Rising Oil Prices & 5% Treasury Yields Are Breaking the Traditional 60/40 Portfolio

Treasury yields above 5% are breaking the traditional bond hedge as inflation persistence pressures industrials, metals, and long-duration portfolios.

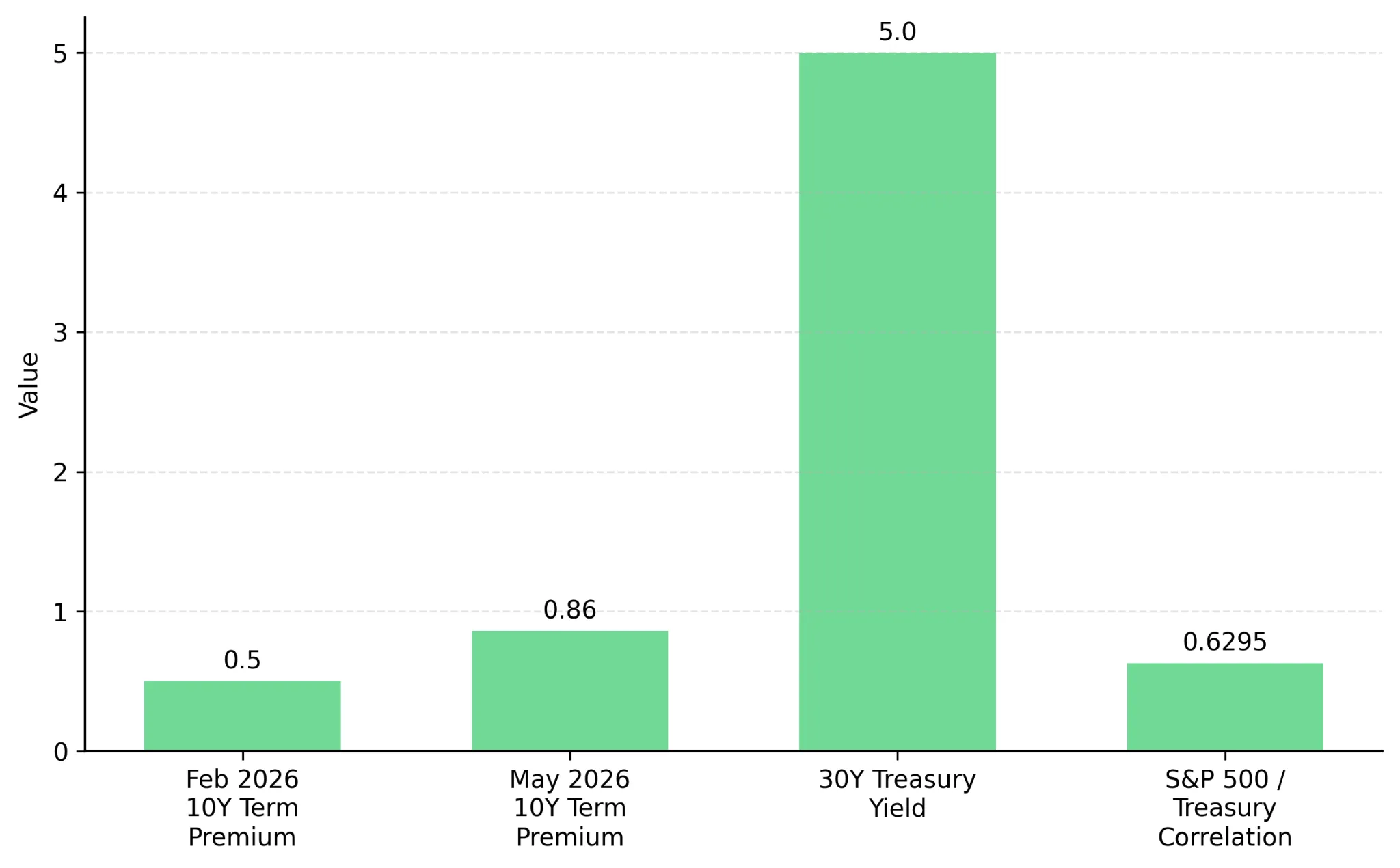

- The 30-year US Treasury yield rose above 5% on May 28, 2026 while the 60-day correlation between the S&P 500 and Treasury returns reached 0.6295, its highest level in more than 20 years.

- Spot silver fell 3.7% to $72.13/oz while front-month silver futures settled at $72.16 as industrial demand concerns outweighed safe-haven buying after oil prices jumped more than 2%.

- The 10-year Treasury term premium rose to 0.86% in May from below 0.50% in February as investors demanded higher compensation for holding long-duration bonds during elevated inflation periods.

- Brent crude above $95/barrel for 10 consecutive trading sessions would support defense and energy infrastructure equities while pressuring airlines, transport firms, chemicals manufacturers, and cyclical industries through Q3 2026.

- Demand for long-duration bonds could recover and pressure on cyclical industrial equities could ease if US core inflation falls below 3.3% year-over-year and the 30-year Treasury yield drops below 5%.

Higher Oil Prices Are Pressuring Growth Stocks & Long-Duration Bonds

Oil prices rose more than 2% on May 28, 2026 after renewed US-Iran military escalation pushed investors out of long-duration assets and into inflation hedges. Higher oil prices pushed the 30-year US Treasury yield above 5% while spot silver fell 3.7% to $72.13/oz and front-month silver futures settled at $72.16. The 60-day correlation between S&P 500 returns and Treasury returns reached 0.6295, its highest level in more than 20 years.

Higher oil prices are feeding into inflation expectations faster than central banks can cut interest rates. US inflation reached a three-year high in April 2026, forcing investors to price higher financing costs into both bonds and economically sensitive equities.

Treasury Term Premiums Are Increasing Losses Across Bonds & Cyclical Equities

Higher crude prices raise shipping, aviation fuel, petrochemical, and industrial manufacturing costs within weeks because transport and commodity contracts reset faster than wages. Investors responded by demanding greater compensation for holding long-duration debt, pushing the 10-year Treasury term premium to 0.86% in May from below 0.50% in February.

During previous equity selloffs, Treasury bonds typically rallied because weaker growth lowered inflation expectations. Jonathan Cohn, head of US rates desk strategy at Nomura, said government bonds are now amplifying portfolio volatility during inflation shocks instead of offsetting it. That shift is pressuring long-duration bond funds, industrial metals, transport equities, and manufacturing shares tied to discretionary demand.

Fiscal Deficits & Inflation Risk Are Driving Long-Duration Bond Selling

Institutional desks are focusing more on inflation risk than recession risk because higher energy costs are colliding with elevated fiscal deficits and rising government borrowing needs. John Luke Tyner, head of fixed income at Aptus Capital Advisors, said long-duration bonds have become “certificates of confiscation” during high inflation periods because nominal yields still fail to protect purchasing power.

The Bureau of Economic Analysis core Personal Consumption Expenditures release is the next key inflation signal for bond markets. The annual rate reached 3.3% in April 2026, keeping pressure on the Federal Reserve to maintain restrictive monetary policy into 2027.

Companies With Pricing Power & Near-Term Cash Flows Are Holding Up Better Under High Inflation

Industrials with limited pricing flexibility face the fastest margin compression because fuel, freight, and financing costs are rising at the same time. Airlines, chemical producers, transport operators, and manufacturers tied to discretionary consumer spending cannot fully pass higher costs to customers without weakening demand.

Bond investors are moving toward shorter-duration securities because they carry lower sensitivity to long-term inflation risk. George Catrambone, head of fixed income for the Americas at DWS Group, said shorter maturities now provide better portfolio diversification than long-dated Treasuries during high inflation periods.

Trading geopolitical headlines is unreliable because military escalation can reverse commodity prices intraday while inflation data can shift bond and equity positioning each month. Investors without institutional hedging tools cannot predict those reversals in real time. Companies with strong balance sheets, recurring revenue, and pricing power are better positioned than investors attempting to time diplomatic developments.

Core Inflation & Treasury Yields Will Signal When Bond Markets Stabilize

Defense contractors, energy infrastructure companies, and shorter-duration fixed-income instruments are likely to outperform while the 30-year Treasury yield stays above 5% and US core inflation remains above 3.3%.

Core inflation below 3.3% year-over-year combined with the 30-year Treasury yield falling below 5% would likely increase demand for long-duration bonds. That move could reduce pressure on cyclical industrial equities while weakening demand for defense and energy-linked sectors.

Investors should monitor the monthly US core PCE release from the Bureau of Economic Analysis alongside daily Treasury term premium data published by the Federal Reserve Bank of New York. A decline in the 10-year term premium below 0.50% would signal stronger demand for long-duration bonds and lower inflation risk premiums across financial markets.

Analyst's Notes

Subscribe to Our Channel

Stay Informed