US Critical Minerals Designation & Nuclear Funding Position Uranium for a 2026 Contracting Cycle

US Critical Minerals designation and $80B nuclear funding position uranium for a 2026 contracting cycle as utilities face unavoidable purchasing pressure.

- US designation of uranium as a Critical Mineral marks a structural policy shift that elevates domestic supply security from a market issue to a national priority.

- An estimated $80 billion in US nuclear funding and rising electricity demand from AI data centers are tightening long-term uranium demand visibility.

- A prolonged utility under-contracting cycle has created pent-up demand that must be addressed in 2026, irrespective of short-term spot volatility.

- Uranium equities are acting as leading indicators, pricing in higher incentive prices ahead of physical contracting.

- Producers, developers, and explorers in tier-one jurisdictions with permitting momentum are increasingly differentiated in investor portfolios.

Policy Reframes Uranium From Commodity to Strategic Asset

Late 2025 marked an inflection point for uranium's role in US energy policy. The inclusion of uranium on the US Critical Minerals List by the US Geological Survey represents more than a symbolic gesture; it materially alters capital access, permitting timelines, and the scope of government participation in the sector. For producers and developers operating in domestic jurisdictions, this designation opens pathways to preferential financing, streamlined environmental review, and potential inclusion in strategic reserve programs.

Strategic Reserve & Section 232 Implications

The policy architecture now under consideration extends beyond classification. A Strategic Uranium Reserve, if implemented, would introduce price-floor mechanisms and offtake support that fundamentally change the risk profile for project developers. The ongoing Section 232 review, expected to be released in the first half of 2026, further signals that the administration views uranium supply through a national security lens, paralleling prior interventions in steel and rare earths. For utilities and investors, the implication is clear: domestic uranium supply is now a matter of strategic priority, not merely economic preference.

Domestic Infrastructure Gains Strategic Premium

This policy environment is reshaping financing conversations across the uranium value chain. Companies with operating US infrastructure are finding that critical-minerals status translates directly into improved terms and expanded access to capital. The White Mesa Mill in Utah, the only conventional uranium mill operating in the United States, exemplifies this dynamic. Facilities with existing permits and operational history now command strategic premiums that were absent in prior cycles when uranium was viewed purely through commodity economics.

Energy Fuels is among US-based producers who are positioning themselves at the center of this policy shift. Mark Chalmers, Chief Executive Officer of Energy Fuels highlights:

"Energy Fuels is a company that is unique from all others because we are focused on building a critical mineral hub that is built around our uranium business but also includes the rare earth suite of elements... If the United States wants to reshore the ability to be independent of China, we have a facility in the United States that's constructed, permitted, and operating to do that."

Nuclear Power & US Industrial Electricity Demand

Nuclear energy currently supplies approximately 19% of US electricity, a baseload contribution that has remained stable for decades. What is changing is the demand side of the equation. AI data centers, electrification of transport, and industrial reshoring are collectively redrawing forward demand curves. Utilities that once planned for flat or declining load growth are now confronting scenarios where reliable baseload power becomes a competitive differentiator.

$80 Billion Reactor Initiative

The announced $80 billion in reactor funding reflects this recalculation. The initiative, structured as a public-private partnership in coordination with the Department of Energy, aims to build ten new reactors with construction beginning in 2030. While new reactor capacity is largely a post-2030 phenomenon, utilities must secure uranium supply well ahead of construction timelines. Fuel procurement cycles for nuclear plants operate on multi-year horizons, meaning that contracting decisions made in 2026 and 2027 will determine supply availability for the next decade.

Global Demand Trajectory

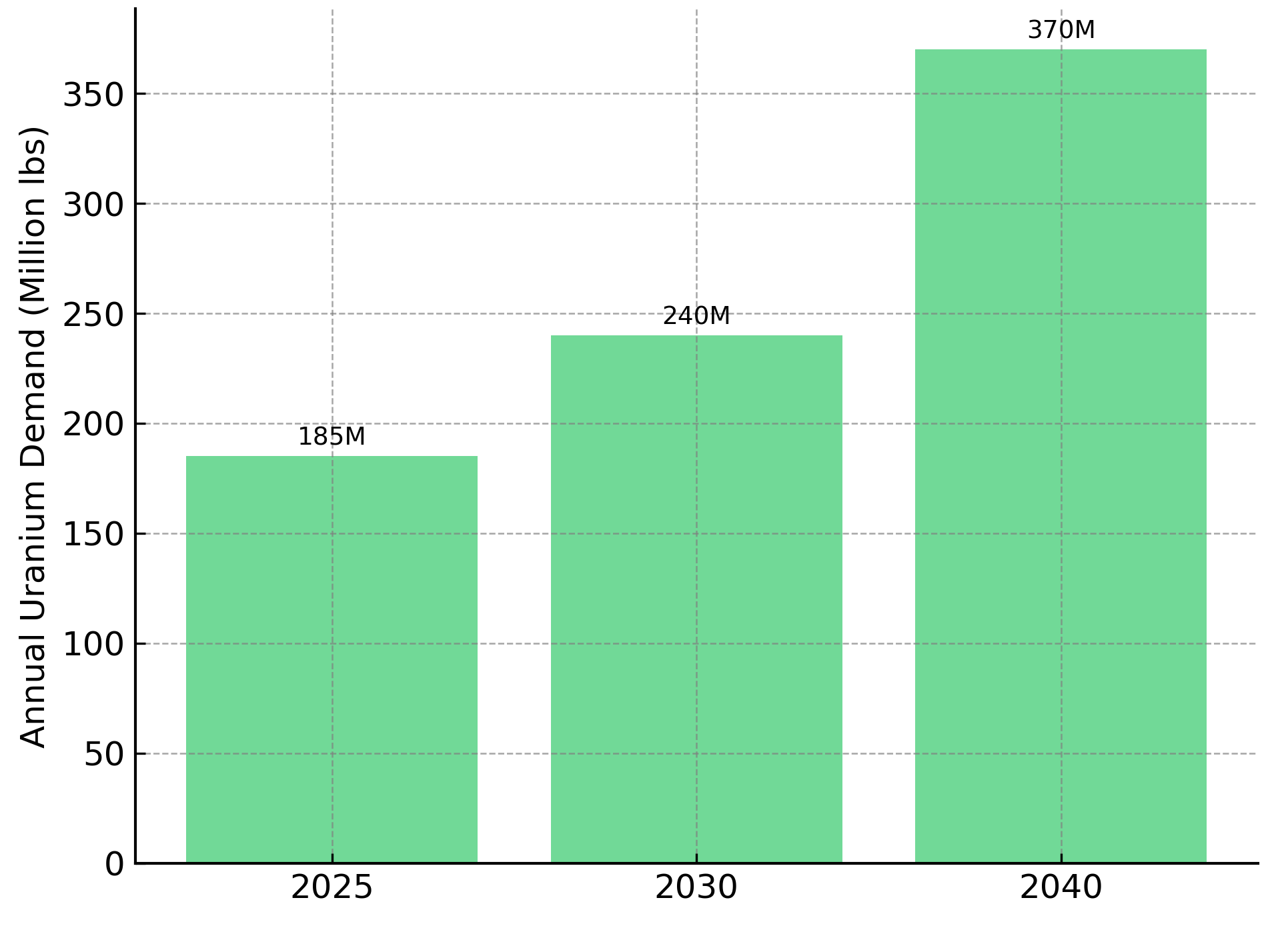

Globally, the demand picture is reinforced by China's accelerated reactor buildout and strategic uranium stockpiling. The shift toward small modular reactors and public-private partnerships aimed at reducing construction timelines adds further optionality to the demand outlook. The World Nuclear Association's 2025 Fuel Report projects that uranium demand will rise by approximately 30% by 2030 and more than double by 2040, a trajectory that would require sustained increases in uranium supply.

The Contracting Stalemate & Why It Cannot Persist

Annual global uranium requirements stand at approximately 185 million pounds, while the replacement contracting rate averages roughly 150 million pounds. Through the first 11 months of 2025, utilities contracted only an estimated 75 million pounds, representing 50% of the replacement rate. This under-contracting reflects a combination of policy uncertainty, price volatility, and utility procurement inertia. However, the fundamental mismatch between consumption and new contracting cannot persist indefinitely.

Producer Discipline & Price Recovery

Producer discipline has been a defining feature of this cycle. Major producers have demonstrated an unwillingness to sign new contracts at prices below long-term incentive levels, effectively withdrawing supply from the market until economics improve. Spot prices have recovered from approximately $63 per pound in April 2025 to the high $70s, with early signs of term price repricing emerging in late 2025. The dynamics suggest that the contracting wave, when it arrives, will occur at prices meaningfully above recent lows.

ISR Operations & Term Price Leverage

In situ recovery operations offer particular leverage to term price normalization given their lower capital intensity and faster production ramp profiles. William Sheriff, Executive Chairman of enCore Energy, describes the operational tempo:

"Our production rate on a daily basis has gone from up 200% to up 300%... Our uranium comes out of the ground quicker than most, we don't have the typical problems that you see on restarts… We felt that the sense of urgency was something that needed to be reinforced."

The capital markets have validated this operational momentum with financing terms that reflect institutional confidence. William Sheriff describes the reception:

"The cost of capital is something we've never seen before in terms of a five and a half percent coupon on a non-secured note… It introduced us to an entirely new level of investor; most of these funds were 10, 20, 30 billion dollar funds… We did 115 million and we were still significantly oversubscribed. "

Equity Markets Signal the Next Phase of the Uranium Cycle

A notable divergence has emerged between modest 2025 spot price performance and strong uranium equity returns. This pattern is consistent with prior uranium cycles, where equities have historically moved 12 to 24 months ahead of physical market inflections. Equity investors are discounting forward term prices, permitting outcomes, and production optionality that have not yet materialized in spot transactions.

Capital Formation & Strategic M&A

The capital markets are also responding to improved balance sheet positioning across the uranium sector. Recent financings have been heavily oversubscribed, with companies accessing both equity and convertible debt at terms that would have been unattainable two years ago. This capital formation is enabling accelerated development timelines and strategic acquisitions that consolidate asset portfolios in favorable jurisdictions.

Investor Preferences & Portfolio Positioning

The investor preference is increasingly for companies with visible permitting milestones, secured funding, and jurisdictional clarity. Producers with operating infrastructure benefit from the near-term term price normalization thesis. Developers with high-grade permitted projects offer leverage to incentive pricing. Explorers with scale in tier-one jurisdictions provide asymmetric upside in a market where new discoveries are increasingly rare.

IsoEnergy is one example of a company structuring its portfolio to participate across multiple stages of uranium development. Philip Williams, Chief Executive Officer of IsoEnergy, outlines the approach:

"We're focusing on the highest grade uranium resource in the world in Canada at the Hurricane deposit... We think about the core four, Hurricane, the Utah assets, Coles Hill, and then Wiluna... The characteristics that we have there at Hurricane, this is a top tier asset, it will be developed into a mine."

Philip Williams also emphasizes the strategic importance of US asset exposure in the current policy environment:

"The uranium supply side is broken in the United States today and this administration is going to do everything it can to fix it... We have a group of assets in the United States that could be a part of the solution to the problem, we have near-term production assets... We have the largest uranium resource in the United States in Virginia, 160 million pounds; this could go a long way to helping solve some of these supply chain issues."

Permitting, Jurisdiction & Execution as Capital Filters

For investors evaluating uranium exposure, the primary risk has shifted from commodity price to execution pathway. Environmental permitting milestones expected in Q1 2026 will determine which projects advance toward production and which remain in development limbo. The differentiation between producers, late-stage developers, and early-stage explorers is becoming more pronounced as capital flows toward companies with clear regulatory visibility.

Jurisdictional Premiums & ESG Factors

Jurisdictional premiums have emerged for Canada, the United States, and Australia relative to higher-risk regions. ESG performance, Indigenous engagement, and regulatory transparency increasingly function as determinants of valuation multiples. In exploration, the combination of scale and tier-one jurisdiction creates re-rating potential that pure grade or resource size cannot replicate.

District-Scale Exploration in the Athabasca Basin

The Athabasca Basin in Saskatchewan remains the global benchmark for high-grade uranium deposits, where intersection widths and grades achieved in recent drilling programs continue to validate the geological thesis.

ATHA Energy demonstrates how district-scale exploration in favorable jurisdictions can create differentiated positioning. Troy Boisjoli, Chief Executive Officer of ATHA Energy, speaking to the company's Anjukuni basin results:

"We have full control over the Anjukuni basin... We found a 31 km long structural trend that cuts across this thing and this is our fourth discovery in a single drill program... I view it as being analogous to exploring in the northeast Athabasca basin circa 1965. We have the opportunity and the ability to be executing on a project that has tremendous scale potential."

Troy Boisjoli further elaborates on the strategic advantage of district-scale control:

"We're in an entire uraniferous basin here... Being in control of a district like we're in has us in a very good position of strength relative to the market and relative to our strategic opportunities."

The Investment Thesis for Uranium

The uranium market is entering a phase where structural policy support, utility procurement pressure, and producer discipline converge. For investors seeking exposure to this cycle, the thesis rests on several reinforcing factors.

- Structural policy support via Critical Minerals designation underpins long-term demand visibility and improves capital access for domestic producers.

- Utility under-contracting through 2025 creates unavoidable purchasing pressure in 2026 and 2027, with procurement decisions concentrated in a narrow window.

- Producers with operating infrastructure and established cost structures benefit first from term price normalization as utilities return to the market.

- Developers with permitted, high-grade projects offer leverage to incentive pricing and production timelines aligned with utility demand.

- Explorers with scale in tier-one jurisdictions provide asymmetric upside in a market where new discoveries are increasingly scarce and permitting timelines extend.

- Equity markets are already discounting higher uranium prices, favoring execution-ready companies with visible milestones and jurisdictional clarity.

Why 2026 Represents an Inflection Year for Uranium Investors

The convergence of policy clarity, infrastructure funding, and utility procurement cycles positions 2026 as an inflection year for uranium markets. Critical Minerals designation removes a key uncertainty delaying utility action. Infrastructure funding and AI-driven power demand lock in long-dated consumption. Producer discipline ensures that new contracts will be struck at economically sustainable prices.

For investors, uranium exposure increasingly becomes a question of which part of the value chain offers the most attractive risk-adjusted returns, not whether the cycle exists. Producers with operating assets, developers with permitted projects, and explorers with district-scale optionality each offer distinct profiles aligned with different investment horizons and risk tolerances. The structural case for uranium has been established; the differentiation now lies in execution.

TL;DR

The US designation of uranium as a Critical Mineral in late 2025 marks a structural policy shift elevating domestic supply to a national security priority. With $80 billion in reactor funding announced and AI data centers driving electricity demand, long-term uranium demand visibility is strengthening. Utilities under-contracted significantly in 2025—only 75 million pounds versus 185 million pounds in annual requirements—creating unavoidable purchasing pressure for 2026-2027. Producer discipline is holding supply off market until term prices reach incentive levels. Equity markets are already pricing in higher uranium prices, with capital flowing toward execution-ready producers, permitted developers, and district-scale explorers in tier-one jurisdictions.

FAQs (AI-Generated)

The US Geological Survey added uranium to the Critical Minerals List in late 2025, recognizing domestic uranium supply as a national security priority rather than merely an economic preference. This designation opens pathways to preferential financing, streamlined permitting, and potential strategic reserve programs.

The initiative aims to build ten new reactors with construction beginning in 2030. Because nuclear fuel procurement cycles operate on multi-year horizons, utilities must secure uranium supply well ahead of construction, meaning contracting decisions in 2026-2027 will determine supply availability for the next decade.

Through late 2025, utilities contracted only an estimated 75 million pounds—roughly 50% of the replacement rate against 185 million pounds in annual global requirements. This reflects policy uncertainty, price volatility, and procurement inertia, but the mismatch cannot persist indefinitely.

Uranium equities historically move 12 to 24 months ahead of physical market inflections. Investors are discounting forward term prices, permitting outcomes, and production optionality that haven't yet materialized in spot transactions.

Canada, the United States, and Australia carry jurisdictional premiums relative to higher-risk regions. ESG performance, Indigenous engagement, and regulatory transparency increasingly function as determinants of valuation multiples.

Analyst's Notes

Subscribe to Our Channel

Stay Informed