Federal Reserve Holds Rates: Guidance May Leave Gold's Near-Term Direction Unresolved

Fed holds rates at 3.5-3.75% with balanced guidance, leaving gold's near-term direction data-dependent while structural demand keeps the price floor intact.

- The Fed held the federal funds rate at 3.5%-3.75% on March 18, with one dissenting vote preferring a 25bp cut, the clearest internal signal of dovish pressure within the committee.

- Powell's statement acknowledged elevated inflation and softening labor markets simultaneously, delivering balanced dual-mandate language rather than a directional signal on rate cut timing.

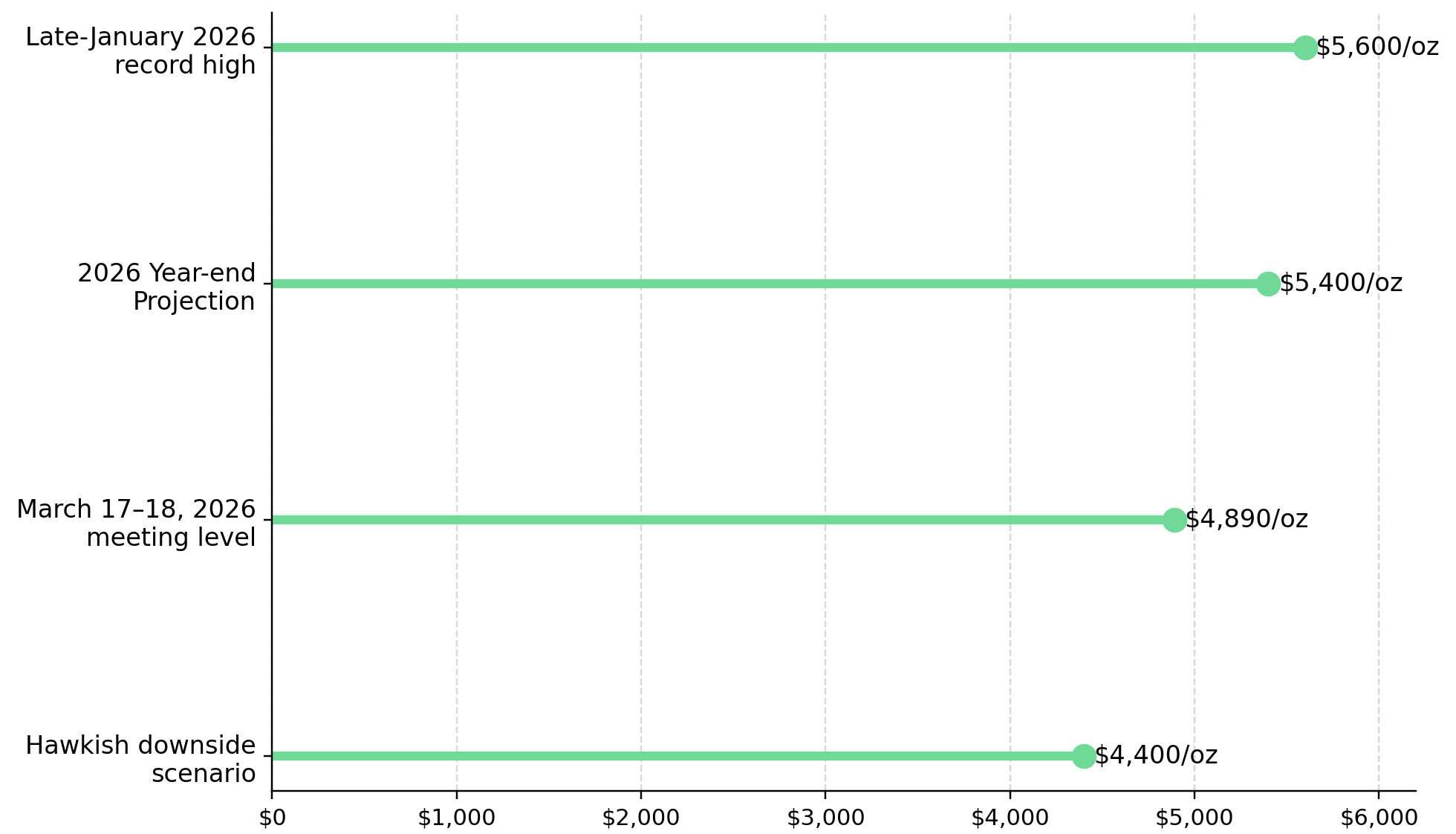

- The outcome avoids the hawkish scenario that would have accelerated downside toward $4,400/oz, but falls short of the dovish pivot needed to re-accelerate gold toward $5,400/oz in the near term.

- Gold's structural price floor, anchored by central bank accumulation exceeding 1,000 tonnes annually and record January 2026 ETF inflows, remains intact and independent of the Fed's near-term policy ambiguity.

- For investors evaluating producers, developers, and explorers, the analytical distinction remains between short-term volatility driven by policy uncertainty and structural value creation driven by project economics and resource quality.

The Policy Dilemma at the March 2026 FOMC Meeting

Gold entered the March 17–18, 2026 Federal Reserve meeting at $4,890/oz, having corrected from a January 2026 all-time high of nearly $5,600/oz. The Federal Reserve held the federal funds rate at 3.5%–3.75%, as widely anticipated, with the committee's forward guidance serving as the primary market catalyst.

The policy dilemma is direct: US military strikes on Iran's Kharg Island, the country's primary deep-water oil export facility, have pushed oil prices sharply higher, amplifying headline inflation pressures at the same time US labor market conditions are weakening.

Gold is a non-yielding asset, meaning it competes directly with real yields, inflation-adjusted bond returns. When real yields rise, the opportunity cost of holding gold increases, placing downward pressure on prices. The Fed's guidance on rate trajectory is therefore the transmission mechanism between policy language and gold price movement.

Structural Demand Conditions at the Time of the Rate Decision

Central bank gold accumulation has exceeded 1,000 tonnes annually for three consecutive years, with sovereign buyers in China, India, Turkey, and Poland among the most active. January 2026 registered record gold ETF inflows, with institutional outflows remaining contained during the subsequent price correction, indicating longer-duration capital deployment that is less sensitive to short-term yield spreads than tactical positioning.

This demand profile does not eliminate downside risk from a hawkish Fed outcome, but it establishes a structural price floor. The distinction between policy-driven volatility and structural demand is material when evaluating how much short-term market volatility they can take.

Fed Guidance Scenarios & Their Transmission to Gold Pricing

The Fed did not characterize oil-driven inflation as persistent, which avoids the conditions that would accelerate downside toward $4,400/oz through a materially stronger dollar and rising real yields. Equally, the statement did not signal a shift toward rate cuts or frame labor market softness as the dominant concern, which means the conditions required to re-accelerate gold toward Goldman Sachs' $5,400/oz target have not yet materialized from this meeting.

The practical effect is that gold's near-term direction remains data-dependent rather than policy-resolved. The committee's statement identified four variables that will govern its next move: labor market conditions, inflation pressures and inflation expectations, and financial and international developments. For gold investors, these map directly onto the tracking indicators that carry the most forward signal, the next PPI release, subsequent labor market data, dot plot revisions at future meetings, and geopolitical developments affecting oil supply from the Middle East.

For producers, the guidance preserves current margin structures without the immediate financing headwinds a hawkish outcome would have introduced. For developers and explorers, financing conditions remain unchanged in the near term, with the Miran dissent providing a marginal signal that the committee's next move is more likely to be a cut than a hike, a directional indicator that improves the probability-weighted NPV case for capital-intensive projects.

Cost Structures & Capital Positioning Among Producers and Developers

Integra Resources produces at Florida Canyon with 2026 guidance of 70,000–75,000 oz and a multi-year ramp to 80,000-90,000 oz/year by 2027. George Salamis, President and Chief Executive Officer of Integra Resources, frames the current investment phase:

"2026 is about building capacity today at Florida Canyon to deliver more ounces, stronger cash flow, lower costs tomorrow."

Margin resilience across both scenarios is anchored in cost structure and balance sheet strength. Perseus Mining operates three producing mines, Yaouré, Edikan, and Sissingué, with a net cash position of $755 million, and total liquidity of $1.2 billion. Serabi Gold holds the Palito Complex in Brazil's Tapajós province, generating a projected 2026 free cash flow yield of 21% at a market-implied deep discount to net asset value. West Red Lake Gold Mines restarted Madsen Mine at 500 tonnes per day in May 2025, ramping toward 50,000 oz/year in 2026 and adding 35,000 oz/year from the Rowan deposit by 2028.

i-80 Gold is advancing the Lone Tree autoclave facility, a former Newmont-operated pressure oxidation plant in Nevada, with an overall capital cost of $430 million and a target for first gold production by the end of 2027, ramping to approximately 150,000 oz/year at commercial production. Paul Chawrun, Chief Operating Officer of i-80 Gold, contextualizes the institutional confidence behind the financing process:

"We have first-rate institutions that have been able to provide us with the confidence to put this together, we went through comprehensive due diligence, we had a competitive process, and there were a lot of interested parties to be part of this story."

Near-Term Milestones & Project Advancement

Several companies carry near-term catalysts that are relevant regardless of the macro scenario because they reflect execution progress rather than gold price dependency. New Found Gold is advancing its Queensway project in Newfoundland toward first production by targeting ore delivery to the Pine Cove Mill, a third-party permitted processing facility, by end of 2027, subject to financing and permitting. Keith Boyle, Chief Executive Officer of New Found Gold, describes the economic profile at current prices:

"The cost of trucking plus processing is about a gram, we're shipping 9 to 10-gram material, at an all-in sustaining cost of $1,300/oz, you're looking at over $250 million of free cash flow over the first four years."

U.S. Gold Corp., with its CK Gold Project in Wyoming, offers a different dimension of near-term optionality: state-level permitting in place, a feasibility study described by management as imminent, and an 18–24 month construction timeline targeting production by late 2027 or 2028, subject to financing. George Bee, President, Chief Executive Officer, and Director of U.S. Gold Corp., identifies the jurisdictional advantage as a differentiator:

"We're situated in Wyoming, the state is a resource state. They have people in the regulatory agencies that understand the industry, and we're not subject to changing laws."

Development Timelines & Resource Scale

Cabral Gold's Phase 1 heap leach operation at Cuiú Cuiú in Brazil's Tapajós province is 54% complete, fully funded via a $45 million gold loan, and targeting commercial production in Q4 2026 at an after-tax IRR of 78% and initial capital of $37.7 million.

Tudor Gold's Treaty Creek project hosts 24.9 million indicated ounces of gold in British Columbia's Golden Triangle, with a preliminary economic assessment targeting completion in summer 2026. Joseph Ovsenek, President and Chief Executive Officer of Tudor Gold, identifies infrastructure proximity as a key cost management factor:

"Our Treaty Creek project is located 70 kilometers north of the town of Stewart... That keeps costs down, and we can build our transmission line right alongside the road."

Hycroft Mining, which published its 2026 Mineral Resource Estimate showing an average 50% increase in gold and silver, sits at a comparable transition point. President and Chief Executive Officer Diane Garrett quantifies the updated resource position:

"Measured and indicated, we had about 10.5 million ounces of gold, we're now over 16 million ounces, plus substantial inferred material. On silver, we were at 362 million ounces and are now just shy of 600 million."

Exploration-Stage Exposure

P2 Gold's exploration project in Nevada holds 3.45 million AuEq ounces, with a 2025 preliminary economic assessment projecting after-tax net cash flow of $1.7 billion at $2,350/oz gold, and a water permit targeting approval in Q1 2026.

Large-scale resource systems with infrastructure access provide convex exposure to higher gold prices under sustained easing.

The Investment Thesis for Gold

- Gold's structural demand profile, anchored by central bank accumulation exceeding 1,000 tonnes annually and record January 2026 ETF inflows, supports a price floor that is not dependent on any single Fed policy decision.

- Low-cost producers with strong balance sheets and defined production growth timelines provide direct leverage to gold prices with margin resilience across different policy scenarios.

- Developers with fast-payback project economics and jurisdictional advantages in stable regulatory environments offer NPV expansion potential that is material at current and higher gold prices.

- Large-scale development projects with institutional financial backing and defined construction timelines translate macro tailwinds into production-stage earnings visibility within a two-to-three-year window.

- Explorers and advanced-stage resource holders with multi-million-ounce systems and infrastructure access provide convex exposure to higher gold prices and are positioned for valuation re-ratings under sustained easing conditions.

- Jurisdictional positioning in the United States and Canada reduces permitting risk and execution uncertainty relative to comparable assets in higher-risk geographies, a distinction that institutional capital is increasingly pricing into valuation.

The March 2026 Federal Reserve meeting produced a hold, a dissent, and deliberate ambiguity, a combination that resolves neither the hawkish nor the dovish scenario gold markets were positioned around. The committee acknowledged elevated inflation and softening labor markets without prioritizing either, leaving rate cut timing dependent on incoming data rather than a policy signal.

For gold, the meeting outcome removes the immediate risk of a hawkish repricing toward $4,400/oz while leaving the catalyst for a re-acceleration toward $5,400/oz deferred to future data releases and subsequent meetings. The three variables that may carry the clearest directional signal from here are the next PPI release, subsequent labor market reports, and geopolitical developments affecting oil supply from the Middle East. What none of these variables will alter is the demand beneath gold's price: central banks accumulating at scale, institutional capital deployed with longer duration, and a production side that remains structurally constrained. Policy ambiguity, in this context, is a condition to navigate, not a reason to exit a position grounded in durable, measurable demand.

TL;DR

The March 2026 FOMC meeting held the federal funds rate at 3.5%–3.75%, with one dissenting vote favoring a cut. Powell's balanced language acknowledged both elevated inflation and softening labor markets without signaling a directional shift, leaving gold's near-term trajectory unresolved. The outcome removes the immediate risk of a hawkish repricing toward $4,400/oz but defers the catalyst for a move toward $5,400/oz to future data. Gold's structural floor, supported by central bank accumulation exceeding 1,000 tonnes annually and record January 2026 ETF inflows, remains intact. For equity investors, the distinction between policy-driven volatility and project-level value creation remains the relevant analytical lens.

FAQs (AI-Generated)

The Federal Reserve held the federal funds rate at 3.5%–3.75% at its March 17–18 meeting, citing a policy dilemma created by simultaneously elevated inflation—partly driven by oil price spikes following US military strikes on Iran's Kharg Island—and softening US labor market conditions. Rather than prioritizing one mandate over the other, the committee issued balanced dual-mandate language, leaving rate cut timing dependent on incoming economic data rather than a firm policy signal.

The hold with balanced guidance removes the immediate downside risk of a hawkish scenario that could have driven gold toward $4,400/oz through a stronger dollar and rising real yields. However, it also stops short of the dovish pivot required to re-accelerate gold toward the $5,400/oz target cited by Goldman Sachs. Gold's near-term direction is now data-dependent, with the next PPI release, labor market reports, and Middle East geopolitical developments serving as the primary forward signals.

Central bank gold accumulation has exceeded 1,000 tonnes annually for three consecutive years, with sovereign buyers in China, India, Turkey, and Poland among the most active. January 2026 registered record gold ETF inflows, and institutional outflows remained contained during the subsequent price correction. This demand profile reflects longer-duration capital deployment that is less sensitive to short-term yield spreads than tactical positioning, establishing a price floor that is independent of any single Fed policy decision.

For developers, financing conditions remain unchanged in the near term. The single dissenting vote in favor of a rate cut provides a marginal signal that the committee's next move is more likely to be a cut than a hike, which improves the probability-weighted NPV case for capital-intensive development projects. For explorers holding large-scale resource systems with infrastructure access, the removal of immediate hawkish repricing risk preserves the valuation conditions under which multi-million-ounce assets attract institutional attention.

Several company-specific catalysts are relevant independent of the macro outcome. New Found Gold is targeting ore delivery to the Pine Cove Mill by end of 2027. U.S. Gold Corp. has described its CK Gold Project feasibility study as imminent, with an 18–24 month construction timeline. Tudor Gold is targeting completion of its Treaty Creek preliminary economic assessment in summer 2026. i-80 Gold is advancing the Lone Tree autoclave facility toward first gold production by end of 2027, ramping to approximately 150,000 oz/year at commercial production. Each milestone reflects execution progress rather than gold price dependency.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed