Undervalued? Amex Exploration Showing a 2–3x Valuation Gap to Peers

AMEX Exploration argues 2-3x undervaluation vs peers despite 5.1g/t grade, $146M Phase 1 capex, bulk sample targeting early-2028 commercial output.

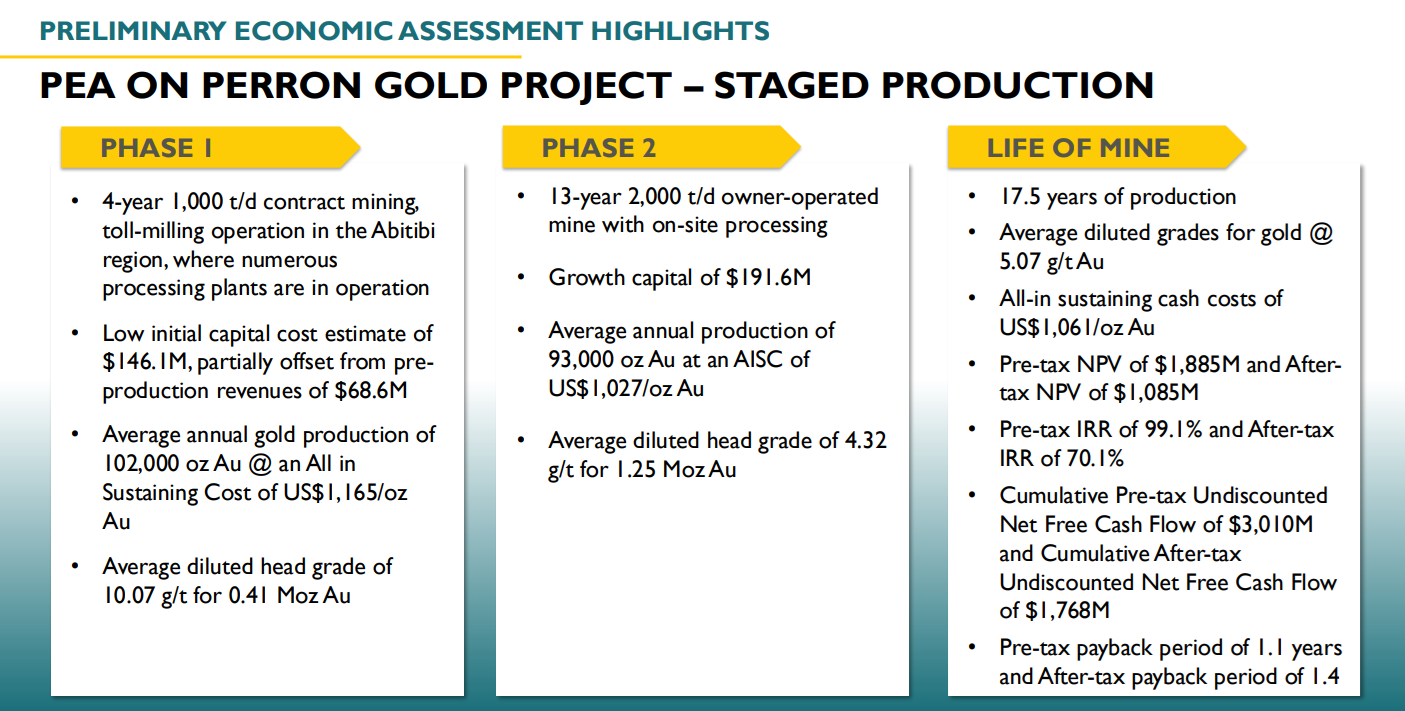

- Amex Exploration trades at approximately C$494 million market cap following the recent fall in Gold price, which management considers significantly undervalued compared to peers trading at 2-3x higher valuations with similar production timelines but lower grades and higher capex.

- Company employs three-stage development (bulk sample, Phase 1, Phase 2) designed to minimise financial and technical risk, with each phase funding the next through revenue generation rather than dilutive financing.

- Bulk sample permit expected imminently (currently at 6-month review mark), targeting mid-2026 for 20,000-23,000 ounce bulk sample from 40,000-ton sample, with Phase 1 production beginning 2028.

- Project grade of 5.1 g/t (diluted basis) substantially exceeds peer average of 1.9-3.6 g/t, with flagship Champagne zone grading 16 g/t undiluted, enabling economic production at smaller scale with $146 million Phase 1 capex versus industry norm

- Proximate location to existing town provides immediate access to workforce, electricity grid connection, and water supply, reducing capital requirements and operational risks compared to remote deposits requiring diesel generation

Amex Exploration Inc. (TSXV:AMX), a Quebec-based gold developer, has emerged as a case study in perceived market mispricing within the junior mining sector. With a market capitalisation of C$494 million, the company trades at a material discount to comparable development-stage peers, which are valued at approximately 2–3x higher levels. CEO Victor Cantore outlines a detailed case for this valuation gap and the factors that could support a re-rating.

The discussion centers on three key differentiators: exceptional ore grades, a capital-efficient phased development strategy, and favourable infrastructure positioning. As gold prices remain elevated and investors scrutinise development timelines and capital requirements, understanding the gap between Amex's current valuation and management's assessment provides insight into how the market values grade versus scale in precious metals development.

The Peer Comparison Framework

The company’s valuation case is grounded in peer comparison. Slide materials indicate that development-stage companies with similar production timelines are trading at market capitalisations two to three times higher than Amex, despite, in management’s view, less favourable project economics, though Cantore is clear to state they are great projects in their own right. The gap appears to be driven more by differences in grade quality and capital intensity than by resource size or jurisdictional risk.

The comparison framework focuses on projects approaching production with similar timelines early-to-mid 2028 for initial commercial production but differentiated by technical and economic parameters. Where peer projects report grades in the 1.9 to 3.6 grams per tonne (g/t) range and require larger processing facilities to achieve economic throughput, Amex's feasibility study contemplates production exceeding 100,000 ounces annually from a 2.3 million ounce gold equivalent resource base with Phase 1 capital expenditure of $146 million.

Phased Development Strategy: Mitigating Risk Through Sequencing

The company's development approach diverges from conventional single-phase construction models through deliberate staging designed to reduce both financial and technical risk. The three-phase structure: Bulk sample, Phase 1, and Phase 2 creates a self-funding pathway where each stage generates revenue to finance subsequent expansion without proportional equity dilution.

The bulk sample phase, currently awaiting what Cantore expects is imminent permit approval, involves processing 40,000 tonnes of ore yielding between 20,000 and 23,000 ounces. Critically, this preliminary mining operation utilises infrastructure identical to Phase 1 requirements, functioning as operational validation rather than mere exploration.

Phase 1 development requires $146 million in capital expenditure according to the preliminary assessment, becomes substantially self-funded through bulk sample proceeds. Under this model, the majority of construction capital derives from operational cash flow rather than capital markets, reducing dilution and financing costs. The transition from Phase 1 to Phase 2 follows the same principle, with Phase 1 revenues funding Phase 2 expansion.

Interview with Victor Cantore, President & CEO of Amex Exploration Inc.

Regulatory Progress Toward Production

Regulatory progress represents a near-term catalyst with material implications for valuation. The bulk sample permit application filed in mid-September 2025 entered the government review process with guidance indicating a three-to-six-month timeline. At the time of discussion, the application had reached the six-month threshold, with approval characterised as imminent.

Upon permit receipt, construction mobilisation follows within approximately 45 days, positioning the project for bulk sampling to ore extraction and processing. The toll milling arrangement whereby third-party facilities process ore in exchange for fixed fees while Amex retains all gold proceeds provides operational flexibility and capital efficiency. Processing facility selection remains in advanced stages, with metallurgical consultants evaluating multiple mill options for compatibility with the ore characteristics.

The Phase 1 exploitation permit, distinct from the bulk sample authorisation, follows a parallel track with a conservative three-and-a-half-year timeline. However, management anticipates acceleration based on regulatory precedent and operational similarity to the bulk sample, potentially compressing the timeline by 12-15 months.

Infrastructure Positioning and Operational Advantages

Geographic location contributes materially to the project's economic profile through existing infrastructure access. The deposit's proximity to an established town provides immediate workforce availability, eliminating accommodation construction costs and reducing labor mobilisation expenses. Electrical grid connectivity, recently secured through permit approvals, eliminates diesel generation requirements and associated fuel price exposure.

Water supply availability, another infrastructure element often requiring significant capital in remote locations, exists through municipal connections. These infrastructure elements, which individually might represent modest cost advantages, collectively differentiate the project's capital intensity from remote deposits requiring complete infrastructure construction from greenfield conditions.

Grade as the Fundamental Differentiator

The economic case for Amex centers on ore grade differential rather than resource tonnage. At 5.1 g/t on a diluted whole-deposit basis, the project substantially exceeds industry averages, but the grade distribution reveals even more compelling economics. The Champagne zone, which forms a significant portion of Phase 1 mining inventory, grades 16 g/t before dilution, with practical mining grades expected between 10 and 12 g/t.

This grade advantage creates multiple economic benefits. Higher-grade ore requires proportionally less tonnage to achieve target production, reducing processing facility size, energy consumption, and waste handling, each translating to lower capital and operating costs. The relationship between grade and capital efficiency appears linear in management's assessment, with higher grades enabling smaller, less expensive infrastructure while maintaining equivalent or superior cash flow generation.

The grade differential also provides margin resilience across gold price scenarios. The preliminary assessment, modelled at $2,500 per ounce gold, demonstrates economic viability even at $2,000 gold based on sensitivity analysis. This margin cushion reflects the fundamental advantage of high-grade deposits: when a significant portion of revenue derives from grade rather than volume, commodity price volatility affects returns less dramatically than in lower-grade, higher-volume operations.

Resource Expansion Potential

While development activities dominate near-term focus, exploration programs continue across the company's 502 km2 land position within the Abitibi Greenstone Belt. The recent agreement with First Nations in Ontario opens additional exploration territory, with drilling programs deploying immediately to test targets identified through previous work.

The exploration strategy balances resource expansion against the demonstrated economics of existing reserves. Management articulated the strategic choice: prioritise advancement of the known high-grade deposit to production while maintaining exploration programs funded increasingly by operational cash flow rather than equity financing. This approach addresses a common junior mining challenge, the tension between drilling to expand resources and advancing development to demonstrate value.

Re-evaluation Catalysts

The discussion occurred against a backdrop of elevated gold prices (even allowing for recent retrenchment), though the company's economic thesis deliberately minimises gold price dependency. Management emphasised that project economics derive primarily from grade and cost structure rather than commodity price assumptions, creating what they characterise as a margin-protected investment profile.

Near-term catalysts for potential revaluation include bulk sample permit receipt, construction commencement, and production in 2028. The transition from exploration company to revenue-generating entity represents a fundamental category shift potentially warranting different valuation multiples. The progression from Phase 1 to Phase 2, demonstrating the self-funding model's viability, constitutes a subsequent milestone.

Key Takeaways

Amex Exploration's investment proposition rests on several interlocking elements: exceptional ore grades generating superior margins, a phased development strategy designed to minimise capital requirements and dilution, favourable infrastructure reducing both capex and operating costs, and near-term catalysts including imminent permitting and bulk sampling initiation. The valuation argument compares the company's C$494 million market cap against peers trading at 2-3x multiples with similar timelines but lower grades and higher capital intensity.

The strategy's effectiveness will ultimately be validated through execution milestones: permit receipt, construction completion within budget and timeline, metallurgical performance confirming grade expectations, and the transition to self-funded development demonstrating the phased model's financial viability. The Ontario exploration program provides optionality for resource expansion, though the core thesis prioritises advancing the known deposit to production. For investors evaluating development-stage gold companies, Amex represents a test case for whether the market ultimately rewards grade quality and capital efficiency over resource tonnage and scale.

TL;DR:

Amex Exploration (TSXV:AMX) trades at C$494M market cap while management argues for 2-3x revaluation based on peer comparison, citing 5.1 g/t average grade (versus peer average 1.9-3.6 g/t) and flagship Champagne zone at 16 g/t enabling $146M Phase 1 capex versus industry norm. Phased development strategy targets bulk sampling, funding Phase 1 construction around 2027 towards 2028 commercial production, with bulk sample permit approval imminent after 6-month review. Key differentiators include superior grade economics, infrastructure access near existing towns with electrical grid connection, and self-funding development model minimising dilution while maintaining $5.5B life-of-mine revenue potential from 2.3M oz resource.

FAQs (AI Generated)

The phased strategy (bulk sample → Phase 1 → Phase 2) mitigates financial and technical risk by using revenue from each stage to fund subsequent expansion, minimising equity dilution and external financing requirements while validating operations incrementally.

At 16 g/t undiluted (10-12 g/t mining grade), Champagne zone substantially exceeds peer averages of 1.9-3.6 g/t, enabling profitable production at a smaller scale with lower capital requirements while generating higher margins per tonne processed.

Mid-2027 production initiation is targeted, following permit approval (expected imminently), 45-day construction mobilisation, and facility commissioning. Toll milling arrangement allows Amex to retain all gold proceeds minus processing and transport fees.

Management asserts the bulk sample will generate sufficient revenue to cover most Phase 1 capex, contrasting with industry norms requiring full capital raise. The self-funding model reduces dilution and eliminates traditional construction financing needs.

Proximity to an established town delivers immediate workforce access, municipal electricity grid connection eliminating diesel generation, water supply availability, and reduced accommodation/mobilisation costs versus remote deposits requiring complete infrastructure construction.

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

.jpg)

Stay Informed