150 US Fuel Cycle Bills & WNA's 2040 Projection Push Long-Term Repricing of Domestic Uranium Assets

US nuclear policy acceleration, WNA's 391–532M lb 2040 demand forecast, and fuel cycle localization are repricing uranium equities across the value chain.

- Nuclear energy is transitioning from a policy-constrained sector to a strategic infrastructure priority, driven by decarbonisation mandates, AI-driven electricity demand, and energy security legislation that extends uranium demand visibility across a multi-decade horizon.

- Fuel cycle localization is accelerating across the US and Europe, with federal and state governments committing capital to enrichment, conversion, and reprocessing capacity, tightening long-term uranium supply availability and creating jurisdictional pricing premiums for domestically aligned operators.

- Permitting reform and state-level deregulation are unlocking project pipelines, but multi-year regulatory timelines and capital intensity requirements for large-scale nuclear builds remain the primary deployment bottlenecks.

- Institutional capital is re-engaging with nuclear infrastructure following the cost overrun precedent established by Vogtle Units 3 and 4, but remains sensitive to capex discipline, ESG compliance frameworks, and skilled labor constraints.

- Equity markets are beginning to differentiate across the uranium value chain, with producers re-rated and capital rotating toward developers and explorers positioned to fill the supply gap created by declining output from legacy Tier-1 assets.

Nuclear Energy Strengthen Its Role in the Global Energy System

After more than a decade in which US and European nuclear policy retreated following the Fukushima accident in March 2011, governments across the United States and Europe are reframing nuclear energy as a permanent pillar of both energy security and decarbonisation strategy, not a transitional technology, but a long-duration infrastructure commitment with multi-decade capital implications.

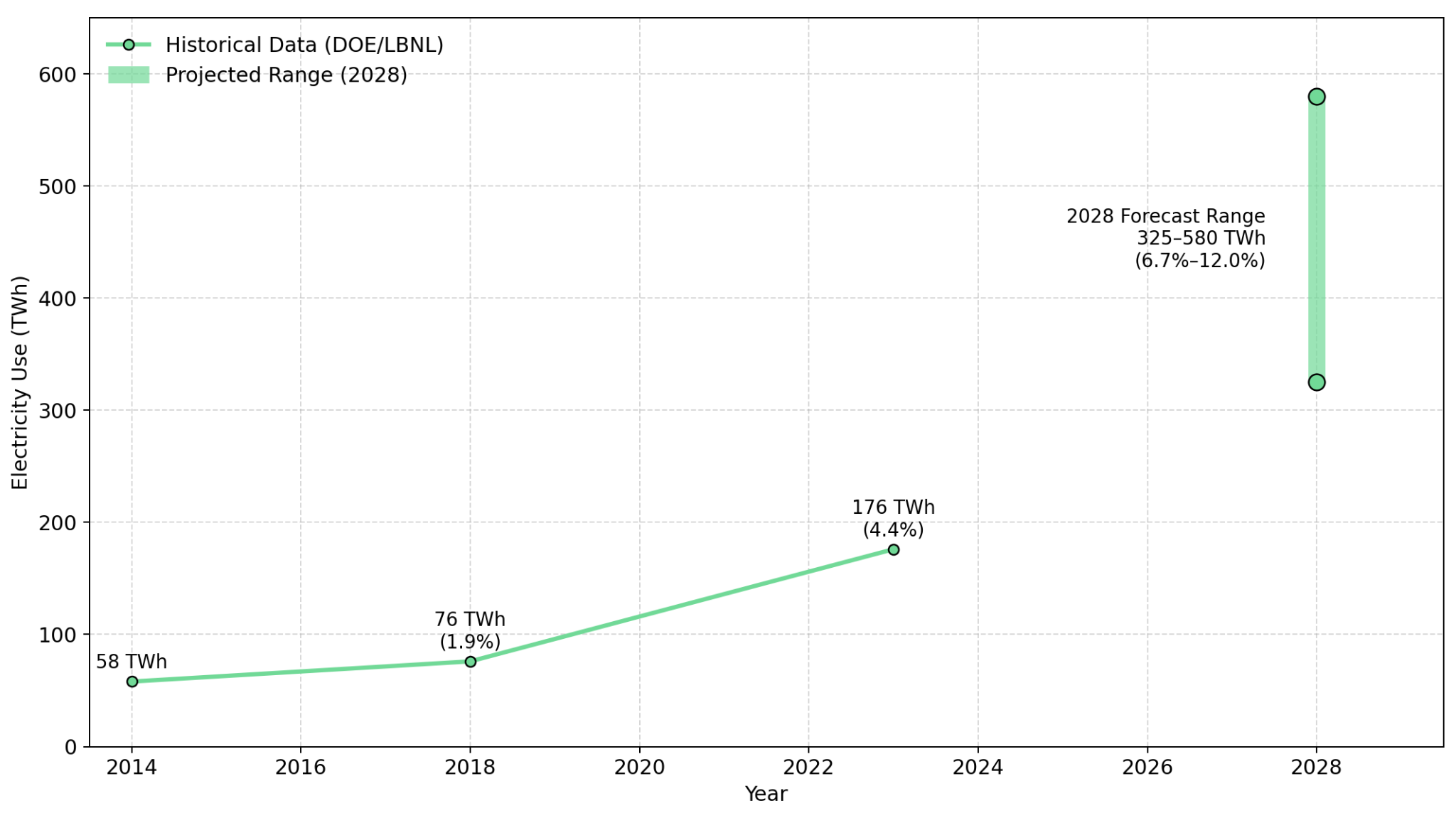

The rapid expansion of artificial intelligence infrastructure, cloud computing platforms, and hyperscale data centres, anchored by companies including Meta, Amazon, and Microsoft, is generating baseload electricity demand that intermittent renewable sources cannot reliably satisfy at scale. Nuclear energy, which delivers consistent carbon-free power, is emerging as the necessary complement to variable renewables across grid planning frameworks. The central question is not whether uranium demand will grow, but how quickly domestic supply chains can respond, and which segments of the value chain are positioned to capture the resulting jurisdictional pricing premium.

From Policy Resistance to Policy Acceleration

The National Conference of State Legislatures, in its News Reactor newsletter published 17 March 2026, tracked over 150 pro-nuclear bills introduced across US states in 2026 to that date. Arizona enacted legislation prohibiting local governments from blocking Small Modular Reactor construction once a federal early site permit has been granted, establishing a regulatory floor that reduces project-level political risk at the permitting stage. States including California and Oregon are reported to be reconsidering nuclear moratoriums under pressure from grid reliability requirements, though confirmed legislative actions in either state had not been publicly filed as of this publication.

Momentum & Market Signaling

This legislative volume functions as a direct signal to capital markets that nuclear energy has re-entered the investable infrastructure category. Regulatory clarity is extending long-term project visibility, and institutional investors are gaining confidence in deployment timelines previously treated as too uncertain to underwrite. However, policy acceleration does not eliminate execution risk: local opposition can still delay projects despite favorable national frameworks, introducing non-technical risk factors not captured in standard discounted cash flow models.

Big Tech, SMRs, & the New Demand Curve for Uranium

Small Modular Reactors, factory-built nuclear reactors designed for faster deployment and lower upfront capital costs than conventional gigawatt-scale plants, are increasingly structured as dedicated power solutions for data centre campuses, shifting nuclear procurement from a utility-driven model to a corporate-anchored energy market. The World Nuclear Association's Nuclear Fuel Report 2025 projects global uranium requirements reaching 391 million pounds per year by 2040 under its reference scenario, rising to 532 million pounds under the upper scenario, a demand range that reflects both traditional reactor buildouts and accelerating SMR deployment.

Supply responses to this demand profile are not yet visible in current production volumes. IsoEnergy's Hurricane deposit, at 34.5% U3O8 across 48.6 million pounds of resource, is among the few high-grade undeveloped assets globally capable of contributing meaningfully to supply at the scale this demand trajectory requires. Chief Executive Officer Philip Williams frames the deposit's significance:

"Hurricane is the highest-grade uranium resource in the world, we made a discovery in 2018, put a resource out in 2022, 34.5% grades, 48.6 million pounds. Extraordinary."

Domestic Fuel Processing: The Bottleneck Investors Are Watching

The binding near-term constraint on the uranium investment thesis operates within the nuclear fuel cycle itself. Conversion, enrichment, and fuel fabrication each carry geographic concentration risk linked to Russian-controlled infrastructure. Assets with jurisdictional alignment to US or European policy frameworks carry a structural pricing premium over equivalent assets in non-allied jurisdictions, a dynamic now beginning to be reflected in producer-level equity valuations.

Energy Fuels' March 2026 corporate presentation confirms that the White Mesa Mill in Blanding, Utah is the only operating conventional uranium mill in the United States, providing domestic processing capacity at the precise moment US policy is designed to support its utilization. Chief Executive Officer Mark Chalmers frames the company's positioning:

"Energy Fuels is a unique company because it is focused on building a critical mineral hub that revolves around the uranium business."

The same March 2026 presentation lists the Donald rare earth project in Victoria, Australia as shovel-ready and at the permitted, pre-construction stage, with Chalmers targeting a construction start in 2026, subject to a final investment decision, across a project carrying exposure to both heavy and light rare earth elements.

enCore Energy's domestic In-Situ Recovery production strategy complements the fuel cycle localization theme at the production stage. In-Situ Recovery dissolves uranium underground rather than requiring conventional mining infrastructure, reducing both the capital threshold for new production and permitting complexity. Executive Chairman William Sheriff stated that the company's New Mexico asset base holds approximately 80 million pounds of resources across four large deposits.

Capital Intensity, Permitting Timelines, & the Institutional Constraint

The Vogtle Units 3 and 4 project in Georgia established the most visible institutional benchmark for nuclear cost escalation risk. The Department of Energy subsequently extended a $26.5 billion loan package to Southern Company and its subsidiaries to support the company's financial recovery from Vogtle cost overruns alongside new generation and grid investments. For institutional investors, this precedent reinforces the importance of assessing capex discipline and financing structure sensitivity to inflation before committing capital to nuclear-adjacent equities.

For developers operating below the gigawatt scale, capital efficiency becomes the primary performance differentiator. IsoEnergy's corporate disclosures confirm toll milling agreements are in place with Energy Fuels' White Mesa Mill, allowing ore processing without constructing a new facility. The company's most recent corporate presentation reports a pro forma cash balance of approximately C$144 million as of 31 December 2025, adjusted for subsequent events. Philip Williams noted that the company's $50 million equity raise attracted investor demand he described as exceeding $300 million, more than six times subscribed.

Atomic Eagle's Muntanga uranium project in Zambia demonstrates an alternative capital efficiency pathway. An ASX announcement dated 10 March 2026 confirmed an upgraded JORC resource of 58.8 million pounds at 309 parts per million, comprising 40.0 million pounds in the Measured and Indicated categories and 18.8 million pounds Inferred. The company's 2025 Feasibility Study supports a net present value at an 8% discount rate of $243 million and an internal rate of return of 20.8%, underpinned by a heap leach design that avoids greenfield mill construction. Chief Executive Officer Phil Hoskins describes Atomic Eagle’s operating advantages:

"It is a very simple heap leach operation, excellent recoveries, plus 90% on average, 21-day average leach kinetics, and an extremely low acid consumption of 20 kilograms per ton of ore treated."

Supply Pipeline Reality & Exploration Upside

IsoEnergy's corporate presentation, citing Cameco's 2023 Cigar Lake Technical Report, identifies a scarcity of known resources capable of replacing Cigar Lake as it progresses through its mine life, an observation that underpins the supply replacement deficit visible in published forward contract market analysis. ATHA Energy holds a land position of over 7 million acres across Canada, comprising 3.8 million acres in the Athabasca Basin, 3.1 million acres in Nunavut, and 268,000 acres in the Central Mineral Belt. Investors should note that this total includes acreage held under a 10% carried interest on portions of NexGen and IsoEnergy land within the Athabasca Basin, which carries a different capital exposure profile than directly held mineral rights, providing discovery optionality at a capital efficiency level structurally distinct from development-stage project investment.

The Investment Thesis for Uranium

- Nuclear energy's re-designation as critical infrastructure by the US and European Union governments extends demand visibility across a multi-decade timeframe, supporting a sustained re-rating of uranium equities and reducing the policy risk that previously suppressed institutional capital allocation to the sector.

- Fuel cycle localization policy in the US and Europe creates a structural pricing premium for operators within allied jurisdictions, with Energy Fuels, operator of the only conventional US uranium mill, and enCore Energy's domestic In-Situ Recovery assets positioned as direct beneficiaries that competitors cannot replicate on short timelines.

- Developers minimizing capital intensity through confirmed toll milling arrangements or low-cost extraction methods, IsoEnergy through its White Mesa Mill agreements and Atomic Eagle through the Muntanga heap leach design supporting a 20.8% IRR in the 2025 Feasibility Study, are positioned to deliver superior returns relative to conventional projects requiring greenfield processing infrastructure.

- The supply pipeline's structural deficit, anchored by the scarcity of known resources capable of replacing Cigar Lake and the absence of an equivalent Tier-1 asset at construction-ready status, creates conditions for sustained uranium price support that benefit explorers with large, high-quality land positions, most directly ATHA Energy's 7-million-plus-acre Canadian portfolio.

- The WNA Nuclear Fuel Report 2025 projects demand reaching between 391 million and 532 million pounds annually by 2040, a range that distributes consumption growth across a broader set of end users than prior cycles and accelerates the timeline to supply-demand imbalance.

Policy Is Driving the Cycle, but Execution Will Define Returns

The global nuclear renaissance is an active infrastructure investment program supported by federal legislation, state-level permitting reform, and corporate energy procurement commitments from the world's largest technology companies. For investors, this cycle requires differentiation across the value chain. Producers with domestic processing infrastructure and policy alignment are positioned to capture the jurisdictional premium embedded in US fuel cycle localization. Developers with high-grade resources, established feasibility economics, and capital-efficient structures offer re-rating potential as supply gaps become visible in forward contract markets. Explorers with large land positions and carried interest structures provide optionality on the discovery upside required to sustain reactor buildout commitments through the 2030s. The policy architecture is in place - execution risk across permitting timelines, capital deployment, and skilled labor will determine which companies convert structural demand growth into investor returns.

TL;DR

Global nuclear energy has shifted from a policy-constrained sector to a strategic infrastructure priority, driven by AI-generated baseload demand, energy security legislation, and fuel cycle localization across the US and Europe. The World Nuclear Association projects uranium requirements reaching between 391 million and 532 million pounds annually by 2040, while domestic supply chains remain structurally underprepared to meet that trajectory. With over 150 pro-nuclear state bills tracked in Q1 2026, institutional capital is re-engaging and differentiating across producers, developers, and explorers. Execution risk, across permitting timelines, capital discipline, and skilled labor - will determine which companies convert structural demand growth into returns.

FAQs (AI-Generated)

The World Nuclear Association's Nuclear Fuel Report 2025 projects global uranium requirements reaching between 391 million and 532 million pounds per year by 2040, driven by traditional reactor buildouts, accelerating Small Modular Reactor deployment, and corporate energy procurement commitments from major technology companies requiring reliable baseload power for AI infrastructure and data centres.

Fuel cycle localization refers to government-backed efforts to build domestic conversion, enrichment, and fuel fabrication capacity, reducing dependence on Russian-controlled infrastructure. For investors, assets jurisdictionally aligned with US or European policy frameworks carry a structural pricing premium over equivalent assets in non-allied jurisdictions, a dynamic now beginning to appear in producer-level equity valuations.

The Vogtle Units 3 and 4 project in Georgia established the most visible benchmark for nuclear cost escalation risk, requiring a $26.5 billion Department of Energy loan package. This has made institutional investors more sensitive to capex discipline, financing structure, and inflation exposure before committing capital to nuclear-adjacent equities — elevating capital-efficient development models such as toll milling and heap leach extraction.

SMRs are increasingly structured as dedicated power solutions for data centre campuses, shifting nuclear procurement from a utility-driven model to a corporate-anchored energy market. Companies including Meta, Amazon, and Microsoft are anchoring baseload demand through SMR offtake agreements, expanding the end-user base for uranium beyond traditional utilities and accelerating the timeline to supply-demand imbalance.

Producers with domestic processing infrastructure — such as Energy Fuels, operator of the only conventional US uranium mill — are positioned to capture the jurisdictional premium from fuel cycle localization policy. Developers with high-grade resources and capital-efficient structures offer re-rating potential as supply gaps become visible in forward contract markets. Explorers with large land positions, such as ATHA Energy's seven-million-plus-acre Canadian portfolio, provide optionality on the discovery upside required to sustain reactor buildout commitments through the 2030s.

Analyst's Notes

Subscribe to Our Channel

Stay Informed