Why is The European Gas Market Failing to Price the Winter Risk the Iran Deal Leaves Behind?

Oil fell 5.5% on Iran deal signals, but European gas faces a 6-month LNG restart lag. TTF remains 30% below Rabobank's year-end target of 69 EUR/MWh.

- WTI settled at $88.68/barrel (−5.5%), and Brent at $94.29/barrel (−5.3%) at six-week lows, after US and Iranian negotiators issued concurrent positive signals for the first time since the US-Iran conflict began blockading the Strait of Hormuz, per WSJ.

- Options markets assign a 37% implied probability to WTI above $100/barrel within three months; the deal is priced as probable, not complete, and the tail risk has not been removed.

- Iranian LNG export infrastructure requires a minimum of six months of assessment and restart after hostilities cease; a deal signed in June does not change European gas availability before October's injection season closes.

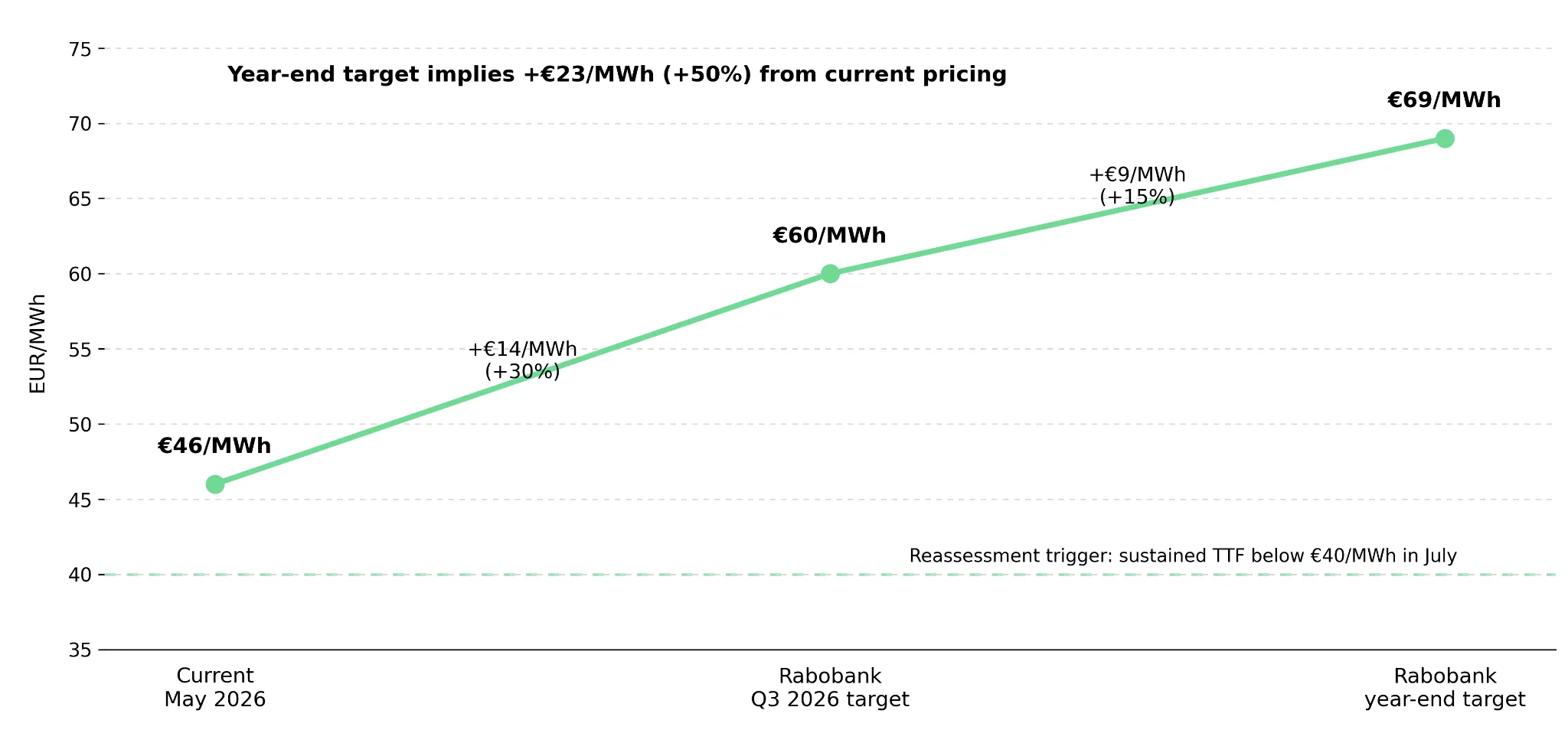

- European TTF gas is trading at approximately 46 EUR/MWh against Rabobank's Q3 2026 target of 60 EUR/MWh and year-end target of 69 EUR/MWh, with supply normalization delayed until 2028 when additional US and Qatari LNG capacity comes online, per WSJ.

- WTI below $85/barrel for 10 consecutive trading days signals the Hormuz war premium has been fully removed; TTF falling below 40 EUR/MWh into July signals European storage injections are running ahead of schedule and Rabobank's year-end target is no longer operative.

The Oil Decline Was Probability Repricing, Not Physical Relief

The market's response to US-Iran deal signals on May 27 was the strongest and longest-lasting since the ceasefire, and that is precisely why European gas has not priced the winter risk. When oil falls 5.5% in a single session on diplomatic progress, the market reads it as broad energy normalization.

WTI crude fell 5.5% to $88.68/barrel, and Brent dropped 5.3% to $94.29 on May 27, six-week lows for both benchmarks, after US Secretary of State Rubio stated an agreement was days away and Tehran confirmed talks were continuing despite ongoing military skirmishes, marking the first concurrent positive signals from both sides since the February 28 conflict began. The session decline unwound six weeks of war-premium accumulation in hours.

What the price action did not do is change physical supply conditions. Options markets continue placing a 37% implied probability on WTI above $100/barrel within three months, per Kieran Tompkins of Capital Economics (WSJ). A market that had fully priced a completed deal would not sustain that tail. What moved on May 27 was probability weighting on the diplomatic outcome, not the underlying physical condition of either the crude or LNG supply chain.

Two Supply Chains Are Running on Two Separate Timelines

The Hormuz blockade simultaneously disrupted crude exports and LNG transit, but the mechanisms governing each market's recovery operate on different clocks. Physical crude flows through the Strait require infrastructure damage assessment before normalization can begin, and that assessment cannot start until hostilities end. Iranian LNG export infrastructure specifically requires a minimum six-month restart window post-hostilities; the October European gas storage injection deadline falls within that window regardless of when a deal is signed.

US natural gas settled higher on May 27 for reasons entirely disconnected from the diplomatic news: Nymex June contract expiry triggered short-covering, summer heat demand is building nationally, and global LNG export demand is running at exceptional strength as facilities return from maintenance. The link between oil and gas markets runs through the Strait itself; the near-term pricing of each now runs through entirely separate mechanisms.

A Signed Deal Ends the Oil Crisis Before It Ends the Gas Shortage

European LNG import operators and storage names face a six-month lag that a diplomatic headline cannot compress. Even with a signed agreement, physical flows may require six months to normalize, and infrastructure damage cannot be assessed until hostilities end. Europe's injection season closes in October; Iranian LNG cannot reach European terminals before that deadline under any current negotiating timeline. Investors holding European LNG import terminal equities or TTF-linked instruments collect the storage deficit premium regardless of whether negotiations succeed or collapse; the six-month restart lag is the position, not the diplomatic outcome.

The Structural Gas Trade Pays in Both Scenarios; Oil Equity Faces a Binary

European LNG import terminal operators and gas storage names carry the asymmetric position: TTF at Rabobank's Q3 base case of 60 EUR/MWh and year-end target of 69 EUR/MWh represents a 30% premium over current spot (WSJ), and that target is driven by the six-month LNG restart lag rather than by the diplomatic outcome. The position pays under both the base case and the bear case because the mechanism, infrastructure restart time, is independent of whether negotiations succeed.

The Numbers That Confirm or Collapse Each Position

WTI holding above $85/barrel sustains the Hormuz war premium. US shale, West African, and Canadian oil sands operators collect elevated margins at this level, and short oil equity positions built on deal expectations face sustained mark-to-market pressure while this threshold holds. A single close below $85/barrel is noise; 10 consecutive closes below it is the exit signal for upstream producers outside Persian Gulf transit.

WTI closing below $85/barrel for 10 consecutive trading days signals the market has concluded the deal is effectively complete, the war premium is removed, and oil equity valuations built on $90+ crude require reassessment. TTF falling below 40 EUR/MWh in July signals European storage injections are running ahead of schedule, and Rabobank's year-end target of 69 EUR/MWh is no longer operative. Oil equity and gas storage exposure diverge at this threshold; the oil position requires reassessment while the gas position remains intact, because the six-month LNG restart lag does not change when oil falls.

Analyst's Notes

Subscribe to Our Channel

Stay Informed