330,000-Tonne Copper Deficit Forecast & Chilean Production Shortfalls Increase the Value of New Mine Supply

Copper supply deficits, Chilean production shortfalls, and rising demand from electrification and AI are increasing the value of new copper projects.

- J.P. Morgan projects a 330,000-tonne refined copper deficit in 2026, while production shortfalls at Chile's Codelco are reducing supply from the world's largest copper producer and increasing the risk of higher copper prices.

- A projected copper supply deficit increases the value of producers and developers that can bring new copper supply to market, particularly in jurisdictions outside Chile.

- US Section 232 copper tariffs are widening the price gap between COMEX and the London Metal Exchange, increasing the value of refined copper production that meets COMEX delivery standards.

- Any reduction in US-Iran tensions could lower the geopolitical premium in copper prices, but the projected 2026 supply deficit remains the more important driver of long-term copper equities.

- Investors seeking exposure to higher copper prices can invest across developers, explorers, and brownfield restarts, but project, financing, and execution risks increase further down the development curve.

Copper entered 2026 with a first-quarter surplus but a projected full-year deficit. The refined copper market recorded a surplus of roughly 386,000 tonnes in the first quarter, but supply growth is expected to fall short of demand growth over the next several years. J.P. Morgan projects a refined copper deficit of approximately 330,000 tonnes in 2026, meaning global consumption is expected to exceed refined metal production. The London Metal Exchange three-month copper price has held near $13,500 per tonne, about 7% below the record $14,527.50 reached on 29 January 2026.

The refined copper market and the concentrate market should be distinguished because shortages in one do not always translate into shortages in the other. Refined copper is the finished cathode used in electrical wiring and busbars. Concentrate is the intermediate product mined ore is processed into before smelting. The refined market can show a short-term surplus even when concentrate supply remains constrained, limiting future refined metal production.

Copper demand continues to grow across power, transport, defence, and data-centre infrastructure. Grid expansion, electrification, electric vehicles, defence systems, and AI data centres all increase copper consumption. The key uncertainty is whether mine supply can grow fast enough to meet that demand. If copper demand continues to rise while Chilean supply growth remains constrained, producers and developers that can add new supply may attract capital and command higher valuations.

Codelco Production Shortfalls & Rising Value of Alternative Copper Supply

Concerns about future copper supply are increasingly focused on Codelco, the world's largest copper producer. Chile's state-owned Codelco is the world's largest copper producer, but recent production setbacks have raised concerns about its ability to increase output.

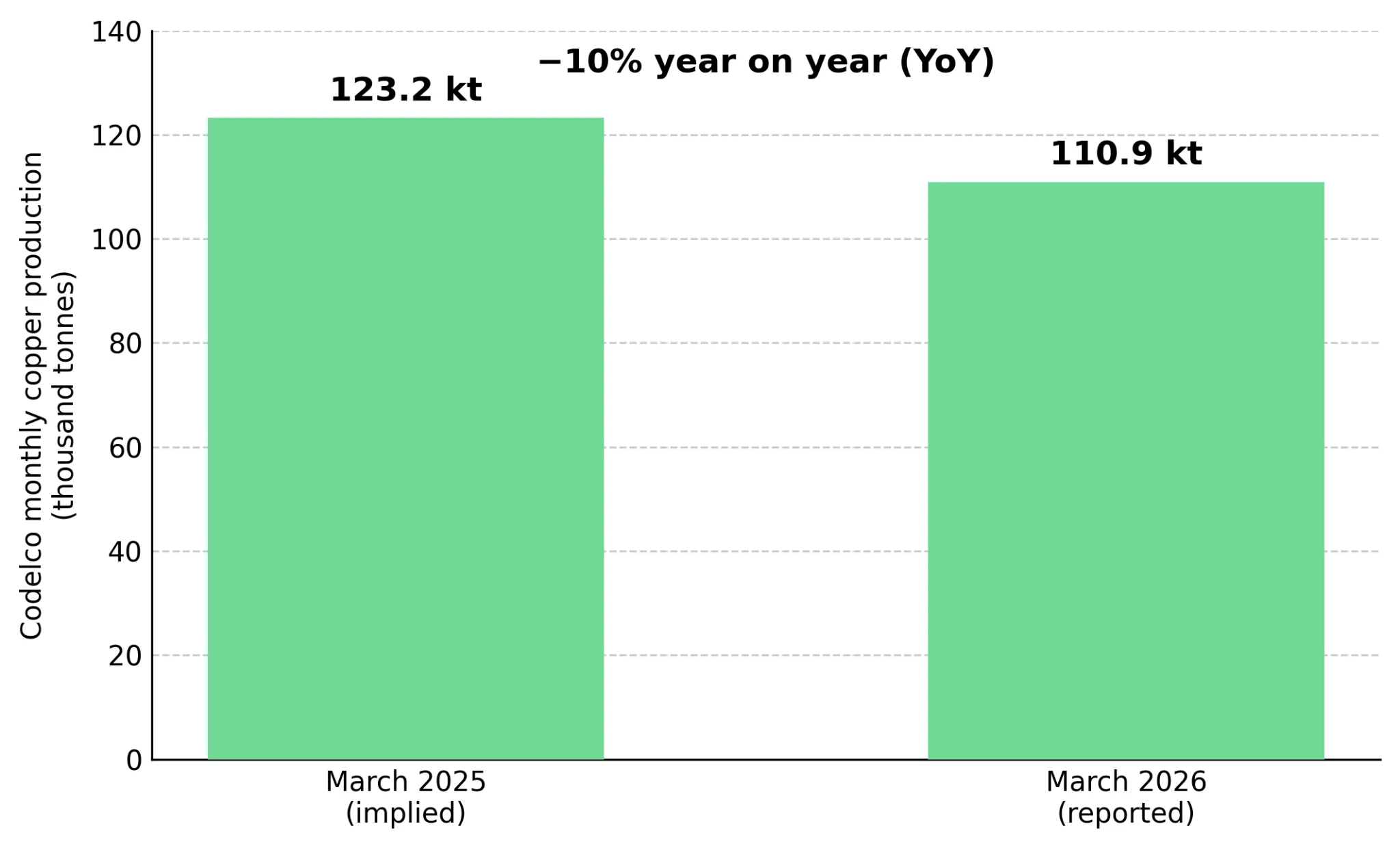

Following an internal audit, Codelco acknowledged that its 2025 production figure was overstated by roughly 26,875 tonnes, triggering executive departures, a criminal complaint, and disputes with unions. The corrected figure implies Codelco's output fell to its lowest level since 1998. March production fell 10% year on year to 110,900 tonnes, according to Cochilco data reported by Reuters. A magnitude 6.9 earthquake near Calama in late May did not affect production beyond 24 hours, but it highlighted the concentration of global copper supply in Chile.

Heavy reliance on one producer can increase valuations for companies with advanced copper projects in other jurisdictions. It also increases the importance of resource quality because higher-confidence resources are easier to finance and develop. An inferred resource has the lowest geological confidence, followed by indicated and then measured resources. Upgrading tonnes from inferred to indicated reduces geological uncertainty, improves financing prospects, and can increase project value when new copper supply is scarce.

Section 232 Tariffs & Premium Valuations for Refined Copper Assets

US copper tariffs are changing trade flows and increasing the value of some copper assets. Under Section 232, the US changed its copper tariff rules in April 2026 so duties apply to the full customs value of covered products. The Commerce Secretary is due to report on refined copper by 30 June 2026, a decision that could lead to tariffs of 15% in 2027 and 30% in 2028. The policy has already widened the gap between COMEX and London copper prices and encouraged copper inventories to build in US warehouses. Tariffs on refined copper can increase margins for producers that sell cathode into US-accessible supply chains.

Marimaca Copper is developing a northern Chile copper project that produces cathode through heap leaching and SX-EW, aligning its output with demand for refined copper. Oxide ore can be processed directly into cathode through SX-EW, avoiding smelting and reducing processing complexity. Marimaca's 2025 definitive feasibility study reported a post-tax NPV of US$709 million at US$4.30 per pound copper, a 31% IRR, US$587 million in pre-production capital expenditure, capital intensity of roughly US$11,700 per tonne of capacity, and a 2.5-year payback based on planned cathode production of 50,000 tonnes per year. These figures are based on company disclosures and have not been independently verified.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, explains why the company is advancing the Marimaca Oxide Deposit toward production rather than pursuing an early exit:

"We do see a significant amount of value to be created while pushing ahead on the Marimaca Oxide Deposit and moving towards a construction decision and going to FID and turning ourselves into a producer while exploring in parallel."

Concentrate Scarcity & Rising Value of High-Grade Copper Deposits

While tariffs may benefit cathode producers, concentrate shortages increase the value of new copper discoveries. Benchmark treatment and refining charges (TC/RCs), the fees miners pay smelters to process concentrate, fell toward $0 per tonne in 2026, while the China Smelters Purchase Team agreed to cut production by more than 10%. A TC/RC near zero indicates that concentrate supply is scarce relative to available smelting capacity. In a concentrate-constrained market, higher-grade deposits can generate wider operating margins because they produce more metal per tonne mined. Grade is measured as copper percentage or copper-equivalent percentage, which includes the value of by-product metals. Higher grades also increase the amount of ore above the cut-off grade, the minimum grade that can be mined profitably.

Abitibi Metals provides an example of the grade thesis through its B26 polymetallic deposit in Quebec, held in an 80-20 joint venture with SOQUEM. The resource includes 12.96 million tonnes indicated at 2.08% copper-equivalent and 12.34 million tonnes inferred at 2.20% copper-equivalent. A recent drill intercept returned 1.48% copper-equivalent over 46.7 metres, including 4.04% copper-equivalent over 14 metres, exceeding the company's current block-model grades and supporting the potential for resource growth. These results remain exploration intercepts and have not yet been incorporated into an updated resource estimate or mineral reserve.

Jonathon Deluce, Chief Executive Officer of Abitibi Metals, explains why the scarcity of large, high-grade copper deposits may increase their value in a concentrate-constrained market:

"The consistency is how rare these deposits are in the marketplace. There's very few of these available across Canada that have the size and scale like B26."

Heap-Leach Partnership Could Generate Non-Operated Cash Flow from Buen Retiro's Oxide Copper Discovery

Fitzroy Minerals provides exposure to near-surface oxide copper exploration in Chile. At Buen Retiro, drilling returned near-surface oxide intercepts including 78 metres at 1.70% copper, including 40 metres at 3.02% copper. Oxide ore can be processed through leaching rather than flotation and smelting, which can reduce processing costs and capital requirements. The company is targeting a maiden mineral resource estimate in the fourth quarter of 2026 and an initial pre-feasibility study in the first quarter of 2027.

Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, explains how the company's planned heap-leach partnership could accelerate cash generation from its oxide copper discoveries:

"That gives us the potential for near-term non-operated cash flow which we think will distinguish us from many, many other explorers in the market."

Copper Supply Deficit & Different Paths to New Production

New copper supply can come from permitted developers, brownfield mine restarts, or greenfield discoveries still defining their first resource. Each pathway carries different development timelines and financing requirements, but a projected copper deficit increases the value of projects that can reach production sooner.

Selkirk Copper is advancing a brownfield restart of the former Minto mine in the Yukon, a development pathway that can shorten the time to production. A brownfield restart can use existing infrastructure that a greenfield project would need to build. The bankruptcy of the previous operator also removed a precious-metals stream and a concentrate offtake agreement, leaving only a 1.5% net smelter return royalty based on metal sales. The resource contains 12.6 million tonnes indicated at 1.20% copper and 23.7 million tonnes inferred at 1.05% copper, with a preliminary economic assessment targeted for mid-2026. The Selkirk First Nation holds roughly 18% equity and two board seats, aligning local stakeholders with the project's development. Project economics beyond existing study work remain targets rather than demonstrated results.

Colin Joudrie, President and Chief Executive Officer of Selkirk Copper, quantifies how existing infrastructure can reduce capital requirements and accelerate a brownfield mine restart:

"Over $330 million has been spent on the above-ground infrastructure. If we had to go do that in a greenfield setting today, you're probably looking at $800 to 900 million US to get it back into production."

Shallow High-Grade Intercepts Point to a District-Scale Copper-Gold Discovery in Argentina's Vicuña Belt

Mogotes Metals offers exposure to greenfield copper-gold exploration in Argentina's Vicuña district, the kind of discovery still defining its first resource. At the Albor target on its Filo Sur project, a discovery hole returned 86 metres at 0.7% copper, 0.55 g/t gold, 2.7 g/t silver and 169 ppm molybdenum from 108 metres depth, including a higher-grade core of 43 metres at 1.1% copper, 0.82 g/t gold, 4.0 g/t silver and 281 ppm molybdenum.

The shallow starting depth reduces the strip-ratio exposure that can weigh on early-stage porphyry economics, and the result marked the company's second copper-gold-silver-molybdenum discovery in a single inaugural drilling season, strengthening the case for a district-scale system along the regional Macho Muerto Fault Zone. With approximately C$40.1 million in cash as of June 2026, Mogotes is funded for a follow-up campaign without an immediate return to equity markets. These results remain exploration intercepts and have not yet been incorporated into a mineral resource estimate.

Heap-Leach Startup Could Lower Initial Capital Requirements While Advancing a Larger Copper System

Cobra Resources provides exposure to early-stage copper and rare earth exploration in South Australia. At Blue Rose, drilling has traced copper-gold mineralisation over 1.6 kilometres of strike, including 74 metres grading more than 1% copper. The company is testing whether the system is linked to a deeper porphyry source that could support a larger resource. At Boland, Cobra is evaluating the recovery of dysprosium and terbium through in-situ recovery, a method that can reduce development and operating costs compared with conventional mining.

Rupert Verco, Managing Director of Cobra Resources, outlines a staged development strategy designed to lower upfront capital requirements while advancing a larger copper system:

"You've probably got a low-cost, low-capex startup treating it heap leach, and then a standard flotation circuit to treat your primary sulphide mineralisation."

If demand from grid expansion, electrification, and AI data-centre infrastructure continues to grow, projects capable of adding copper supply through lower-capital development pathways could become increasingly important to meeting future demand.

The Investment Thesis for Copper

- A projected refined copper deficit of about 330,000 tonnes in 2026, combined with demand growth from electrification, power grids, and data centres, supports investment in companies that can add new copper supply rather than in copper prices alone.

- Production setbacks at Codelco increase the value of developers and explorers operating in jurisdictions with established permitting processes and lower political risk.

- US tariffs on refined copper can increase margins for producers and developers that supply cathode into US-accessible markets.

- A treatment and refining charge near zero signals concentrate scarcity, increasing the value of high-grade deposits that can generate wider operating margins above cut-off grade.

- Brownfield mine restarts can reach production faster and with lower capital requirements than greenfield projects, while greenfield discoveries offer greater upside potential but carry higher geological, permitting, and financing risk.

- Junior mining equities face dilution, permitting, financing, and execution risks. Resource estimates and preliminary studies are not reserves, so investors should assess NPV sensitivities, all-in sustaining costs where available, and available funding before investing.

Copper demand continues to grow, but the key question for investors is which projects can add new supply and where that supply will come from. Production setbacks at Codelco and the widening gap between London and US copper prices have increased the value of companies that can deliver new copper supply, particularly refined copper for US markets.

Any reduction in US-Iran tensions could lower the geopolitical premium in copper prices, but it does not change projections for a multi-year copper supply deficit. Investors should evaluate developers, explorers, and brownfield restarts based on jurisdiction, grade, financing, and expected time to production rather than short-term movements in copper prices. With new copper supply failing to keep pace with demand growth, the strongest investment opportunities may come from companies that can bring additional production to market.

TL;DR

J.P. Morgan forecasts a 330,000-tonne refined copper deficit in 2026 as demand from power grids, electrification, electric vehicles, defence systems, and AI data centres outpaces mine supply growth. Production setbacks at Codelco, the world's largest copper producer, are increasing concerns about future supply, while US copper tariffs are creating premiums for refined copper assets. Concentrate shortages are raising the value of high-grade deposits, and investors are increasingly focusing on developers, brownfield restarts, and explorers capable of bringing new copper supply to market. The key investment opportunity lies in companies that can add production efficiently in a market where supply growth is struggling to keep pace with demand.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed