10,000-tU Uranium Supply Gap Widens as Russian Import Ban & AI Demand Increase Future Requirements

Russian import restrictions, AI-driven nuclear demand, and a 10,000-tU supply deficit are increasing the need for new uranium supply.

- The Prohibiting Russian Uranium Imports Act will ban Russian enriched uranium imports into the US by January 1, 2028, removing a supply source that previously met approximately 25% of US utility requirements and increasing demand for alternative Western supply.

- Global uranium production of approximately 60,000 tU per year falls 10,000 tU short of reactor requirements, while secondary supply sources that have filled the gap are declining.

- Meta's plan to procure up to 6.6 gigawatts of nuclear power by 2035 and Microsoft's similar commitments have introduced a new source of uranium demand beyond traditional utilities.

- The DOE has committed $2.7 billion to restore domestic uranium enrichment capacity, while the Trump administration aims to expand US nuclear capacity from approximately 100 gigawatts to 400 gigawatts by 2050, increasing future uranium demand.

- Production-stage US uranium producers and development-stage assets in Western-aligned jurisdictions are positioned to benefit as utilities replace Russian supply and secure future uranium production.

Supply Removal & New Nuclear Buyers Increase Pressure on Uranium Markets

In 2026, government policy and new sources of nuclear demand are influencing uranium markets alongside traditional utility buying. The US ban on Russian uranium imports will remove a supply source that previously met approximately 25% of US utility requirements by January 2028. Technology companies are also signing long-term nuclear power agreements to support artificial intelligence data centers, creating an additional source of uranium demand.

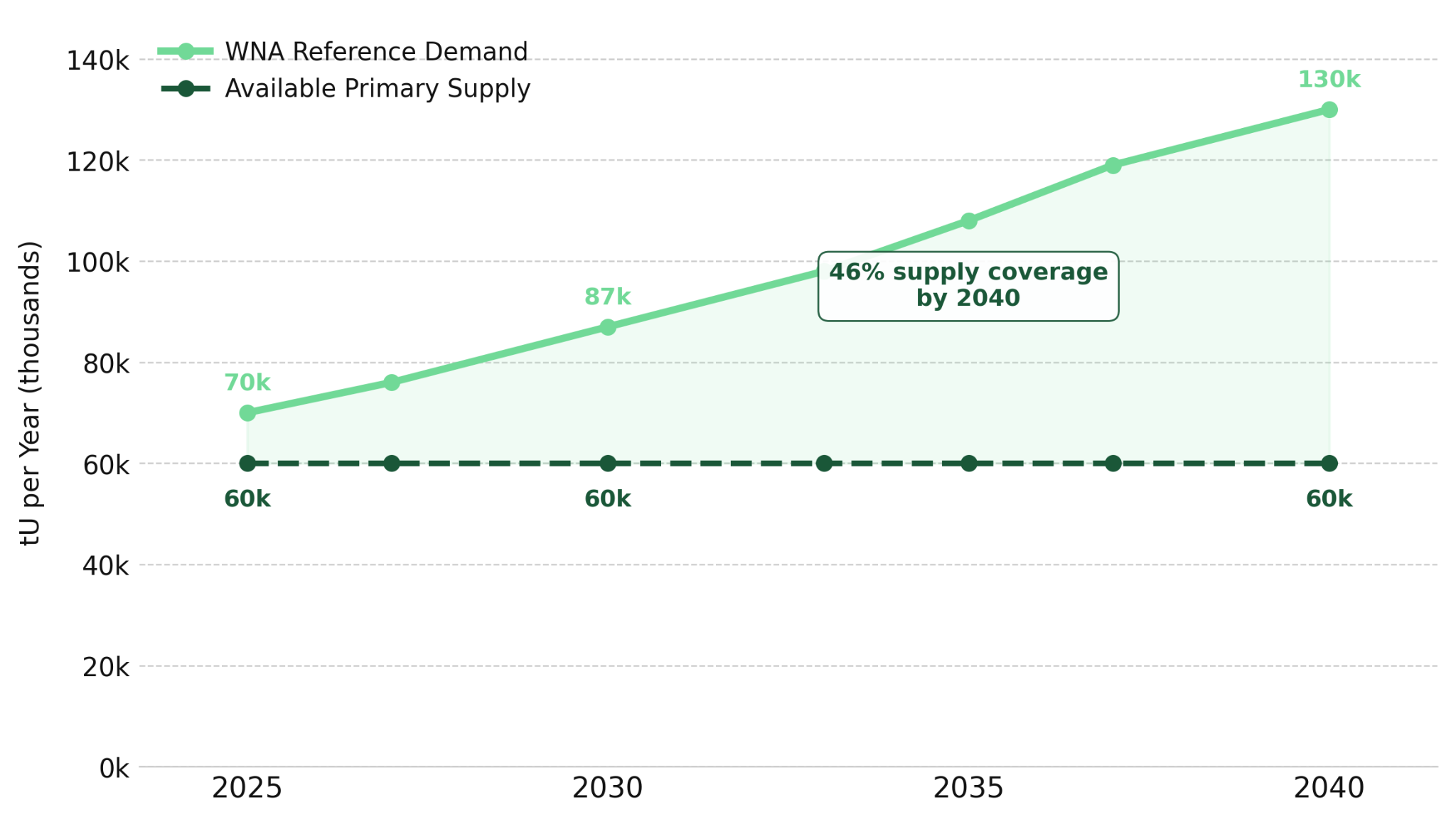

The uranium market was already undersupplied before the Russian import ban and AI-related nuclear demand emerged. The World Nuclear Association's 2025 Nuclear Fuel Report estimates annual reactor fuel requirements of approximately 70,000 tU versus mine production of approximately 60,000 tU, leaving a supply gap of about 10,000 tU per year. Secondary supplies such as government stockpiles and reprocessed fuel have helped fill that gap, but those sources are declining.

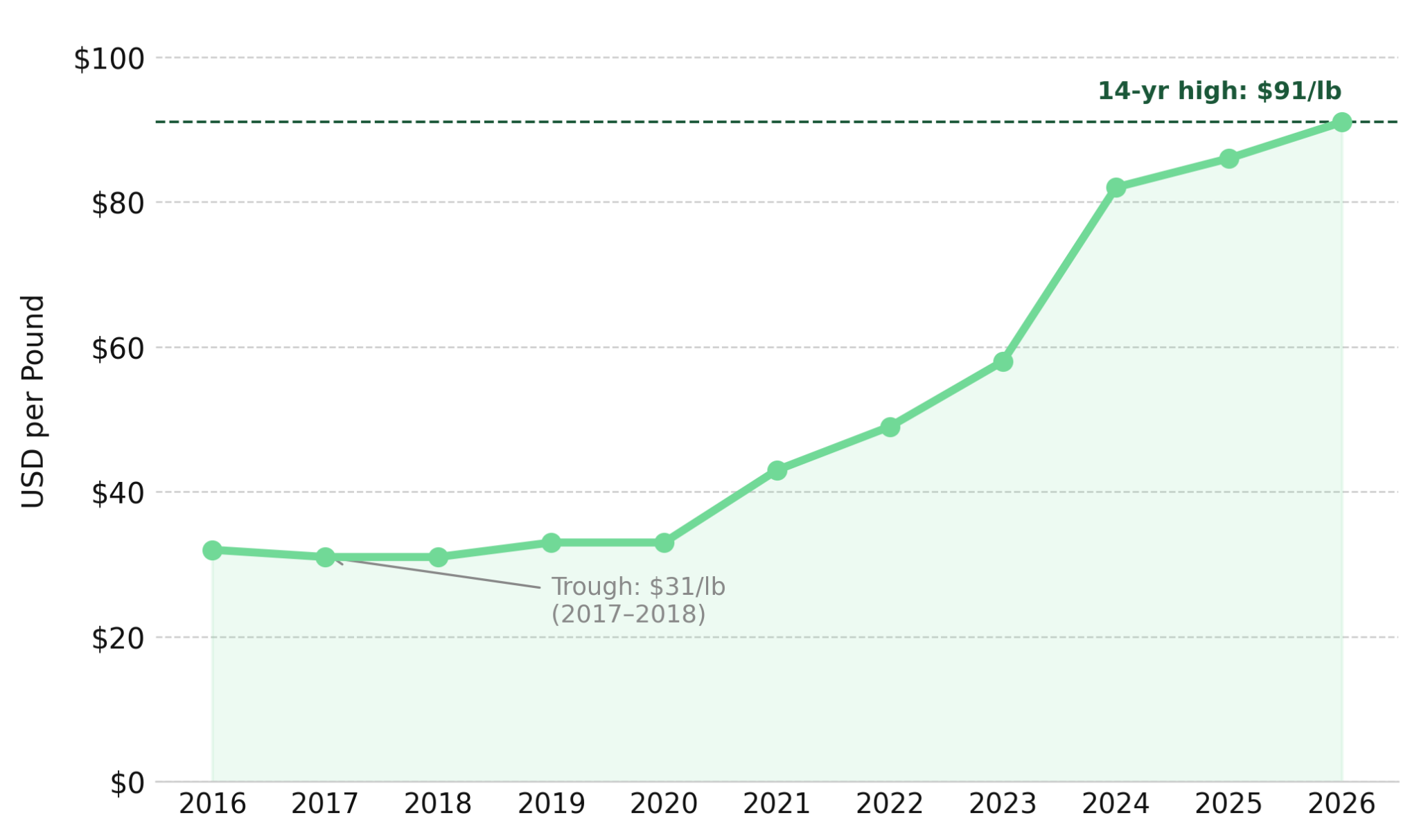

As of June 22, 2026, uranium spot prices stood at $85.75 per pound, down from a 2026 high of $101.41 per pound on January 29. Long-term contract prices remained at a 14-year high of $90 to $91.50 per pound, indicating utilities are still securing future supply at those levels. Higher long-term contract prices support producers and developers that can add new uranium supply.

Import Restrictions & Enrichment Constraints Accelerate Utility Contracting

The Prohibiting Russian Uranium Imports Act, enacted in May 2024, will ban low-enriched uranium (LEU) imports from Russia beginning January 1, 2028. Before the ban, Rosatom controlled approximately 44% of global uranium enrichment capacity and supplied approximately 25% of the enriched uranium consumed by US utilities. That supply source will disappear in 18 months, while Western enrichment capacity remains insufficient to replace it.

The DOE awarded $2.7 billion in enrichment contracts in January 2026 to expand US uranium fuel supply capacity. The contracts provide $900 million each to American Centrifuge Operating, General Matter, and Orano Federal Services to expand LEU and high-assay low-enriched uranium (HALEU) capacity. Industry estimates indicate Western enrichment capacity will not fully replace Russian supply before 2030, increasing pressure on utilities to secure long-term contracts before the 2028 ban takes effect. Annual contracting volumes remain below the industry's 150 million pound replacement-rate benchmark, leaving utilities with uranium purchases that must be contracted before 2028.

Energy Fuels owns and operates the White Mesa Mill in Utah, the only operating conventional uranium mill in the US. Its mid-year 2026 production update reported approximately 1.6 million pounds of finished U₃O₈ production in six months, reaching the lower end of its full-year guidance range of 1.5 to 2.5 million pounds ahead of schedule. Mark Chalmers, Chief Executive Officer of Energy Fuels, highlights the difficulty of bringing new uranium supply online:

"You see it around the world, the challenges people have been having are restarting and getting projects going. Prices still aren't where they really need to be long term. The uranium business looks fantastic going forward."

Data Center Power Demand & Nuclear Procurement Increase Uranium Requirements

In 2026, technology companies began signing nuclear power agreements to support AI infrastructure. Meta agreed in January 2026 to procure up to 6.6 gigawatts of nuclear power by 2035 through a 20-year power purchase agreement with Vistra and additional agreements with TerraPower and Oklo. Microsoft has also signed agreements to secure future nuclear power capacity. Each gigawatt of nuclear capacity requires approximately 400 tonnes of uranium annually for fuel. Meta's 6.6 gigawatt commitment implies recurring uranium demand of approximately 2,640 tU per year. The World Nuclear Association projects global uranium requirements will increase to approximately 87,000 tU annually by 2030.

Production Cuts & Supply Disruptions Tighten Uranium Markets

Global uranium mine production of approximately 60,000 tU per year remains below reactor requirements, while some producers have chosen not to return to full capacity. Kazatomprom, which controls approximately 40% of global uranium mine output, reduced its 2026 production target from 32,777 tU to 29,697 tU, removing approximately 6.8 million pounds from supply. The company stated that prevailing market conditions did not justify a return to full production, indicating the reduction was a commercial decision. SOMAÏR in Niger produced no uranium in 2025 under military junta control, removing another source of uranium supply available to Western buyers.

enCore Energy increased uranium extraction 22% year over year to 90,000 pounds in the first quarter of 2026 at cash extraction costs of $34.94 per pound. The company reported net income of $0.03 per share versus a loss of $0.13 per share a year earlier and held 153,956 pounds of uranium inventory. William Sheriff, Executive Chairman of enCore Energy, outlines the uranium market's supply challenge:

"The demand is there. The supply seems to be the troublesome component here. It is a lot harder and possibly even a little more expensive than people realize going forward."

Projected Supply Shortfalls Support New Uranium Mine Development

Current uranium production helps meet near-term reactor requirements but not projected demand growth in the 2030s. The World Nuclear Association projects that existing uranium supply could meet only 46% of projected demand between 2030 and 2040. Closing that gap will require development-stage projects to move through feasibility studies, permitting, and construction. Long-term uranium contract prices of $90 to $91.50 per pound increase the value of future mine production and may not be reflected in all developer valuations.

IsoEnergy is advancing the Hurricane deposit at the Larocque East project in Saskatchewan's Athabasca Basin, which hosts an indicated mineral resource of 48.6 million pounds of U₃O₈ at 34.5% U₃O₈, the world's highest-grade indicated uranium resource. The deposit is located approximately 40 kilometers from the McClean Lake processing facility and at a depth of approximately 325 meters, compared with approximately 450 meters at Cigar Lake, which could reduce future development costs. Philip Williams, Chief Executive Officer of IsoEnergy, discusses the growing competition for future uranium supply:

"The North American utilities and maybe European utilities are on the back foot. The Chinese just took a direct 45% interest in an African uranium project and got 60% of the off-take. They're thinking differently. Western utilities are behind and they're going to have to be scrambling to play a game of catch-up."

Atomic Eagle is advancing the Muntanga Uranium Project in Zambia, which hosts a combined Measured, Indicated, and Inferred resource of 58.8 million pounds of U₃O₈ and sits outside the Kazakhstan-Russia supply corridor. The 2026 drilling program expanded multiple mineralized zones and returned intercepts including 5.4 meters at 422 ppm U₃O₈, with additional grade-confirmation drilling expected shortly. Phil Hoskins, Chief Executive Officer of Atomic Eagle, explains why new uranium mine supply will be needed this decade:

"For the first time since the 1960s, towards the end of this decade, reactors are going to be dependent on new supply coming out of the ground. Since Fukushima, the market has been working through significant secondary supplies. That deficit, around 30 million pounds, is going to need to be rectified from uranium coming out of the ground."

Future Uranium Supply Depends on Discoveries Made Today

The discovery-to-production timeline in uranium averages 15 to 20 years, meaning projects needed between 2040 and 2045 must be identified and advanced today. The WNA's Upper Scenario projects annual uranium production must increase more than fourfold to support a tripling of global nuclear capacity. Existing mine restarts and development-stage projects are unlikely to provide all of that supply, increasing the need for new discoveries today.

ATHA Energy controls 6.8 million acres of prospective uranium exploration ground across Canada, including 100% ownership of the Angikuni Basin in Nunavut. Three drill rigs are targeting approximately 20,000 meters across three mineralized corridors in 2026. The program follows 2025 drilling that intersected uranium mineralization on every target tested, including 34.7 meters of composite mineralization in the RIB North zone with grades up to 8.16% U₃O₈ over 0.5 meters. Troy Boisjoli, Chief Executive Officer of ATHA Energy, frames the growing gap between uranium supply and demand:

"Consensus supply-demand forecasts across the sector show the gaps are massive. We have had a lack of investment in new projects, new exploration, and new development-stage projects at the same time as demand is increasing at a rate that we haven't really seen before in the nuclear energy space."

Long-Term Contracting & Supply Requirements Support Uranium Markets

Uranium markets face near-term contracting pressure, medium-term supply constraints, and long-term demand growth. The Russian uranium import ban, technology company nuclear procurement, and DOE enrichment investments are supporting long-term uranium contract prices of $90 to $91.50 per pound, the highest level in 14 years. Utilities and government-backed buyers are signing contracts at those prices to secure future supply. By 2040, the World Nuclear Association projects that existing uranium supply could meet only 46% of projected demand. That gap increases the importance of companies capable of bringing new uranium supply into production.

The IEA's World Energy Outlook 2025 projects annual nuclear investment increasing from more than $70 billion today to approximately $210 billion by 2035, provided sufficient uranium mining, enrichment, and conversion capacity is available. The DOE's Reactor Pilot Program targets criticality for at least three advanced reactor designs by July 4, 2026, while its $2.7 billion enrichment investment supports expansion of the US nuclear fuel cycle. Reactor fuel requirements already exceed annual uranium mine production by approximately 10,000 tU, while long-term uranium contract prices of $90 to $91.50 per pound indicate utilities are already paying more to secure future supply.

The Investment Thesis for Uranium

- The Russian uranium import ban will remove a supply source that previously met approximately 25% of US utility enrichment requirements by January 2028.

- Long-term uranium contract prices have reached 14-year highs ahead of the January 2028 Russian uranium import ban, strengthening the position of domestic producers with US operating permits and processing infrastructure.

- Annual uranium mine production already falls approximately 10,000 tU short of reactor requirements, creating a supply gap that existing production cannot fully close.

- Kazatomprom reduced its 2026 production target by approximately 10%, while Niger's political disruption removed another source of uranium supply available to Western buyers. Secondary supplies also continue to decline, increasing the need for new uranium production.

- Technology companies are becoming a new source of uranium demand through multi-gigawatt nuclear power agreements signed to support artificial intelligence infrastructure.

- AI related nuclear power procurement sits outside traditional utility purchasing patterns and could increase uranium requirements beyond current forecasts through 2030 and beyond.

- Development-stage uranium projects are needed to help close projected supply gaps in the 2030s. Exploration programs in Canada's major uranium districts are targeting deposits that could become uranium mines in the 2040s.

The uranium market is entering a period in which supply growth is struggling to keep pace with rising demand. The January 2028 Russian import ban will remove a supply source that previously met approximately 25% of US utility requirements, while technology companies are adding new nuclear demand through long-term power agreements. Annual uranium mine production remains approximately 10,000 tU below reactor requirements, supporting long-term contract prices of $90 to $91.50 per pound. Meeting future demand will require new supply from producers, developers, and explorers across the uranium value chain.

TL;DR

The uranium market faces a growing supply challenge as the January 2028 US ban on Russian uranium imports removes a supply source that previously met about 25% of US utility needs, while technology companies add new nuclear power demand to support artificial intelligence infrastructure. Global uranium production remains about 10,000 tU below reactor requirements, and secondary supply sources continue to decline. Long-term uranium contract prices have risen to 14-year highs, reflecting utility concerns about future fuel availability. Meeting projected demand growth will require new supply from existing producers, development-stage projects, and exploration programs capable of bringing additional uranium resources into production.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed