Higher Real Yields Limit Gold Gains, Favoring Low-Cost Producers as Gold Trades 26% Below Peak

Higher real yields cap gold prices despite strong central bank demand, making low-cost, cash-generating gold producers better positioned in a rangebound market.

- Gold trades near $4,150 per ounce, about 26% below its January 2026 peak of roughly $5,597, even as renewed conflict between the US and Iran pushes oil prices higher.

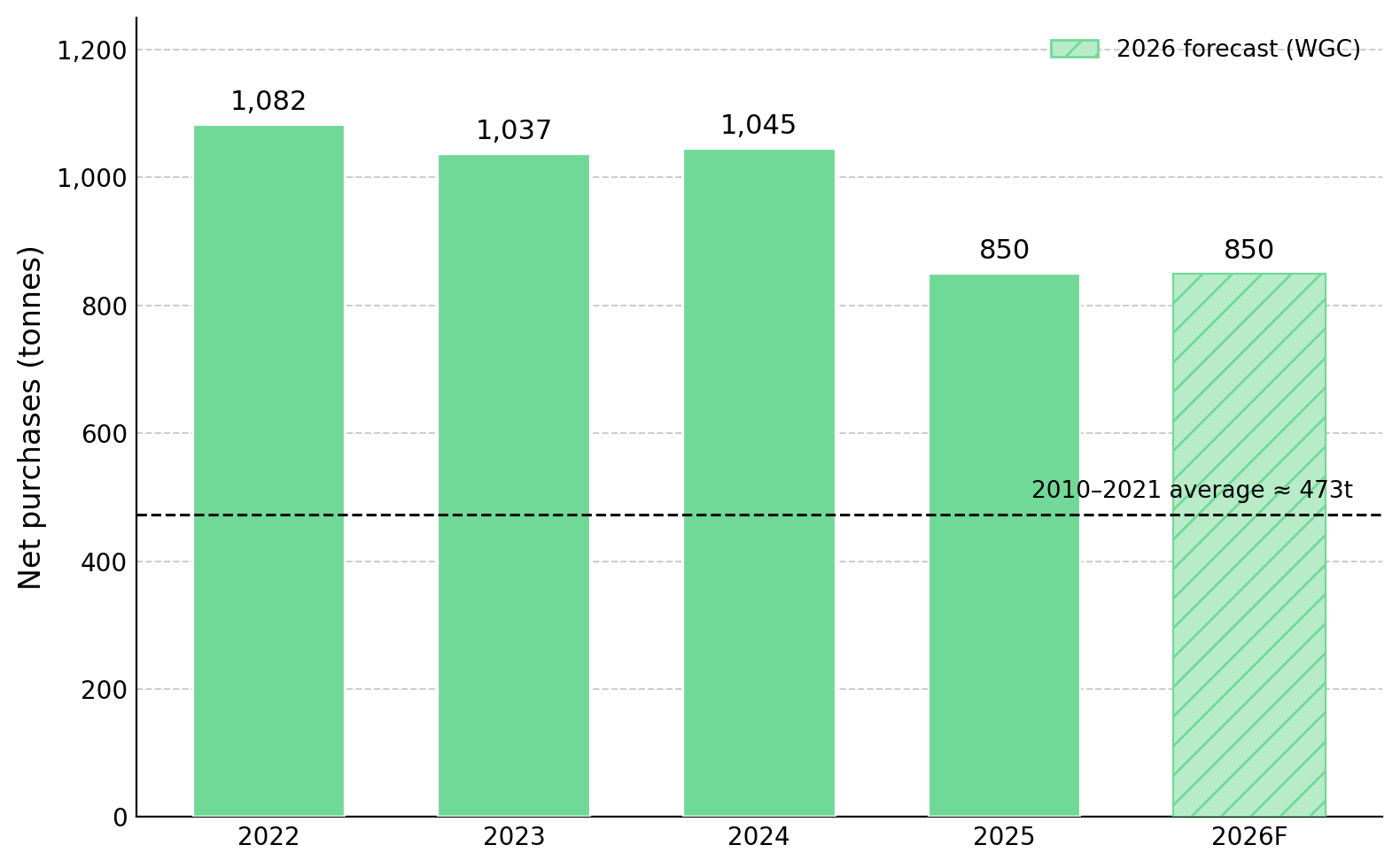

- The World Gold Council estimates central banks bought about 244 tonnes in the first quarter of 2026, while the European Central Bank reports that gold has overtaken US Treasuries as a share of official reserves, accounting for roughly 27% versus 22%.

- Higher real yields limit gold price upside, while central-bank buying supports demand, making cost discipline more important than metal-price leverage in gold equities.

- Higher real yields limit gold price upside, while central-bank buying supports demand, shifting the focus in gold equities from gold-price leverage to cost discipline.

- Gold equities carry gold-price, execution, permitting, and dilution risk, and capital is at risk of permanent loss.

Higher Real Yields Limit Gold Price Gains Despite Geopolitical Risk

Gold sits about 26% below its January 2026 record of roughly $5,597 per ounce, having recorded its worst quarter in thirteen years, and it has stayed capped even as fresh strikes between the United States and Iran push oil higher again. The reason is not that the safe-haven bid has disappeared. It is that the same shock is driving inflation higher, reinforcing expectations for tighter Fed policy and higher real yields.

Renewed risk around the Strait of Hormuz has pushed Brent crude back toward the high $70s per barrel, renewing upward pressure on inflation. US consumer price inflation reached 3.8% in April, its highest reading since May 2023, kept the Fed's policy rate at 3.50% to 3.75% with a hawkish bias. Its June projections showed nine of eighteen officials projecting at least one additional rate hike in 2026 while raising the core inflation forecast to 3.3%. Ten-year Treasury yields near 4.58% reflect that stance. Higher real yields, or bond yields after inflation, increase the opportunity cost of holding non-yielding gold.

Gold pays no coupon or dividend, so its relative appeal depends on the real return available on cash and bonds. An inflationary conflict can therefore pressure gold rather than lift it because it encourages the Fed to keep interest rates higher for longer. Gold still hedges geopolitical risk, but in this cycle higher real yields have outweighed safe-haven demand.

Real Yields Cap Gold Prices While Physical Demand Stays Strong

Futures markets and real yields explain only part of the gold market. Central-bank buying continues to support physical demand despite short-term price swings, making that demand an important driver of gold-equity valuations. Central-bank purchases provide the clearest evidence of sustained physical demand. The World Gold Council estimates net official-sector purchases of about 244 tonnes in the first quarter of 2026, above the five-year average, and forecasts roughly 850 tonnes for the full year. Officially reported purchases were lower, but the Council's estimate includes over-the-counter and refinery flows that are reported with a lag.

The European Central Bank reports that gold has surpassed US Treasuries as a share of global official reserves, accounting for roughly 27% versus 22%. In the Council's annual survey, 89% of reserve managers expect global gold holdings to rise over the next year, while a record 45% plan to increase their own holdings. This policy-driven reserve diversification continues whether gold trades at $4,000 or $5,000.

Industrial demand provides a second source of support for gold prices. Technology and industrial applications consumed roughly 82 tonnes in the first quarter, with electronics demand rising 3% year over year to about 69 tonnes. Artificial-intelligence servers, high-reliability chips, and automotive power modules are increasing gold demand for conductivity and heat dissipation, while consumer electronics manufacturers continue reducing gold use to offset higher prices. The World Bank projects its precious-metals price index will rise 42% in 2026, supported by continued official-sector and industrial demand.

Rangebound Gold Prices Shift the Focus to Producer Margins

With higher real yields limiting gold prices and central-bank buying supporting demand, the focus shifts to gold equities. In a rangebound gold-price environment with higher costs for fuel, explosives, labor, and royalties, free cash flow depends on the margin between the gold price and all-in sustaining cost (AISC), the fully loaded cost of producing and sustaining an ounce. Gold price direction matters less than that margin.

Integra Resources raised its 2026 AISC guidance to $3,300-$3,500 per ounce, above the life-of-mine average of about $2,331, as waste stripping and input-cost inflation increased operating costs. The company's strategy is to reduce costs and fund growth at DeLamar and Nevada North from operating cash flow rather than compete as a low-cost producer.

George Salamis, Chief Executive Officer of Integra Resources, says input-cost inflation is increasing operating costs across the gold mining industry:

"It's affecting us right now, like every other gold producer out there. Fuel prices are high, explosive prices are high, and that's being reflected in our all-in sustaining costs right now."

Operating Cash Flow Reduces Dilution Risk for Gold Producers

When higher gold prices cannot be relied upon to strengthen a stretched balance sheet, the ability to fund growth without issuing new shares becomes a key differentiator. Dilution reduces existing shareholders' ownership and future cash flow per share, making internally funded growth more valuable when gold prices remain rangebound.

Operating Cash Flow Funds Growth Without Equity Dilution

Serabi Gold’s Palito and Coringa operations in Brazil produced a record 44,169 ounces in 2025, up from about 38,000 the prior year, at an AISC of $1,816 per ounce, generating roughly $79 million of EBITDA and leaving the company debt-free with about $64 million in cash and an inaugural dividend set at 20% of cash flow. Growth is being driven by grade rather than throughput, with Palito feed rising from 4.86 to 6.04 grams per tonne of gold, and the consolidated resource has grown from 1.0 to 1.4 million ounces. Crucially, Coringa ore is being routed through existing Palito infrastructure via a fourth ball mill due in late 2026 rather than a costly standalone plant, though the expansion remains gated on federal permitting from Brazil's indigenous affairs and land agencies.

Operating Margins Increase Flexibility During Mine Ramp-Up

West Red Lake Gold Mines shows how wider operating margins provide greater flexibility during a production ramp-up. Its Madsen mine in Ontario entered commercial production at the start of 2026 and is ramping toward its 800-tonne-per-day design rate. Rowan's indicated resource increased about 70% to roughly 334,000 ounces at 13 grams per tonne, strengthening the project's high-grade production profile. A combined Madsen and Rowan pre-feasibility study is due in the third quarter of 2026 and supports a hub-and-spoke development plan targeting more than 150,000 ounces of annual production.

Shane Williams, Chief Executive Officer of West Red Lake Gold Mines, says today's higher gold prices provide a wider operating margin than was available to the mine's previous operator:

"The previous operator, Pure Gold, had to have an average gold production rate of around 4,000 ounces to break even. We have the luxury of the gold price being double what it was at this stage. That gives you a lot of leeway."

Permitting & Processing Drive Gold Project Economics

Mining costs extend beyond diesel and labor. Permitting timelines and ore metallurgy influence project economics alongside operating costs. In a rangebound gold market, multi-year permitting delays or lower metallurgical recoveries are harder to offset through higher gold prices. Jurisdiction therefore becomes a measurable driver of project value and development risk.

i-80 Gold combines a favorable jurisdiction with technically complex ore. All of its assets are in Nevada, ranked the most attractive mining jurisdiction in the Fraser Institute's 2025 survey. The company currently processes Nevada ore through a third-party autoclave while refurbishing its own Lone Tree facility, a roughly $430 million project targeting first gold production by the end of 2027. Much of Nevada's gold is refractory, meaning it is locked within sulfide minerals and requires pressure oxidation before recovery. Owning its own autoclave should increase gold recoveries and reduce reliance on lower-margin third-party toll processing. The larger open-pit projects still require Environmental Impact Statement (EIS) approvals, which typically take three to four years.

Paul Chawrun, Chief Operating Officer of i-80 Gold, explains why so much Nevada gold carries a processing penalty that shapes the region's cost of supply:

"The reason why you need an autoclave, and it's very common in Nevada, is the gold is occluded in a pyrite or an arsenopyrite… Fundamentally you need pressure oxidation leach to remove that part of the mineral away and have the gold free, and then it's a standard carbon-in-leach process afterwards."

Fed Policy & Real Yields Will Drive Gold Prices

In the near term, gold prices will depend more on real yields than on geopolitical developments alone. The outlook depends less on developments in the Strait of Hormuz than on whether the conflict keeps inflation high enough for the Fed to maintain restrictive monetary policy.

Gold's near-term outlook depends on inflation, Fed policy, and oil prices. A stronger-than-expected consumer price index reading, hawkish Fed meeting minutes, and sustained strength in oil prices would increase the likelihood of a September rate hike, which futures markets currently price at roughly 50% to 55%. That combination would keep real yields elevated and limit gold price upside. A softer inflation reading or a more dovish Fed signal would lower real yields and could support a move back toward the $4,300 to $4,500 range.

Central-bank buying continues to support gold demand while higher real yields limit price gains. Together, these forces are likely to keep gold prices within a narrower trading range. That environment favors producers with wide margins between the gold price and AISC, while higher-cost operators remain more dependent on rising gold prices.

The Investment Thesis for Gold

- Central-bank reserve diversification and de-dollarization continue to support gold demand even when private investment demand weakens.

- Producers with wider margins between the gold price and all-in sustaining cost are better positioned than those that depend on higher gold prices to generate returns.

- Balance sheets that support growth funded by operating cash flow, reducing reliance on dilutive equity issuance in a rangebound gold market.

- Jurisdictions with predictable permitting and established infrastructure that reduce development timelines and execution risk.

- Cost structures and processing infrastructure that limit margin pressure from higher fuel, explosives, and labor costs.

- Development pipelines aligned with continued official-sector gold demand above historical averages.

- A decisive Fed pivot to rate cuts would lower real yields, support higher gold prices, and favor producers with greater gold-price leverage over those that rely on cost discipline, changing the investment thesis outlined here.

The defining feature of the gold market in mid-2026 is not the conflict itself or the record price reached earlier in the year. Continued central-bank buying supports gold demand, while higher real yields limit price gains. In that environment, the focus shifts from gold prices to producers with low costs, self-funded growth, and predictable permitting. The companies discussed here illustrate those characteristics rather than represent investment recommendations, and capital remains at risk of permanent loss. The direction of real yields, more than any single geopolitical development, will determine gold's near-term price direction.

TL;DR

Higher real yields have become the dominant force limiting gold price gains, outweighing the traditional safe haven effect of geopolitical tensions. At the same time, sustained central bank buying continues to support physical gold demand, creating a rangebound market rather than a structural decline. In this environment, gold equities are increasingly differentiated by operating margins instead of metal price leverage. Producers with low all-in sustaining costs, self-funded growth, predictable permitting, and efficient processing infrastructure are better positioned to generate returns, while higher-cost operators remain more exposed to inflation, dilution, and execution risks if gold prices fail to move higher.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed