US Aluminum Tops $6,000/Tonne: Why the Cost Floor Holds After the War Ends

US aluminum tops $6,000/tonne as Hormuz closure and full-value tariffs combine - why the cost floor holds even if the war ends and what investors need to watch.

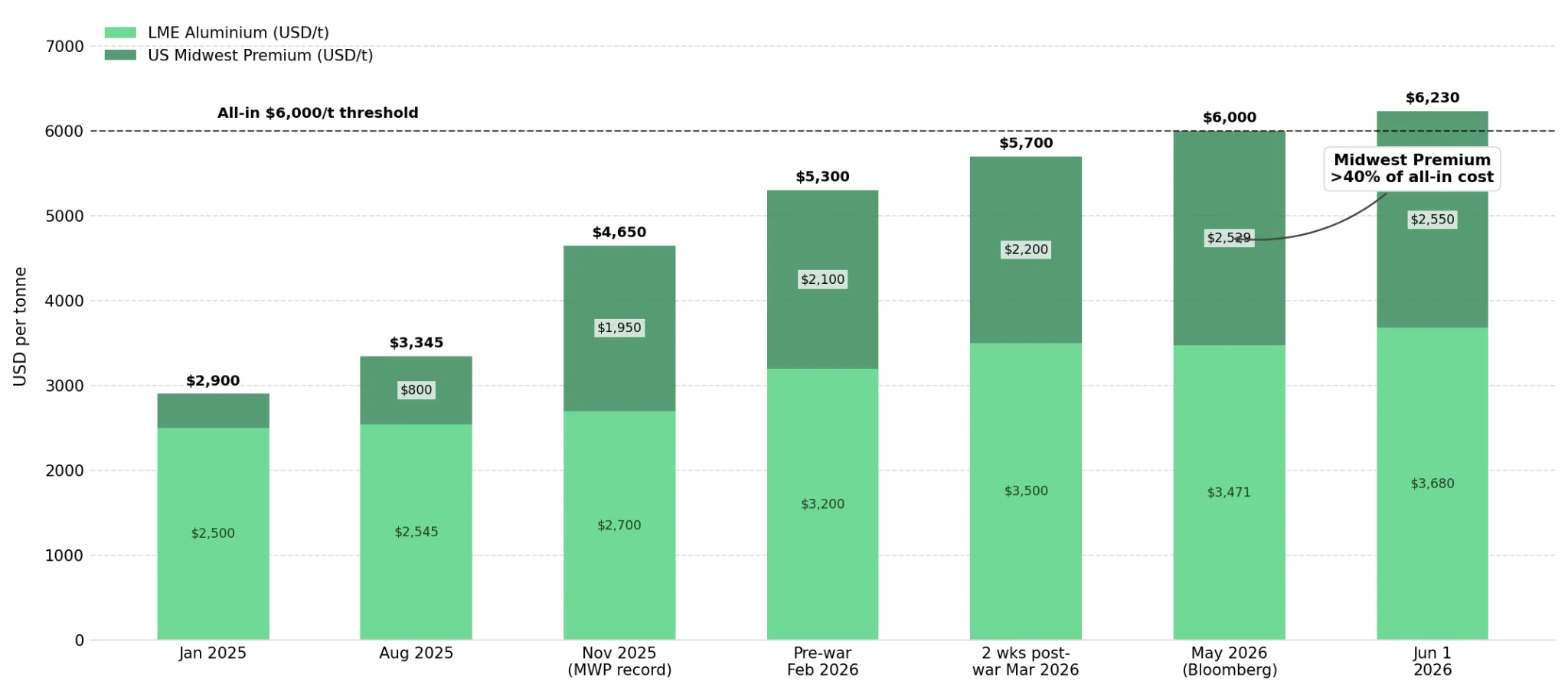

- LME aluminum rose from $3,200 to $3,500/tonne, a four-year high, within two weeks of the Iran war's late February 2026 start, when the Strait of Hormuz closure removed 9% of global supply from normal transit routes as per CME Group.

- The US Midwest Premium reached $2,529/tonne in early May 2026, pushing the all-in US transaction price past $6,000/tonne; the premium accounts for over 40% of that total.

- Presidential Proclamation 11021 (April 2, 2026) shifted Section 232 aluminum tariffs from metal content to full invoice value, expanding the effective tariff base for every US importer of aluminum articles.

- A Strait reopening lowers the LME flat price but leaves Canada's 50% full-value tariff intact; the July 2026 USMCA review may be the only near-term structural relief mechanism.

The War Accelerated a Deficit That Was Already Building

The Iran war, which began in late February 2026, closed the Strait of Hormuz, the transit route for Middle East aluminum production representing 9% of global output. LME aluminum, trading at $3,200/tonne before the conflict, rose to a four-year high of $3,500/tonne within two weeks. In the United States, the Midwest Premium reached $2,529/tonne in early May 2026, lifting the all-in price past $6,000/tonne and placing the premium at over 40% of total transaction cost as per CME group.

The price move compounded a supply deficit that predated the war. Wood Mackenzie had already forecast a 2026 shortfall well above the 50,000-tonne gap expected in late 2025, driven by EV production, solar panel manufacturing, and AI data center construction. Aluminium Bahrain announced a 19% output cut following the maritime disruption, and the deficit is projected at 800,000 tonnes by 2028 if disruption continues.

The Tariff Floor Compounds the Supply Disruption

Presidential Proclamation 11021 (April 2, 2026) shifted the tariff base from aluminum metal content to the full value of finished goods and derivatives. Canada, which supplied 43% of US aluminum imports ($7.5 billion) in 2025, now faces a 50% tariff on the entire invoice value, with no exemption since March 2025. A Strait reopening lowers the LME component but does not touch the 50% full-value duty on Canada's dominant supply share.

Portfolio Exposure and the Operational Flexibility Test

US manufacturers without domestic scrap access - EV producers, aerospace, and consumer goods companies - face the $6,000/tonne all-in cost directly, with the Midwest Premium representing over 40% of the total transaction price. The April 2026 full-value tariff base means Canadian-sourced finished aluminum components carry a 50% duty on the entire invoice, raising per-unit costs beyond what the $3,500/tonne LME price alone implies.

Manufacturers with domestic scrap access occupy a structurally different position. US secondary aluminum capacity is estimated to reach 4 million tonnes in 2026, up from 3 million tonnes in 2025, following $10 billion in recent investment. Substituting domestic scrap for Canadian primary imports avoids the full 50% tariff on that fraction - a cost differential that compounds while the Midwest Premium remains elevated.

The actionable constraint is that the USMCA review outcome is unknowable in advance. The signal to monitor: whether the July 2026 USTR proceedings formally open a Section 232 aluminum exemption discussion - that event, not the Strait's status, is what could move the Canadian cost floor.

Analyst's Notes

Subscribe to Our Channel

Stay Informed