AI-Driven Nuclear Expansion & Uranium Deficits: How Rising Energy Requirements Pressure Uranium Supply

AI-driven demand and the Russian uranium ban are boosting supply deficits, creating investment opportunities across uranium producers, developers, and explorers.

Baseload Power Requirements in an AI-Driven Electricity System

The exponential rise of artificial intelligence, hyperscale cloud infrastructure, and grid electrification is materially altering global electricity planning. Data centers are energy-intensive assets requiring uninterrupted baseload supply. Unlike intermittent renewables, nuclear power provides high-capacity-factor output of approximately 90% and zero-carbon baseload generation. The United States is targeting an expansion of nuclear capacity from roughly 100 gigawatts today to 400 gigawatts by 2050, per executive orders issued in May 2025, subject to legislative and regulatory implementation. This shift is occurring alongside reactor life extensions, restart discussions for idled facilities, and policy frameworks emphasizing domestic fuel security.

This demand shift is not cyclical. It represents a multi-decade structural reorientation of energy infrastructure planning with direct implications for uranium procurement strategies at the utility level. William Sheriff, Executive Chairman of enCore Energy, currently in its second year of production across its Alta Mesa and Rosita Central Processing Plants, highlights enCore's operational approach:

"In-Situ Recovery of uranium is our business. We only use In-Situ methods and have been in production now going on our second year, and have expanded operations considerably."

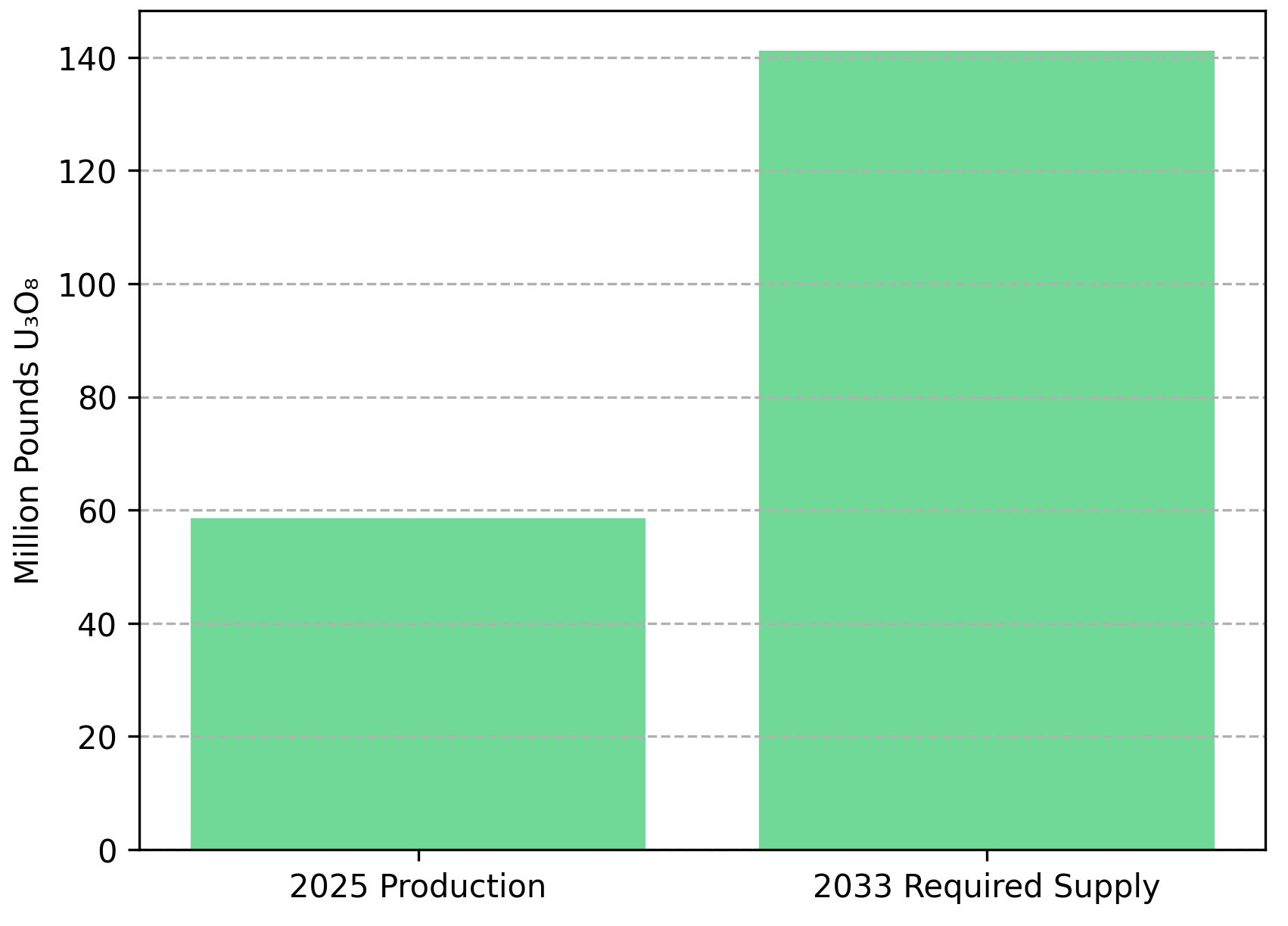

Global Uranium Supply Relative to Projected Reactor Demand

The uranium market is entering this demand expansion phase from a position of structural weakness. For several decades, primary mine supply has lagged reactor demand. Utilities bridged the gap through secondary supplies, government stockpiles, and underfeeding in enrichment markets.

World uranium production in 2025 is approximately 58.5 million pounds of U₃O₈, with supply needing to reach roughly 141.2 million pounds by 2033 - a 2.5-fold increase - to balance projected demand. No single mine or jurisdiction can absorb that shortfall.

Closing a gap of that magnitude requires assets that combine scale, grade, and jurisdictional credibility. In the Athabasca Basin, where geological endowment is concentrated and discovery history is well-established, a small number of deposits carry the grade profile and resource scale to make a meaningful contribution to the Western supply response.

IsoEnergy's Hurricane deposit contains 48.6 million pounds at an indicated grade of 34.5% U₃O₈. Philip Williams, Chief Executive Officer, describes IsoEnergy's dual strategy focus:

"We're focused on restarting production in the United States and on exploring our ultra-high-grade Hurricane deposit in Athabasca, Saskatchewan. We're back in mining at Tony M which really just represents a small-scale mining exercise."

The 2,000-tonne bulk sampling program at Tony M is currently active, with completion targeted for April 2026 and subsequent processing at the White Mesa Mill under toll milling agreements that are in place. Results from the program will inform ongoing technical and economic evaluations preceding a potential production restart decision.

US Uranium Policy, the 2028 Enrichment Ban & Domestic Supply Capacity

The structural supply deficit becomes acute when layered with geopolitical constraints. The United States generates approximately 30% of global nuclear power but holds roughly 1% of global uranium reserves and imports close to two-thirds of its enriched uranium. The Prohibiting Russian Uranium Imports Act restricts Russian enriched uranium imports, with full effect from 2028, subject to existing waiver provisions. This creates a simultaneous gap across mining, conversion, and enrichment.

Western enrichment providers including Centrus Energy, Urenco, and Orano USA are expanding facilities in Ohio, New Mexico, and Tennessee. However, enrichment capacity without feedstock uranium is insufficient. Domestic uranium production becomes strategically critical.

Energy Fuels, which operates the White Mesa Mill, the only currently operating conventional uranium mill in the United States, is positioned at the nexus of this constraint. The facility also processes alternative uranium-bearing feedstock materials and has been producing neodymium-praseodymium oxide through an existing solvent extraction circuit since 2024, establishing it as a multi-commodity processing hub. Mark Chalmers, Chief Executive Officer of Energy Fuels, describes the company's processing advantages:

"We're building a critical mineral hub using our longstanding uranium processing capabilities, but also the ability to mine and recover rare earth into oxides."

On production economics, Mark Chalmers is direct about the margin available at current price levels:

"Our costs at Pinyon Plain are between $23 to $30 per pound. So if you're selling at $75 a pound plus, you've got a really nice margin."

Uranium Price Mechanisms & Long-Term Contract Economics

Realized uranium prices averaged $59.60 per pound in 2023. Per S&P Global Market Intelligence, consensus forecasts project approximately $98.70 per pound by 2033, reflecting long-term contracting cycles, utility re-entry into term markets, and supply replacement economics.

enCore's Gas Hills project carries a pre-tax internal rate of return of approximately 54.8%, based on a long-term uranium price assumption of $87 per pound which reflects the margin leverage achievable through low-capex modular wellfield development under a rising price environment.

IsoEnergy's toll milling strategy at White Mesa further compresses time-to-cash-flow. Philip Williams explains the operational advantage:

"The White Mesa Mill is the only operable conventional uranium mill in the United States today... We can move ahead very quickly because the mill is operating and running, and we don't have to bear the costs of starting it up and maintaining it."

Capital Expenditure Trends Across the Uranium Development Spectrum

Aggregate uranium capital expenditure is projected to rise from approximately $704 million in 2024 to $969 million in 2025, peaking at roughly $1.6 billion in 2027. This trajectory signals that developers are advancing toward final investment decisions and the second supply wave is forming.

Exploration-stage companies provide exposure to discovery optionality in proven jurisdictions. ATHA Energy controls over 7 million acres of exploration ground, including 3.8 million acres in the Athabasca Basin, the largest exploration land package in the Basin, as described in its February 2026 corporate presentation. The company also holds a 10% carried interest in key exploration lands operated by NexGen Energy and IsoEnergy, providing capital-light exposure to their programs. Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the significance of the company's Angikuni Basin position:

"At ATHA, we have full control over the Angikuni basin, that's a sub-basin to the Athabasca... We are in sole control of it, and I view it as being analogous to exploring in the northeast Athabasca basin circa 1965."

Recent drilling at the Angilak Project has produced technically significant results. Drill hole RIBN-DD-001 - the RIB North discovery hole - returned over 26 metres of continuous uranium mineralization, anchoring future resource classification work and exploration target definition.

Risk Factors & Volatility Considerations

Institutional investors must apply differentiated risk frameworks across the uranium equity spectrum. Commodity price volatility remains the primary variable, particularly for developers whose project economics depend on long-term contract price assumptions. Capital cost inflation, enrichment buildout delays, political shifts in nuclear policy, and currency exposure represent additional risk vectors.

In-situ recovery operations carry lower upfront capital requirements but face groundwater regulatory scrutiny. Conventional operations carry higher capital requirements and longer permitting windows. Exploration-stage companies face financing dilution risk and resource classification uncertainty as inferred resources are advanced toward indicated status. Balanced contracting strategies, calibrating term commitments to retain upside exposure to spot price appreciation, provide a measured risk allocation suited to the current price environment.

The Investment Thesis for Uranium

- Artificial intelligence infrastructure buildout and accelerating grid electrification are extending baseload nuclear demand well beyond traditional utility planning cycles, shifting contracting behavior toward multi-decade agreements that underwrite capital deployment decisions in the present cycle rather than deferring them.

- The Prohibiting Russian Uranium Imports Act has introduced a measurable and time-bounded Western supply gap, structurally repositioning domestic producers as the default beneficiaries of regulatory-driven demand redirection, with urgency compounding as the compliance timeline advances.

- Heavy concentration among a small number of incumbent producers means the supply response to rising demand will increasingly depend on second-wave developers reaching production before 2033, compressing the capital formation window and elevating execution risk across the development pipeline as a sector-wide variable.

- High-grade Athabasca Basin jurisdictions continue to command a cost and margin premium over lower-grade alternatives, with indicated grades in the range of 30% or above offering operating leverage and NPV sensitivity to price increases that lower-grade assets structurally cannot replicate at equivalent capital intensity.

- In-situ recovery methodology and conventional milling infrastructure represent two distinct but complementary supply pathways, with ISR delivering capital-light near-term production leverage and conventional mill capacity provides irreplaceable processing optionality that new entrants cannot reproduce on a commercially relevant timeline.

The uranium market is no longer defined by post-Fukushima underinvestment cycles. It is defined by AI-driven electricity demand, energy security policy, enrichment constraints, and long-dated contracting cycles. Supply must expand materially by 2030 to 2033 to avoid a widening gap between reactor requirements and available feedstock that requires a 2.5-fold increase in global production from current levels.

Producers with operating assets in the United States benefit from immediate alignment with domestic supply policy and active term contracting programs. High-grade Canadian developers offer long-term supply replacement leverage anchored in tier-one geological endowment. Exploration platforms provide convexity to rising long-term prices through discovery optionality in the world's most prolific uranium basin. The cycle presents a macro-driven re-rating opportunity across a differentiated risk spectrum, spanning producing companies with near-term cash generation, developers with defined project timelines, and exploration-stage platforms with asymmetric upside. The supply curve is being reset and capital markets may be expected to adjust accordingly.

TL;DR

The uranium market faces a structural supply deficit requiring a 2.5-fold production increase by 2033, driven by AI infrastructure buildout, grid electrification, and accelerating nuclear capacity expansion. The 2028 Russian enriched uranium import ban compounds this shortfall, repositioning domestic US producers and high-grade Athabasca Basin developers as strategic beneficiaries. Supply is heavily concentrated among Kazatomprom and Cameco, meaning second-wave developers must reach production before 2033 to close the gap. Across the investment spectrum, ISR operators offer capital-light near-term leverage, conventional mill infrastructure provides irreplaceable processing optionality, and exploration-stage companies offer asymmetric upside through discovery in proven jurisdictions.

FAQs (AI-Generated)

AI data centers require uninterrupted, high-capacity-factor baseload power that intermittent renewables cannot reliably provide. Nuclear energy, operating at approximately 90% capacity factor with zero carbon emissions, is increasingly the preferred solution. As hyperscale data center buildout accelerates globally, utilities are extending reactor lifespans, restarting idled facilities, and planning new capacity, all of which require significantly more uranium fuel over multi-decade timeframes.

Global uranium production in 2025 is approximately 58.5 million pounds of U₃O₈, while projected reactor demand requires roughly 141.2 million pounds by 2033. Closing that gap demands a 2.5-fold increase in primary mine supply within roughly eight years — a challenge no single producer, jurisdiction, or mining method can address alone, making a broad second wave of developer production critical.

The Prohibiting Russian Uranium Imports Act eliminates a significant source of enriched uranium for the US market from 2028 onward. Since the US generates approximately 30% of global nuclear power but holds only around 1% of global uranium reserves and imports close to two-thirds of its enriched uranium, the ban creates simultaneous gaps across mining, conversion, and enrichment — structurally elevating the strategic value of domestic US producers and Western-aligned supply chains.

The Athabasca Basin in Saskatchewan, Canada, hosts some of the world's highest-grade uranium deposits, with assets like IsoEnergy's Hurricane deposit grading 34.5% U₃O₈. High-grade deposits provide superior operating leverage, lower unit costs, and stronger NPV sensitivity to uranium price increases compared to lower-grade alternatives. The Basin's established discovery history and geological endowment make it one of the few jurisdictions capable of contributing meaningfully to Western supply at scale.

ISR operations require lower upfront capital, enabling faster production ramp-up and near-term cash flow, though they face groundwater regulatory scrutiny. Conventional milling requires higher capital and longer permitting timelines but processes a broader range of ore types and, in the case of the White Mesa Mill, provides irreplaceable multi-commodity processing infrastructure that new entrants cannot replicate on a commercially relevant timeline. Both methodologies represent complementary and necessary components of the Western uranium supply response.

Analyst's Notes

Subscribe to Our Channel

Stay Informed