and enabling larger mining complexes. The Pre-Feasibility Study outlines a post-tax NPV of approximately C$496 million with diluted head grades around 8 grams per tonne gold. At current gold prices, Madsen's economics improve materially. The Rowan Project, located 80 kilometers from Madsen, offers toll-milling optionality that could support a combined development pathway without duplicating processing infrastructure.

Shane Williams, President & Chief Executive Officer of West Red Lake Gold, stated:

"Graduating to the OTCQX Best Market represents an important milestone for West Red Lake Gold as we continue to execute on the restart of the Madsen Mine. This upgrade improves our visibility and accessibility to U.S. investors at a time when we are focused on delivering operational results and advancing initiatives designed to enhance long-term value."

Serabi Gold: Cash-Flow-Funded Organic Growth in Brazil

Serabi Gold represents an established mid-tier producer with a 20-year operating record in Brazil, transitioning from single-asset reliance to multi-asset platform. The company operates the Palito underground mine, which delivers consistent 30,000 to 40,000 ounces per year with demonstrated resource replacement. The Coringa underground mine, under development with less than $10 million in initial capital, is designed to lift group production toward 60,000 ounces per year by 2026. Ore sorting at Coringa upgrades sub-2 g/t feed to double-digit grades by rejecting over 90% of waste material before transport. This technology unlocks transport economics, preserves Palito mill capacity, and reduces AISC without facility expansion. An updated Preliminary Economic Assessment at Coringa confirms robust margins at conservative gold prices and meaningful free cash flow generation. All growth plans are organically funded from operating cash flow, with minimal debt at the corporate level and no reliance on equity dilution to achieve stated production targets.

Mike Hodgson, CEO of Serabi Gold, said:

"2024 was a highly successful year for Serabi with many milestones achieved. These include a 13% increase in annual gold production, permitting progress at Coringa with the renewal for three years of the trial mining permit, the successful build and commissioning of the Coringa classification plant out of cashflow, whilst ending the year with a healthy cash position."

At current gold prices, Serabi's margin expansion from ore sorting creates disproportionate cash flow upside.

Hycroft Mining: Large-Scale Nevada Silver Optionality with Grade Enhancement

Hycroft Mining controls a large-scale gold-silver development asset in Nevada with significant existing infrastructure. Recent drilling at the Vortex silver system returned thick intervals with materially higher silver grades than the global resource average, including localized zones of very high-grade silver with visible silver in core. The Vortex results represent a potential quality upgrade within a very large system, demonstrating continuity sufficient to justify follow-up drilling but not yet mine design. Hycroft's existing resource base is very large but low-grade on average. Even modest volumes of higher-grade material can improve early cash-flow profiles, enhance project IRR, and reduce effective capital payback periods. Ongoing metallurgical work shows improved and more consistent gold and silver recoveries via flotation and pressure oxidation, with reduced variability across domains.

Diane R. Garrett, President and Chief Executive Officer of Hycroft Mining, stated:

"The Vortex drilling results continue to demonstrate the presence of materially higher-grade silver mineralization within the broader Hycroft system, including zones of visible silver. These results confirm that Vortex represents a meaningful opportunity to enhance the quality of the existing resource base and warrants continued follow-up work."

At current silver prices approaching $70 per ounce, the economic sensitivity of high-grade silver zones increases materially. Silver's 139% year-to-date gain elevates the strategic value of assets with significant silver inventory, particularly when processing decisions favor selective mining of high-grade domains over bulk-tonnage scenarios. Hycroft's strong cash position and lack of debt provide flexibility to advance studies methodically without liquidity pressure.

i-80 Gold: Nevada Multi-Asset Platform with Processing Control Strategy

i-80 Gold is transitioning from single-asset ramp-up to multi-asset development across five core Nevada assets split between high-grade underground refractory projects and large-scale oxide open pits. The company's central processing hub autoclave is designed to improve recoveries and payability, lower long-term unit costs, and reduce reliance on third-party processors. The underground resource base features high grades around 8 to 10 g/t Au with strong continuity, while the open-pit resource base offers large tonnage, lower grade, and long mine lives. Until in-house processing is available, toll-milling economics cap margins, as payability and processing costs remain the main constraint on free cash flow. The autoclave refurbishment is expected to deliver recovery uplift from 55 to 60% payability to 90%+ recoveries, materially reducing AISC across underground assets. The company has raised significant equity to stabilize the balance sheet and fund near-term work, with remaining priorities including addressing convertible debt maturities and eliminating metal prepay obligations. The autoclave is the fulcrum: economics, margins, and credibility hinge on successful processing control.

Richard Young, President and Chief Executive Officer of i-80 Gold, stated:

"The refurbishment of the Lone Tree autoclave is a transformational step for i-80 Gold. Having our own processing facility is expected to significantly improve recoveries and payability for our refractory ore, reduce unit costs, and unlock the full value of our high-grade underground assets that are currently constrained by toll-milling economics."

New Found Gold: Infill Drilling De-Risking at Queensway

New Found Gold is transitioning from discovery narrative to development discipline at its Queensway project, an orogenic gold system hosted along a major fault corridor extending over 100 km in Newfoundland. Current development focus concentrates within a defined core corridor rather than district-wide exploration, with mining concepts assuming shallow, high-grade open pit transitioning to underground. The infill drilling program is designed to reduce drill spacing within the core resource area, improving confidence in grade continuity, geometry of mineralized shoots, and structural controls influencing mining dilution. Results confirm internal continuity within known zones, with high-grade mineralization persisting at tighter spacings, supporting reduced geological risk and lower grade-smearing risk in future mine plans. Infill data supports conversion of Inferred material toward Indicated categories and more reliable input parameters for economic studies. This represents a quality upgrade, not a quantity expansion.

Melissa Render, President of New Found Gold, stated:

"We are pleased to report these results from infill drilling of Phase I and II open pits at Monte Carlo. Overall, we see consistency with past drilling, indicating good continuity of gold mineralization in this proposed open pit. Select holes from 2025 drilling have returned higher grade intervals than in the initial mineral resource estimate block model. We look forward to integrating these results into the updated Queensway mineral resource currently planned for H1/26."

U.S. Gold Corp: Permitted Wyoming Development Project

U.S. Gold Corp is transitioning from permitted asset to construction-ready project with its CK Gold Project in Wyoming. The project is fully permitted at the state level with no federal permitting dependency, with updated Pre-Feasibility Study completed under SEC S-K 1300 standards. Advanced engineering and trade-off studies are underway, moving toward a final feasibility study. The project is designed as a 110 koz/year gold-equivalent producer with 10-year initial mine life and expansion potential, structured as an open-pit, conventional truck-shovel operation with dry-stack tailings. Strong margins exist across a wide commodity price range due to gold-copper by-product credits, with after-tax NPV and IRR remaining robust even at conservative price assumptions and short payback period of two years or less in base cases. Located on State of Wyoming land with Approved Mine Operating Permit, Industrial Siting Permit, and water agreements in place, the project benefits from proximity to infrastructure, rail, power, labor, and services.

Luke Norman, Chairman and Chief Executive Officer of U.S. Gold Corp, stated:

"CK Gold is a fully permitted project at the state level with no federal permits required, and we are advancing engineering and technical studies as we move toward a construction decision. With strong economics, copper by-product credits and infrastructure already in place, CK Gold is positioned as a compelling, near-term development project in a top-tier U.S. jurisdiction."

Tudor Gold: Golden Triangle Scale-to-Economics Transition

Tudor Gold controls a large-scale gold-copper-silver project in British Columbia's Golden Triangle, undergoing strategic transition from resource scale validation to economic optionality. The company increased project ownership to 80% in 2025, simplifying decision-making and long-term development pathways. The 2024 resource update confirmed approximately 27.9 Moz AuEq Indicated and 6.0 Moz AuEq Inferred, with resources remaining open in multiple directions and at depth. The 2026 strategy explicitly targets higher-grade subsets within the bulk-tonnage system to provide early-stage development optionality and technical inputs required for a future PEA. The SC-1 Zone is identified as a high-grade gold zone within the broader Treaty Creek system, with visible gold within quartz stockwork. The 2026 plan prioritizes underground exploration to define continuity, assess underground mining potential, and determine if SC-1 can meaningfully impact early project economics.

Ken Konkin, President and Chief Executive Officer of Tudor Gold, stated:

"Our 2026 strategy is focused on advancing Treaty Creek toward economic studies by prioritizing higher-grade opportunities within the broader system. The identification of the SC-1 Zone as a high-grade gold domain provides us with the opportunity to evaluate underground development scenarios that could meaningfully impact the project's economics, while continuing to preserve the scale optionality of the overall resource."

