ValOre Metals Leads Brazil's Platinum Resurgence in 2026

Discover why Brazilian precious metals offer compelling returns: structural PGM deficits, geopolitical diversification, underexplored geology & strong fundamentals.

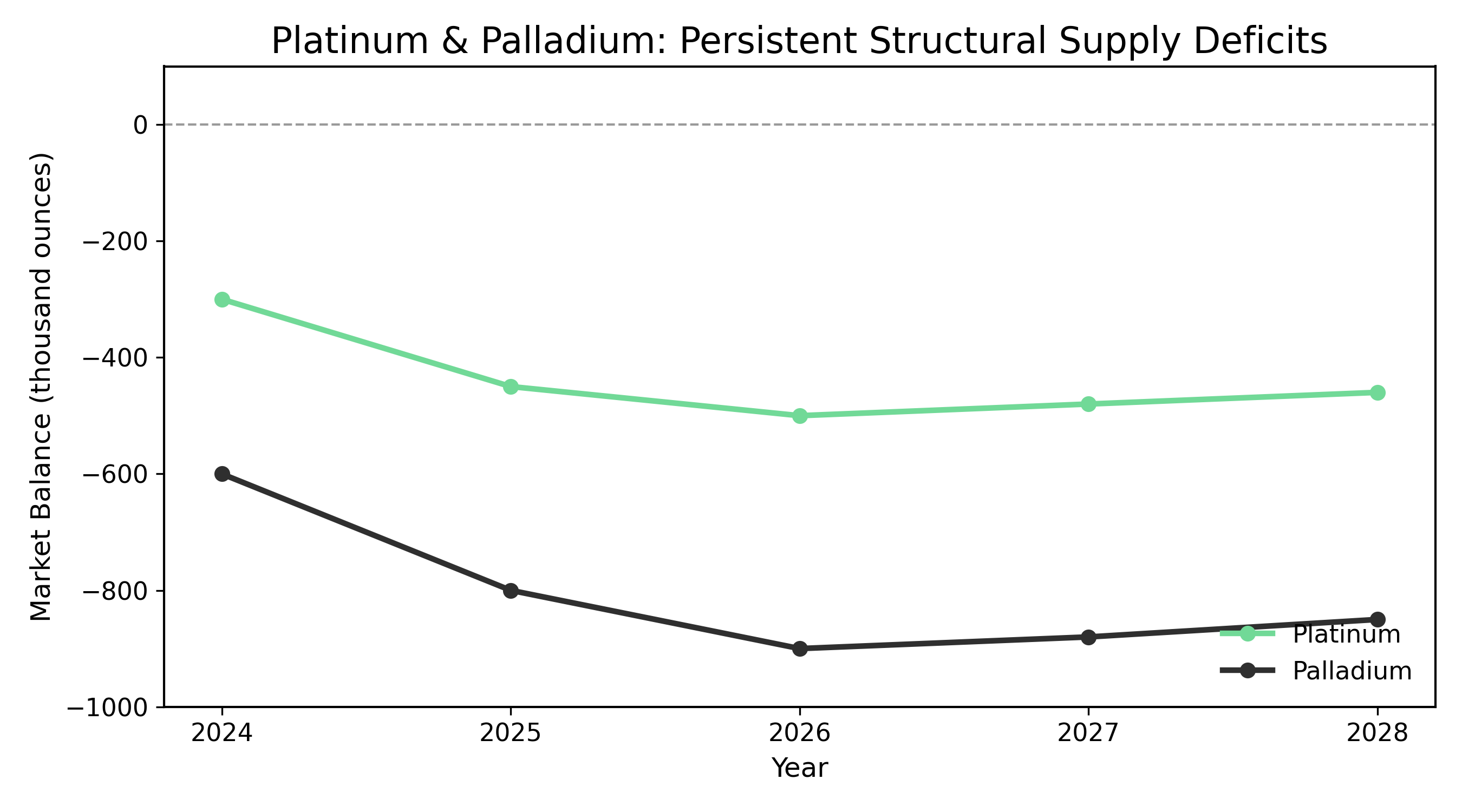

- Platinum and palladium markets face persistent deficits through 2028, with palladium showing particularly acute shortages. Strong price performance in 2025 has created a favorable environment for producers, with platinum and palladium both experiencing substantial year-over-year gains.

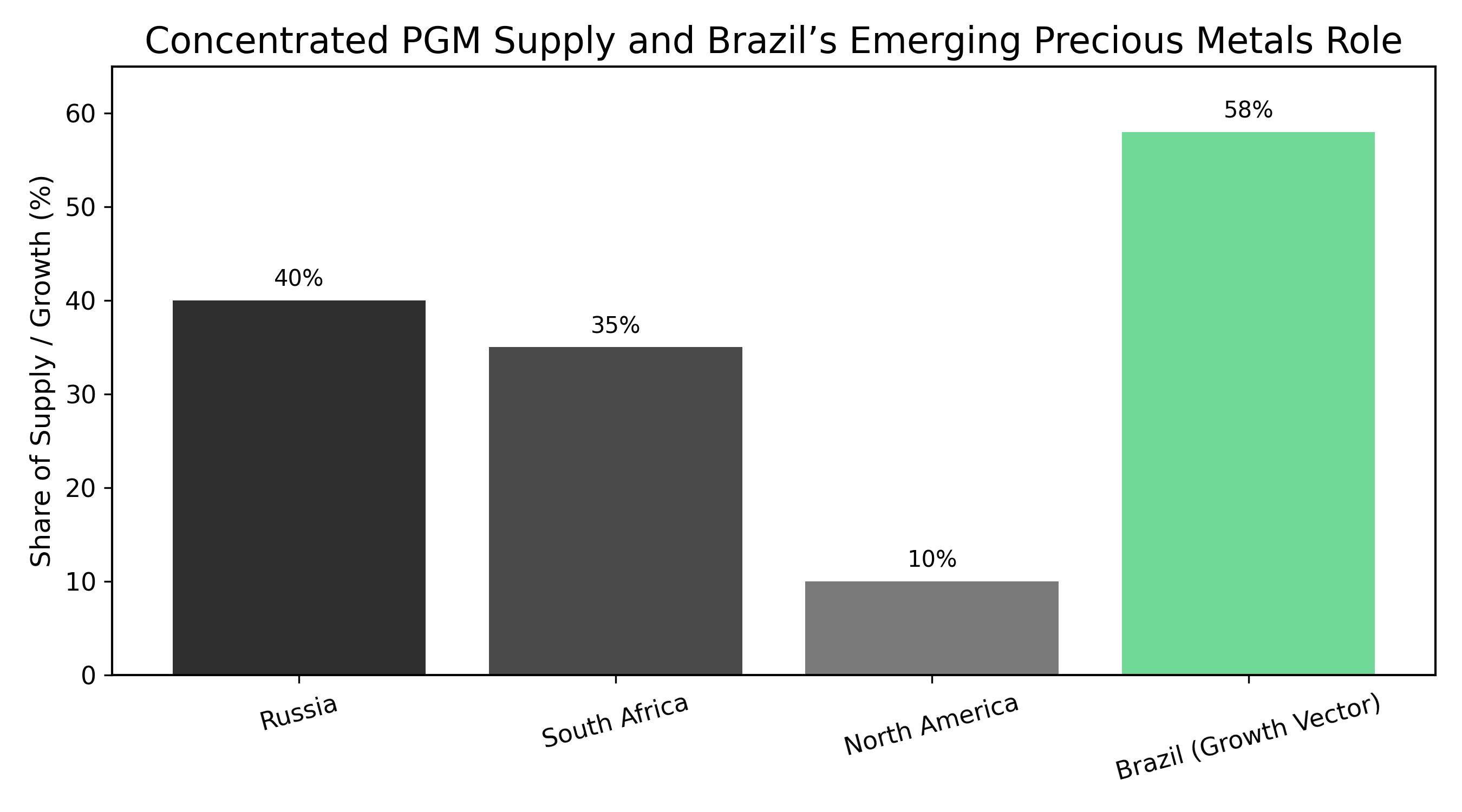

- Mine supply remains heavily concentrated in Russia and South Africa, with declining primary supply from Southern Africa and North America due to cost and capital pressures. This concentration creates supply vulnerability and price support, particularly given ongoing trade disruptions and potential US tariffs on PGM imports.

- Brazil ranks among the top 10 global gold producers with annual output of $3.8 billion growing to over $6 billion by 2030. The country offers stable regulatory frameworks, strong technical talent (now graduating more mining engineers than the US and Canada combined), and remains significantly underexplored with less than 30% mapped at high-resolution standards.

- Bank of America Securities raised its 2026 platinum forecast to $2,450/oz from $1,825/oz and palladium to $1,725/oz from $1,525/oz, citing strong demand, market tightness, Chinese import growth, and supply constraints. Current spot prices already exceed these revised forecasts, suggesting continued upward momentum.

- Internal combustion engine (ICE) and hybrid vehicles will continue to represent over 50% of PGM demand for an extended period (10+ years), ensuring sustained industrial consumption even as the automotive sector transitions. This demand floor provides downside protection while supply constraints offer upside leverage.

A Convergence of Market Forces

The precious metals sector stands at an inflection point in early 2026, with platinum group metals experiencing their most favorable supply-demand dynamics in over a decade. While investor attention has historically centered on traditional producing regions like South Africa's Bushveld Complex and Russia's Norilsk operations, a compelling alternative narrative is emerging from Brazil's underexplored precious metals districts.

The investment case for Brazilian precious metals, particularly platinum, palladium, and gold, rests on three converging themes: structural supply deficits in global PGM markets, geopolitical fragmentation of traditional supply chains, and Brazil's maturation as a premier mining jurisdiction with significant untapped potential. For investors seeking exposure to precious metals with asymmetric risk-reward profiles, understanding Brazil's evolving role in global supply chains has become essential.

Global Trends: The New PGM Market Reality

The platinum and palladium markets have undergone fundamental transformation since 2022, with both metals facing persistent structural deficits through 2028. Bank of America Securities raised its 2026 platinum price target to $2,450 per ounce from $1,825 per ounce (34% increase) and palladium to $1,725 from $1,525. Spot prices have already exceeded these targets, with platinum near $2,446 and palladium around $1,826 as of early 2026.

Strong demand continues across industrial applications while supply remains constrained by inelastic mine output and production discipline. This creates a market where price increases translate directly to producer margins rather than stimulating rapid supply expansion. The automotive sector remains the dominant PGM demand source, with internal combustion engine and hybrid vehicles forming over 50% of demand for the next decade despite the EV transition narrative.

Supply Challenges: Concentration, Depletion, & Geopolitical Risk

Russia and South Africa collectively account for the vast majority of global platinum and palladium mine supply. South African production faces mounting headwinds from aging infrastructure, deepening ore bodies (now exceeding 2,000 meters depth), rising costs, and periodic labor disruptions. The Bushveld Complex contains approximately 75% of the world's known platinum reserves, but high-grade deposits are becoming exhausted. Energy reliability challenges including load-shedding further constrain production.

North American production has declined due to economic pressures. Geopolitical fragmentation adds another layer, with US tariffs disrupting supply chains and potential Russian sanctions representing tail risks. Against this backdrop, supply diversification becomes strategically valuable, positioning Brazil advantageously as an alternative source outside traditional producing regions.

Brazil's Mining Resurgance: Infrastructure, Talent, & Opportunity

Brazil ranks among the top 10 global gold producers, generating approximately $3.8 billion annually with growth trajectories toward $6 billion by 2030. The country graduates more mining engineers annually than the United States and Canada combined, creating a deep talent pool that reduces project execution risk and operating costs. This human capital advantage, combined with expertise in tropical and lateritic ore environments, provides competitive advantages.

Brazil remains significantly underexplored, with less than 30% mapped at high-resolution standards, suggesting substantial discovery upside. The northeastern states, including Ceará, benefit from established industrial corridors, reliable electrical grids, and proximity to Atlantic shipping routes. Brazil's regulatory environment has improved significantly with streamlined permitting processes, while government commitment to developing the mining sector provides policy stability that reduces sovereign risk.

ValOre Metals & the Pedra Branca Project

ValOre Metals (TSX-V: VO, OTCQB: KVLQF, FSE: KEQ0) exemplifies the emerging Brazilian precious metals opportunity with its flagship Pedra Branca project in Ceará State hosting a 2.2 million ounce inferred resource of platinum, palladium, and gold grading 1.08 g/t across seven near-surface resource zones with excellent regional infrastructure and strong community support. The management team forms part of the Discovery Group, which has collectively raised over $1 billion and participated in $2.6 billion in M&A transactions. The board includes executives who have driven major value-creating transactions with assets acquired by Rio Tinto ($650 million), Goldcorp ($520 million), Royal Gold ($200 million), and Coeur Mining ($117 million).

Newly appointed Chief Executive Officer Nick Smart noted about their project:

"I am honored to join ValOre at such an opportune and important time for the company. I have had the privilege to meet and begin working alongside the truly talented members of the ValOre team, as they are taking forward the development of our flagship Pedra Branca PGE project and actively exploring new, district-level precious metals opportunities in some of the most prospective areas of Brazil. I am beyond excited by the capacity and potential we have together - to build on this base and create a world-class integrated precious metals company."

Chairman Jim Paterson brings 27 years of executive leadership experience with companies that raised over $300 million in equity and participated in over $1 billion in M&A transactions. CEO Nick Smart contributes 21 years of experience, including roles at Anglo American and De Beers, with expertise spanning platinum operations in South Africa, zinc projects globally, nickel projects in Brazil (where he worked for six years in the states of Minas Gerais and Goiás developing nickel mines), and diamond mining in Canada. At De Beers Group, he held executive leadership roles establishing their laboratory-grown diamonds entity. This combination of transaction expertise and operational experience positions ValOre to execute both technical development and strategic value creation. ValOre has invested CAD$6.1 million in exploration at Pedra Branca, drilling 17,434 meters and doubling the inferred resource from 1.1 million to 2.2 million ounces. Previous operators invested an additional over USD$35 million and 30,000 meters of drilling, representing substantial sunk costs that ValOre acquired at a fraction of replacement value.

The Pedra Branca property covers 51,096 hectares of 100% owned mineral rights with over 80 kilometers of prospective PGE trend and five new zones drilled in 2023 not yet incorporated into resource estimates. Metallurgical testwork currently underway at the University of Cape Town aims to demonstrate optimal process routes, including innovative bacteria-based bio-extraction testwork for PGMs, potentially offering efficient, lower-cost alternatives to conventional methods. ValOre is pursuing aggressive acquisition targets in Brazil's gold sector, with management anticipating M&A announcements in Q1 2026 and targeted gold production from acquisitions by Q3 2026. This strategy aims to generate near-term cash flow from gold operations while advancing the longer-cycle Pedra Branca PGM project. A preliminary economic assessment for Pedra Branca is scheduled for Q4 2026, followed by licensing and environmental impact assessment work in Q1 2027, positioning the project for potential development decisions in 2027-2028.

Investment Considerations: Valuation & Market Positioning

ValOre Metals currently trades with a market capitalization of approximately CAD$27.1 million based on 257.9 million shares at $0.105 per share, implying approximately $12 per contained ounce - well below typical transaction multiples for PGM projects. The shareholder structure includes 20% insider ownership, 25% held by resource-focused funds, and 10% by close associates, indicating strong alignment.

Current market conditions favor near-term positioning, as PGM prices have broken through institutional forecasts. The valuation gap between operating producers and development-stage projects has widened substantially and should narrow as higher PGM prices become established. Acquisition activity in Brazil's mining sector appears poised to accelerate as major producers seek to diversify supply sources, creating potential exit opportunities for early investors.

The Investment Thesis for Brazilian Precious Metals

- Establish positions in platinum and palladium exposed companies while prices remain below long-term equilibrium, targeting near-term developers with low cash costs

- Reduce portfolio concentration risk by allocating to Brazilian precious metals assets without geopolitical risks of Russian or South African production

- Prioritize companies led by teams with demonstrated success in discovery, development, and value-creating transactions

- Consider building positions progressively as companies achieve de-risking milestones while maintaining conviction through short-term volatility, as value creation occurs over multi-year timeframes

The investment thesis for Brazilian precious metals rests on fundamental supply-demand imbalances in global PGM markets, geopolitical vulnerability of concentrated supply chains, and Brazil's underappreciated potential as a premier mining jurisdiction. For investors willing to accept risks inherent in exploration companies, Brazilian precious metals offer asymmetric return profiles with limited downside given current valuations and substantial upside tied to resource expansion and potential strategic transactions.

ValOre Metals, with its 2.2 million ounce Pedra Branca resource, proven management team, and aggressive growth strategy, represents a leveraged opportunity to participate in Brazil's precious metals renaissance. The multi-pronged approach of advancing the flagship PGM project while pursuing near-term gold production provides multiple catalysts for value realization over the next 12 to 24 months.

TL;DR

Brazilian precious metals present a compelling investment opportunity driven by structural supply deficits in platinum and palladium markets, with both metals experiencing significant gains in 2025. Brazil offers geopolitical diversification from concentrated Russian and South African supply, with stable regulations and strong technical capacity. The country remains significantly underexplored with less than 30% mapped at high-resolution standards. ValOre Metals exemplifies this opportunity with its 2.2 million ounce Pedra Branca PGM project and aggressive acquisition strategy targeting Brazilian gold assets. Management's proven track record includes $2.6 billion in M&A transactions. ValOre has invested CAD$6.1 million drilling 17,434 meters at Pedra Branca, while previous operators invested over USD$35 million and 30,000 meters. Bank of America Securities raised 2026 platinum forecasts to $2,450/oz, 34% above previous targets, while current spot prices already exceed these levels. The convergence of favorable metal prices, jurisdictional advantages, and attractive entry valuations creates asymmetric return potential for informed investors.

FAQs (AI-Generated)

Prices are rising due to structural supply deficits, driven by underinvestment in new supply, declining production from South Africa and North America, and sustained automotive and industrial demand.

Brazil offers stable regulatory frameworks, strong technical talent (graduating more mining engineers than the US and Canada combined), excellent infrastructure, and significant underexplored potential (less than 30% mapped at high-resolution), providing geopolitical diversification from concentrated Russian and South African supply.

Pedra Branca hosts a 2.2 million ounce inferred resource of platinum, palladium, and gold in Ceará State, Brazil, with over 47,000 meters of drilling completed and a preliminary economic assessment planned for Q4 2026.

Key risks include currency volatility, potential regulatory delays, metallurgical complexity, resource conversion uncertainty, substantial capital requirements for development, and general exploration risk.

ValOre is pursuing aggressive acquisitions targeting advanced-stage gold projects in northeastern Brazil, with M&A announcements anticipated in Q1 2026 and targeted gold production by Q3 2026.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed