Inventus Mining Charts Self-Funding Path to Production as Bulk Sample Economics Prove Out

Inventus Mining self-funds Ontario gold project via bulk sampling, targets Q3 '26 resource & '27 production. Backed by Sprott/McEwen. Shares +145% to $0.27.

While most junior gold explorers navigate a familiar cycle of drilling, dilution, and capital raises, Inventus Mining has spent the past year demonstrating a fundamentally different approach, one that generates cash from its Ontario paleoplacer deposit before defining a formal resource estimate.

The Toronto-based company, which saw its share price more than double over the past 12 months to $0.27, is now positioning for a critical 12-month stretch that could transform it from bulk-sampling explorer to near-term producer. With a maiden resource estimate targeted for Q3 2026 and a production permit application slated in 12 - 18 months, CEO Wesley Whymark is executing a strategy that has attracted backing from some of the mining sector's most discerning investors including Eric Sprott and the founder of McEwen Mining.

The Economics of Extraction Before Definition

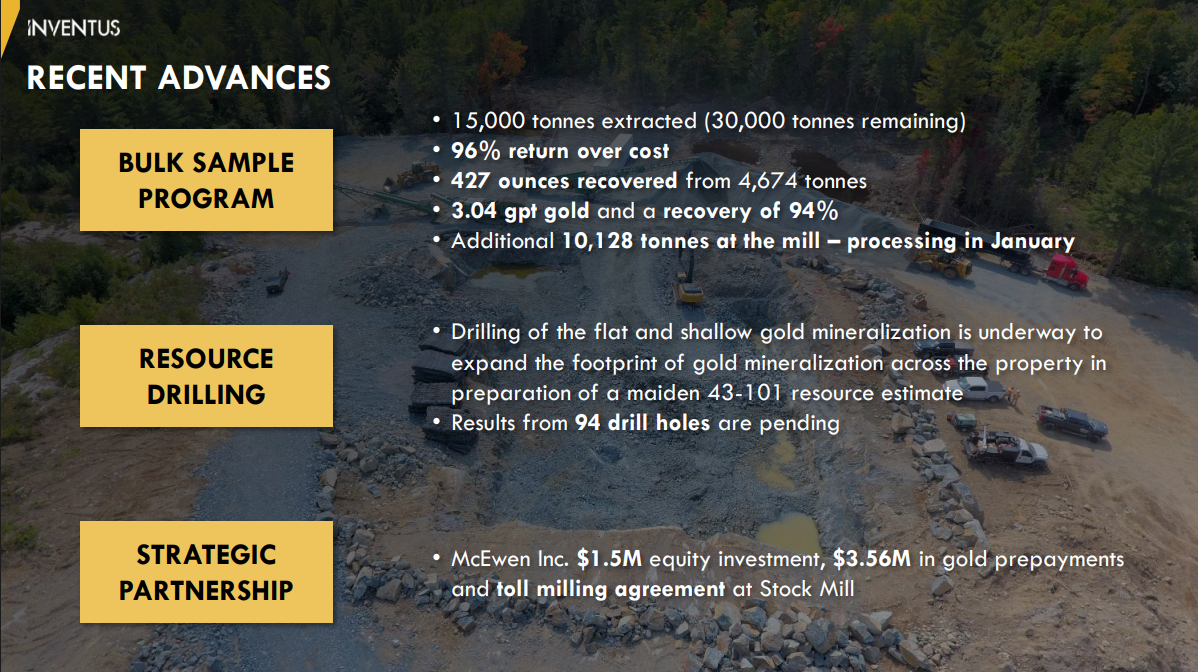

At the heart of Inventus's model is a 50,000-tonne bulk sample permit at the Pardo Paleoplacer project, roughly 30,000 tonnes of which has now been extracted and processed. Rather than stockpiling material or conducting small-scale metallurgical tests, the company pre-sells extracted gold to McEwen Mining's nearby mill under an arrangement that covers extraction costs and funds ongoing technical work.

"We were showing we essentially doubled our money on the first bulk sample, put in a dollar, and got two dollars back. If we can keep doing that, it'll be great."

The economics work because of the deposit's unusual geometry. The primary gold-bearing conglomerate reef sits at or near surface in a flat-lying orientation, allowing the company to blast off overburden, extract mineralised material, crush it on-site, and truck it to processing all without the capital intensity of underground ramps or deep drilling campaigns. With grades consistently running between 2.5 and 3.5 grams per tonne across a roughly two-metre-thick unit, Whymark's team can complete two to three drill holes per day using a single rig, dramatically reducing per-metre exploration costs.

The metallurgy, described by Whymark as "largely de-risked," plays to the deposit type. Free gold particles in sedimentary host rock respond well to gravity separation and carbon-in-leach processing, with approximately 70% of gold recovery captured in the gravity concentrate alone and overall mill recoveries in the mid-90% range at McEwen's facility.

From Bulk Sample to Formal Resource

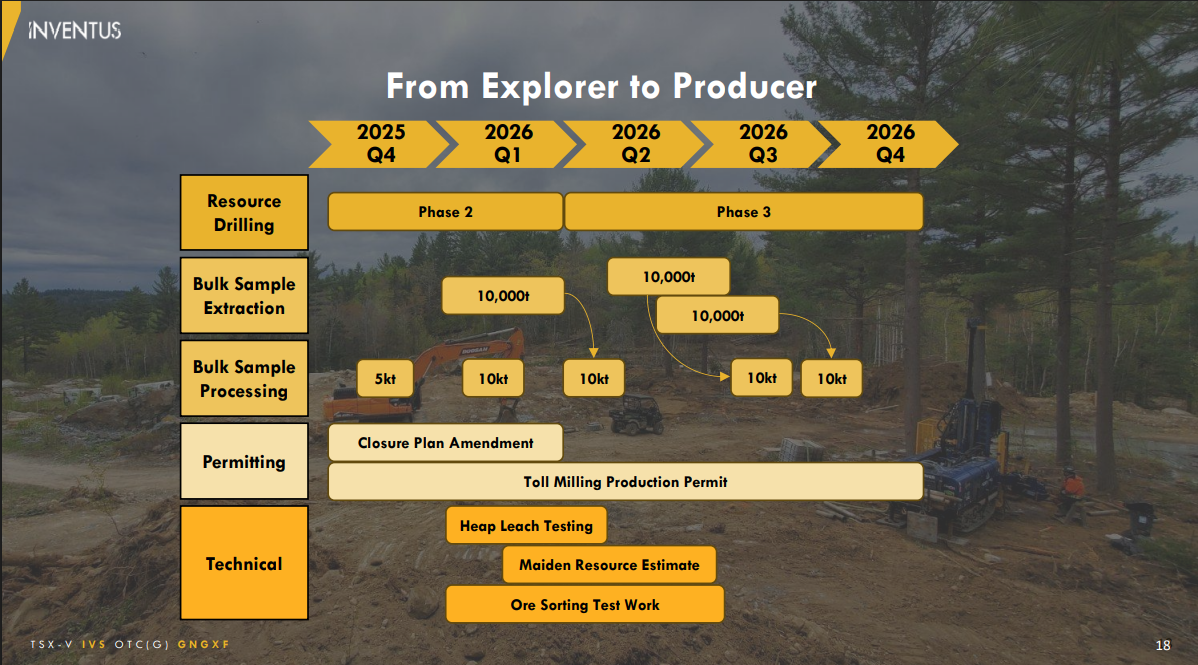

With 20,000 tonnes of permitted bulk sample capacity remaining, Inventus is now prioritising grid drilling to support the Q3 resource estimate. That milestone will form the technical foundation for a subsequent off-site processing production permit targeting approximately 200,000 tonnes of material.

Ontario's permitting framework offers a potential advantage. According to Whymark, once a third-party environmental report is completed, a process he estimates at three to four months, the Ministry can return an approval decision within 45 days of receiving a complete submission. The company already has a blueprint for closure planning from its existing bulk sample program, which should streamline the larger permit application.

If the timeline holds, permit submission would occur in late 2026 / early 2027, positioning the company for potential production commencement shortly thereafter, subject to seasonal considerations in Ontario's winter operating environment. At a processing rate of approximately 10,000 tonnes per month, the 200,000-tonne permitted volume would represent roughly 20 months of operation at current throughput rates.

Ore Sorting: A Potential Margin Multiplier

Beyond the base case of truck-and-mill economics, Inventus is advancing work on XRF particle sorting technology that could materially change project economics. A 2018 scoping study demonstrated that ore sorting could concentrate 93% of the gold into just 40% of total material, effectively eliminating 60% of mined tonnes before trucking and processing.

"If you can take the material and reduce it to only 40% of the volume, you're hauling something at a much higher grade and much less tonnage, cheaper trucking costs, less milling costs."

The company noted that XRF sorter technology has advanced significantly since the initial 2018 testing, with modern units now capable of processing between 40 and 120 tonnes per hour compared to slower first-generation machines. Capital cost for a sorting unit is estimated at roughly $1 million to $1.5 million a manageable outlay relative to potential operating savings. Bulk-scale testing is planned to confirm commercial viability before any equipment commitment.

Successful ore sorting could also unlock economic value in two additional conglomerate units that sit above and below the primary target zone. These lower-grade layers have received less attention to date but could become relevant if sorting can cost-effectively upgrade material or if heap leaching proves viable for lower-grade concentrate streams.

Strategic Validation and Commercial Alignment

The shareholder register provides a form of external validation that most junior explorers lack. Eric Sprott's 16% position and the personal 17% stake held by McEwen Mining's founder signal recognition of both the geological setting and the execution model. McEwen Inc. holds an additional 10%, bringing the combined strategic and institutional ownership to approximately 43% of outstanding shares.

The McEwen relationship extends beyond shareholding. The company's mill provides the processing capacity that makes Inventus's self-funding model viable, creating a commercial partnership with aligned incentives. While Whymark acknowledged that processing pace has been slower than initially anticipated driven by McEwen's own production requirements the arrangement has nonetheless allowed Inventus to advance the project with minimal shareholder dilution.

"We're kind of a unicorn in space in the sense that not many groups can go and extract gold without a lot of capital, we can do it with no capital."

That said, the CEO indicated a modest capital raise may be considered to accelerate ore sorting studies and drilling activity, though the core message remains that Inventus aims to be substantially less dilutive than typical drill-and-raise junior models.

Interview with Wesley Whymark, CEO of Inventus Mining

The Paleoplacer Parallel

The geological rationale for early investor interest lies in the deposit type itself. Paleoplacer deposits ancient riverbeds or sedimentary basins where gold accumulated within conglomerate formations are associated globally with large gold endowments. The Witwatersrand Basin in South Africa, the world's largest gold district, is a paleoplacer system, and it was this analogue that initially drew attention to Pardo.

At Pardo, the shallow depth and flat geometry not only reduce exploration costs but also create the optionality for low-strip-ratio surface mining if the deposit proves large enough to support standalone operations. The proximity to existing infrastructure, including McEwen's mill and Ontario's established mining supply chain, further supports the economic framework.

Execution Year Ahead

The next 12 months will test whether Inventus can deliver on the dual objectives of resource definition and permitting advancement while maintaining its self-funding discipline. The Q3 resource estimate represents the first formal quantification of the deposit's scale, providing a baseline for future growth and a technical foundation for regulatory submissions.

Market reception has been supportive. With shares up more than 145% over the past year and a market capitalisation approaching $56 million, investors appear willing to assign value to the operational execution story even ahead of a maiden resource. Whether that momentum continues will likely depend on the size and grade of the Q3 estimate and the company's ability to demonstrate that bulk-scale ore sorting can deliver the economics suggested by earlier scoping work.

For a junior gold space increasingly characterised by capital discipline and operational pragmatism, Inventus Mining offers a case study in alternative development pathways one where extraction economics are proven before resource estimates, where cash flow funds technical studies rather than the reverse, and where strategic partnerships substitute for repeated equity raises. If Whymark and his team execute on the 2026 milestones, the company may offer a template for how patient capital and geological luck can converge into a self-reinforcing development cycle.

TL;DR:

Inventus Mining is executing a rare self-funding development model at its Ontario Pardo Paleoplacer project, extracting and selling gold before defining a formal resource while backed by Eric Sprott (16%) and McEwen Mining's founder (17%). The company targets a Q3 2026 maiden resource estimate and late-2026 production permit for ~200,000 tonnes, with potential early 2027 production start, while advancing ore sorting technology that could eliminate 60% of processing costs. Shares have doubled to $0.27 as the company demonstrates it can generate positive cash flow from bulk sampling, positioning it as a low-dilution alternative to typical drill-and-raise junior models.

FAQs (AI Generated)

The company extracts gold-bearing material under a 50,000-tonne bulk sample permit and pre-sells it to McEwen Mining's nearby mill. This arrangement covers extraction costs and funds technical work, essentially doubling invested capital per bulk sample cycle.

The flat-lying conglomerate reef sits at or near surface, allowing blast-and-extract operations without underground development. Grades of 2.5-3.5 g/t gold across a two-metre-thick unit, combined with 90%+ mill recoveries, enable profitable extraction before formal resource definition.

Q3 2026 maiden resource estimate, late 2026 production permit submission (45-day approval timeline), and potential early 2027 production start. The 200,000-tonne permit would support approximately 20 months of operations at 10,000 tonnes/month processing rates.

2018 testing showed XRF sorting could concentrate 93% of gold into 40% of material, eliminating 60% of trucking and milling costs. Modern sorters process 40-120 tonnes/hour at $1-1.5M capital cost. Bulk-scale testing planned to confirm commercial viability before equipment purchase.

Combined strategic ownership of 43% (Sprott 16%, McEwen founder 17%, McEwen Inc. 10%) validates both the paleoplacer geological model and self-funding execution approach. McEwen's mill partnership enables the cash-generative business model while aligning commercial incentives.

Analyst's Notes

Subscribe to Our Channel

Stay Informed