Marimaca Copper (TSX-V: MARI) - Understanding Copper Investment Fundamentals

Interview with Hayden Locke, President & CEO of Marimaca Copper Corp. (TSX: MARI)

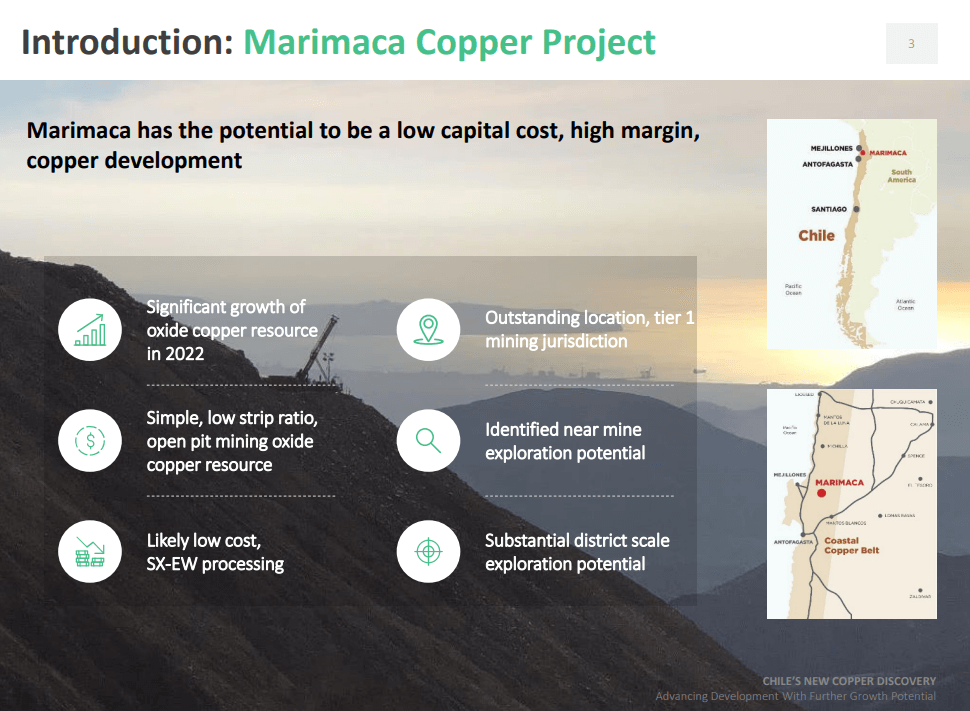

Marimaca Copper Corp. is a Canadian copper exploration company focused on exploring and developing new copper resources to supply an increasing global demand for this essential commodity. The company's flagship asset is the Marimaca Copper Project in Chile's Antofagasta region. It is the only copper discovery made globally within the last five years. It is a low-risk project that offers substantial exploration potential.

Matt Gordon caught up with Hayden Locke, President, and CEO, Marimaca Copper. Hayden has extensive experience as a mining executive with a significant part of his career spent in the development and leadership of successful LSE and ASX-listed mining companies. He has previously worked with J.P Morgan and Barclays Natural Resource Investments. As of 2018, he has served as the CEO at Emmerson Plc, a Morocco-based potash development company where he currently holds the Director position.

Company Overview

Marimaca Copper (formerly known as Coro Mining Corp.) is a copper exploration and development company. It was founded in 2004 and is headquartered in Canada. The company is listed on the Toronto Stock Exchange (TSX-V: MARI). Compañía Minera Cielo Azul Ltda, Minera San Jorge S.A., Minera Coro Chile Limitada, Minera Rayrock Ltda., Machair Investment Ltd., Rising Star Copper Limited, and Sea To Sky Holdings Ltd. are the company's subsidiaries. The Marimaca Project has been one of the most important copper oxide discoveries in northern Chile for over a decade. The company believes that it has the potential to be one of the best open-pit copper oxide projects globally.

The Market Landscape

Marimaca Copper is developing the Marimaca oxide project. The company recently put out a big resource upgrade. Commodities is a highly cyclical business where investors need to be contrarian. While people can still make money by way of the market's momentum, the best money is made by assuming that the pendulum will swing back at some point. Coal is one such commodity where 12-24 months ago, investors would have made exceptional money, but now, it is perceived as a dirty word due to its inefficiency and potential for harming the environment. Lithium has observed huge gains in the market over the last 2 years, and Copper is currently sitting in a similar position.

According to the company, the real challenge is to successfully take a contrarian view, picking the best assets, especially for resources. One such example is Papillon Resources. The company made an exceptional discovery in Mali, West Africa, delivering a huge resource. Shortly after the discovery, the gold price tanked, which was followed by two coups in Mali, causing the share price to drop from $2.50 to $0.50 in a very short timeframe. As per Papillon Resources’ Chairman, the best projects always bubble to the surface. Somebody will always want to own the asset at some point, and one needs to be patient. Investors should focus on identifying such projects.

While the gold price was able to recover up to mid $1s, it didn’t bounce back. Eventually, Papillon’s project was acquired by B2Gold. The investors who held the transaction would have made money in multiples over the following 7-year period, an exceptional result for long-term holders. People need to think long-term when it comes to investments.

Marimaca Copper’s asset is based in a good jurisdiction, but that isn’t always the biggest driver of the investment thesis. While the grade is considered king in projects, investors also need to consider other aspects such as the strip ratio relative to the grade and metallurgical recovery along with the associated costs and the return on invested capital. There needs to be a margin of safety. A 20%+ IRR (Internal Rate of Return) in a reasonable commodity price is a good starting point to screen decent projects. If all these boxes are ticked, the projects are worth looking into, and when the opportunity presents itself, investors should have the courage to pursue it.

An investor should also research the company’s management team as there’s often a lot of variability. One needs to look for a management team that is executing a strategy in order to create shareholder value. The management should be focused on minimising dilution and managing money efficiently during difficult conditions, raising capital at opportune times with limited dilution.

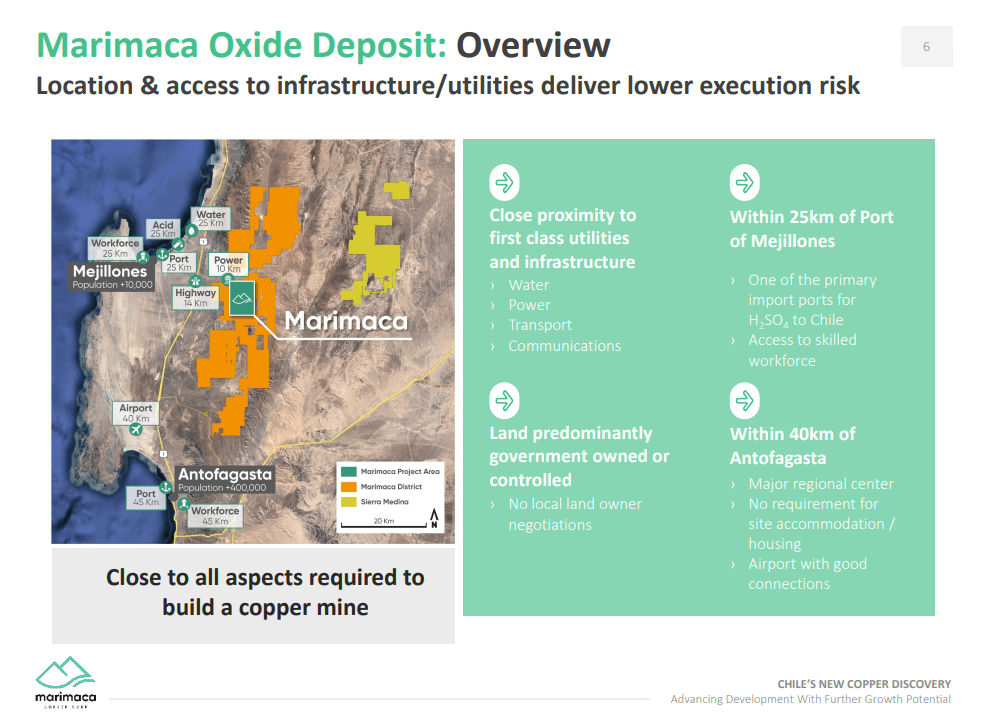

The project’s jurisdiction also makes a huge difference, especially when it comes to acquiring permits across the board. It is also important to have a thorough understanding of the environment for a specific project because it can vary across assets. Every project is different and there are nuances that need to be considered. This helps identify good projects from bad ones because while things may look good on paper, some projects may have challenging operational conditions that could make it harder to realise their value.

For most investors, crystallising losses is one of the most challenging things to execute. Investors should constantly reassess projects based on new information, taking into consideration the long-term ramifications. They should be willing to invest and wait for the pendulum to swing in their favour. In copper, the thesis remains relatively unchanged. While the global inflation was unforeseen, in the long term, copper continues to provide an exciting opportunity to make really good money.

Copper Investment Fundamentals

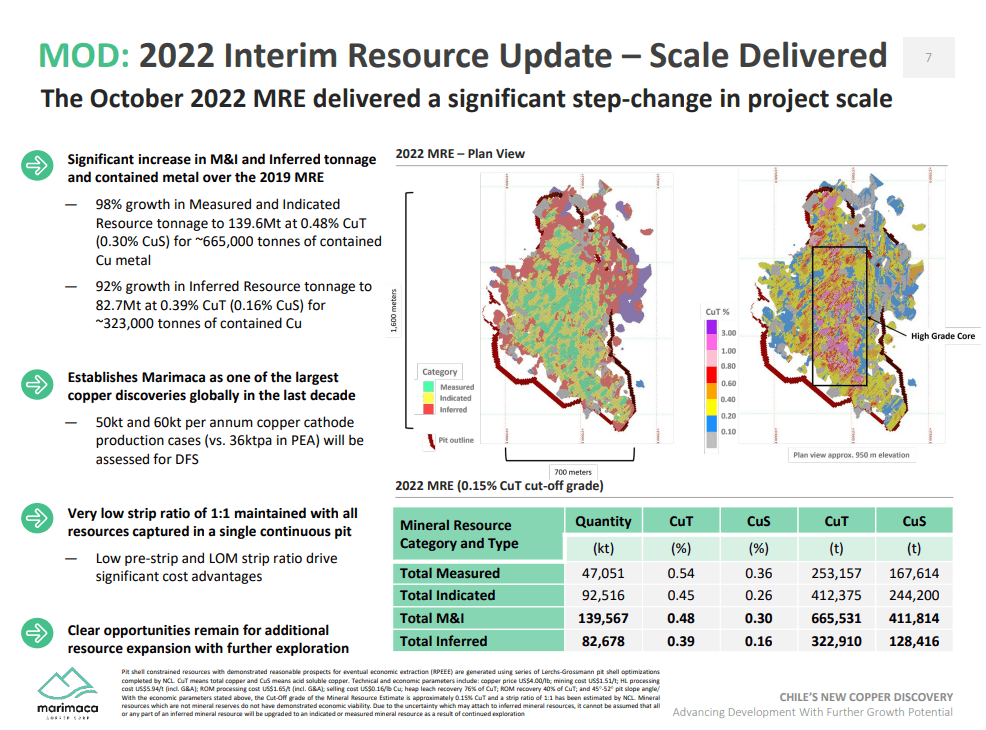

Marimaca Copper has delivered substantial value in the last 2 years. During this time, the company’s share price has remained quite steady. It did have an uptick early on in the ride, but it’s largely remained consistent within the price range. It has added significant value in terms of de-risking from a technical perspective along with a resource upgrade that led to a 65%-75% increase in contained metal tons. The company is looking to further increase the scale of the project and bring forward cash flows. It has achieved between 50%-60% increase in project value with no share price movement. The company is cognizant of the structural constraints that make it potentially challenging for large institutions to consider an acquisition. The company intends to address this in future capital raises.

Despite de-risking the project and adding incremental value, the company anticipates that it has yet to be rewarded for its efforts. This seems to be a widespread trend within the copper space as the company isn’t the only one facing this issue.

The Marimaca Copper Project has a relatively short timeline for production, which is fairly unique in terms of development-stage copper projects. Since the project is easy to finance as a standalone company, it offers much lower risk in virtually every aspect when compared to the vast majority of its peers. In its current position, the company isn’t looking to gain exposure to any other development-stage projects.

From a producer’s perspective, the company is highly focused on the commodity price. However, higher-costs projects can be tricky to navigate and the way reporting is done can vary significantly. One such instance is Atalaya Mining, which has a high AISC project (All-in Sustaining Costs), which offers an accurate AISC outlook than most other companies in the space. This results in much higher confidence in the cash flow that Atalaya Mining is looking to deliver. It is a company with high operating leverage to a change in the copper price environment.

In Chile, Capstone Copper has come off significantly from its highs. As per Marimaca Copper, the ideal investment strategy would be to buy all the majors including First Quantum, that have done exceptionally well over the last 2 years. Companies with very strong management teams and high operating leverage to the commodity prices are preferred for potential investments.

According to Marimaca Copper, it’s very difficult to time the market. It put out a resource, however, the market didn’t react. The company is well-funded, and it intends to keep delivering news flow while continually de-risking the project because the pendulum will eventually swing back in its favour at some point. It is positioning itself to get the project off the ground once the markets turn. The company is in a unique position where it does not need a significant copper price to finance the project or to incentivize investors to come in. While the company would prefer higher prices, the project will be built regardless of the copper pricing environment. The company intends to build the project as quickly as possible.

While there’s a lot of talk in the markets about the impact of EVs (Electric Vehicles), the quantity or the percentage of the demand that is coming from the decarbonizing world isn’t that significant when compared to the old-world economic drivers of copper. There is genuine fear across the board with respect to the rising interest rates and the fight against inflation that will have a significant impact on global economic growth. This, in turn, would affect the old economy's demand for copper. Furthermore, the Russia-Ukraine crisis has also raised supply concerns. There’s already a huge rightness of supply. The ban on Russian copper exports is expected to have a knock-on impact on global trade. The market has only 3-4 days of physical copper inventory available, which is highly concerning.

At the same time, Codelco has set a premium for delivering the grade-A cathode which is currently at an all-time high. There’s also an Austrian company that is pricing low-carbon copper. The company is talking nearly a $300 premium or roughly 3%-4% on today’s copper price premium for low-carbon copper. This serves as an indicator for future market conditions when the de-carbonization takes hold and the investments start to take off.

Hayden Lock, Marimaca Copper’s CEO is in Chile working on the planning phase for the permit applications. It’s a high-risk prospect that offers significant potential for value addition. All the associated parties will be meeting tomorrow to go over the operational strategy, allocation of responsibilities, and delivery timelines.

To find out more, go to the Marimaca website

Analyst's Notes

Subscribe to Our Channel

Stay Informed