Section 232 Tariff Deadline & a 600,000-Tonne Copper Deficit Push Capital Toward Deliverable Projects

Copper markets face their first projected refined deficit since 2009 as Section 232 tariffs, AI demand and mine constraints reward projects with strong deliverability.

- The June 30, 2026 Section 232 deadline for a US refined-copper tariff recommendation has driven a record 652,200 tonnes of copper into COMEX warehouses while reducing London Metal Exchange inventories to about 352,100 tonnes, creating a widening price gap between the US and international copper markets.

- The International Copper Study Group and Morgan Stanley forecast a 2026 refined-copper deficit of 150,000 to 600,000 tonnes, marking the market's first projected shortage since 2009.

- Mine disruptions across Chile, Indonesia and the Democratic Republic of Congo are tightening supply just as new sources of demand emerge, with J.P. Morgan forecasting data centres alone will consume about 475,000 tonnes of copper in 2026.

- The tightening market favors deliverability over ore grade, rewarding projects with the permits, processing access, jurisdiction and funding needed to bring copper to market.

- The focus shifts from ore grade alone to the projects, jurisdictions and balance sheets most likely to deliver new copper supply into a market projected to record its first deficit since 2009.

Section 232 Tariff & the Copper Price Divide

Section 232 authorizes the US to restrict imports on national-security grounds. Under a July 2025 proclamation, the Commerce Secretary must deliver a copper-market report to the President by June 30, 2026, after which the administration may impose a 15% tariff on refined copper from January 2027, rising to 30% from January 2028. A separate 50% tariff on semi-finished and copper-intensive products has been in effect since August 2025, reinforcing the broader shift in US copper trade flows.

Traders have repositioned ahead of the June 30 Section 232 decision, reshaping global copper trade flows. COMEX inventories have climbed to a record near 652,200 tonnes while London Metal Exchange inventories have fallen to about 352,100 tonnes, widening the price premium between US and international copper markets. The roughly $200-per-tonne COMEX-LME arbitrage has become a real-time measure of the pricing gap created by shifting copper inventories. COMEX copper settled near $6.14 per pound on June 26, or about $13,200 to $13,500 per tonne on a London-equivalent basis. Prices remained about 21% above year-earlier levels but retreated to a seven-week low as a stronger US dollar and a more hawkish Fed weighed on sentiment.

Rising Copper Demand Meets Constrained Mine Supply

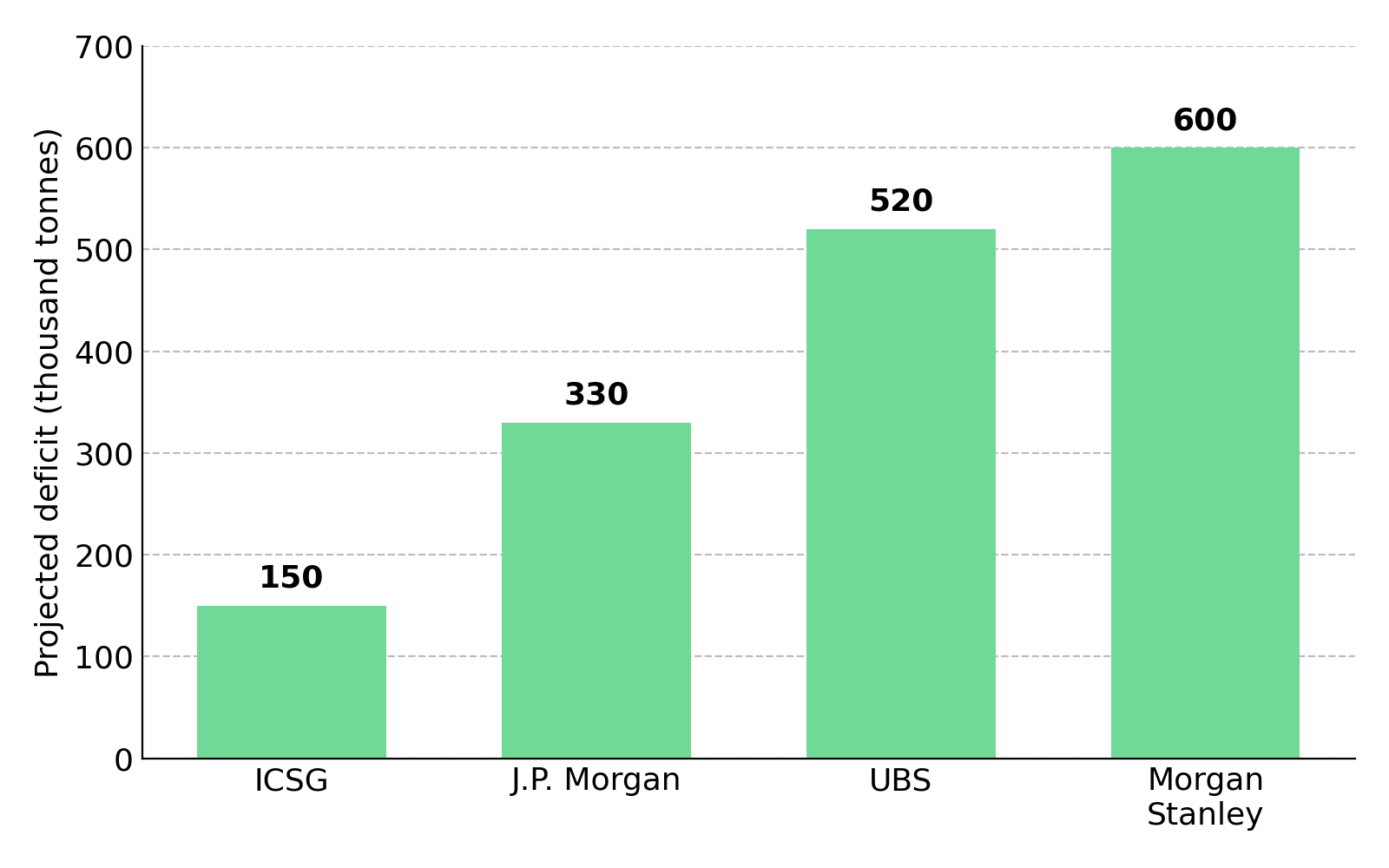

After years of projected surpluses, leading market forecasts now point to a refined-copper deficit in 2026. The International Copper Study Group revised its outlook from a projected 209,000-tonne surplus in October 2025 to a 150,000-tonne deficit in May 2026, the market's first projected shortage since 2009.

J.P. Morgan forecasts a 330,000-tonne deficit, UBS about 520,000 tonnes, and Morgan Stanley roughly 600,000 tonnes, implying the largest refined-copper deficit in more than two decades. The forecast sizes differ, but every major institution now projects a refined-copper deficit for 2026.

AI Infrastructure & Grid Expansion Sustain Copper Demand

Copper demand is becoming less sensitive to higher prices because AI infrastructure and grid expansion continue regardless of short-term price movements. J.P. Morgan estimates data centres will consume about 475,000 tonnes of copper in 2026, with a single hyperscale facility requiring up to 50,000 tonnes. Goldman Sachs attributes more than 60% of copper demand growth through 2030 to grid and power infrastructure. These investments are tied to long-term electrification and computing projects rather than discretionary purchases that decline when copper prices rise.

China, which consumes roughly half of the world's copper, is slowing but not reversing global demand growth. Growth in China's new-energy copper demand is projected to slow to about 2% in 2026 from an estimated 27% in 2025, while traditional sectors remain weak. Demand growth is becoming more geographically diversified, leaving mine supply rather than end-market demand as the main limit on the copper market.

Mine Supply Cannot Keep Pace with Copper Demand

Copper mine supply cannot respond quickly to rising demand because new production depends on long development timelines and existing operations face growing disruptions. Chilean copper output fell 9.04% year on year in March 2026, while Freeport's Grasberg restart in Indonesia slipped from 2027 to 2028. Ivanhoe's Kamoa-Kakula mine in the Democratic Republic of Congo also remains constrained by sulphuric acid shortages after China halted acid exports in May 2026, affecting an input used in roughly 15% of global copper production. Treatment and refining charges, the fees smelters earn to process copper concentrate, have fallen toward zero, indicating that concentrate has become scarce relative to available smelting capacity.

Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, an exploration-stage copper company in Chile, points to the economics facing the world's largest copper producer:

"You go to BHP, the world's largest copper producer, and at Escondida they are going to spend approximately $5 billion. The production profile in 2030 is likely to be 1 million tons per annum, down 20%, maybe even 30%, from where they are today. BHP, in the same report from August 2025, says there is going to be zero growth from Chile in 2031 to 2040."

Deliverability Outranks Ore Grade

In a market facing a refined-copper deficit, ore grade alone no longer determines value. Deliverability, the combination of permitting, processing and infrastructure access, jurisdiction and funding, determines whether a project can bring new copper supply to market. Investors can evaluate deliverability using standard mining metrics, including net present value and internal rate of return from technical studies, operating costs per pound and enterprise value per pound of contained copper, which indicates how much the market values copper resources before production.

A project's processing route often determines how quickly it can bring copper to market. Oxide ores can be processed through heap leaching followed by solvent extraction and electrowinning to produce cathode on site, reducing reliance on third-party smelters. Sulphide ores require a concentrator and a smelter, leaving producers exposed to the collapse in treatment and refining charges that reflects scarce concentrate supplies. As smelting capacity tightens, projects that can produce cathode on site have a shorter path to market than those that depend on third-party processing.

Development-Stage Projects Gain the Deliverability Premium

Marimaca Copper’s flagship Marimaca Oxide Deposit completed a definitive feasibility study in 2025, secured environmental approval and submitted its sectoral permits, with remaining approvals targeted for the fourth quarter of 2026 ahead of a final investment decision. As an oxide project using heap leaching and electrowinning, it is designed to produce cathode on site, while its self-supplied sulphuric acid strategy reduces exposure to the acid shortages affecting other producers. Its earlier-stage Pampa Medina discovery provides additional exploration upside but is not included in the current development case.

Hayden Locke, Chief Executive Officer of Marimaca Copper, explains why advanced copper projects are attracting major mining companies:

"If you start to deliver a project that contains three to five million tons of copper, in Chile's low-cost coastal belt with access to infrastructure and Antofagasta, that would grab the attention of just about every major mining company in the world because all of them are desperate for copper exposure."

Brownfield Assets Accelerate the Path to Production

Selkirk Copper, anexploration-stage company,is advancing a restart of the past-producing Minto mine, with a preliminary economic assessment and updated mineral resource estimate targeted for mid-2026. More than $330 million of existing infrastructure, including a 4,100-tonne-per-day mill, could reduce restart costs to about 25% of a comparable greenfield development. With prior streaming and concentrate offtake claims extinguished, the project also retains greater flexibility to secure non-equity financing if copper markets remain tight.

M. Colin Joudrie, Chief Executive Officer of Selkirk Copper, explains how the project's concentrate compares with the broader market:

"That 39% to 40% has been the historic concentrate grade for this asset over its life of mine, placing it probably in the top 5% of concentrates globally. Today, the average concentrate grade across the market is 26% to 28%, and it continues to decline."

Jurisdiction Shapes Project Value

Jurisdiction now matters as much as resource size because it influences how quickly copper projects reach production. Jurisdiction affects net present value because stable permitting and existing infrastructure reduce the discount rate applied to future cash flows, while political uncertainty and community opposition increase it. Recent policy changes in Peru and Chile could reduce permitting risk for new copper projects. Peru's mining-friendly election outcome and Chile's permitting reform, which targets a 30% to 70% reduction in approval times, could shorten development timelines across two of the world's largest copper-producing jurisdictions.

Jurisdiction now matters as much as resource size because it influences how quickly copper projects reach production. Jurisdiction affects net present value because stable permitting and existing infrastructure support lower discount rates, while political uncertainty and community opposition increase project risk and raise the discount rate applied to future cash flows. Peru's mining-friendly election outcome and Chile's permitting reform, which targets a 30% to 70% reduction in approval times, could shorten development timelines across two of the world's largest copper-producing jurisdictions.

Tier-One Geology Carries Higher Execution Risk

Mogotes Metals, an exploration-stage company in the Vicuña belt spanning Argentina and Chile, represents the earliest stage of the deliverability framework, offering greater exploration upside but higher execution risk. Its ground adjoins one of the largest recent copper-gold-silver discoveries, and a first drill hole at its Albor target returned 86 metres at 0.7% copper and 0.55 grams per tonne gold, including 43 metres at 1.1% copper. A Rio Tinto option over a separate asset provides third-party validation of the district's potential. However, Mogotes has not yet published a mineral resource estimate, making it the earliest-stage project discussed in this analysis. Its exposure to Argentina also introduces greater jurisdiction risk than the Chilean and Canadian projects highlighted above.

Allen Sabet, Chief Executive Officer of Mogotes Metals, explains why proximity to a major discovery attracts industry attention:

"There have been no other large discoveries like Filo, full stop, in the last 30 years. So, when you start to clip into something like that, it attracts interest, regardless of whether you want it or not."

Higher-for-Longer Rates Reward Strong Balance Sheets

With the Fed under Chair Kevin Warsh holding rates at 3.5% to 3.75% and markets pricing out near-term rate cuts, junior miners face a higher cost of raising equity capital. That makes the balance sheet a deliverability metric in its own right, because a funded developer can advance studies and drilling without dilutive equity raises, while an underfunded peer may have to delay development or issue new shares. Enterprise value per pound of contained copper helps investors assess valuation, while warrant overhang highlights the potential for future shareholder dilution.

Abitibi Metals shows how access to capital can become a competitive advantage when financing conditions tighten. The company consolidated full ownership of its B26 volcanogenic massive sulphide deposit, which contains a combined 25.3 million tonnes grading roughly 2.1% copper equivalent, and raised C$31 million without issuing warrants. The financing is expected to fund the project through a planned preliminary economic assessment in the first quarter of 2027. Recent transactions involving comparable volcanogenic massive sulphide deposits show continued strategic interest in this deposit type, although any relative valuation remains an analytical comparison rather than evidence of market value.

Jonathon Deluce, Chief Executive Officer of Abitibi Metals, explains how the current financing environment aligns with the copper cycle:

"This is the early stages of a copper bull rally, where we see sustainable increases in the copper price. We look at the recent closing of the Foran takeover by Eldorado for almost $4 billion, which showcases the demand for these deposits in the market, but also how rare they are."

The Copper Thesis Beyond the Tariff Deadline

The June 30 Section 232 report is a near-term catalyst, but it will not determine the long-term direction of the copper market. A determination confirming the phased 15% to 30% refined-copper duty would reinforce the year-long shift of copper inventories into the United States, widen the COMEX-to-LME premium and tighten supply elsewhere, while a softer or delayed outcome could unwind the inventory arbitrage and pressure international prices. Regardless of the outcome, institutional forecasts still point to a refined copper deficit, mine supply remains constrained and electrification continues to support long-term demand beyond any single policy decision.

The primary risk to the investment thesis is macroeconomic rather than geological. A sharp global growth slowdown would reduce copper demand, and J.P. Morgan notes the metal has historically fallen about 25% from its peak during major downturns. A stronger US dollar and higher-for-longer interest rates would also remain near-term headwinds for copper prices. Investors should also recognise that the companies discussed are pre-production developers and explorers. Project milestones may be delayed, additional financing will likely be required before production, and future equity raises could dilute existing shareholders. As with all early-stage mining investments, investors face the risk of partial or total capital loss.

The Investment Thesis for Copper

- Institutional forecasts point to the first refined-copper deficit since 2009, making permitting, processing, jurisdiction and funding more important than ore grade alone when assessing future copper supply.

- Development-stage assets with permits, a defined processing route and sufficient funding are best positioned to bring new copper supply to market and generate cash flow during a projected supply deficit.

- Development-stage assets with permits, a defined processing route and sufficient funding are best positioned to bring new copper supply to market if the projected refined-copper deficit materialises.

- Non-dilutive funding structures and warrant-free balance sheets improve deliverability by allowing companies to advance projects without relying on dilutive equity raises when higher-for-longer interest rates increase the cost of raising capital.

- Tier-one deposits can command a valuation premium, but earlier-stage projects face greater exploration and jurisdiction risk, which increases the discount rate investors apply to future cash flows until permitting, funding and development risks are reduced.

- Processing flexibility matters, since oxide projects that produce cathode through heap leaching and electrowinning can bypass the smelter bottleneck that constrains sulphide producers

- The tariff-driven price premium and the COMEX-LME arbitrage increase the value of projects that can deliver copper into the highest-priced market, making jurisdiction, trade exposure and deliverability central to evaluating producers, developers and explorers.

The June 30 Section 232 decision may move copper prices in the short term, but investors are increasingly valuing projects that can deliver new supply. Copper investment analysis is shifting from forecasting prices to identifying the projects, jurisdictions and balance sheets most likely to bring new supply to market during the first projected refined-copper deficit since 2009. The companies discussed illustrate different points along the deliverability spectrum rather than investment recommendations. Investors should review primary company filings and technical reports before making investment decisions.

TL;DR

Institutional forecasts point to the first refined copper deficit since 2009 as Section 232 tariffs reshape global trade flows, mine disruptions constrain supply and AI infrastructure boosts long-term demand. Record copper inventories in COMEX warehouses and declining London Metal Exchange stocks highlight a growing divide between US and international markets. The article argues that investors should look beyond ore grade and focus on deliverability, including permitting, processing, jurisdiction and funding, when evaluating copper companies. While the tariff decision may influence short-term prices, the longer-term investment case depends on which projects can bring new copper supply to market in an increasingly constrained industry.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed