Gold's $4,000 Breakout Signals a Flight to Safety: How Policy Uncertainty & Rate Cuts Are Reshaping Capital Flows

Gold breaks $4,000 as policy uncertainty drives safe-haven flows. Fed rate cuts, dollar weakness, and central bank buying lift forecasts to $4,900 by 2026.

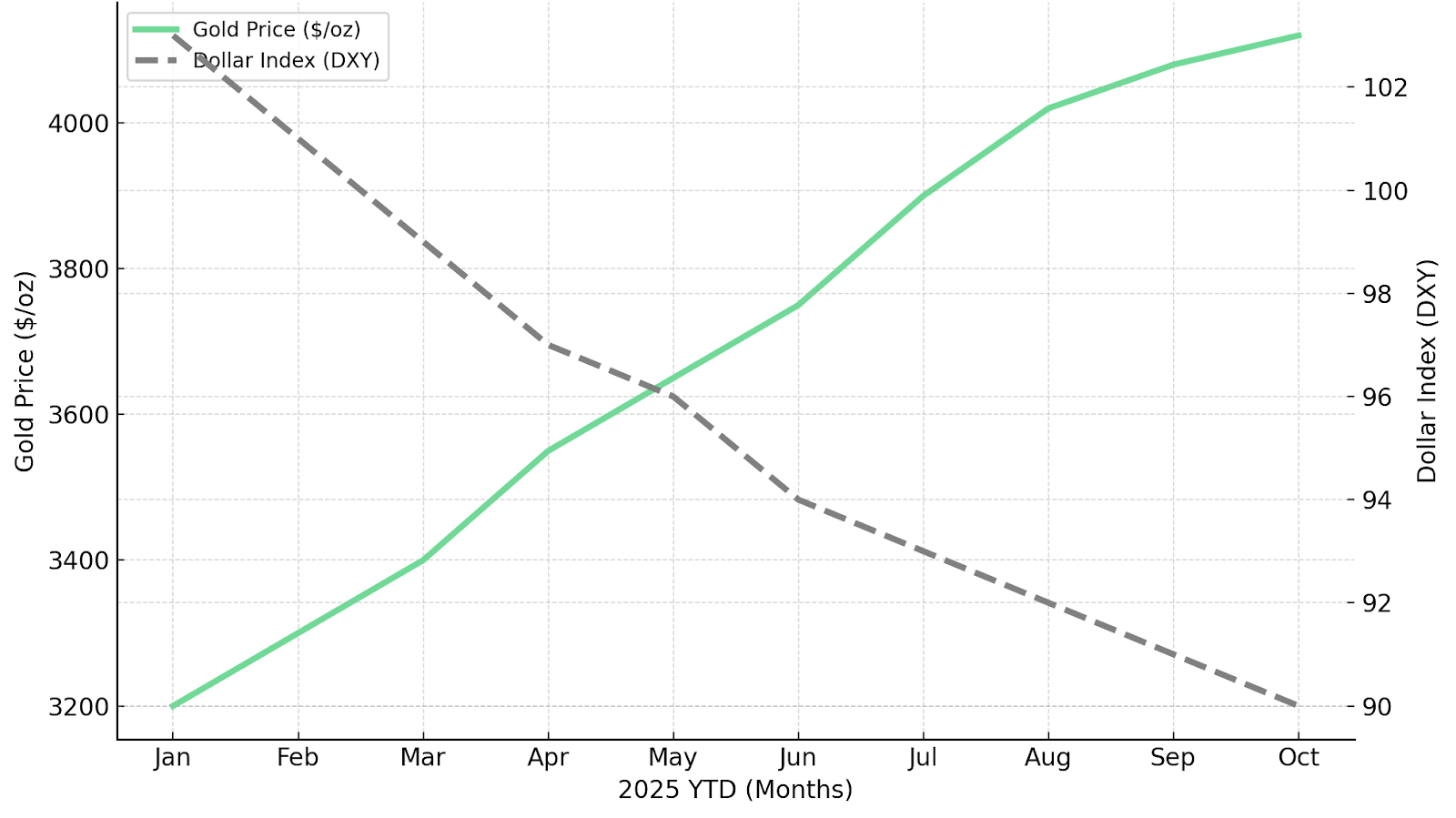

- Gold futures broke past $4,000 per ounce for the first time in history, marking a 50% to 54% year-to-date gain in 2025 and establishing it as one of the year's best-performing assets across all categories.