P2 Gold: PEA-Stage Nevada Gold-Copper Developer

P2 Gold is advancing the Gabbs Project in Nevada, a PEA-stage gold-copper development project. Recent option grants represent standard equity-based compensation used to retain technical and executive talent and align management incentives with long-term equity value, typical for companies transitioning from PEA to feasibility stage where execution intensity increases. Options granted under the company's existing equity incentive plan with exercise prices set at or above prevailing market levels at grant date and vesting structure designed to reward time-based and performance-linked execution. The updated 2025 PEA outlines large-scale, long-life gold-copper operation with strong after-tax NPV and IRR at conservative price assumptions, with SART-based copper recovery as a key economic lever.

Joe Ovsenek, President & Chief Executive Officer of P2 Gold, stated:

"The Company is "advancing the PEA-stage, gold-copper Gabbs Project in Nevada to production with a focus on feasibility-level studies, metallurgy optimization, and disciplined capital progression."

Cabral Gold: Fully-Funded Brazilian Oxide Starter with District Upside

Cabral Gold operates a district-scale gold project in northern Brazil combining near-term production with large exploration upside through its fully funded Stage 1 gold-in-oxide starter operation under construction at the Cuiú Cuiú project. Located within a prolific Brazilian gold province with historical production exceeding 30 Moz from placer activity, the project sits along a major regional structural corridor controlling multiple known deposits. The company holds NI 43-101 resources totaling approximately 450 koz gold indicated and 455 koz gold inferred in primary hard rock, plus 216 koz gold indicated and 71 koz gold inferred in oxide material distributed across multiple deposits. Stage 1 targets five near-surface gold-in-oxide blankets within 60 meters of surface requiring no drill and blast, no crushing or grinding, and amenable to heap leach processing. The heap leach operation with 3,000 tpd capacity targets 88% average gold recovery over a 6.2-year mine life, producing approximately 113 koz gold life-of-mine at 25 koz per year initially with AISC of approximately $1,210 per ounce. Stage 1 economics show 78% after-tax IRR, $74 million NPV at 5% discount, $37.7 million initial capex, and 10-month payback period. The company closed a $45 million gold-linked loan in November 2025 that fully funds Stage 1 construction, with first gold pour targeted for Q4 2026. Three drill rigs remain active across priority targets, with long-term objective to expand the global resource base beyond 2 Moz. Near-term cash flow provides funding for district-scale exploration, reducing reliance on equity markets during resource expansion and creating optionality for Stage 2 expansion and larger-scale hard-rock development.

Alan Carter, President and Chief Executive Officer of Cabral Gold, stated:

"Construction of the Stage 1 oxide operation at Cuiú Cuiú is progressing on schedule and on budget, supported by the recently completed gold-linked loan facility. With first gold targeted for Q4 2026, this starter operation is designed to generate early cash flow while preserving significant upside through continued district-scale exploration across the broader Cuiú Cuiú project."

Integra Resources: Great Basin Producer Transitioning to Multi-Asset Platform

Integra Resources is transitioning from developer to producer with a three-asset portfolio located entirely in tier-one U.S. jurisdictions, structured to support sequenced growth rather than parallel dilution. The company operates a conventional open-pit heap leach operation as its producing asset, generating operating cash flow that now anchors portfolio advancement. Recent balance-sheet action eliminated all corporate-level debt through full conversion and repayment of a convertible debenture facility, with conversion retiring the entire drawn principal and accrued interest settled in cash. This debt elimination removes overhang on equity valuation, simplifies financial disclosures, and improves flexibility heading into permitting and development phases at advanced-stage assets. The development pipeline includes an advanced heap-leach project in a past-producing district with substantial measured and indicated resources, where recent engineering and stockpile work increases mine life, operational flexibility, and potential capital efficiency. A secondary development asset with preliminary economic study outlining long-life, low-complexity heap-leach operation provides future growth optionality without immediate capital draw. Current cost structure at the producing asset reflects capital-intensive reinvestment phase tied to waste stripping catch-up, mobile fleet renewal, and heap leach pad expansion, with optimization work ongoing and feeding into future technical updates. The company's strategic objective is building a multi-decade Great Basin platform rather than single-cycle mine, with aggregate resource base measured in multiple millions of gold-equivalent ounces distributed across three assets to reduce single-project risk. Capital structure now aligns with cash-flow-funded growth and selective, disciplined capital allocation, with all assets benefiting from mining-established jurisdictions and federal and state-level initiatives aimed at accelerating domestic mineral development.

