US Copper Tariffs Increase the Value of Allied Supply as Deficits Reach 640,000 Tonnes

US copper tariffs are widening ex-US shortages, driving a 640,000-tonne copper deficit and increasing the value of allied-jurisdiction refined supply.

- US trade policy has become a key driver of regional copper pricing, with a Section 232 proclamation taking effect on June 8and a refined-copper tariff decision due on June 30.

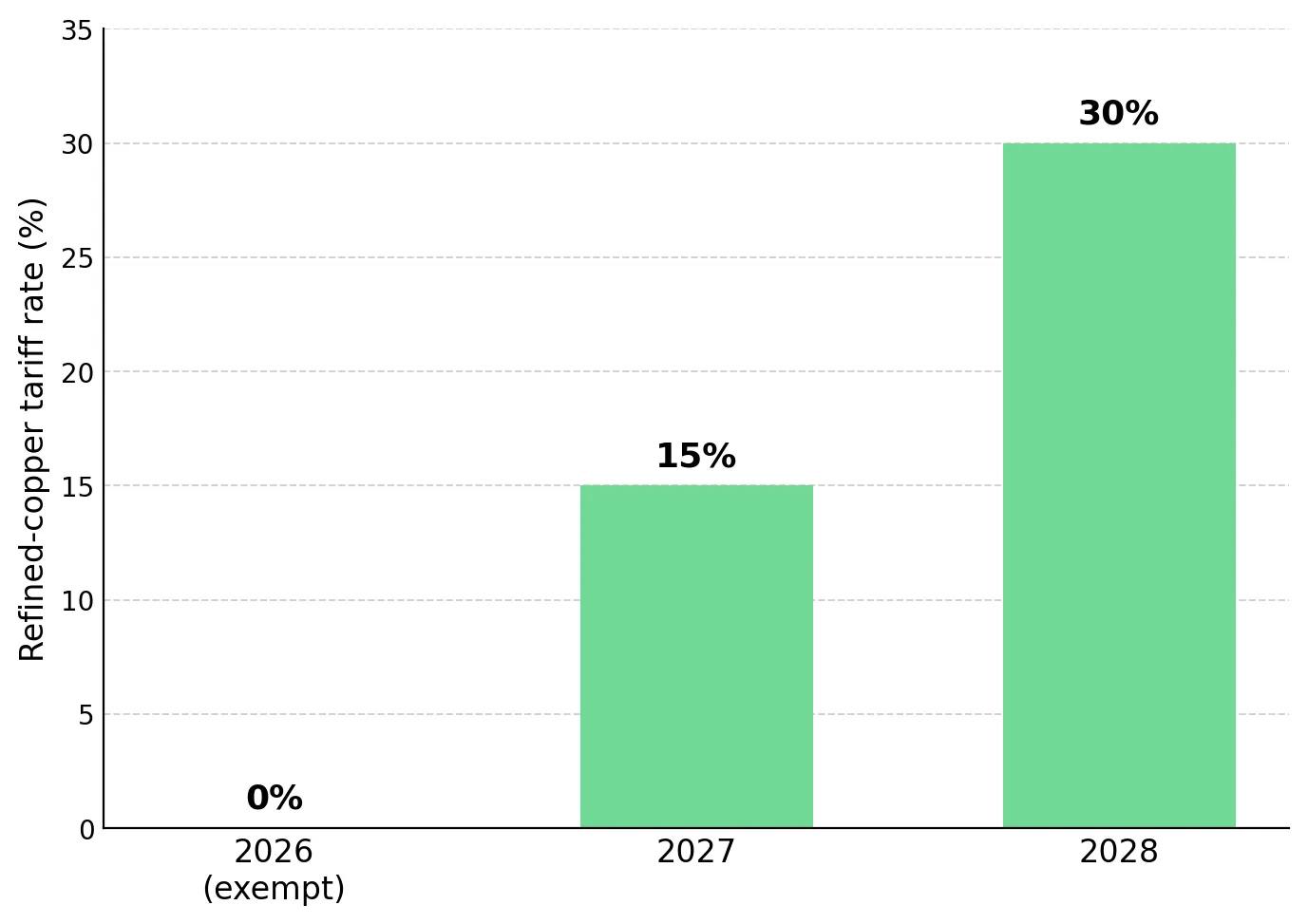

- A 50% tariff on semi-finished copper, while refined cathode remains exempt, has created a two-tier market and encouraged importers to move copper into the US ahead of potential future duties.

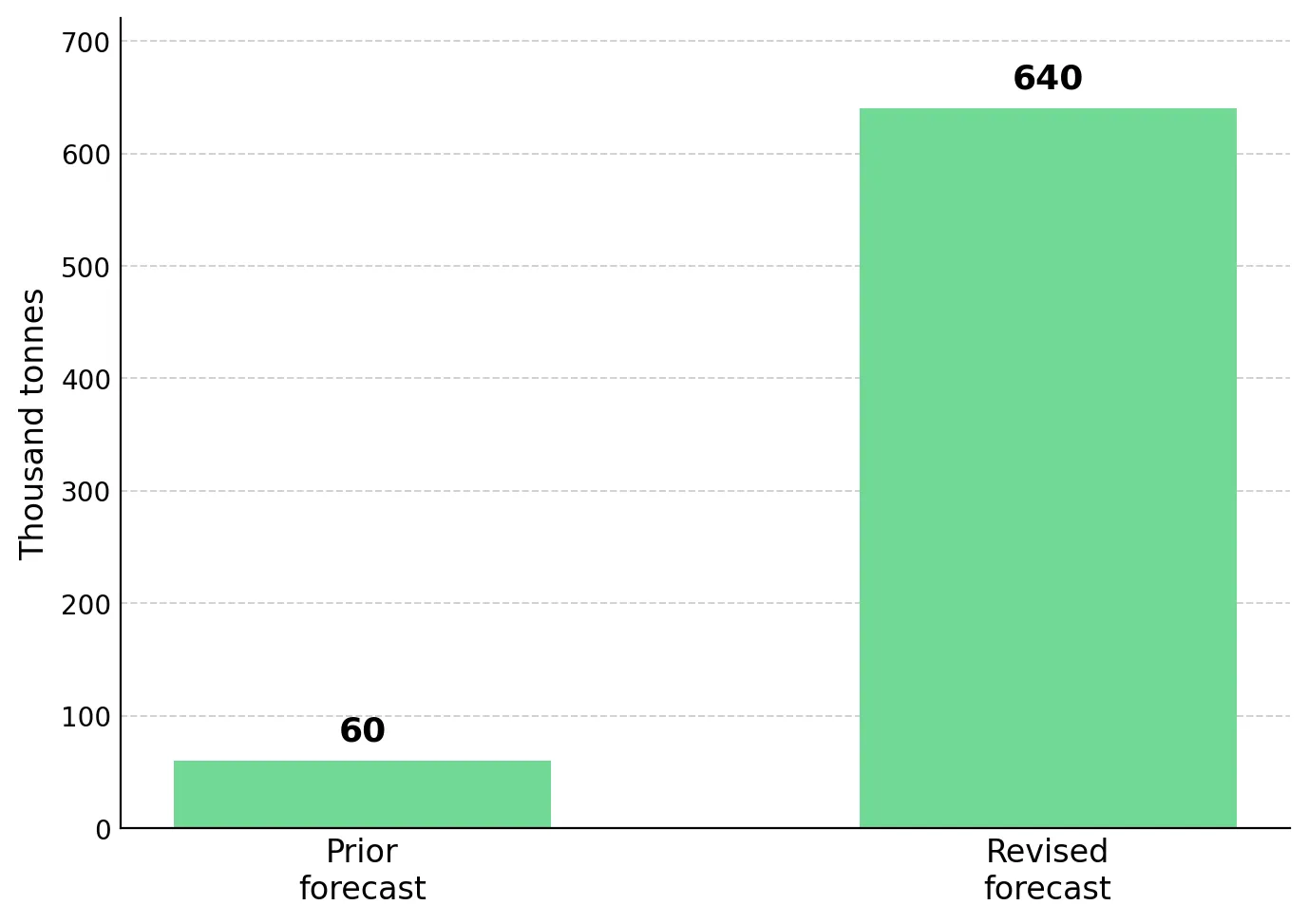

- Goldman Sachs Research has raised its copper deficit forecast outside the US to roughly 640,000 tonnes from about 60,000 tonnes, while Shanghai inventories have fallen to a yearly low, indicating that copper shortages are increasingly concentrated outside the US.

- US tariff policy has increased the value of assets in allied jurisdictions, particularly those with access to refined-copper production and funding for near-term development.

- Developers and explorers in Chile, Canada and Australia offer varying exposure to this theme, but most have no reserves or economic studies and remain highly dependent on exploration success.

US Copper Tariffs Drive Regional Price Formation

For most of the past decade, copper demand from electrification grew faster than mine supply, supporting the long-term investment case for the metal. In 2026, US trade policy has become an additional driver of copper pricing. Section 232 tariffs have increased the influence of US trade policy on regional copper prices by changing the economics of importing copper products. Since the initial 2025 action, the US has expanded the policy by applying duties to the full customs value of imports on April 6, 2026 and lowering the domestic-content threshold for preferential treatment from 95% to 85% effective June 8.

US tariffs are widening regional price differences by restricting trade flows in a market that already faces a copper supply deficit. J.P. Morgan Global Research and Goldman Sachs Research identify the pending refined-copper decision as a key near-term catalyst for copper prices. A refined-copper tariff would likely increase the value of domestic and allied supply, while a delay to the June 30 decision could reduce stockpiling demand and pressure copper prices.

US Tariffs Create a Two-Tier Copper Market

The 50% tariff applies to semi-finished and copper-intensive derivative products, while refined copper cathode remains exempt. The exemption, combined with a proposed refined-copper tariff of 15% in 2027 rising to 30% in 2028, has encouraged importers to bring refined metal into the US ahead of any future duty. As a result, copper has moved toward the US to capture tariff-related pricing differences between regions.

Importers brought an estimated 500,000 tonnes into the US in a single month, versus normal monthly imports of about 70,000 tonnes, lifting US copper premiums while London inventories tightened and Shanghai inventories fell to a yearly low. Goldman Sachs Research raised its forecast copper deficit outside the US to roughly 640,000 tonnes from about 60,000 tonnes and cut its 2026 global mine supply estimate by about 350,000 tonnes following disruptions at Grasberg in Indonesia and Kamoa-Kakula in the Democratic Republic of Congo.

Copper shortages outside the US reflect both trade policy and limited concentrate supply. Treatment and refining charges, a key indicator of concentrate availability, have fallen toward zero in some 2026 benchmark agreements. This indicates that concentrate supply remains tight regardless of tariff policy, supporting copper prices even without trade-related stockpiling.

US Tariffs Increase the Value of Allied-Jurisdiction Copper Assets

US tariff policy increases the value of copper assets in allied jurisdictions by improving their access to tariff-advantaged markets. Faster permitting, existing infrastructure and political stability can shorten development timelines and reduce discount rates, increasing the relative value of assets in allied jurisdictions.

Canada is a key beneficiary of investor interest in allied-jurisdiction copper assets. In Quebec, Abitibi Metals holds the B26 polymetallic deposit with 25.3 million tonnes grading more than 2.1% copper equivalent across indicated and inferred resources. A Preliminary Economic Assessment targeted for the first quarter of 2027 could increase confidence in a portion of the inferred resource and advance project evaluation. SOQUEM, a subsidiary of Investissement Québec, holds a 20% stake in the project, while Eldorado's roughly C$3.8 billion acquisition of Foran Mining highlights market demand for large copper assets in Canada.

Mogotes Metals provides earlier-stage exposure to copper discovery in Argentina's Vicuña district, where the company reported a second copper-gold-silver-molybdenum discovery during its inaugural 2025-2026 drill campaign at Filo Sur. The Albor target returned 86 metres grading 0.7% copper, 0.55 g/t gold, 2.7 g/t silver and 169 ppm molybdenum from 108 metres depth, including a higher-grade interval of 43 metres grading 1.1% copper and 0.82 g/t gold. Unlike developers with defined reserves or economic studies, Mogotes remains exploration-stage and its valuation depends on continued drilling success. However, with approximately C$40.1 million in cash and 3,681 metres of drilling still awaiting assay results, investors gain exposure to district-scale copper discovery potential in a jurisdiction that could benefit from growing interest in allied copper supply.

Existing Infrastructure Lowers Capital Requirements at Minto

Selkirk Copper provides exposure to a brownfield copper restart in the Yukon. The Minto project is a past-producing mine with 12.6 million indicated tonnes grading 1.20% copper and 23.7 million inferred tonnes grading 1.05% copper, while First Nation control may support community alignment during project redevelopment. The investment case depends on lower capital requirements, as most new copper projects require significant infrastructure spending before production.

M. Colin Joudrie, President and Chief Executive Officer of Selkirk Copper, explains how existing infrastructure could reduce development capital requirements at Minto:

"We don't have to build a power line, we don't have to build a road, we don't have to build the above ground facility. Over $330 million has been spent in the above ground infrastructure, processing plant, roads, and underground."

Refined-Copper Tariffs Increase the Value of Cathode Production

If the June 30 ruling extends duties to refined copper, producers and developers of cathode in allied jurisdictions would have the most direct exposure to the policy. Oxide deposits can produce refined cathode through heap leaching and electrowinning, typically at lower capital cost than sulphide projects that require concentrators. As a result, oxide projects with planned cathode production may benefit more from refined-copper tariffs than concentrate-producing projects.

Oxide Expansion Could Increase Cathode Production by 50%

Marimaca Copper's Oxide Deposit contains proven and probable reserves of 179 million tonnes grading 0.42% copper, supporting a planned 50,000-tonne-per-annum cathode operation in Chile that the company states is permitted and self-financeable. Near-term upside depends on expanding cathode production, while Pampa Medina remains an exploration target rather than a defined resource.

Hayden Locke, Chief Executive Officer of Marimaca Copper, outlines the company's plan to increase cathode production by 50% through the Pampa Medina oxides:

"We see a very real short-term opportunity to expand our cathode production from 50,000 tons to 75,000 tons per annum through the Pampa Medina oxides."

Heap-Leach Development Offers a Lower-Capital Path to Copper Production

Fitzroy Minerals is exploring an oxide copper project in Chile that could support future cathode production. Buen Retiro has returned shallow oxide intercepts including 78 metres at 1.70% copper, while a heap-leach pre-feasibility study and partnership with Pucobre support a maiden mineral resource estimate targeted for the fourth quarter of 2026. While the potential for a larger iron-oxide-copper-gold system remains unproven, the oxide project could support a lower-capital development route if further work is successful.

Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals, explains how the company's heap-leach development strategy could generate near-term cash flow while maintaining a low-capital route to copper production:

"That operation gives us the potential for near-term non-operated cash flow which we think will distinguish us from many other explorers in the market. This would give us non-operated cash flow and a very, very low capital intensity."

Tariff Uncertainty Increases the Value of Fully Funded Copper Developers

Uncertainty around the June 30 tariff decision favours companies funded through near-term milestones and increases risk for projects that require future equity financing. Equity financings and warrants can reduce existing shareholders' ownership and are common funding tools for junior mining companies. Higher interest rates reduce the value of long-dated project cash flows and make capital-intensive developments less attractive.

Funding Through Key Milestones Reduces Dilution Risk

Abitibi Metals is funded through key development milestones without issuing warrants. The company's C$31 million financing was completed without warrants and funds an 80,000-metre-plus drill programme, a planned Preliminary Economic Assessment and feasibility work, reducing future shareholder dilution risk.

Jonathon Deluce, Chief Executive Officer and Founder of Abitibi Metals, explains how the company's C$31 million financing funds key development milestones while avoiding warrant-related shareholder dilution:

"This injects $31 million and we now have a war chest to deliver 80,000 metres plus of drilling, to deliver the PEA and put a huge dent into our feasibility study. We are not issuing any warrants, which keeps everybody on a similar playing field without any capping on the stock."

Exploration Success Remains Critical to Unlock Project Value

Cobra Resources provides earlier-stage copper exploration exposure than the other companies discussed. The Blue Rose copper prospect in South Australia has returned near-surface copper intercepts but has no defined resource or reserve, while a fully funded diamond drilling programme is testing for a deeper source. The project remains pre-revenue, and its value depends on drilling success and future financing.

Rupert Verco, Managing Director of Cobra Resources, explains the development concept that successful drilling could support as the company works to define the scale and economics of the project:

"You've probably got a low cost, low capex startup treating it as heap leach, and then you have a standard flotation circuit to treat your primary sulphide mineralisation."

The June 30 refined-copper ruling will test whether trade policy can continue to reshape regional copper markets. With an estimated 640,000-tonne copper deficit outside the US and concentrated supply remaining tight, policy decisions are becoming an increasingly important driver of copper prices alongside traditional supply and demand fundamentals.

The Investment Thesis for Copper

- Trade policy has increased the impact of copper supply shortages, making the refined-copper ruling a key catalyst that could widen price differences between the US and other markets and increase the value of secure refined supply.

- Developers in allied jurisdictions that are advancing cathode production would benefit most from a refined-copper tariff because they produce the metal directly affected by the policy.

- Jurisdictions with predictable permitting, existing infrastructure and government or community support can shorten development timelines and improve project economics.

- Companies funded through their next major milestones face less financing risk and shareholder dilution than peers that may need additional capital in a higher-interest-rate environment.

- Brownfield restart projects with existing infrastructure often require less upfront capital than greenfield developments, improving project economics when discount rates are high.

- Exploration upside and critical-minerals exposure should be assessed against defined resources and economic studies, since exploration targets are not reserves and early-stage projects can fail to reach production.

US trade policy is increasingly determining where copper shortages emerge and how copper is priced across regions. The estimated 640,000-tonne copper deficit outside the US reflects both trade policy and supply constraints, increasing investor interest in refined-copper projects located in allied jurisdictions. The companies discussed illustrate different ways investors can gain exposure to refined-copper production, brownfield restarts and early-stage exploration. The June 30 ruling will test the thesis. This analysis is intended as market context, not investment advice, and outcomes remain uncertain.

TL;DR

US trade policy has become a major driver of copper pricing, creating a two-tier market where refined copper remains exempt from tariffs while other copper products face duties. This has pulled large volumes of copper into the US, contributing to a projected 640,000-tonne deficit outside the country. As a result, investors are increasingly favoring allied-jurisdiction copper assets, cathode-producing projects, brownfield developments with existing infrastructure, and companies funded through key development milestones ahead of the June 30 refined-copper tariff decision.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed