Supply Security Risks & Western Uranium Scarcity Drive Contract Prices to 14-Year Highs

Uranium contract prices hit a 14-year high as supply cuts, geopolitical risk, and energy security policies increase competition for future uranium supply.

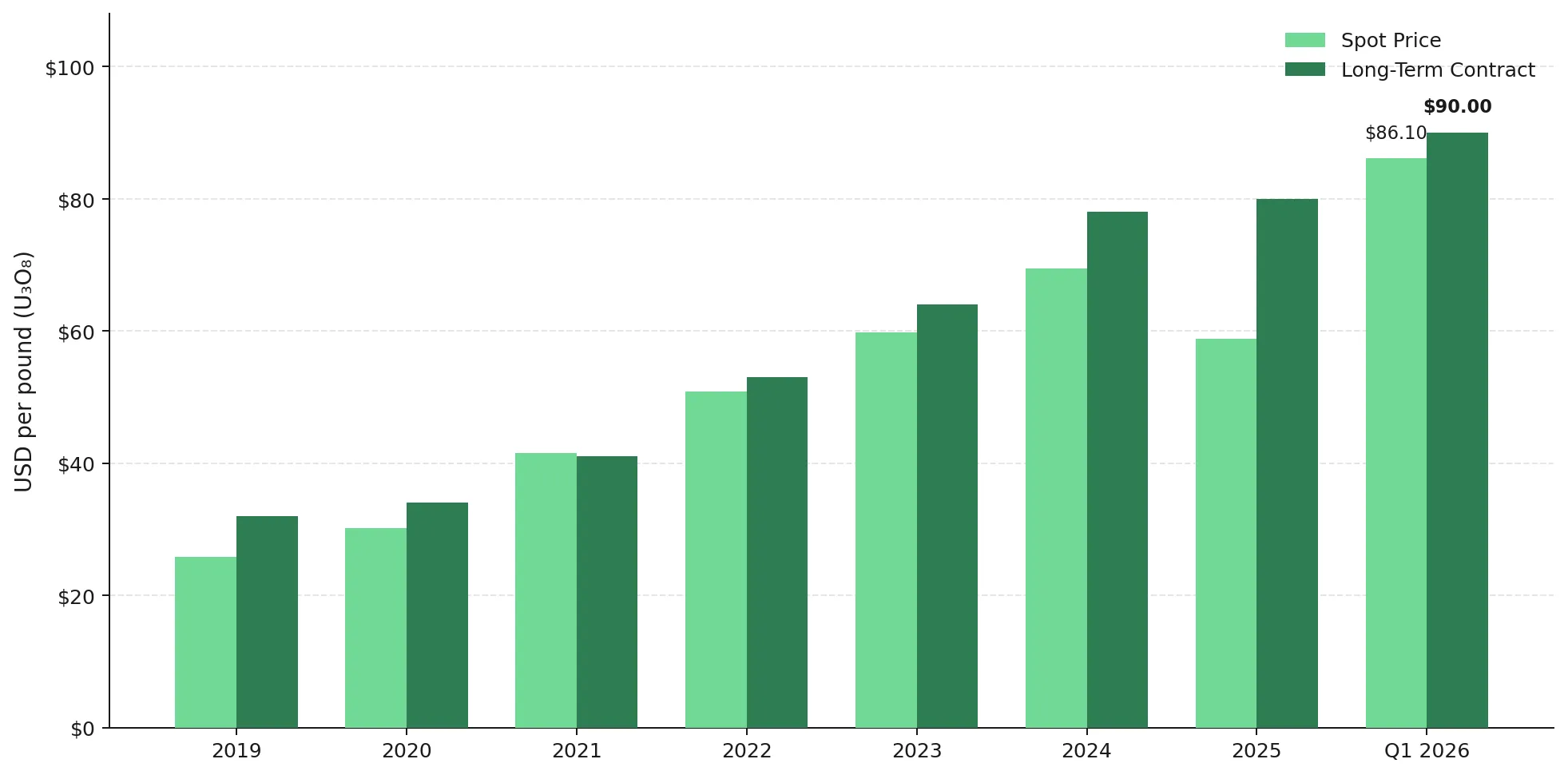

- Long-term uranium contract prices reached $90 per pound in Q1 2026, their highest level since 2008, as utilities secured supply amid production cuts in Kazakhstan and reduced Western access to Nigerien uranium, while spot prices remained at $86.10 per pound.

- The IAEA Board of Governors meeting in Vienna on June 8-12, 2026 follows the Agency's disclosure that 440 kilograms of highly enriched uranium in Iran cannot be verified, increasing geopolitical risk and supporting higher uranium contract prices.

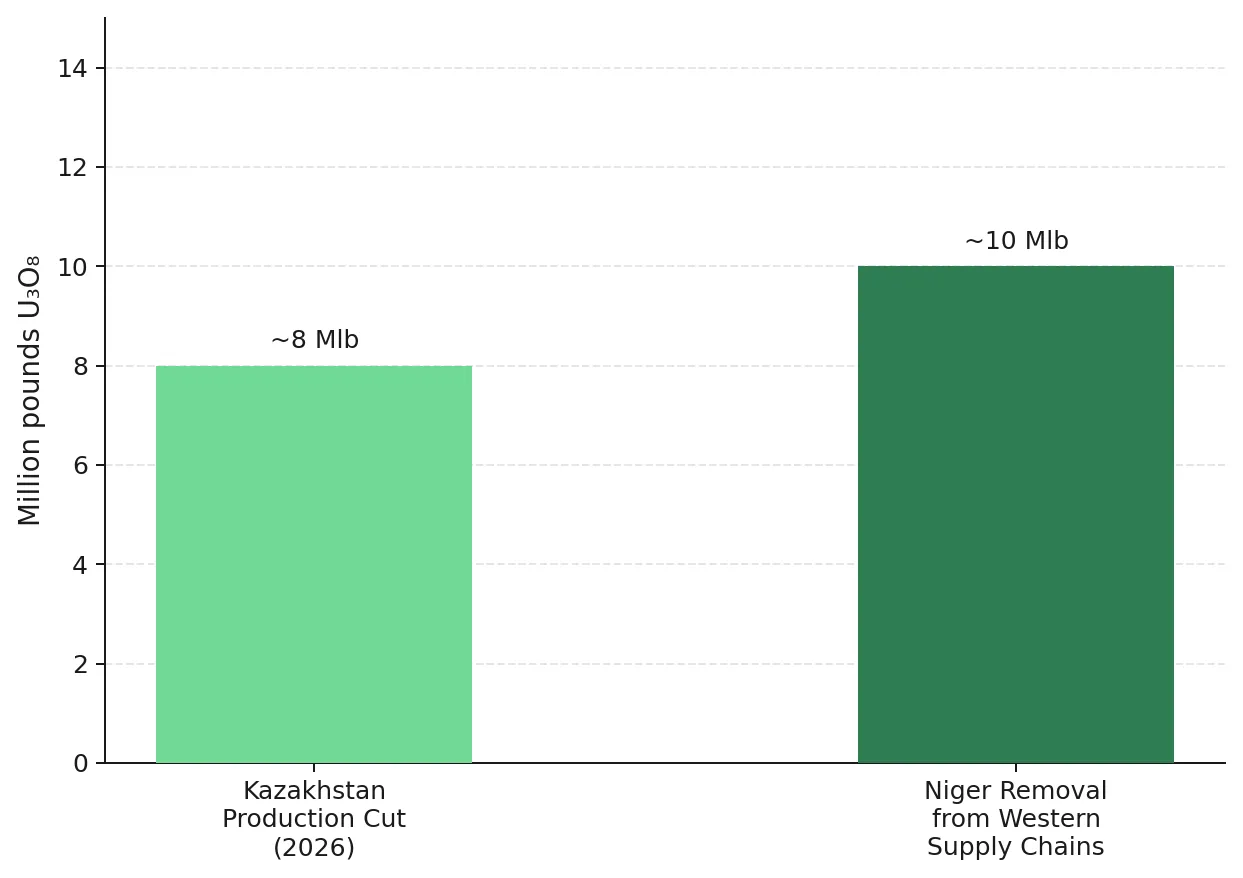

- Niger's SOMAÏR nationalization and Kazakhstan's 10% production cut have reduced uranium available to Western buyers, increasing competition among European and US utilities for contracted supply.

- The US Department of Energy's "Nuclear Dominance - 3 by 33" Defense Production Act initiative brings together more than 90 companies under a coordinated framework to build a domestic nuclear fuel supply chain by 2033.

- Uranium producers, developers, and explorers in politically stable jurisdictions may benefit from higher contract prices as utilities shift procurement away from geopolitically exposed supply sources.

Long-Term Uranium Contracts Trade Above Spot as Supply Risks Rise

As of June 8, 2026, U3O8 traded at $86.10 per pound after several weeks of limited price movement. However, long-term uranium contract prices reached $90 per pound in Q1 2026, indicating stronger utility demand for future supply than the spot market suggests.

