Kodiak Copper Eyes Significant Resource Increase as M&A Wave Reaches Explorers

With 440Mt maiden resource in hand, Kodiak Copper targets aggressive expansion drilling in 2026 as Hudbay's Arizona Sonoran deal sets new valuation bar for sector.

When Hudbay Minerals paid a 30% premium for Arizona Sonoran Copper earlier this month, it marked the first significant takeover of a non-producing copper company in the current cycle. For Claudia Tornquist, the timing couldn't be better.

The Kodiak Copper CEO had just released her company's maiden resource estimate in December - 440 million tons containing 2.4 billion pounds of copper and 1.7 million ounces of gold at the MPD project in southern British Columbia. Now she's watching the market reset its expectations for what explorers with scale potential might be worth. Tornquist said during the PDAC conference in Toronto,

"What the market wants from us and what potential acquirers want to see is really the scale potential. If we can show that ... it will add significant value because that then brings us into the region where many of our more advanced peers are."

Those peers - Osisko Metals, Faraday Copper, Northisle - carry market caps between $412 million and $1.3 billion. Kodiak trades at $ ~72 million. The gap isn't subtle, and closing it depends almost entirely on what happens with the drill bit this year.

The Infill Opportunity

Unlike most exploration stories that lean heavily on blue-sky discovery potential, Kodiak's near-term growth pathway is refreshingly straightforward. The maiden resource incorporated roughly 70,000 meters of historical drilling completed by various operators over decades - exploratory work aimed at figuring out what existed rather than systematically defining it.

That leaves gaps. Lots of them.

Where previous operators drilled sporadically across seven zones spanning a 40-kilometer north-south trend, Kodiak now has a consolidated land package and a clear target: fill the spaces between known mineralisation. The company expects to announce detailed 2026 drill plans shortly, with the bulk of meterage aimed at resource expansion through infill work, plus testing on high-priority extensions and select targets from the roughly 20 additional zones identified across the 357-square-kilometer property.

An updated resource incorporating this year's drilling should land in Q1 2027. The size of resource growth achieved by the drill bit will determine how quickly Kodiak narrows that valuation gap.

The metallurgy, at least, isn't a concern. Testing confirmed the mineralization responds to conventional flotation processing with copper recoveries reaching 89.9% and concentrate grades exceeding 26%. Gold grades in the concentrate range between 6.2 and 16.9 grams per ton - meaningful byproduct credits that improve project economics.

Interview with Claudia Tornquist, President and CEO & Christopher Taylor, Chairman of Kodiak Copper

Why Majors Are Moving Earlier

Christopher Taylor, Kodiak's founder and chairman, has seen this movie before. His previous company, Great Bear Resources, was acquired by Kinross Gold for $1.8 billion after making a district-scale gold discovery in Ontario. He knows what strategic buyers look for, and he knows the timing of approaches matters.

The Hudbay premium - right around 30% - sits in the range that boards find difficult to ignore. But Taylor also understands that majors don't pay for potential alone. They pay for de-risked tonnage in jurisdictions where mines actually get built.

British Columbia checks those boxes. MPD sits in the established Quesnel terrane mining belt near operating mines including Copper Mountain and Highland Valley Copper. Year-round access via paved highways, existing road networks on the property, grid power that's 98% renewable, water, and a skilled workforce in nearby Merritt and Princeton all reduce development risk and capital intensity.

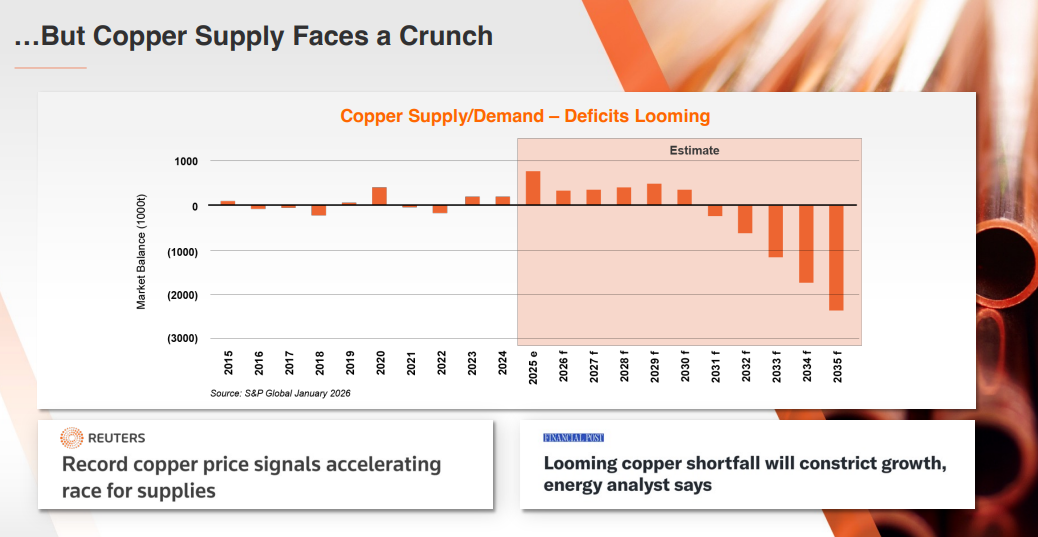

More broadly, the copper market is tightening in ways that make development-stage assets increasingly strategic. Existing mines are depleting faster than new discoveries replace them. S&P Global projects supply deficits reaching 2 million tons annually by the mid-2030s. Meanwhile, electrification, EV adoption, and the power demands of AI data centers are accelerating consumption - the International Energy Agency estimates data centers alone could add 5 million tons of demand by 2030.

Majors have acknowledged publicly on earnings calls that they need to expand their copper pipelines. That means moving earlier in the development cycle, accepting higher risk in exchange for securing future supply. Arizona Sonoran proved they're willing to pay for it.

Capital Structure and What Comes Next

Kodiak has kept dilution relatively modest despite consolidating a district and completing more than 90,000 meters of drilling - $56 million raised to date with 96.6 million shares outstanding. The largest shareholder is Swiss resource fund Konwave at just under 10%, with institutions and family offices holding more than half the register.

Tornquist noted increasing interest from generalist investors newly entering the resource sector, a migration that typically accompanies companies transitioning from pure exploration toward development. That trend should accelerate as the resource grows and economic studies come into view.

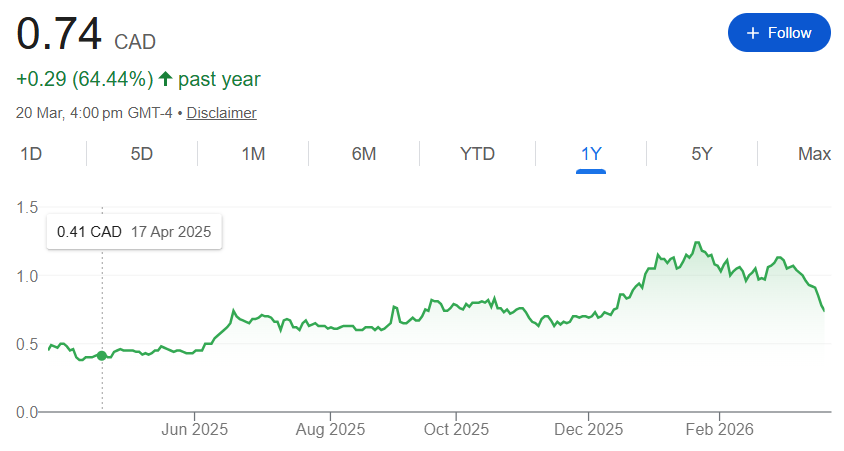

The share price has cooperated - up more than 64% over the past year - though the real test arrives when drill results start flowing in Q2 and continue through year-end.

Near-term milestones include drill target announcements and soil sampling results in Q1, additional metallurgical data and the start of resource expansion drilling in Q2, and exploration results from the additional targets rolling out from Q3 onward. It's an aggressive schedule, but the infill nature of much of the work reduces execution risk compared to pure grassroots exploration.

Scale First, Economics Later

The decision to prioritise resource growth over advancing economic studies reflects both market realities and strategic positioning. Investors and potential acquirers want to see multi-decade mining potential before committing capital or paying premiums. Demonstrating that MPD can support large-scale, long-life production establishes negotiating leverage whether Kodiak ultimately develops the project itself or becomes an acquisition target.

Taylor, drawing on his Imperial Metals experience at the Mount Polley mine, noted that alkalic porphyry systems in British Columbia have a habit of getting bigger over time. Thirty years after initial development, companies are still drilling discoveries at Mount Polley. Nobody's found the bottom of a porphyry system yet.

For Kodiak, first comes proving their 440 million tons can meaningfully expand. If the infill drilling delivers and the 2026 program adds the tonnage management expects, the company enters 2027 with a fundamentally different profile - and potentially a market cap that reflects it. In a sector where majors are paying 30% premiums for supply security, that matters more than ever.

Analyst's Notes

Subscribe to Our Channel

Stay Informed