George Salamis, President, CEO and Director of Integra Resources, stated:

"This transaction also materially strengthens our financial position by eliminating the convertible debt from our balance sheet, leaving Integra debt-free at the corporate level as we move forward into permitting and future development at DeLamar."

The Investment Thesis for Precious Metals Producers

- Companies with declining AISC profiles, processing control, and visible production growth capture exponential free cash flow expansion at current prices. Resource ounces without clear mine plans offer limited near-term valuation support.

- Producers and advanced developers funding growth organically from operating cash flow, with minimal equity dilution, offer superior risk-adjusted returns compared to companies dependent on external financing during volatile equity markets.

- The narrowing gold-silver ratio and silver's 139% YTD gain create disproportionate upside for producers with high silver credits or silver-dominant projects, particularly those with existing infrastructure in Nevada and established mining jurisdictions.

- High-grade drill intercepts without processing pathways, permitting clarity, or mine-plan integration offer optionality but not certainty. Valuation re-rating depends on demonstrated conversion of geology into economics through feasibility studies and construction decisions.

- At record metal prices, the primary differentiator between outperforming and underperforming equities is operational execution. Companies demonstrating sustained production delivery, cost control, and reconciliation performance command premium valuations regardless of jurisdiction or commodity mix.

- If gold sustains above $4,000/oz and silver above $60/oz, allocate 60 to 70% to producing companies with sub-peer costs and capital return frameworks, 20 to 30% to advanced developers within 18 months of production, and 5 to 10% to high-conviction exploration stories with clear processing pathways and permitting momentum.

The precious metals rally of 2025 is distinguished by structural demand, monetary policy expectations, and safe-haven positioning that show no signs of abating. For mining equities, this environment creates asymmetric upside, but only for companies with operational leverage, processing control, and capital discipline. Resource scale alone does not drive re-rating; execution, margin expansion, and free cash flow visibility determine valuation outcomes.

Investors should focus on producers and advanced developers capable of demonstrating sustained operational delivery, declining unit costs, and organic growth funded from operating cash flow. Silver's outperformance creates tactical opportunities in Nevada-based projects with existing infrastructure. Long-dated exploration stories without processing certainty or permitting clarity offer limited near-term value despite high metal prices.

TL;DR

Gold and silver reached record levels in late 2025, with year-to-date gains of 68% and 139% respectively, driven by monetary policy expectations, dollar weakness, and safe-haven demand. Investment flows via ETFs and central bank buying have replaced traditional jewelry demand as primary price drivers. For mining equities, valuation upside depends on operational leverage rather than resource scale. Producers with sub-peer costs, processing control, and visible production growth capture exponential free cash flow expansion at current price levels. Silver's outperformance creates tactical opportunities in Nevada-based projects with existing infrastructure. Companies demonstrating sustained operational delivery, declining unit costs, and organic growth funded from cash flow command premium valuations, while resource scale and exploration upside alone offer limited near-term re-rating potential without processing certainty and execution milestones.

FAQs (AI-Generated)

Gold reached $4,474 per ounce in December 2025 due to expectations of further U.S. Federal Reserve interest rate cuts, a weakening dollar, sustained central bank accumulation, and safe-haven demand driven by geopolitical tensions.

Producers with operational leverage through declining all-in sustaining costs (AISC), owned processing facilities like autoclaves or flotation circuits, and visible production growth capture exponential free cash flow expansion at current gold prices.

Valuation depends on operational execution rather than gold price levels, with companies demonstrating sustained production delivery, declining unit costs, and capital discipline commanding premium valuations while those with execution risk or capital intensity trade at discounts.

Allocate 60 to 70% to producing gold companies with sub-peer AISC and demonstrated capital return frameworks, 20 to 30% to advanced developers within 18 months of production with financing clarity, and 5 to 10% to high-conviction exploration stories with clear processing pathways.

Execution risk dominates commodity price sensitivity through ramp-up challenges, cost inflation during construction, permitting delays, reconciliation failures, complex metallurgy, capital structure risks, and potential dilutive financing that can offset margin expansion from higher gold prices.

Analyst's Notes

Subscribe to Our Channel

Stay Informed