Spot transactions primarily reflect near-term uranium deliveries between traders and intermediaries. Long-term contracts allow utilities to secure multi-year uranium supply for reactor operations. Utilities are accepting $90 per pound in long-term contracts while spot uranium trades at $86.10 per pound, indicating greater concern about future supply availability than near-term market conditions.

The gap between spot and long-term uranium prices reflects reduced Western access to uranium supply following Kazakhstan's 10% production cut and Niger's SOMAÏR nationalization, alongside higher geopolitical risk linked to the IAEA's inability to verify 440 kilograms of highly enriched uranium in Iran.

IAEA Verification Concerns & Rising Demand for Stable Uranium Supply

The IAEA Board of Governors meeting in Vienna on June 8-12, 2026 is focused on unresolved questions surrounding Iran's nuclear program. On June 8, IAEA Director General Rafael Mariano Grossi said the Agency could no longer verify 440 kilograms of highly enriched uranium at Iranian nuclear facilities after in-field verification activities were suspended in February 2026. A US-drafted resolution would refer the issue to the UN Security Council, while Iran's parliament has voted to end cooperation with the IAEA after the ceasefire period.

The issue is not a loss of uranium supply but higher geopolitical risk. The IAEA's inability to verify 440 kilograms of highly enriched uranium increases uncertainty around Iran's nuclear program and raises geopolitical risk in uranium markets. An extraordinary IAEA session on June 5 addressed Iran's drone attack on the UAE's Barakah nuclear power plant, highlighting that civilian nuclear infrastructure can be targeted during regional conflicts. Both developments increase the value of uranium supply from politically stable jurisdictions as utilities seek to reduce geopolitical risk in fuel procurement.

Kazakhstan Production Cuts and Niger Nationalization Tighten Uranium Supply

Geopolitical risk is occurring alongside reduced uranium supply available to Western buyers. Kazakhstan's 10% production cut and Niger's removal from Western supply chains have reduced uranium available to Western buyers and supported higher contract prices.

Kazakhstan Cuts Uranium Output While Expanding Domestic Nuclear Demand

Kazatomprom, which supplies approximately 38% of global uranium output, confirmed a 10% production cut for 2026, removing roughly 8 million pounds from global supply. Kazakhstan is also planning three nuclear power plants, each expected to consume approximately 400 tonnes of uranium annually, increasing domestic demand.

Niger's SOMAÏR Nationalization Ends a 58-Year Uranium Supply Relationship

Niger's military junta nationalized the SOMAÏR mine in June 2025, in which Orano held a 63.4% stake, and cancelled France's 58-year Arlit uranium concession in 2026. Approximately 1,000 tonnes of uranium yellowcake remain stranded at Niamey's international airport under a World Bank ICSID tribunal order. Niger historically supplied 5-7% of global uranium production, and its removal from Western supply chains is directing European demand toward Canadian and Australian producers. Phil Hoskins, Chief Executive Officer of Atomic Eagle, describes the projected uranium supply shortfall and the need for new production before 2040:

"By 2040, supply is going to drop to 50 million pounds based on current production and demand will double to 400 million pounds. Our project is capable of bringing on pounds by circa 2030 or 2031, when that shortfall is going to hit. We believe that leaves us well placed to help fill that supply gap."

US Nuclear Fuel Policy Drives Domestic Uranium Supply Chain Growth

The US Department of Energy's "Nuclear Dominance - 3 by 33" campaign, launched through the Defense Production Act Nuclear Fuel Cycle Consortium in April 2026, brings together more than 90 companies across the nuclear fuel chain under a federally coordinated framework with antitrust protection, targeting a domestic fuel supply chain by 2033.

Energy Fuels operates the White Mesa Mill in Utah, the only fully licensed and operating conventional uranium mill in the US, giving the company a direct role in the domestic fuel supply chain targeted by the DOE initiative. The company produced 790,000 pounds of finished U3O8 in Q1 2026 at a weighted average inventory cost of approximately $36 per pound, compared with long-term uranium contract prices of $90 per pound. Mark Chalmers, Chief Executive Officer of Energy Fuels, explains how uranium producers are balancing long-term contracts with exposure to strengthening spot prices:

"We have long-term contracts, and those are getting into larger quantities this year. If we're mining at a 2 million pound rate, there's a lot of freeboard there for capitalizing on the spot market if we elect to. We like that ability to have some under contract and some ability to deal on the spot."

The Defense Production Act initiative also benefits in-situ recovery producers as the US seeks to increase domestic uranium production. enCore Energy completed construction of its largest satellite ion exchange plant at Upper Spring Creek on June 4, 2026 and is targeting full flow capacity of 3,200 gallons per minute by the end of July 2026. According to the US Energy Information Administration, domestic uranium demand is rising by 48 million pounds per year while domestic supply is declining by approximately 200,000 pounds per year, increasing the value of new US production. William Sheriff, Executive Chairman of enCore Energy, explains why bringing new uranium supply to market remains more difficult than many investors expect:

"There aren't too many producers. In fact, there's a real shortage of them. A lot of companies want to produce, but we've seen a lot of hurdles to that production. It's a lot easier to talk about than to actually do. The supply side is the troublesome component and it's probably more expensive than people realize going forward."

$90 Uranium Contracts Improve Financing Conditions for Developers

A $90 per pound long-term uranium price improves project financing conditions for developers. At $90 per pound, feasibility-stage uranium projects can secure financing without relying on below-market offtake agreements to support project debt. Debt financing often requires producers to commit future uranium sales at fixed prices, limiting exposure to higher uranium prices later in the cycle.

IsoEnergy provides an example of how stronger uranium prices can improve project financing flexibility. Following a 2026 financing that attracted more than $300 million of demand for a $50 million offering from 45 institutional investors, IsoEnergy held approximately CAD $130 million in cash and can evaluate a restart of its Tony M mine in Utah without taking on debt. Philip Williams, Chief Executive Officer of IsoEnergy, explains how debt-linked contracting can limit exposure to higher uranium prices during bull markets:

"When producers sign contracts and prices spike to $150 per pound while they realize $90 per pound, they're not maximizing the value of every pound produced. They've left $60 per pound on the table because they signed contracts that were subpar. We don't need to do that because we're fully funded for a restart and we're restarting mines that already exist."

Projected Uranium Deficits Increase the Value of New Discoveries

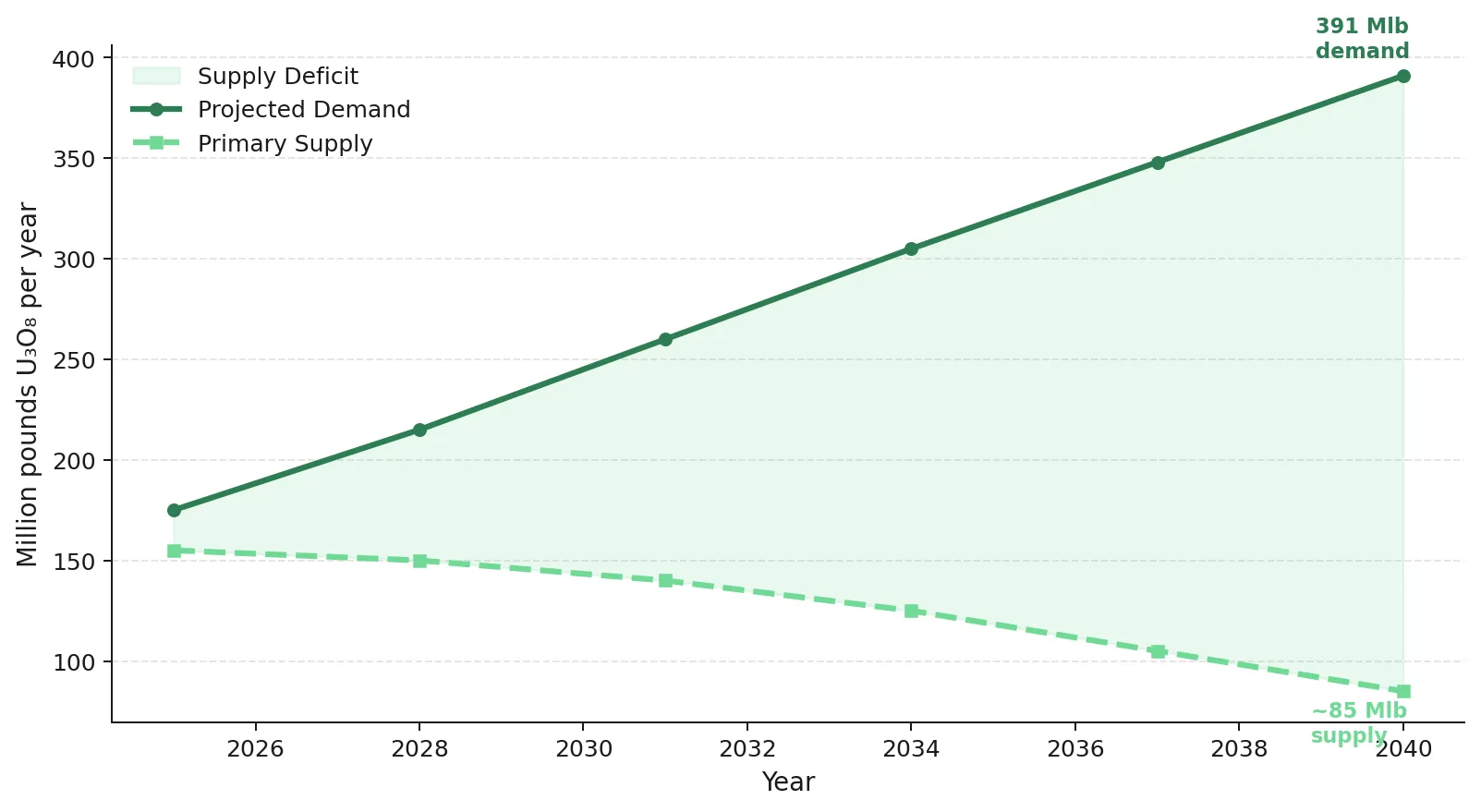

No significant new uranium supply is expected before 2030, even under optimistic development timelines. The World Nuclear Association's 2025 World Nuclear Fuel Report reference scenario projects uranium demand of 391 million pounds by 2040 against identified supply of 179 million pounds, leaving supply equal to 46% of projected demand. This projected supply deficit increases the value of exploration projects capable of adding future uranium supply in politically stable jurisdictions.

ATHA Energy provides exposure to the exploration side of the uranium supply response, controlling 100% of the 6.8-million-acre Angikuni Basin in Nunavut, Canada. In 2025, ATHA drilled 13 holes across the RIB Corridor and intersected uranium mineralization in all 13, returning grades of up to 8.16% U3O8 over 0.5 metres across a system spanning 14 kilometres of strike. By comparison, major Athabasca Basin deposits including Cigar Lake and NexGen's Arrow each have strike lengths of less than one kilometre. Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the combination of rising uranium demand and supply-side uncertainty supporting exploration activity:

"The macro environment in the uranium sector is unlike any time I've seen in my career. The sentiment and real demand that's being built up, coupled with some of the supply-side risk, is a setup we have not seen in the uranium space."

The Investment Thesis for Uranium

- Long-term uranium contract prices of $90 per pound exceed the spot price of $86.10 per pound, indicating that utilities are willing to pay more to secure future supply than immediate deliveries.

- Kazatomprom's removal of approximately 8 million pounds from 2026 global supply and Niger's exit from Western supply chains have reduced uranium available to Western buyers, while new mine development is unlikely to add significant supply before 2030.

- The DOE's Defense Production Act Nuclear Fuel Cycle Consortium brings together more than 90 companies under a federally coordinated framework with antitrust protection, supporting domestic uranium producers and fuel-cycle operators through a 2033 supply chain buildout.

- At $90 per pound, long-term uranium prices can allow developers to finance mine construction without relying on below-market hedging agreements tied to project debt, increasing exposure to future uranium price gains.

- High-grade uranium exploration projects may gain value if the projected supply deficit persists, as new mines typically require years to reach production.

- The IAEA's inability to verify 440 kilograms of highly enriched uranium in Iran and Niger's removal from Western supply chains may increase utility demand for uranium sourced from politically stable jurisdictions.

Long-term uranium contract prices reached $90 per pound in Q1 2026 while spot uranium traded at $86.10 per pound on June 8, indicating stronger demand for future supply than immediate deliveries. Kazakhstan has reduced uranium production by 10% for 2026 while planning three domestic nuclear power plants, and Niger has nationalized SOMAÏR and cancelled France's 58-year Arlit uranium concession, reducing uranium available to Western buyers. The IAEA cannot verify 440 kilograms of highly enriched uranium in Iran. The DOE's Defense Production Act Nuclear Fuel Cycle Consortium has brought together more than 90 companies to support a domestic nuclear fuel supply chain by 2033, which may benefit producers, developers, and explorers in politically stable jurisdictions.

TL;DR

Long-term uranium contract prices reached $90 per pound in Q1 2026, exceeding the $86.10 spot price as utilities prioritized supply security amid tightening market conditions. Kazakhstan's 10% production cut, Niger's removal from Western supply chains, and the IAEA's inability to verify 440 kilograms of highly enriched uranium in Iran have increased competition for contracted uranium supply. At the same time, the US is building a domestic nuclear fuel supply chain through a DOE-backed initiative involving more than 90 companies. Higher contract prices are improving financing conditions for developers and increasing the potential value of exploration projects as projected uranium demand continues to outpace identified supply.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed