Inflation Volatility & Portfolio Correlation Shifts: Why Rising Vol Has Not Eroded Gold's Strategic Role

Rising gold volatility hasn't eroded its strategic role. In inflation-dominant regimes, gold reduces portfolio risk disproportionately through correlation control.

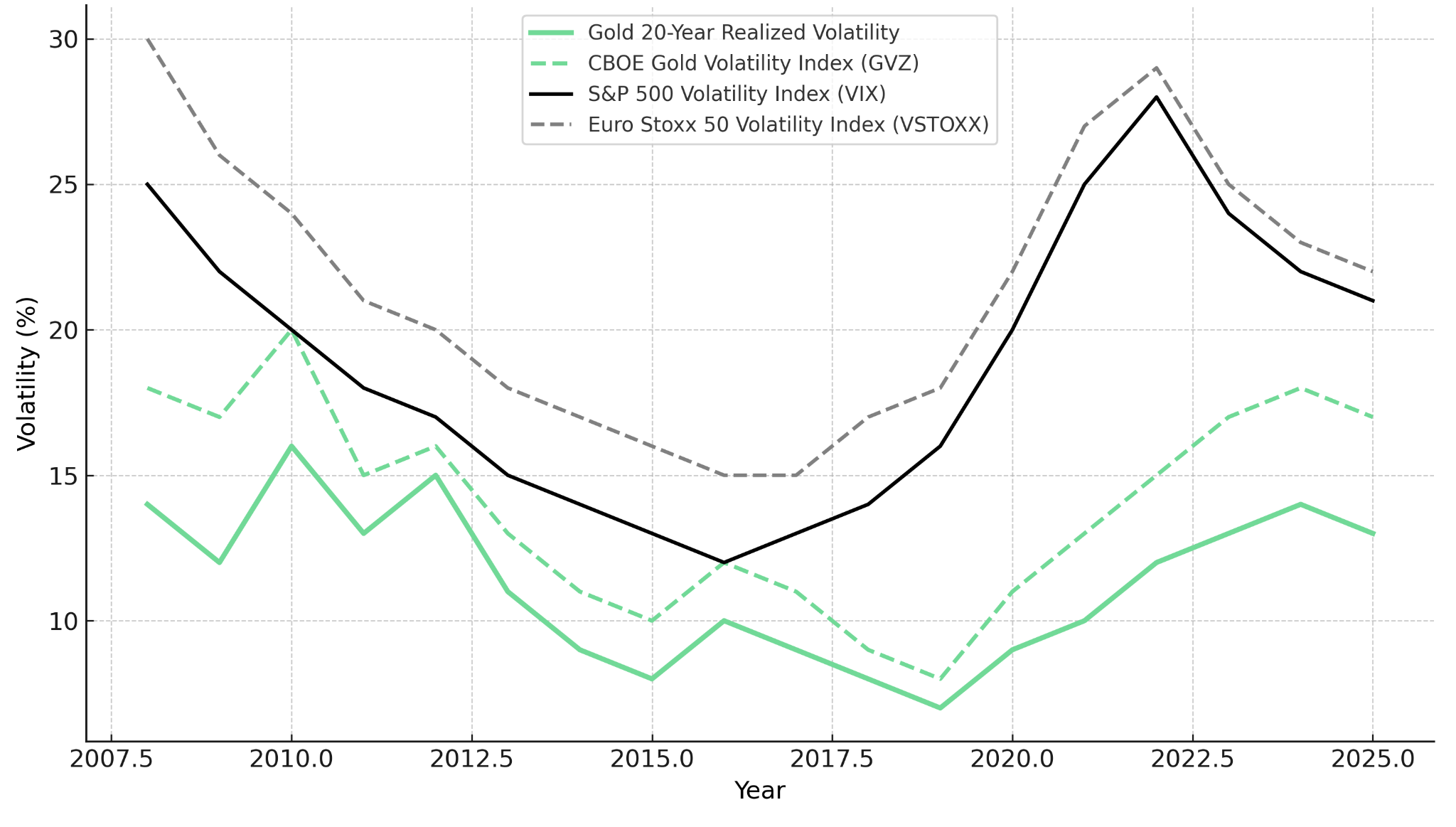

- Rising gold volatility in 2025 has occurred from a historically low base and remains broadly aligned with long-term averages rather than signaling structural instability.

- Inflation volatility, not growth risk, has become the dominant macro variable, driving positive bond-equity correlations and weakening traditional diversification.

- In inflation-dominant regimes, gold's value lies less in price momentum and more in correlation control and portfolio risk reduction.

- Empirical portfolio analysis shows that a 5% gold allocation reduces total portfolio volatility by approximately 5%, while contributing less than 2% to overall risk.

- Mining equities with cost discipline, jurisdictional security, and near-term cash-flow visibility remain leveraged beneficiaries of gold's orderly price strength.

Gold Volatility in Context: Separating Perception from Statistical Reality

Gold's volatility has risen during 2025, prompting questions about whether its appeal as a defensive asset is fading. The critical distinction for investors is whether this volatility represents regime change or normalization from an unusually compressed base. Data from the World Gold Council indicates that gold's realized volatility, while elevated relative to the past two years, remains consistent with its 20-year average range. The recent increase reflects a return to historical norms rather than a departure from them.

Despite heightened geopolitical uncertainty, tariff-driven trade fragmentation, and monetary policy divergence across major economies, gold volatility remains materially below that of US and European equities. The CBOE Gold Volatility Index has not approached the levels observed during genuine stress episodes such as March 2020 or the 2008 financial crisis. Unlike previous high-performance periods characterized by sharp, speculative price spikes, the 2024-2025 appreciation has occurred in a measured, orderly fashion. This pattern suggests institutional accumulation and central bank purchasing rather than retail-driven excess.

For portfolio construction purposes, this distinction is consequential. Volatility alone does not negate diversification value. Correlation behavior, not absolute price movement, determines risk outcomes in multi-asset frameworks. Gold's recent price performance, achieved without the volatility signature of speculative episodes, reinforces rather than undermines its role as a portfolio stabilizer.

The Inflation-Dominant Regime & the Breakdown of Traditional Diversification

Markets are currently operating in what quantitative strategists characterize as a low growth-volatility, high inflation-volatility environment. This regime configuration has historically proven challenging for balanced portfolios that rely on negative bond-equity correlations for risk management. When inflation becomes the dominant source of uncertainty, both asset classes tend to move in the same direction, eroding the defensive function of fixed income.

The mechanism is straightforward. Inflation shocks compress equity multiples through higher discount rates while simultaneously reducing bond prices through rising yields. The result is positive bond-equity correlation, a condition that amplifies portfolio volatility precisely when investors expect protection. Research from the International Monetary Fund and major asset managers confirms that this correlation structure has persisted through 2024 and into 2025, representing a meaningful shift from the post-2008 regime where bonds reliably offset equity drawdowns.

Within this macro framework, gold's low correlation to both equities and fixed income regains strategic importance. Gold is not competing with equities for growth capital. It is competing with bonds as a risk-management asset in portfolios where fixed income has lost its hedging function. This reframing explains the renewed institutional interest in gold allocations despite already elevated price levels.

Producers with demonstrated cost discipline provide concrete evidence of margin protection in inflationary environments. Craig Jones, Managing Director and Chief Executive Officer of Perseus Mining, describes the company's financial positioning as of June 2025:

"Ending up with net cash and bullion of $827 million. We can pay for all of our aspirations within our current cash flows."

The practical consequence for portfolio managers is significant. Traditional 60/40 portfolios that delivered consistent risk-adjusted returns over the past decade face structural headwinds when bonds fail to provide ballast during equity drawdowns. Gold's correlation profile, which has remained stable even as bond-equity correlations have risen, offers a partial solution to this diversification challenge. Mining equities operating within this framework benefit indirectly from gold's portfolio relevance, particularly where operational cost inflation is controlled and margin visibility remains high.

Portfolio Construction Implications: A Structural Rather Than Tactical Allocation

Quantitative portfolio modeling reinforces gold's relevance within modern asset allocation frameworks. A 5% gold allocation reduces overall portfolio volatility by nearly 5%, a disproportionate impact relative to the position size. Gold contributes only approximately 1.9% to total portfolio risk despite meaningfully lowering aggregate volatility. This asymmetry underscores gold's efficiency as a risk dampener rather than a return maximizer.

For institutional investors, this analytical framework shifts gold from a tactical inflation hedge to a structural allocation within diversified portfolios. The implication extends beyond spot price exposure to the equities of gold producers and developers. Valuation frameworks increasingly reflect gold's strategic utility, not merely its commodity price. Assets with clear development timelines, funding visibility, and jurisdictional security are better positioned to attract capital from allocators who view gold exposure as a portfolio construction tool rather than a directional bet.

This structural demand provides support for mining equities even in periods of price consolidation. Companies demonstrating operational execution and financial discipline benefit from capital flows driven by portfolio rebalancing mechanics rather than commodity speculation alone.

Cost Control as Competitive Advantage in an Inflation-Dominant Market

Rising input costs across energy, labor, and reagents remain a primary risk in inflation-heavy environments. Gold miners able to maintain all-in sustaining cost discipline gain disproportionate leverage to price stability. The spread between realized gold prices and AISC determines margin capture, and companies with structural cost advantages preserve profitability across commodity cycles.

Perseus Mining delivered FY25 AISC of US$1,235 per ounce while expanding a multi-mine portfolio across West Africa, preserving margins even amid regional cost inflation. New Found Gold is advancing its Hammerdown project in Newfoundland, which achieved first gold pour in November 2025 and is currently ramping toward commercial production targeted for early 2026. The company's acquisition of Maritime Resources, which closed in December 2025, provides processing infrastructure that supports capital-efficient development.

Keith Boyle, Chief Executive Officer of New Found Gold, describes the company’s production milestone:

"Hammerdown is a mine that poured its first gold in November. We announced the first pour from Hammerdown on November 12th."

Cabral Gold has outlined a starter operation in Brazil with AISC of US$1,210 per ounce according to its updated Pre-Feasibility Study released in July 2025, supported by a fully funded construction plan. The company closed a US$45 million gold loan in November 2025 without shareholder dilution. Alan Carter, President and Chief Executive Officer of Cabral Gold, explains the company’s financing approach:

"We recently raised $45 million US through a gold loan. The project is in construction... There was no equity raise as part of that, which I think surprised a lot of people."

These examples demonstrate that cost visibility, not resource grade alone, is becoming a key valuation differentiator in the current environment.

Jurisdictional Security & Permitting Visibility in a Fragmented Geoeconomic Landscape

Geoeconomic fragmentation has elevated jurisdictional risk from a background consideration to a core investment variable. Investors increasingly favor assets in jurisdictions with transparent permitting regimes, established mining law, and rule-of-law protections for foreign capital. Regulatory predictability reduces discount rates applied to net present value and internal rate of return models, directly influencing project valuations. The scarcity of fully permitted development assets in Tier 1 jurisdictions has created a valuation premium that market participants now explicitly recognize.

George Bee, President and Chief Executive Officer of U.S. Gold Corp, whose CK Gold Project secured its Mine Operating Permit in April 2024 and Air Quality Permit in November 2024, articulates the supply constraint:

"You can count on one hand the number of fully permitted projects in a safe jurisdiction like the United States."

Integra Resources is advancing large-scale projects in Nevada and Idaho, with federal permitting milestones forming near-term catalysts. The company's Florida Canyon operation provides operating cash flow that funds development activities. As of January 2026, Integra reported a cash position of US$81 million. George Salamis, President and Chief Executive Officer, describes Integra Resources’ financial position:

"We have a treasury of $63 million. We're producing, we're making cash flow... If it generated $20 to $30 million a year in free cash flow, now it's doing much more than."

West Red Lake Gold Mines restarted operations at its Madsen Mine in Ontario's Red Lake district in May 2025 at 500 tonnes per day and is currently in ramp-up phase, targeting full-scale production of approximately 50,000 ounces annually from 2026. Gwen Preston, Vice President of Corporate Development, describes the operational trajectory:

"We'll be in full-scale production early in 2026… Madsen mine is up. It's running. It's got its money spent. It's making money. We're inside of commercial production. "

Serabi Gold operates in Brazil's Tapajós region with an established operating history, demonstrating that jurisdictional quality extends beyond traditional Tier 1 geographies when operators maintain consistent regulatory relationships.

Scale, Optionality & Resource Longevity as Strategic Differentiators

In an environment where gold's role is portfolio-driven, asset scale and optionality regain strategic importance. Large, long-life deposits offer flexibility in mine planning, capital sequencing, and market timing. This optionality is particularly valuable when price volatility is orderly rather than speculative, allowing operators to optimize development decisions without distressed timelines.

i-80 Gold holds 100% ownership of the Lone Tree autoclave in Nevada's Carlin Trend, which serves as centralized processing infrastructure for its various Nevada assets. The company is currently toll milling material from its Granite Creek Underground project while advancing autoclave refurbishment studies. Richard Young, President and Chief Executive Officer of i-80 Gold, describes the near-term value crystallization path:

"Between the first quarter of 2026 and the first quarter of 2027, we'll have three feasibility studies out. You'll see us report reserves for the first time for all three operations."

