Strip Now, Produce Later: Integra Resources Builds Toward a Higher-Production Florida Canyon

Integra Resources trades higher near-term costs at Florida Canyon for future growth, targeting 80–90k oz/year by 2027–2028 through stripping, fleet upgrades, and expansion.

The Nevada heap leach operation delivered 70,927 ounces in 2025, but costs overran and fourth quarter output fell sharply, setting the stage for a deliberate investment year in 2026 before a targeted step-change in production in 2027 and 2028.

What Has Happened

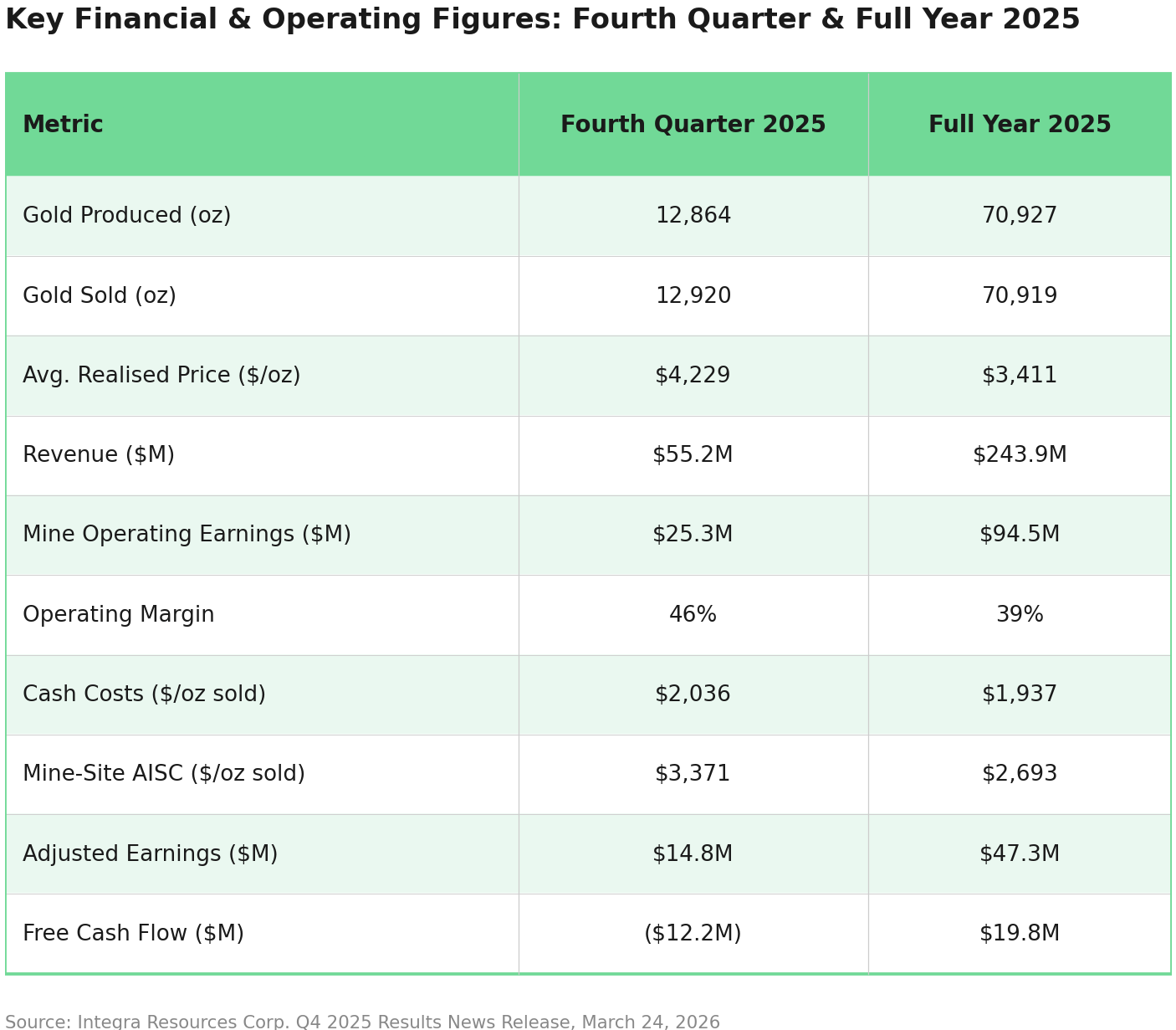

Integra Resources Corp. (TSXV: ITR; NYSE American: ITRG) reported fourth-quarter and full-year 2025 financial and operating results for its Florida Canyon Mine in Nevada. The headline figure: 70,927 gold ounces produced for the full year, meeting the company’s production guidance of 70,000 to 75,000 ounces, arrived alongside a more complicated operational picture: a sharp drop in fourth quarter output, costs above guidance ranges, and a sizeable capital programme in progress.

For investors, the results confirm the mine is performing broadly as planned, but the more significant disclosure is forward-looking. The company guided for production of 80,000 to 90,000 ounces per year in both 2027 and 2028. That guidance, and the investment required to get there, now defines the Integra investment case.

A Managed Fourth Quarter, Not a Problem

The fourth quarter’s production figure of 12,864 ounces of gold, against 20,653 ounces in the third quarter of 2025, demands explanation. The company attributes the shortfall almost entirely to a discrete operational incident: a liner tear in a solution pond identified during the fourth quarter, which caused a one-time, temporary reduction in solution flow rates. The liner was fully repaired by mid-November with no solution releases and no environmental impact, and solution flow rates were restored to normal levels before year-end.

Crucially, the ounces associated with the disruption were deferred, not destroyed. Based on leach pad inventories and normalised solution flow, the company expects the majority of ounces deferred during the fourth quarter, estimated at approximately 2,000 to 3,000 ounces, to be recovered through ongoing leaching throughout 2026. For a heap leach operation where recovery timing can be affected by seasonal and mechanical variables, this kind of deferral is a known feature of the process. The metallurgical performance itself remained intact: recovery rates for the year were consistent with expectations, and the modest fourth quarter variance reflects timing rather than any change in ore quality or metallurgical performance.

Costs Above Guidance: Royalties, Not Inefficiency

The cost picture for 2025 requires similarly careful disaggregation. Mine-site all-in sustaining costs (AISC) averaged $2,693 per gold ounce for the full year, exceeding the guidance range of $2,450 to $2,550 per ounce. At face value, that overshoot looks concerning. But the mechanism behind it matters: the company ended 2025 with an average AISC slightly higher than stated guidance, mainly due to higher royalties as a result of the increase in realised gold prices since issuing guidance in the second quarter.

Royalties and excise taxes are directly impacted by fluctuations in the gold price. A $100 per ounce change in the gold price results in an estimated $7 change to both metrics. With gold prices running materially above the levels assumed when guidance was set, the royalty blowback was both mechanical and largely unavoidable. Underlying operational cash costs of $1,937 per ounce of gold for the full year were similarly above the $1,800 to $1,900 guidance band. This is not a cost discipline problem; it is the price of selling gold above plan.

The financial results reflect a company generating real margin despite the cost miss. Full-year revenue reached $243.9 million, with mine operating earnings of $94.5 million at an operating margin of 39%. Adjusted earnings for the year were $47.3 million, or $0.28 per share, compared to an adjusted loss of $16.1 million in the comparable 2024 period. Full-year free cash flow was $19.8 million, or $0.12 per share.

The Investment Case for 2026: Strip Now, Produce Later

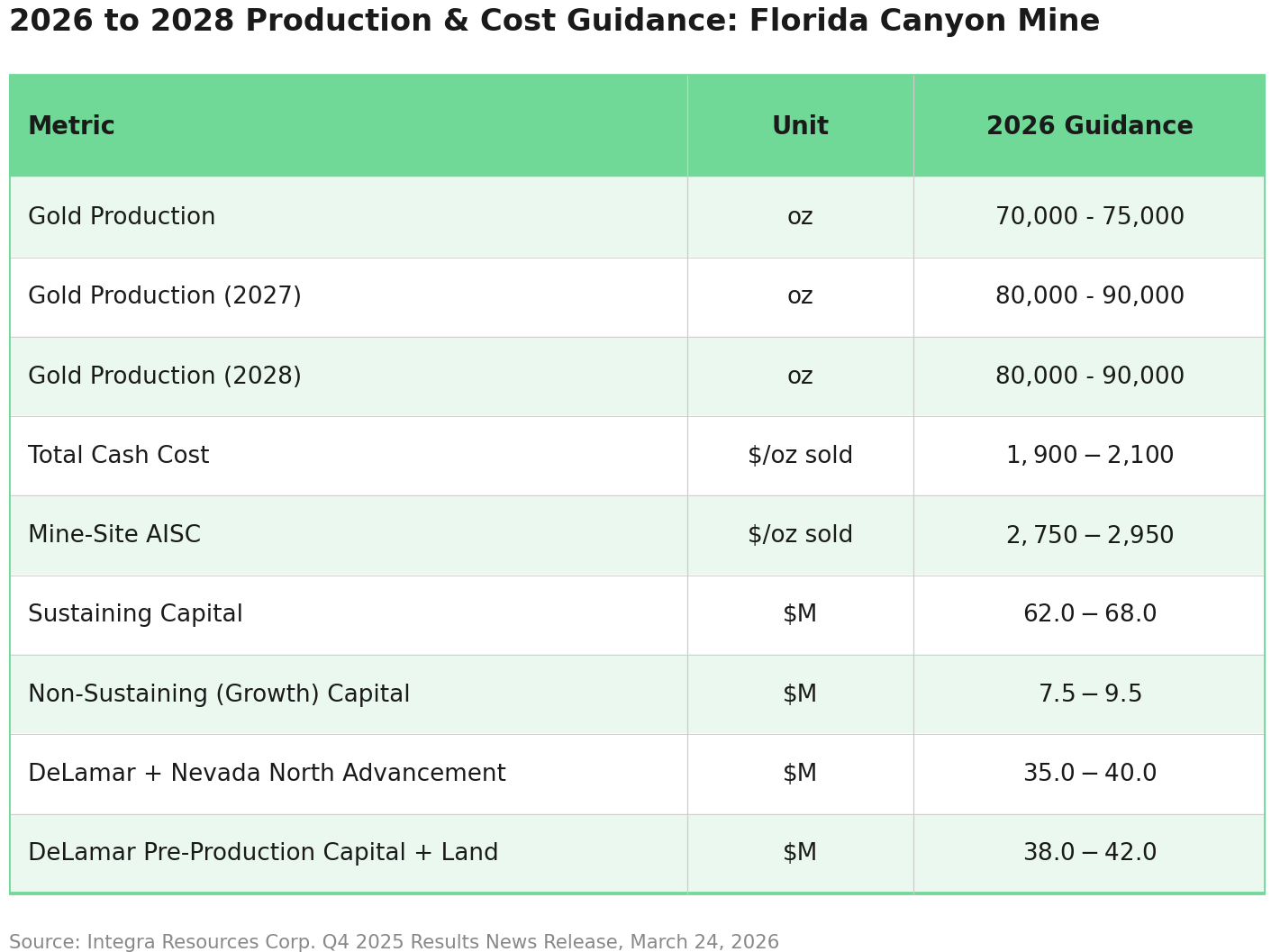

The 2026 guidance package is where the results release becomes most analytically significant. Production guidance for 2026 is unchanged at 70,000 to 75,000 ounces but at considerably higher cost. Mine-site AISC for 2026 is guided at $2,750 to $2,950 per ounce sold, reflecting increased waste stripping, higher gold price assumptions impacting royalty costs, increased fleet rebuild financing, and increased infill and development drilling.

The rationale for accepting elevated near-term costs lies in the mine plan mechanics. The company is planning to mine approximately 13.9 million tonnes of ore and 19.3 million tonnes of waste in 2026 for a strip ratio of 1.39. This reflects continued reinvestment through additional capitalised waste stripping and a targeted pit expansion of the Central Pit, which is expected to support higher annual gold production in 2027 and 2028.

President and Chief Executive Officer of Integra Resources, George Salamis, pointed directly to the mine plan mechanics driving the elevated 2026 cost profile, framing the stripping campaign as a prerequisite for accessing the mine's most productive ground.

"What's driving AISC now is essentially the stripping campaigns that we have to get through that are occurring ahead of accessing ore on the Central Pit, which is one of the largest ore bodies at Florida Canyon. It happens to come with higher grades."

The Central Pit is central to this thesis. It represents one of the largest ore bodies at Florida Canyon and carries higher grades than the areas currently being mined. Access requires clearing a significant pre-strip campaign first, work that drives up the 2026 strip ratio and sustaining capital, but which, once complete, opens a lower-cost, higher-volume mining sequence.

Salamis noted:

“Once we get through that stripping in 2026, we’re into much lower stripping, presumably much lower costs because of that reduced stripping rate.”

Sustaining capital expenditures in 2026 are guided at $62.0 to $68.0 million, with approximately 55% allocated to the first half of the year, focused on capitalised waste stripping, mobile fleet rebuild and replacement, and infill and development drilling. Non-sustaining growth capital of $7.5 to $9.5 million will be deployed on expansion projects and studies to be included in an updated technical report expected in the third quarter of 2026, as well as growth exploration targeting new areas outside the active mine boundary.

Fleet Renewal & Mine Life

Running alongside the stripping programme is a significant investment in mobile equipment. During the fourth quarter of 2025, Integra commissioned four new machines, a Hitachi EX3600 front shovel, a Caterpillar 992HL loader, and two Caterpillar 785 haul trucks, with an additional six Caterpillar 785 haul trucks expected to be commissioned in the first half of 2026. The upgraded fleet is expected to reduce dependence on rental equipment and lower the cost per tonne mined over time, a material efficiency lever for a high-volume heap leach operation.

Florida Canyon carries a mine life question that elevated strip ratios and capital-intensive periods tend to invite, and management acknowledges the asset was once regarded as effectively finished. The 2025 resource growth drilling programme was designed to reframe that narrative: originally planned for 10,000 metres, it was expanded to 16,000 metres on the strength of early results, targeting near-surface oxide potential from historical waste areas, inter-pit resources, and lateral extensions. The technical report, expected in the third quarter of 2026, will incorporate the full 2025 drilling results across near-mine targets including inter-pit areas and historical low-grade stockpiles, and will provide a revised life-of-mine plan against which the mine life question will be resolved.

DeLamar: Capital Deployment Accelerates

Florida Canyon's cash generation is increasingly being directed toward DeLamar. The feasibility study, completed in December 2025, confirmed average annual production of 106,000 ounces of gold-equivalent, mine-site AISC of $1,480 per ounce, and an after-tax net present value at a 5% discount rate (NPV5%) of approximately $774 million at base case prices of $3,000 per ounce gold and $35 per ounce silver. In January 2026, the Bureau of Land Management (BLM) formally established a federal permitting schedule under the National Environmental Policy Act (NEPA), with a Notice of Intent expected in the second quarter of 2026 and a Record of Decision targeted for the third quarter of 2027 following a 15-month review period.

Capital deployment in 2026 reflects the parallel demands of permitting and construction preparation. Project advancement spending across DeLamar and Nevada North is guided at $35.0 to $40.0 million, covering detailed engineering, permitting, and baseline studies. A further $38.0 to $42.0 million has been allocated to pre-production capital and strategic land acquisition, with approximately 70% directed to long lead equipment procurement and early works.

Subsequent to year-end, the company completed a bought deal public offering of 18,121,600 common shares at $3.40 per share for gross proceeds of $61.6 million, intended to fund pre-production capital expenditures at DeLamar.

What to Watch Next

Several discrete catalysts will define Integra’s trajectory over the next 12 to 18 months. The most significant near-term disclosure is the updated Florida Canyon technical report, expected in the third quarter of 2026, incorporating 2025 drilling results and the revised life-of-mine plan.

On the development side, the BLM’s publication of a Notice of Intent for DeLamar in the second quarter of 2026 initiates the formal NEPA public scoping process. Progress under the FAST-41 accelerated permitting framework will be closely watched, with a Record of Decision targeted for the third quarter of 2027.

At Nevada North, the company is planning the commencement of a pre-feasibility study in the latter part of 2026 with an expected announcement in the first half of 2027. With approximately 45% of annual ounces expected in the first half of 2026, production performance in that period will test whether the deferred fourth quarter inventory ounces recover as planned and whether the fleet commissioning programme proceeds on schedule. For a company that is deliberately deferring margin today to build capacity for higher output in 2027 and 2028, execution against the near-term operational plan is the most important signal investors can observe.

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

.jpg)

Stay Informed