- Investors are exiting Treasurys and equities amid US policy paralysis and global instability, driving the strongest safe-haven flows in a decade as faith in conventional assets erodes under governance and fiscal uncertainty.

- The Federal Reserve's dovish tone and renewed rate-cut cycle have eroded real yields and triggered the dollar's steepest decline since the 1970s, re-energizing the debasement trade narrative among macro allocators.

- Central bank purchases exceeding 1,000 tonnes annually since 2022 and record exchange-traded fund inflows of $64 billion year-to-date, including $17.3 billion in September alone, have solidified gold's structural floor above $3,800 per ounce.

- Analysts including Goldman Sachs have raised forecasts to $4,900 per ounce by the end of 2026, with risks skewed to the upside, implying further rerating potential across low all-in sustaining cost producers and advanced developers.

Gold Reclaims Its Role as the Ultimate Hedge

Gold's breach of the $4,000 threshold marks a profound shift in global capital allocation. For the first time since 2020, investors are prioritizing liquidity and preservation over yield as policy uncertainty, rate cuts, and political dysfunction undermine faith in conventional assets. The US government shutdown has paralyzed spending appropriations and delayed the release of key economic indicators, forcing market participants to reprice risk across portfolios using secondary data sources and heightened uncertainty premiums.

This rally reflects a rational repricing of trust rather than speculative exuberance. Institutional portfolios are being recalibrated to reflect geopolitical risk spanning the Middle East and Ukraine, currency debasement concerns tied to ballooning federal debt, and the diminishing appeal of traditional safe havens including US Treasurys. Ray Dalio has compared the current rally to the 1970s gold surge, noting that gold is definitely a safer haven than the US dollar in the present environment.

For producers and developers operating in stable jurisdictions with disciplined cost structures, the $4,000 era creates unprecedented margin expansion and validates multi-year investment theses grounded in operational excellence and balance sheet resilience.

The Enduring Appeal of the Safe Haven Amid Instability

Geopolitical and economic uncertainty has driven gold demand to levels unseen outside of acute crisis periods. Global flashpoints including ongoing conflicts in the Middle East and Ukraine have compounded concerns about supply chain fragility, energy security, and the stability of multilateral institutions. Political turmoil in major economies, including France's snap elections and Japan's ongoing yen interventions, has further fueled safe-haven demand as investors question the durability of policy frameworks in developed markets.

The US government shutdown represents a particularly acute catalyst. The delay in releasing critical economic indicators has forced institutional allocators to operate with incomplete information, creating an information vacuum that amplifies uncertainty premiums across asset classes. Secondary data sources lack the authority and comprehensiveness of official releases, driving investors toward assets that function independently of data dependencies. Gold, which requires no cash flow projections or discount rate assumptions, offers clarity in an environment where traditional valuation frameworks are compromised by data gaps and political noise.

This dynamic has triggered portfolio rotations away from duration-sensitive assets. Treasuries, traditionally viewed as the ultimate safe haven, face growing skepticism as investors question the sustainability of US fiscal policy and the Federal Reserve's ability to maintain independence amid political pressure.

Operational Resilience Against Currency Effects

The weaker dollar amplifies profitability for producers as local currency operating costs decline in real terms, creating natural inflation hedges and margin expansion. Perseus Mining sustains production of approximately 515,000 to 535,000 ounces annually at all-in sustaining costs projected between $1,400 and $1,500 per ounce, maintaining cash operating margins consistently exceeding $500 per ounce. With 93% of planned ounces comprising existing ore reserves, the production outlook is underpinned by high geological confidence.

Jeff Quartermaine, Managing Director and Chief Executive Officer of Perseus Mining, highlighted the operational performance:

"Not only have we enjoyed the continuing elevated gold prices, which is very important, but the business has run extremely well. That combination has meant that our cash margins are up, our earnings are up. We produced just under 500,000 ounces of gold at an all-in sustaining cost of $1,235 per ounce, so our margins are healthy and our cash flows are healthy."

In Brazil's Tapajós province, Serabi Gold operates the high-grade Coringa Project demonstrating compelling economics, projecting a low LOM AISC of $1,241/oz. The Palito Complex holds 531,000 ounces measured and indicated, with ore sorter technology maximizing value by minimizing waste. The Phase 1 growth plan targets approximately 60,000 ounces per annum by 2026 largely self-funded from operational cash flow.

Mike Hodgson, Chief Executive Officer of Serabi Gold, emphasized the currency tailwind:

"We've got this great economic tailwind, not just gold price, but gold price plus Brazilian exchange rate to the dollar."

The Fed, The Dollar & The Debasement Trade

Gold's ascent is closely tied to expectations of further Federal Reserve interest rate cuts. The market has priced two additional rate reductions for 2025, driven by the Fed's easing bias and concerns about economic deceleration. Lower rates decrease the opportunity cost of holding non-yielding assets like gold, particularly as real yields have fallen sharply. The dollar index has declined 10% year-to-date, marking its steepest fall since the 1970s and making gold cheaper for international buyers.

This environment has re-energized the debasement trade narrative. Investors increasingly view gold as a policy hedge against debt monetization, fiscal dominance, and threats to Federal Reserve independence. Concerns over ballooning federal debt and the sustainability of current fiscal trajectories have driven a fundamental reassessment of the US dollar's role as the primary global reserve currency.

Current hedging levels across the industry average approximately 20% of production, suggesting producers are more exposed to spot upside than during the 2011 cycle but also positioned to capture margin expansion as prices continue their structural ascent.

Producers and Developers Benefiting from Lower Discount Rates

Falling interest rates expand project net present values and ease financing conditions for advanced developers. Integra Resources holds a peer-leading resource inventory totaling 7.0 million ounces gold equivalent measured and indicated across three projects in the US Great Basin. The DeLamar Project demonstrates life-of-mine all-in sustaining costs of $814 per ounce with a rapid two-year payback at $1,700 gold. Cash flow from the producing Florida Canyon Mine, expected to generate 70,000 to 75,000 ounces annually, funds the development pipeline without external financing.

George Salamis, President and Chief Executive Officer of Integra Resources, explained the reserve leverage:

"The last reserve estimate was done at $1,750. We're obviously not at $1,750 gold anymore. If you look at higher gold prices, you're going to naturally increase reserves. There's stockpiled material which didn't work at gold prices when they were $1,600, works very well now."

U.S. Gold Corp's CK Gold Project in Wyoming holds 1.672 million ounces of gold equivalent mineral reserves, projected to produce over 110,000 ounces annually. The February 2025 study projects an after-tax net present value of $356 million at $2,100 gold and all-in sustaining costs of $937 per ounce gold equivalent. With development and operating permits already approved and simple flotation metallurgy, the asset is positioned to capture improved financing terms.

Institutional Momentum: Central Bank Diversification & Sticky ETF Flows

Central banks have purchased more than 1,000 tonnes of gold annually since 2022, led by China, Turkey, and emerging market institutions seeking to diversify reserves away from US Treasurys. This represents a durable structural shift in reserve management strategies, driven by geopolitical realignment and sanctions risk. Unlike speculative flows that reverse during risk-on periods, central bank buying is persistent and largely price-insensitive, establishing a structural floor for gold prices.

Western exchange-traded fund inflows totaling $64 billion year-to-date, with $17.3 billion in September alone, represent a fundamental repricing of gold's role within institutional portfolios. Pension funds, sovereign wealth allocators, and registered investment advisors are driving demand rather than retail momentum traders. Goldman Sachs and other strategists have incorporated these flows into pricing frameworks as structural demand anchors, lifting forecasts to $4,900 per ounce by the end of 2026.

Producers Capturing the Institutional Bid

Persistent institutional inflows are translating into premium valuations for efficient producers with transparent cost structures and jurisdictional security. West Red Lake Gold Mines operates a high-grade restart at the Madsen Mine in Ontario's Red Lake region, featuring a diluted head grade of 8.2 grams per tonne gold with probable reserves of 478,000 ounces. The pre-feasibility study demonstrates a net present value of $496 million and annual free cash flow of C$94 million at restart all-in sustaining costs of US$1,681 per ounce. The asset benefits from existing infrastructure requiring minimal development capital, positioning it as a rare new producer ramping in the second half of 2025.

Gwen Preston, Vice President of Communications of West Red Lake Gold Mines, outlined the strategic positioning:

"The companies that are offering up or generating new gold production outperform the rest of the gold equities in gold bull markets."

In Nevada, i-80 Gold commands the fourth largest mineral resource position with 6.5 million ounces measured and indicated plus 7.5 million ounces inferred. The company targets annual production exceeding 600,000 ounces by the early 2030s through a hub-and-spoke model centered on the Lone Tree Autoclave, which will achieve 92% gold recovery. Planned operations feature all-in sustaining costs of $1,303 per ounce for Cove Underground and $1,225 per ounce for Granite Creek.

Capital Returns: High-Grade, Low-Capex Opportunities

Capital is re-entering exploration after prolonged underinvestment, targeting high-grade mineralization, jurisdictional security, and near-term scalability. Investors are prioritizing grade over scale, recognizing that higher-grade deposits offer superior unit economics and shorter payback periods.

New Found Gold continues delineating high-grade zones at its Queensway Project with its preliminary economic assessment demonstrating economics with phased production ramping from approximately 69,300 ounces per year in years one through four to approximately 172,200 ounces per year in years five through nine, supported by over 15 years of mine life totaling 1.5 million ounces. The company's transition from exploration to development is underscored by recent board and management appointments that signal operational intent. Former Newfoundland Premier Dr. Andrew Furey recently joined the board, signaling commitment to advancing the asset.

In Brazil's Tapajós Region, Cabral Gold advances an attractive gold-in-oxide starter project at Cuiú Cuiú. allowstudy released July 29, 2025, confirms robust economics for heap leach processing of oxide material, projecting an after-tax internal rate of return of 78% and net present value of $74 million at $2,500/oz. Phase 1 targets 113,155 ounces over a 6.2-year mine life, including 25,000 ounces per year during the initial two years at cash costs of $950 per ounce. Initial capital expenditure of $37.7 million yields a net present value to capital expenditure ratio of 2.0 with a 10-month payback period. Cabral Gold’s dual-path licensing strategy positions the company for near-term oxide production with minimal capital intensity.

Ruari McKnight, Country Manager of Cabral Gold, explained the licensing approach:

"We have two published licenses which allows you to start the implementation and production on a smaller scale with limitations as to your production profile which then facilitates, in parallel you do your full mining license applications."

Identifying Risks & Technical Indicators

Despite the structural uptrend, volatility remains elevated. Goldman Sachs confirms its $4,900 forecast by end-2026, with risks skewed to the upside. Technical support sits at the 20-day moving average around $3,715 per ounce and the 50-day moving average around $3,515. A swift shutdown resolution or unexpected inflation resurgence could trigger corrections. Exchange-traded fund flows remain critical; material outflows could pressure prices despite institutional composition suggesting greater stability than previous cycles.

The Investment Thesis for Gold Miners

- Macro Alignment: Central bank purchases exceeding 1,000 tonnes annually and exchange-traded fund inflows totaling $64 billion year-to-date provide a robust demand floor above $3,800 per ounce, reducing downside risk regardless of short-term volatility.

- Policy Hedge: Gold equities offer leveraged exposure to the policy uncertainty and debasement trade, providing portfolio protection against fiscal drift, currency erosion, and central bank credibility loss.

- Operational Leverage: Low all-in sustaining cost producers including Perseus Mining at $1,400 to $1,500 per ounce, Serabi Gold at $1,241 per ounce, and Integra Resources at $814 per ounce (LOM) deliver superior margin expansion as spot prices rise.

- Jurisdictional Premium: Tier-1 mining jurisdictions including the United States, Canada, and stable West African locales draw institutional capital seeking transparent permitting regimes and minimal sovereign risk.

- Valuation Rerating: Continued macroeconomic uncertainty and rising price forecasts to $4,900 by 2026 suggest potential for valuation rerating across producers with strong enterprise value per ounce ratios and advanced permitting status.

- Exploration Torque: High-grade developers including New Found Gold and Cabral Gold provide asymmetric upside with limited capital expenditure requirements, offering leveraged exposure to resource expansion in favorable jurisdictions.

- Consolidation Catalyst: Sustained prices above $4,000 per ounce are likely to reignite merger and acquisition activity among mid-tier producers seeking reserve replacement, creating premium valuations for strategic assets with jurisdictional security and near-term production profiles.

The $4,000 Era Redefines Risk & Reward

The $4,000 gold era signals a structural repricing of trust across global capital markets. Investors are not chasing momentum but seeking refuge from policy fragility, fiscal drift, and currency erosion. The US government shutdown, persistent geopolitical tensions, and the Federal Reserve's dovish pivot have converged to create an environment where gold's role shifts from alternative asset to core portfolio ballast.

For producers and developers, the reward lies in disciplined growth, jurisdictional quality, and balance sheet resilience that converts elevated spot prices into sustainable free cash flow. For investors, the mandate is clear: own the operators that convert macro fear into tangible cash flow, prioritize jurisdictions with transparent permitting and rule of law, and favor cost structures that deliver margin expansion without proportional capital intensity increases. The $4,000 threshold is not a peak but a foundation for a multi-year repricing of gold's role within institutional portfolios and a validation of the strategic importance of physical assets in an era of policy uncertainty and monetary accommodation.

TL;DR

Gold's historic breach of $4,000 per ounce represents a structural repricing of trust as U.S. policy paralysis, Federal Reserve rate cuts, and the dollar's steepest decline since the 1970s drive the strongest safe-haven rotation in a decade. Central banks have purchased over 1,000 tonnes annually since 2022 while exchange-traded funds absorbed $64 billion year-to-date, including $17.3 billion in September alone, establishing a structural floor above $3,800. Goldman Sachs forecasts $4,900 by end-2026 with upside risk. Low-cost producers across Tier-1 jurisdictions—including Perseus Mining at $1,235 per ounce all-in sustaining costs, Serabi Gold at $1,241, and developers like Integra Resources at $814 (LOM)—capture exceptional margin expansion while developers including New Found Gold Cabral Gold and U.S. Gold Corp offer asymmetric upside through high-grade, low-capex opportunities.

FAQs (AI-Generated)

Gold broke $4,000 due to a confluence of factors including U.S. government shutdown paralysis, Federal Reserve rate cuts eroding real yields, the dollar's 15% year-to-date decline, and persistent central bank buying exceeding 1,000 tonnes annually. Record exchange-traded fund inflows of $64 billion year-to-date reflect institutional reallocation away from Treasurys and equities toward safe-haven assets.

The debasement trade refers to investors buying gold as a hedge against waning faith in the U.S. dollar and Treasurys, driven by concerns over ballooning federal debt, threats to Federal Reserve independence, and debt monetization. This narrative, reminiscent of the 1970s when gold soared amid instability, positions gold as a policy hedge against fiscal dominance and currency erosion.

Low all-in sustaining cost producers capture the greatest margin expansion, including Perseus Mining ($1,235-$1,400 per ounce), Serabi Gold ($1,241 per ounce), Integra Resources ($814 per ounce at DeLamar). Companies in Tier-1 jurisdictions with transparent permitting— West Red Lake Gold Mines, i-80 Gold—attract institutional capital, while high-grade developers New Found Gold, Cabral Gold and U.S. Gold Corp offer asymmetric upside.

Technical support sits at the 20-day moving average around $3,715 per ounce and the 50-day moving average around $3,515. Downside risks include swift U.S. shutdown resolution restoring fiscal confidence, unexpected inflation resurgence forcing Fed hawkishness, or material exchange-traded fund outflows triggering corrections. However, Goldman Sachs characterizes risks as skewed to the upside given structural demand.

Goldman Sachs forecasts gold reaching $4,900 per ounce by the end of 2026, driven by sticky institutional demand from central bank purchases and exchange-traded fund inflows incorporated into pricing frameworks as structural anchors. The forecast assumes continued policy uncertainty, Fed easing, dollar weakness, and persistent safe-haven flows, with risks characterized as skewed to the upside rather than downside.

Analyst's Notes

Subscribe to Our Channel

Stay Informed