Tudor Gold controls a large-scale resource base at its Treaty Creek project in British Columbia's Golden Triangle. Hycroft Mining holds a significant gold-silver inventory in Nevada totaling 10.6 million ounces of gold and 361 million ounces of silver according to its March 2023 Technical Report, with ongoing metallurgical optimization work targeting improved recoveries.

P2 Gold is advancing the Gabbs gold-copper project in Nevada through a phased development strategy, with a 2025 PEA projecting a 2.4-year payback period at base case metal prices. The company is targeting production by 2028 following permitting milestones and Feasibility Study completion in 2026.

Scale does not eliminate execution risk, but it extends strategic optionality and provides multiple pathways to value creation during periods of macro uncertainty.

The Investment Thesis for Gold

- Inflation volatility and positive bond-equity correlations reinforce gold's role as a structural diversifier rather than a tactical trade.

- Gold reduces total portfolio risk disproportionately relative to its own volatility contribution, offering asymmetric risk-adjusted benefits.

- Producers and developers with controlled all-in sustaining costs benefit most from stable, elevated gold prices through margin expansion.

- Assets in permitting-secure jurisdictions command lower risk discounts in valuation models, improving access to growth capital.

- Large-scale, long-life deposits offer optionality value that markets increasingly recognize during uncertain macro regimes.

- Non-dilutive funding structures and self-sustaining cash flows differentiate operators positioned for value creation without continuous equity issuance.

- Near-term production milestones and feasibility study catalysts provide discrete valuation inflection points independent of commodity price movements.

Volatility Has Clarified Gold's Purpose Rather Than Diminished It

Rising volatility has not diminished gold's relevance within institutional portfolios. Instead, it has reframed and clarified its function. In an inflation-dominant regime where traditional diversification through fixed income has weakened, gold's value lies in correlation control rather than price calm. The metal's ability to reduce portfolio volatility disproportionately relative to its risk contribution makes it a structural allocation rather than a speculative position.

Gold remains a portfolio stabilizer at the asset class level, and mining equities with cost discipline, jurisdictional security, and visible execution pathways remain leveraged beneficiaries of this structural role. The companies positioned to capture this environment share common characteristics: financial flexibility, operational margin protection, and development timelines aligned with sustained institutional demand for gold exposure.

TL;DR

Gold's 2025 volatility increase represents normalization from historically low levels rather than structural instability. In the current inflation-dominant regime, where positive bond-equity correlations have weakened traditional diversification, gold's value lies in correlation control rather than price calm. A 5% gold allocation reduces portfolio volatility by approximately 5% while contributing less than 2% to overall risk—an asymmetric benefit. Mining equities with cost discipline, jurisdictional security, and near-term production visibility remain leveraged beneficiaries. Companies demonstrating AISC control, non-dilutive financing, and permitting clarity in stable jurisdictions are best positioned to capture institutional demand driven by portfolio construction needs rather than commodity speculation.

FAQs (AI-Generated)

Gold's volatility has increased but remains within its 20-year historical average range. The rise reflects normalization from an unusually compressed base rather than structural instability. Unlike speculative episodes, the 2024-2025 price appreciation has occurred in an orderly fashion, suggesting institutional accumulation rather than retail-driven excess.

When inflation becomes the dominant source of uncertainty, both stocks and bonds tend to move in the same direction. Inflation shocks compress equity multiples through higher discount rates while reducing bond prices through rising yields. This positive bond-equity correlation erodes fixed income's defensive function, leaving traditional balanced portfolios exposed.

Quantitative modeling suggests a 5% gold allocation reduces overall portfolio volatility by approximately 5% while contributing less than 2% to total portfolio risk. This asymmetric impact makes gold efficient as a structural risk dampener rather than a return maximizer.

Geoeconomic fragmentation has elevated jurisdictional risk to a core investment variable. Fully permitted projects in Tier 1 jurisdictions with transparent regulatory frameworks command lower discount rates in valuation models, improving access to capital. The scarcity of such assets creates explicit valuation premiums.

Companies with controlled all-in sustaining costs preserve margins regardless of input cost inflation. Key differentiators include cost discipline, non-dilutive financing structures, self-sustaining cash flows, and clear development timelines aligned with institutional demand for gold exposure.

Analyst's Notes

Subscribe to Our Channel

Stay Informed