Why Goldman Sachs Expects Brent Near $90 Even After the Strait of Hormuz Reopens

Goldman Sachs sees Brent near $90 even if Hormuz reopens as supply disruptions persist and oil's risk premium takes months to unwind

- Brent traded near $95 on June 2, 2026, up roughly 5% from the prior session and about 30% above pre-conflict levels, after Iranian state media signaled a possible full closure of the Strait of Hormuz.

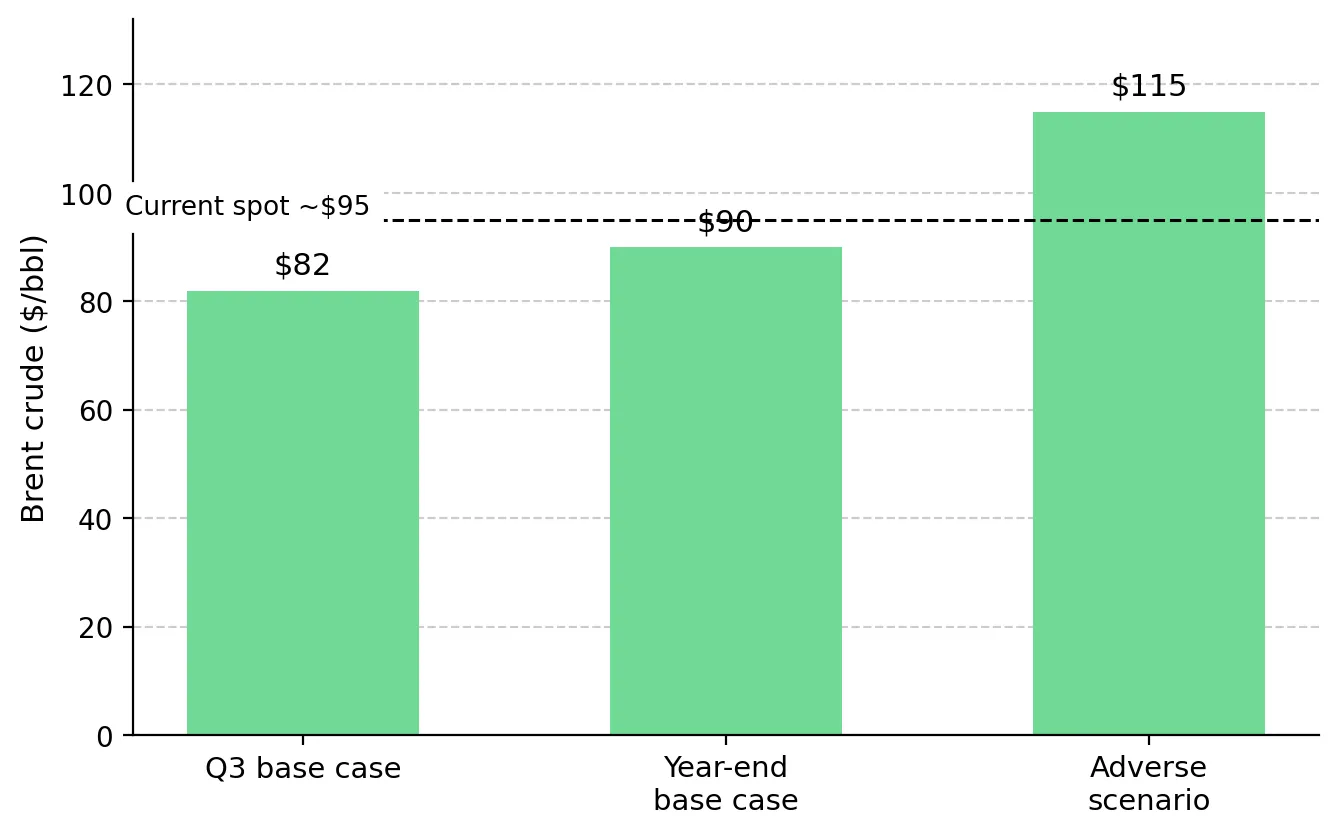

- Goldman Sachs' base case puts Brent near $90 into year-end even if Hormuz reopens, because the risk premium now sits in long-dated forwards.

- About 20% of global oil and LNG transits Hormuz, and movement remains coordinated by Iran's Revolutionary Guard rather than open commercial lanes.

- The US Trade Representative proposed 25% Section 301 tariffs on many Brazilian goods on June 2, exempting beef, coffee, and aircraft parts, with written comments due July 1 and a hearing July 6.

- Brent sustained below Goldman's $82 Q3 base case marks faster normalization; confirmed routine commercial transits through Hormuz are the event that unwinds the premium.

A Strait of Hormuz Reopening May Keep Brent Near $90 Rather Than Trigger a Sharp Selloff

Brent crude surged above $95 per barrel after Iranian state media reported that Tehran was preparing to fully close the Strait of Hormuz. Prices eased the following day after President Donald Trump said US-Iran negotiations would likely "work out well," reducing immediate fears of a prolonged disruption. However, the market response highlights that geopolitical risk premiums do not necessarily disappear as quickly as they emerge.

Andrew Tilton, Goldman Sachs' chief Asia-Pacific economist, said the firm's base case still calls for Brent to average around $90 per barrel through year-end even if the Strait of Hormuz reopens. Energy equities may not face the rapid valuation reset that many ceasefire or de-escalation headlines imply, while traders betting on an immediate collapse in oil prices could find that supply-risk premiums remain embedded in the market longer than expected.

Oil's Risk Premium May Take Months to Unwind After a Hormuz Reopening

Approximately 20% of global oil and LNG trade passes through the Strait of Hormuz, and shipping activity remains dependent on security conditions rather than normal commercial flows. Even if the waterway reopens immediately, consultancy Wood Mackenzie estimates that Middle Eastern energy supply chains could require months to normalize, limiting how quickly the market can unwind disruption-related pricing.

Rather than disappearing with a single de-escalation headline, the geopolitical risk premium has shifted further out along the forward curve, signaling that traders expect elevated supply risks to persist beyond the immediate crisis. As long as European and Asian refiners continue seeking alternative supplies, US crude producers and LNG exporters may continue to benefit from stronger demand for non-Gulf energy exports.

Investors Can Price Oil's Risk Premium More Easily Than a Ceasefire Timeline

With Brent trading near $95 per barrel, the more investable thesis is to position around observable supply constraints rather than attempt to predict diplomatic outcomes. This continues to favor US crude producers and LNG exporters that benefit from elevated energy prices, while fuel-intensive industries such as European and Asian refiners and chemical manufacturers remain exposed to higher input costs until the futures curve normalizes.

Markets cannot reliably forecast whether Washington and Tehran reach an agreement within days or weeks, nor whether regional ceasefires remain intact. Framing an investment around a specific diplomatic deadline turns the trade into a binary event bet. By contrast, using Goldman Sachs' base-case Brent forecast of roughly $90 per barrel while stress-testing against its $115 adverse scenario provides a framework based on probabilities rather than predictions.

Tanker Traffic & Crude Inventories Will Signal When Oil Risks Are Easing

The signal that matters is not a ceasefire announcement but a sustained normalization of physical energy flows. Brent remains elevated because transit through the Strait of Hormuz is still constrained and coordinated under heightened security conditions rather than operating as a fully open commercial shipping route. As long as those restrictions persist, the market has reason to maintain a geopolitical risk premium.

Investors looking for confirmation that the premium is unwinding should focus on measurable indicators rather than political statements. Several consecutive weeks of normalizing tanker traffic through Hormuz, combined with rising US commercial crude inventories in the weekly EIA Petroleum Status Report, would suggest that supply chains are adjusting and physical constraints are easing. A sustained move in Brent below Goldman Sachs' $82 per barrel Q3 base-case forecast would provide additional evidence that the market is removing disruption-related pricing faster than expected.

Analyst's Notes

Subscribe to Our Channel

Stay Informed