Hormuz Minefields Keep Oil Above $90: What It Means for Energy, Gold & Portfolio Positioning

Hormuz minefields and US-Iran tensions keep oil above $90, while Chinese demand and Fed policy determine the outlook for energy and gold.

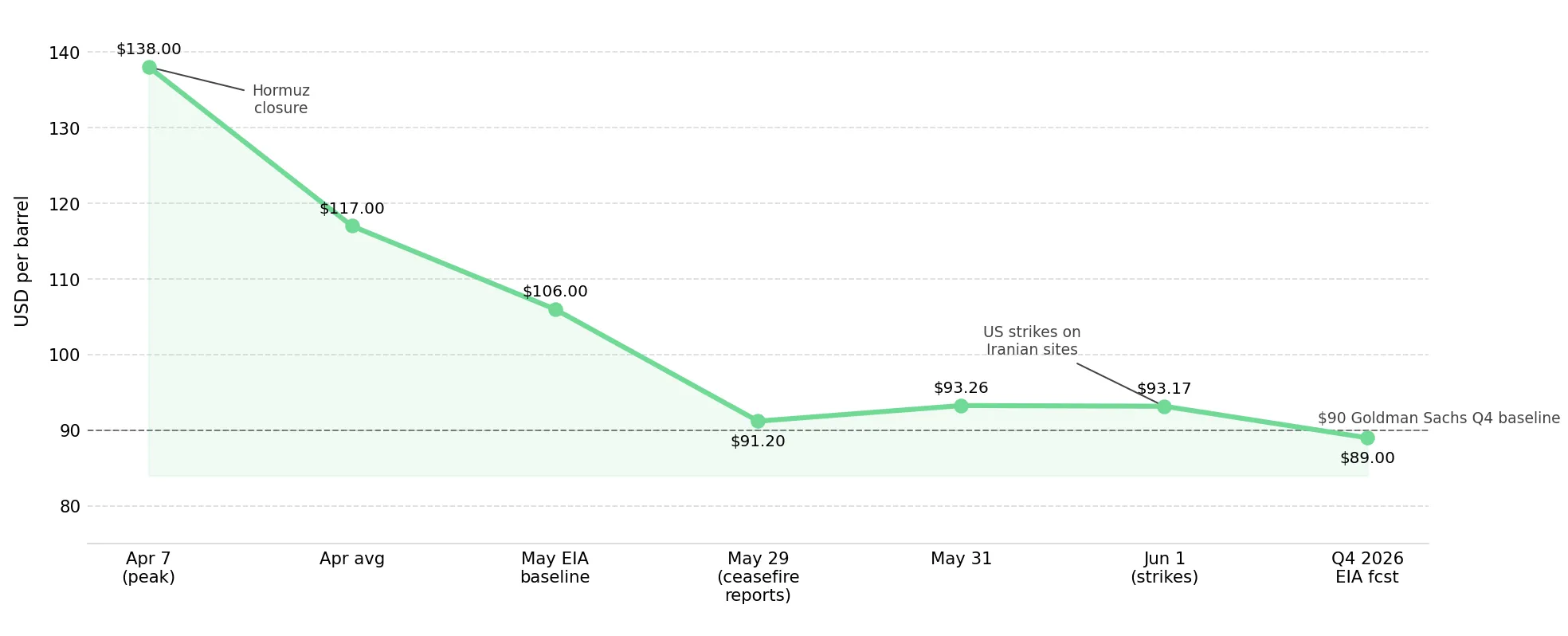

- Brent crude jumped 2.25% to $93.17 a barrel and US WTI rose 2.62% to $89.65 at 0436 GMT on June 1, 2026, after weekend US strikes on Iranian sites and an Iranian Revolutionary Guard counterstrike on a US base.

- The Strait of Hormuz, roughly 20% of global oil and gas flows, stays effectively shut because Iranian sea mines laid in late May must be physically cleared before tankers resume, a process that outlasts any ceasefire signing.

- Goldman Sachs holds a $90 Brent baseline for Q4 2026; a sharp contraction in Chinese factory activity is the named downside risk that pulls Brent below $90.

- Spot gold slipped 0.3% to $4,521.25 an ounce as a firmer dollar offset safe-haven demand; the timing of President Trump's ceasefire decision is not tradeable, because Iran's demand to include Hezbollah remains unresolved.

- The trade reverses if confirmed Chinese demand destruction drives Brent durably below $90, easing inflation, softening the dollar, and opening gold's path toward KCM Trade's $5,500 end-2026 target.

Oil Prices Surge as US-Iran Military Escalation & Hormuz Closure Threaten Supply Flows

Global oil prices surged in early trading on June 1, 2026, with Brent futures rising $2.05 to $93.17 a barrel and US West Texas Intermediate climbing $2.29 to $89.65 by 0436 GMT.. The move followed weekend US military strikes on Iranian radar and drone-control sites at Goruk and Qeshm Island, after which Iran's Islamic Revolutionary Guard Corps struck a US base on Sirik Island on Monday. Spot gold fell 0.3% to $4,521.25 an ounce by 0520 GMT, pressured by a stronger US dollar.

The strikes matter as they extinguish the market's late-May bet on a ceasefire extension, which had cut Brent nearly 19% over the month. The price shock now hardens into a physical supply problem: with the Strait of Hormuz still closed, the conduit for one-fifth of world oil and gas flows is offline, so the question shifts from sentiment to when barrels physically move again.

Hormuz Mine Clearance & Diplomatic Gridlock Delay Supply Recovery

Iran reportedly deployed additional sea mines in the Strait of Hormuz in late May 2026, with US Defense Secretary Pete Hegseth saying the move violated proposed ceasefire terms. The mines continue to restrict tanker traffic, meaning oil flows cannot quickly normalize even if a political deal is reached. Meanwhile, seven wildfires near major Canadian oil sands facilities, including Canadian Natural Resources' Jackfish operation, pose an additional risk to global supply.

The conflict remains difficult to resolve because the key political obstacles are structural, not tactical. Washington's proposed de-escalation framework has been undermined by Israel's expanded operations against Hezbollah in Lebanon, while US-Iran negotiations remain stalled over Iran's insistence on including Hezbollah in any agreement and continuing disagreements over its nuclear program.

Investment Outlook Hinges on Supply Recovery & Chinese Demand

The key risk is assuming a diplomatic breakthrough will quickly restore oil supplies. Even if the US and Iran extend the ceasefire, shipping through the Strait of Hormuz cannot fully resume until mines are cleared and tanker routes are secured. As a result, supply constraints could persist for weeks, supporting Brent near $90 per barrel by Q4 2026, while a weaker US dollar and easing oil prices could help lift gold toward $5,500 per ounce.

A contraction in manufacturing activity would signal softer fuel consumption and could push Brent below $90 per barrel despite supply disruptions. China's manufacturing PMI and trade data, alongside Fed guidance, should be monitored for clues on demand trends and the inflation impact of higher energy prices.

Energy Gains Face Operational Risks as Gold Reacts to Higher Rates

Gold may remain under pressure if conflict-driven inflation supports the US dollar and delays Fed rate cuts, while energy assets continue to benefit from supply constraints. However, wildfires near Canadian oil sands operations highlight the operational risks that can affect individual producers even as oil prices rise.

Rather than betting on the outcome of US-Iran negotiations, the possibility of prolonged inflation and supply disruptions should be considered. Position sizing remains critical, as concentrated energy and gold exposures can be volatile if geopolitical conditions shift unexpectedly.

Chinese Demand Determines Whether Energy or Gold Outperforms

The current market backdrop favors energy as long as the Strait of Hormuz remains disrupted and Brent holds above $90 per barrel. Under that scenario, inflation expectations remain elevated, supporting the US dollar and limiting gold's upside.

Two consecutive readings of factory activity below the 50 PMI threshold, combined with weakening exports, would point to demand destruction and increase the risk of Brent falling below $90 per barrel. That shift could ease inflation pressures, weaken the dollar, and improve the outlook for gold, potentially reversing the current preference for energy exposure.

Analyst's Notes

Subscribe to Our Channel

Stay Informed