The 8-15 Year Discovery Lag Uranium Investors Need to Understand

Uranium exploration data shows market efficiency, 8-15yr discovery lags, and weak junior returns. Diversify, track fundamentals, avoid reactive buying on news.

- An AI-assisted analysis of 650 press releases from 40 uranium companies over five years found that initial price reactions to news normalise within five days, suggesting markets are more efficient than many industry participants expect.

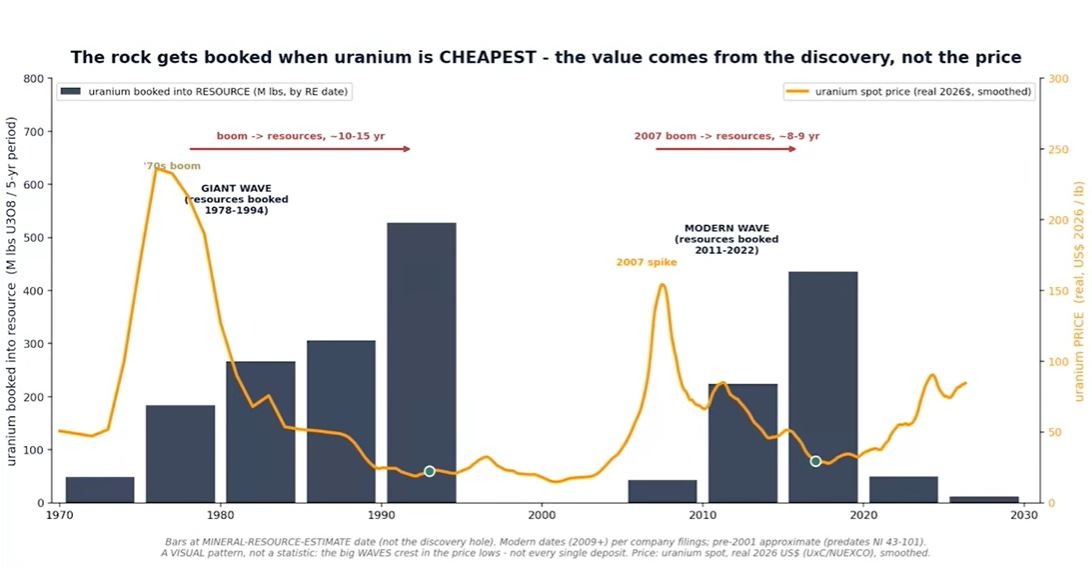

- Historical data spanning 50 years shows an 8-to-15-year lag between uranium price peaks - which attract exploration capital and the point at which that capital produces defined resources in the Athabasca Basin.

- Only six significant uranium resources were discovered in the basin over the past 20 years; successful companies shared common traits including large land positions exceeding 200,000 hectares and sustained capital deployment before their first discovery hole.

- The majority of uranium exploration companies delivered negative returns to shareholders over the past five years despite rising spot prices, with several forced into share consolidations.

- Frostad recommends investors build a diversified portfolio of three to five uranium explorers, prioritising management quality, capital structure discipline, and project fundamentals over commodity price movements alone.

For investors tracking the uranium sector, the gap between the commodity's improving fundamentals and the performance of junior exploration companies has been a persistent frustration. Uranium spot prices have risen meaningfully over the past several years, long-term contracting has increased, and the supply-demand narrative has strengthened - yet shareholders in many exploration-stage companies have seen little corresponding benefit. Chris Frostad, CEO, Purepoint Uranium, with direct experience in Athabasca Basin exploration, covered findings from an AI-assisted press release analysis, a 50-year historical look at discovery timing cycles, and practical guidance on portfolio construction for uranium investors today.

What the Press Release Data Actually Shows

Frostad and his team applied data analysis tools to approximately 650 press releases from 40 uranium companies over five years, pairing that information with corresponding stock price histories. The aim was straightforward: does the language and framing of drill results produce a lasting and measurable impact on share prices?

The findings were revealing for what they did not show. A well-worded or enthusiastically framed press release could generate a first-day price increase, but that gain was typically erased by day three before partially recovering by day five. Regardless of promotional language - terms like "spectacular," "offscale," or "peak mineralisation" - share prices converged to a level reflecting the actual underlying information within approximately one week.

"It was boringly efficient," Frostad said of the market's behavior. "You just had to let it do its job."

One specific pattern stood out: approximately 60% of press releases that cited encouraging handheld gamma readings never followed up with formal assay results. This implied that the initial count-per-second figures being highlighted did not ultimately support the implied discovery narrative. Results framed as "technical successes" - typically conveying geological learning rather than economic mineralisation - were consistently received as neutral-to-negative news by the market, regardless of their operational merit. The data also confirmed that volume spikes around press release dates provided existing shareholders with a convenient exit opportunity, which contributed to the short-term price decline before stabilization.

The practical takeaway is modest but useful: investors who react immediately to a positive press release may be buying at an inflated price. Allowing two to three days for initial trading volume to settle may offer a more representative entry point.

The Historical Timing Gap Between Price Cycles and Discovery

A second component of the analysis examined 50 years of uranium price cycles alongside resource discoveries in the Athabasca Basin, covering approximately two billion pounds of uranium identified across 40 deposits. The data revealed a consistent and significant lag between uranium price peaks - which attract new capital into exploration - and the point at which that capital produces measurable resources.

In the 1970s price boom, the gap between peak uranium prices and peak resource discovery was 10 to 15 years. In the 2007 cycle, it narrowed to approximately eight or nine years. Perhaps counterintuitively, the years with the highest volume of new resource discoveries coincided not with strong uranium prices, but with price troughs. The explanation is mechanical: money flows in at the top of the price cycle, but converting that money into a defined resource requires years of drilling, assaying, and technical work.

"When the price goes up, all of a sudden there's a lot of money available. But if you're in exploration, how long is it going to take me to actually make a discovery? How long is it going to take me to turn that into a resource? Because that's the period of time that an explorer creates the value that everybody's looking for."

This has direct implications for how investors should calibrate expectations. Rising uranium spot prices benefit producers and, to a lesser extent, developers with advanced projects. For exploration-stage companies, the value-creation event is the discovery itself and its subsequent conversion to a resource estimate - not the commodity price trajectory. Investors who entered exploration companies over the past five years expecting commodity-driven returns have largely not seen them, and the historical data suggests that dynamic is structurally predictable rather than a temporary anomaly.

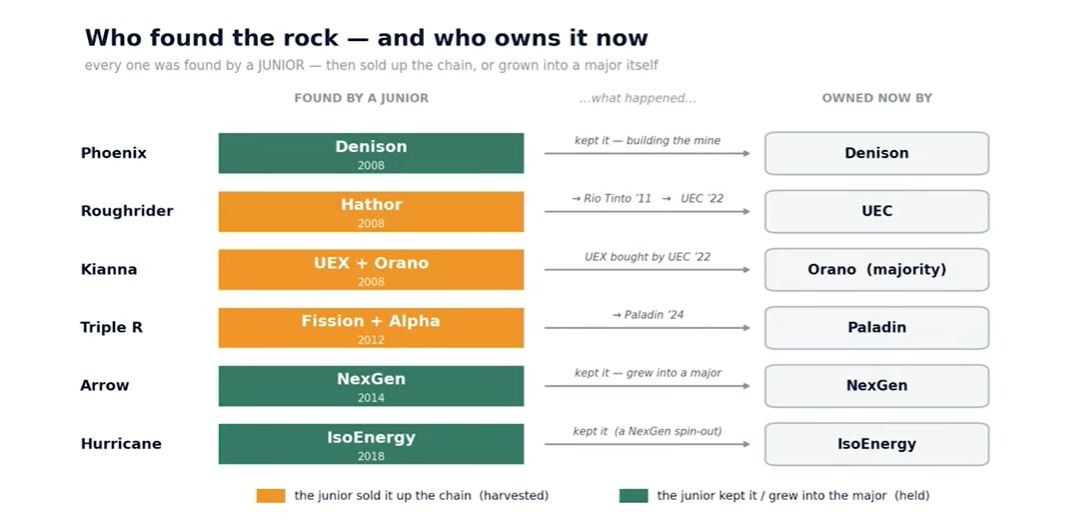

Six Discoveries in Twenty Years: What the Winners Had in Common

Frostad identified six uranium resources placed on the books in the Athabasca Basin over the past 20 years to examine what the successful exploration companies shared. These include Denison’s Phoenix deposit, Hathor’s Roughrider deposit (later acquired by Rio Tinto and subsequently by Uranium Energy Corp), the Kiana deposit at Shea Creek jointly held by UEX and Orano, Fission’s Triple R deposit now owned by Paladin, NexGen’s Arrow deposit, and IsoEnergy’s Hurricane deposit. Each was initially a junior company at the time of discovery.

The common characteristics were notable. All of the companies held large land positions - in excess of 200,000 hectares distributed across the basin - rather than concentrating resources on a single project. All spent millions of dollars and drilled dozens of holes before achieving a significant intercept. None made a rapid or inexpensive discovery.

"You got to look at the rock. Is this company in a position to make a discovery and then is that discovery capable of being turned into a resource?"

He acknowledged, however, that geological merit is necessary but not sufficient. An element of chance remains in determining which company is positioned above an undiscovered deposit. The implication for investors is that no screening process eliminates discovery risk entirely - but attention to land scale, management capability, and capital discipline improves the statistical odds.

The Broader Performance Picture

Looking at a wider group of 16 uranium exploration companies over five years, the performance data presented a difficult picture. Only three delivered positive returns to shareholders, and those gains were modest relative to the risk involved. Several companies were forced into share consolidations - a significant warning sign, according to Frostad, indicating that the share structure had become too diluted to support further capital raising at viable terms.

Dilution is a structural challenge specific to exploration-stage companies. With equity issuance typically their only avenue for raising capital, companies that require extended timelines before discovery will see their share counts grow steadily. This can impair per-share value even when the underlying geological asset remains intact and potentially viable.

The Energy Show with Chris Frostad, CEO, Purepoint Uranium

Building a Uranium Portfolio Today

For investors considering uranium exposure now, Frostad outlined a top-down construction approach. Those with conviction on the commodity thesis - supported by tightening supply, long-term contracting growth, and constrained production from major producers - should allocate first to producers, then to developers, before adding exploration-stage companies.

For the exploration tier, he recommended diversification across three to five companies rather than concentration in a single name. Core assessment criteria should include management track record, the quality and scale of the land position, capital structure sustainability, and the geological case for the project. Importantly, active monitoring and a willingness to exit positions when those criteria are no longer met is preferable to a passive approach.

"Be harsh. When those boxes aren't getting ticked, move on and find another one that ticks the boxes."

He also noted that the current cycle - with significant capital deployed in the past five years - may be approaching a period where new discoveries begin to emerge, though the timeline remains uncertain. His own company recently began following up on intercepts grading upward of 8% uranium, which he cited as an example of the type of early-stage development that warrants continued attention.

Key Takeaways

The data presented in this discussion points to a straightforward but often overlooked reality in uranium exploration investing: geological and financial fundamentals matter considerably more than promotional timing or commodity momentum. The market, as the press release analysis shows, is reasonably efficient at pricing exploration news within days, and investor behavior that chases first-day price spikes is unlikely to generate consistent outperformance. The historical record of discovery timing confirms that explorers create value on their own cycle, which runs years behind commodity price movements. For investors willing to accept that structure - diversifying across well-managed companies with strong land positions and disciplined capital allocation, while actively monitoring and adjusting exposure - the sector may offer meaningful return potential as the current price cycle matures. For those expecting commodity appreciation alone to drive explorer valuations, the evidence suggests that expectation will continue to disappoint.

TL;DR

Uranium exploration companies have broadly failed to deliver shareholder returns over the past five years despite rising spot prices, because of a structural 8-to-15-year lag between capital influx and resource discovery. Press release analysis confirms that market hype normalises within five days, making patient entry points more advantageous than reactive buying. Successful explorers historically share large land positions, significant pre-discovery drilling, and disciplined capital management - traits that should anchor portfolio selection over commodity price direction.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed