US Tariffs Redirect Chinese Battery Oversupply Into Europe, Driving 17% Price Compression

US tariffs redirect Chinese battery oversupply into Europe, driving 17% price compression and repricing upstream assets in allied jurisdictions.

- US tariffs on Chinese battery imports and EU procurement rules restricting below-cost materials have redirected Chinese excess capacity, compressing downstream unit prices and directing institutional capital toward upstream assets in allied jurisdictions across nickel, graphite, and rare earth elements.

- Redirected oversupply, technological improvements, and lower input costs drove approximately 17% price compression between December 2024 and August 2025, creating margin pressure that domestic manufacturers cannot resolve without trade barriers or production subsidies.

- Critical minerals, including nickel, graphite, and rare earth elements, have transitioned from cyclical commodities to strategic assets, with governments now prioritizing supply security over cost efficiency, with direct consequences for which projects attract institutional capital.

- Retail investors holding downstream battery manufacturing positions face asymmetric downside risk, where price compression from subsidized imports erodes margins faster than electric vehicle adoption volumes can compensate.

- Upstream mining and processing assets in Tier 1 jurisdictions aligned with Western supply chain policy are attracting strategic premiums, particularly projects with low all-in sustaining cost, long mine life, and processing infrastructure that reduces Chinese refining dependency.

National Security Policy: Determining Which Critical Mineral Projects Attract Capital

The global critical minerals market is undergoing a supply chain restructuring driven by national security policy rather than cost optimization. Materials including nickel, graphite, rare earth elements, and uranium now underpin electric vehicle batteries, grid storage systems, defense electronics, and advanced manufacturing - making uninterrupted access a state-level priority for the United States and the European Union.

This shift has elevated critical minerals from cyclical commodities to strategic assets, with geopolitical alignment now determining market access as much as cost competitiveness. The US-China trade conflict has accelerated the transition by imposing barriers on Chinese battery imports, forcing China to redirect excess production capacity into more open markets - particularly Europe - where domestic manufacturers lack the scale or policy support to compete on price.

The investment consequence is a bifurcated market: a low-cost, high-volume Chinese supply chain flooding downstream segments with below-cost products, against a higher-cost, policy-supported Western supply chain being assembled through subsidies, trade barriers, and strategic procurement rules. The position of an asset within one of these two systems now determines its valuation risk as much as its resource grade or mine plan.

Trade Diversion & Price Compression: The Immediate Market Impact

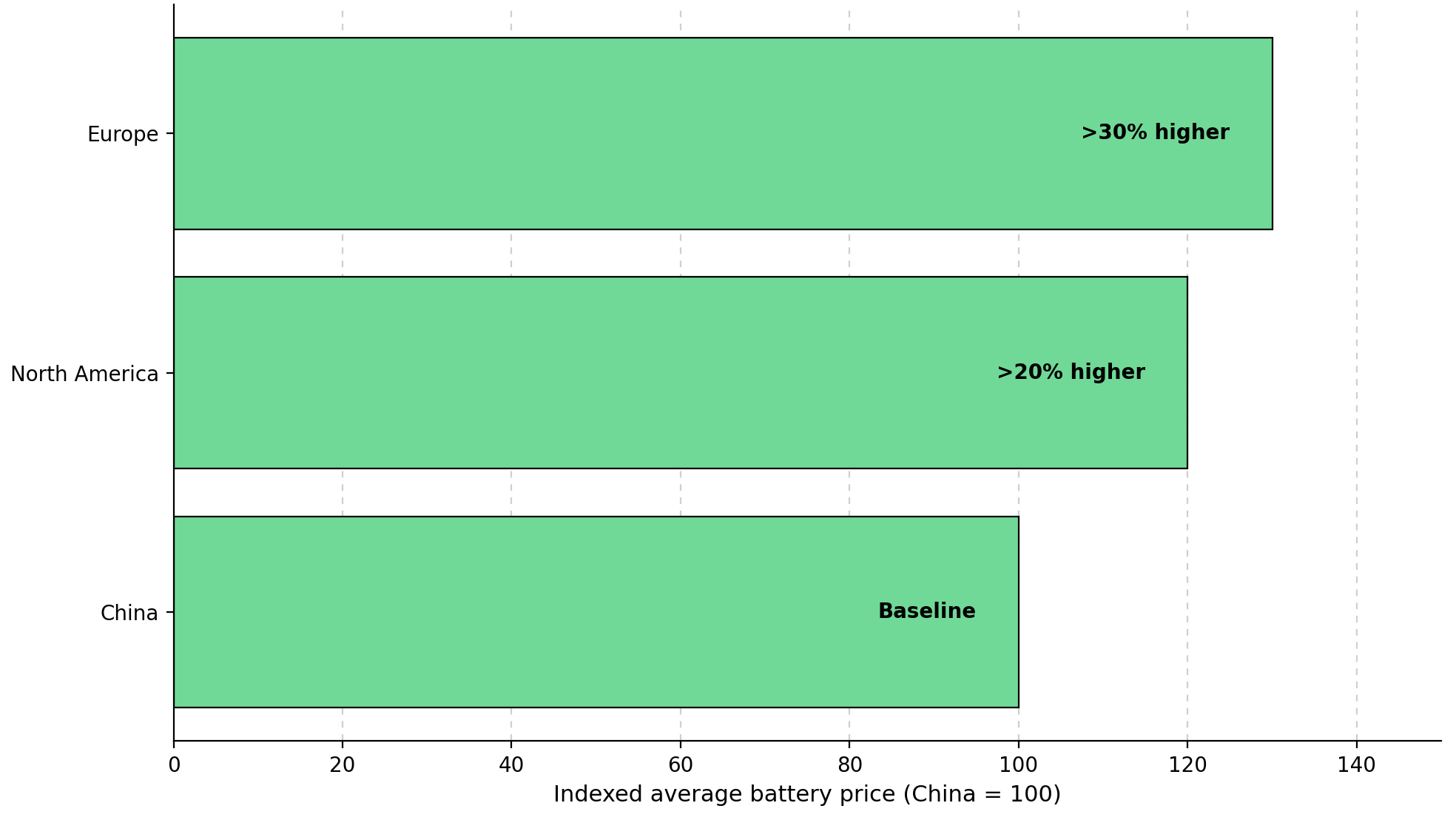

Trade diversion occurs when import barriers in one market redirect surplus supply into less-protected markets. China's excess battery manufacturing capacity, denied access to the United States through tariffs, entered European markets at prices that undercut domestic producers. A December 2025 policy brief published jointly by the Bertelsmann Stiftung, Center for European Reform, and Jacques Delors Center, drawing on UN COMTRADE data, recorded a decline of approximately 17% in the unit price of Chinese batteries imported into the EU between December 2024 and August 2025, a drop reflecting technological improvements, lower input costs, and intense price competition from below-cost imports that threaten to quickly wipe out EU producers.

The downstream consequence for EV adoption is positive in the near term: lower battery prices reduce vehicle costs and National Security Policy, Not Cost, Now Determines Which Critical Mineral Projects Attract Capital can accelerate fleet electrification. However, this demand acceleration does not translate into profitability for producers competing against subsidized imports. Revenue growth from higher unit volumes is offset by unit price compression, producing a margin squeeze that worsens as Chinese supply increases.

Policy Response: The US-EU Critical Minerals Pact

The United States and the European Union are advancing a coordinated critical minerals strategy aimed at reducing dependency on China across the full value chain from exploration to processing. Policy tools under active development include production-linked subsidies supporting capital-intensive project ramp-ups, trade barriers restricting below-cost imports, and strategic procurement rules prioritizing domestically processed materials in public infrastructure and defense spending.

Discounted cash flow models must now incorporate jurisdictional risk premiums and supply chain compliance costs that did not factor into pre-2022 capital allocation frameworks. A project that sits outside the cost top quartile may become viable under policy support if it is located in an allied jurisdiction with permitting visibility. Conversely, a low-cost project in a geopolitically misaligned jurisdiction may face market access constraints that no cost advantage can fully offset.

The practical implication is that project jurisdiction has become a primary investment screen. Projects targeting US or EU markets must demonstrate both cost competitiveness and strategic alignment with domestic supply chain goals to attract the institutional capital required for construction financing.

Supply-Side Realities: Capacity Expansion & Competitive Saturation in the US

Policy support for Western supply chains is accelerating domestic battery manufacturing capacity in the United States to a level that projections from Rhodium Group and MIT-CEEPR indicate will exceed domestic demand within this decade. This reduces US import dependency but simultaneously limits export opportunities for allied producers, narrowing the addressable market for projects targeting American offtake.

Evaluating projects whose thesis depends on US market access, this creates a critical falsification test: any project whose financial model relies on exporting battery materials into the United States must be stress-tested against domestic oversupply scenarios in which demand growth is absorbed by already-financed American capacity.

First-quartile cost positioning, multi-decade mine life, and processing infrastructure capable of delivering battery-grade material are the conditions that determine whether a project can compete for the offtake and financing that remains available. Higher-cost projects that require policy-driven price premiums to reach viability face compounding risk when both domestic oversupply and benchmark price deflation occur simultaneously.

Repricing the Upstream: Why Mining Assets Are Gaining Strategic Premiums

Canada Nickel's Crawford nickel sulphide project in Ontario, Canada carries a net present value at an 8% discount rate of approximately US$2.8 billion, an internal rate of return of 17.6%, and net C1 cash costs of approximately US$0.39 per pound, as reported in the company's Front-End Engineering and Design results dated March 2025 (qualified person: Steve Balch, P.Geo). Wood Mackenzie's comparison of 2023 net C1 cash costs across global nickel operations places Crawford in the first cost quartile.

Mark Selby, Chief Executive Officer of Canada Nickel, outlines the district-level production potential that underpins the long-term investment case:

"We always talk about Crawford being our first project and not our best project. Midlothian and Reid, along with Mann West, are all potentially much better than Crawford… Over a 10 or 15 year period, you can get to 250,000 or 300,000 tons of nickel potentially coming out of this district."

Lifezone Metals' Kabanga Nickel project in Tanzania holds reserves of 52.2 million tonnes at 1.98% nickel with copper and cobalt by-products, carrying an after-tax NPV at an 8% discount rate of US$1.58 billion and a 23.3% IRR, with first-quartile AISC of US$3.36 per pound net of by-product credits. Lifezone's acquisition of BHP's 17% interest delivers 100% ownership of Kabanga Nickel Limited, capturing full offtake control. Lifezone Metals is advancing H1 2026 catalysts, including the amended Framework Agreement, offtake finalization, and the US Development Finance Corporation political risk insurance package, with project finance led by Societe Generale and Standard Chartered Bank at an advanced stage.

Strategic Processing & Midstream Control as a Differentiator

Processing infrastructure is increasingly the bottleneck that determines Western supply chain independence from Chinese refining. Energy Fuels operates the White Mesa Mill in Utah, the only conventional uranium mill currently producing in the United States, and is expanding its capabilities into rare earth element separation and downstream alloy production.

Ownership of every midstream step from mining through refined alloys eliminates the refining dependency that would otherwise allow China to restrict market access at the processing stage, regardless of upstream production volumes. Mark Chalmers, Chief Executive Officer of Energy Fuels, states:

"To really compete with China, you have to have all those steps, you can't be missing a step in the middle of it. We've been very focused on the integration."

Energy Fuels has completed feasibility studies on both its Phase 2 REE expansion and the Vara Mada mineral sands project in Madagascar. Chalmers states the combined net present value of those two projects approaches US$4 billion, with EBITDA targeting approximately US$800 to US$900 million per year. The company closed a US$700 million convertible senior notes offering in October 2025 at a 0.75% coupon, arranged by Goldman Sachs, bringing total deployable capital to approximately US$1 billion when combined with existing cash and equivalents.

By-Product Economics & Cost Advantage in Graphite Supply

Sovereign Metals' Kasiya project in Malawi produces graphite as a by-product of rutile extraction, a cost structure that places the project at the bottom of the global graphite cost curve without requiring standalone graphite processing investment. Chairman Ben Stoikovich quantifies Sovereign Metals’ competitive position:

"Our incremental cost to produce a ton of graphite as a by-product from the Kasiya project will only be US$241 per ton. Where do we plot on the standard industry graphite cost curve? We're at the very bottom."

The US$241 per tonne figure is drawn from Sovereign Metals' Optimized Pre-Feasibility Study published via ASX announcement on 22 January 2025. Benchmark Mineral Intelligence's China weighted average C1 cash cost sits at approximately US$257 per tonne, placing Kasiya below the Chinese production floor at Q4 2024 reference prices. The same study reports a pre-tax NPV exceeding US$2.3 billion and average annual EBITDA exceeding US$400 million.

Rio Tinto became an investor in mid-2023, has invested A$60 million in exchange for a 19.9% shareholding, and oversees project development through a joint Sovereign-Rio Tinto Technical Committee.

Risk Framework: What Could Break the Critical Minerals Thesis?

Policy dependency is the primary structural risk. Delays or dilution of subsidies, tariff regimes, or procurement policies would remove the price floor supporting marginal Western projects, exposing them to unprotected Chinese competition. Investors should monitor legislative calendars and trade negotiation timelines as leading indicators for this risk.

Sustained price deflation driven by continued Chinese dumping poses a second threat. Even first-quartile cost projects face NPV erosion if benchmark prices fall faster than AISC reductions can offset. Permitting delays extend the gap between capital commitment and first revenue, increasing return sensitivity to base-case commodity price assumptions. Technological substitution, advances in solid-state or sodium-ion battery chemistry reducing nickel or graphite content per kilowatt-hour, is speculative at present but warrants stress-testing in financial models targeting production timelines beyond 2030.

The Investment Thesis for Critical Minerals

- Projects eligible under US and EU bilateral supply chain agreements benefit from trade barriers and strategic procurement access unavailable to producers outside those agreements, making eligibility a primary valuation input rather than a secondary consideration.

- Upstream mining assets with first-quartile all-in sustaining costs and large, high-grade resource bases are better positioned to absorb downstream price volatility without NPV erosion than higher-cost peers whose viability depends on policy-driven price premiums remaining intact.

- Companies controlling midstream processing infrastructure capture margins unavailable to pure mining plays, reducing revenue dependency on spot commodity prices.

- Large, long-life assets provide multi-decade supply visibility in a structurally constrained market, delivering the volume and duration that utility-scale offtake buyers require for bankable long-term supply agreements.

- Assets where graphite is produced as a by-product of a primary commodity carry incremental graphite costs below standalone production economics, because the primary revenue stream absorbs fixed costs before graphite costs are incurred, placing them below the Chinese production floor regardless of graphite market cycles.

- Institutional capital will concentrate in assets that have achieved named permitting milestones, secured strategic partnerships with tier-one counterparties, and closed or committed financing, conditions that narrow the discount rate applied to terminal cash flows and compress the risk premium that earlier-stage peers still carry.

Projects that combine first-quartile cost positioning, having jurisdictional advantage, midstream processing ownership, and tier-one strategic partnerships qualify for the construction financing and offtake agreements that projects outside US-EU bilateral supply chain agreements cannot access. Investors who identify assets meeting all four conditions before construction decisions are announced capture the valuation compression between development-stage risk premiums and producer-stage discount rates.

The policy and trade conditions driving this reallocation - US tariffs, EU procurement rules, and bilateral critical minerals agreements - persist as long as the US-EU industrial policy consensus holds. Deterioration in that consensus is the primary macro risk to the thesis and the leading indicator investors should monitor.

TL;DR

US tariffs on Chinese battery imports have redirected excess Chinese manufacturing capacity into European markets, where a December 2025 policy brief recorded approximately 17% unit price compression between December 2024 and August 2025. This margin pressure cannot be resolved by downstream manufacturers without trade barriers or production subsidies. The investment consequence is a bifurcated market in which eligibility under US-EU bilateral supply chain agreements, first-quartile cost positioning, midstream processing ownership, and tier-one strategic partnerships now determine which projects access construction financing and offtake agreements. Deterioration of the US-EU industrial policy consensus is the primary macro risk to this thesis and the leading indicator investors should monitor.

FAQs (AI-Generated)

China's excess battery manufacturing capacity, denied US market access through tariffs, redirected into European markets at below-cost prices. European domestic manufacturers lack the scale or policy support to compete at those price levels, producing a margin squeeze that worsens as Chinese supply volumes increase.

Active policy instruments include production-linked subsidies supporting capital-intensive project ramp-ups, trade barriers restricting below-cost imports, and strategic procurement rules prioritizing domestically processed materials in public infrastructure and defense spending.

Projects outside US-EU bilateral supply chain agreements cannot access the trade barrier protection and strategic procurement offtake that those agreements provide. A low-cost project in an ineligible jurisdiction faces market access constraints that no cost advantage can fully offset.

The four primary risks are: policy dilution or delay removing the price floor for marginal Western projects; sustained Chinese price dumping eroding NPV faster than cost reductions can offset; permitting delays extending the gap between capital commitment and first revenue; and technological substitution — advances in solid-state or sodium-ion chemistry reducing nickel or graphite content per kilowatt-hour — in projects with production timelines beyond 2030.

Chinese dominance across rare earth separation and alloy production means projects that stop at mining or concentrate output remain dependent on Chinese midstream capacity to reach end-use buyers. Ownership of every step from mining through refined alloys eliminates the processing-stage dependency that would otherwise allow China to restrict market access regardless of upstream production volumes.

Analyst's Notes

Subscribe to Our Channel

Stay Informed