Middle East Supply Chain Disruptions Are Driving Cost Inflation Across Salt Markets

Middle East disruptions are inflating mining costs globally. Assets with low FOB costs, port access, and domestic supply advantages are repricing.

- The near-collapse of shipping through the Strait of Hormuz is disrupting energy, fertilizer, and bulk commodity flows, creating second-order inflation across mining inputs and logistics costs that is compressing margins for high-cost producers.

- Energy price volatility is translating directly into all-in sustaining cost (AISC) inflation across the mining sector, with energy comprising 15-30% of operating costs depending on mine type and configuration.

- Global trade growth is forecast to slow materially through 2026, with higher transport and fuel costs acting as a structural drag on bulk commodity flows and producer margins worldwide.

- Supply chain fragmentation is increasing the relative value of regionally secure, infrastructure-linked assets, particularly those with deep-water port access, advanced permitting, and low operating cost structures.

- Development-stage projects with feasibility-level economics, such as Atlas Salt's Great Atlantic salt project in Newfoundland, are gaining investor relevance as capital prioritizes cost discipline and logistics advantage over scale alone.

A Supply Shock with Multi-Commodity Consequences

The escalation of conflict across the Middle East has evolved beyond a regional geopolitical issue. Disruption in the Strait of Hormuz, handling roughly 25-30% of global oil and ~20% of LNG flows, has triggered cascading cost pressures across energy, agriculture, and mineral markets.

This is not a contained energy shock but a systemic inflation event affecting mining operations, bulk logistics, and fertilizer supply chains. Shipping through the Strait has fallen by ~95%, forcing rerouting that raises freight costs, delays delivery, and increases war-risk premiums.

Rising input costs compress margins at the high end of the cost curve, supply disruptions support commodity prices, and assets with structural logistics advantages gain relative value as markets reprice risk.

Global Energy Shock as the Primary Transmission Mechanism

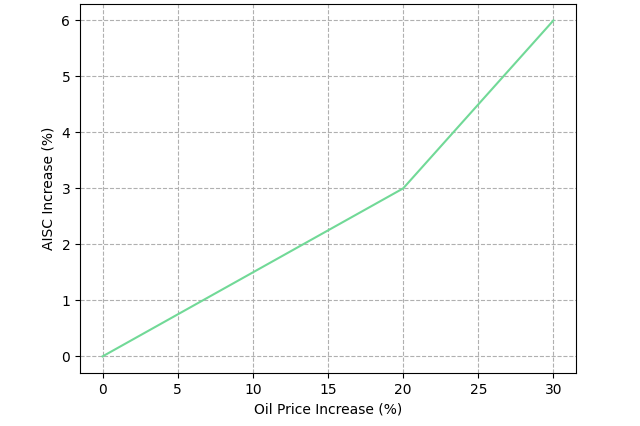

Crude oil and natural gas price spikes from Middle East disruptions feed directly into mining cost inflation via diesel, power generation, and chemical inputs. With energy accounting for 15-30% of operating costs, a sustained 30% rise in oil prices can lift total costs by roughly 4.5-9.0 percentage points for producers lacking hedging or on-site generation.

For bulk commodity producers, where margins are already thinner, this pressure directly compresses profitability. Diesel-dependent operations in potash, salt, and aggregates face immediate cost inflation that is difficult to pass through under fixed or long-term contracts, widening the gap between low-cost and logistics-exposed producers.

These commodities are also highly sensitive to freight volatility due to low value-to-weight ratios. A 20-30% increase in shipping costs materially raises delivery costs as a share of value, compressing FOB-CIF spreads and disadvantageous producers without efficient port access or streamlined logistics.

Fertilizer Shock & the Feedback Loop into Commodity Markets

Urea prices surged roughly 46% month-over-month between February and March 2026, driven by natural gas price escalation, the primary feedstock for nitrogen fertilizers, and disruptions to Middle Eastern export capacity. The ripple effects extend beyond agriculture: fertilizer inflation feeds into food-linked CPI components, lifting labor cost expectations and adding to the broader inflationary pressure that has kept central banks in restrictive mode longer than markets anticipated.

For mining, the impact is both direct and indirect. Ammonium nitrate for blasting and certain flotation reagents share feedstock linkages with the fertilizer complex, while food-driven labor cost inflation adds workforce pressure in inflation-sensitive geographies.

The Hormuz disruption exposed supply chain fragilities rooted in a broader geopolitical fragmentation of global trade accelerating since 2018, spanning sanctions regimes, export controls, and bilateral trade restructuring. Near-term de-escalation might ease energy prices, but structural vulnerabilities in bulk commodity logistics and fertilizer supply chains won't be resolved by a ceasefire. Investors should price a persistent volatility premium into operating cost assumptions for bulk commodity producers.

Trade Flow Fragmentation & Regionalization of Commodity Supply

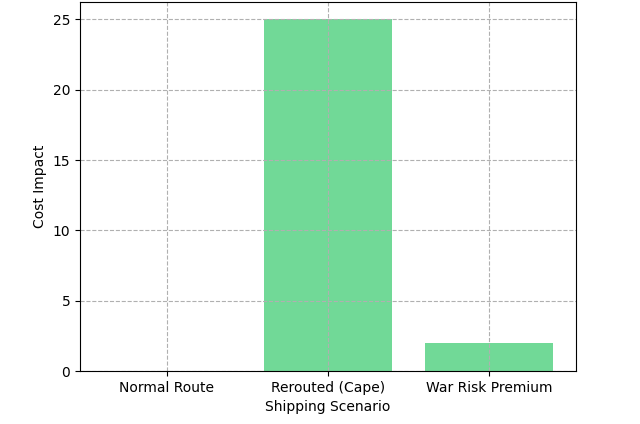

The roughly 95% decline in shipping traffic through the Strait of Hormuz adds 10-14 days to Asia-Europe and Middle East-North America voyages, extending working capital cycles, increasing bunker fuel consumption, and raising per-tonne freight costs beyond what bulk commodity economics are calibrated to absorb. War-risk insurance premiums on Hormuz-adjacent routes have spiked to 2019 tanker-attack levels, adding $1-3 per tonne to effective delivery costs depending on cargo type and vessel classification.

Bulk commodity buyers, industrial salt consumers, agricultural input distributors, infrastructure operators, are accelerating a sourcing shift toward domestic or near-shore supply that was already underway before this disruption. Supply security frameworks formalized across North America and Europe since 2022 now have added urgency and political backing.

Assets in politically stable, infrastructure-capable jurisdictions, particularly those with existing regulatory approvals and proximity to end-market demand, command a measurable premium over equivalent assets facing longer permitting timelines or greater trade route exposure.

Why Infrastructure-Linked Assets Are Repricing

Deep-water port proximity reduces handling costs, eliminates transshipment exposure, and cuts transit time, but more critically, it insulates a producer's delivered cost from third-party logistics risk. When freight rates spike 20-30% and insurance premiums double on affected trade lanes, a mine loading directly onto vessels at a dedicated berth faces an entirely different cost profile than one dependent on trucking to a regional terminal and onward transshipment.

A Case Study in Logistics-Driven Valuation: Atlas Salt

Atlas Salt's Great Atlantic project in Newfoundland sits adjacent to deep-water port infrastructure, designed for 4.0 Mtpa of production at a feasibility-study FOB cost of approximately $28 per tonne. Against a North American market importing 8-10 Mtpa of de-icing salt annually with no new mine commissioned in 25 years, that cost structure and logistics positioning carry measurable competitive relevance.

The 2024 feasibility study supports an NPV (8% discount rate) of approximately $920 million, an IRR of 21.3%, and a payback period of roughly 4.2 years. In an inflationary cost environment where competing producers face AISC escalation from energy and freight inputs, a locked FOB cost well below market with direct port access maintains margin integrity that higher-cost operations cannot replicate.

Atlas Salt's Chief Executive Officer Nolan Peterson frames the company's market position in terms of the supply-demand imbalance that underpins the project's pricing assumptions:

“There’s not enough supply, while demand remains strong. No new mine has been built in 25 years at this point. As a result, we have pricing power across many domestic operations, as well as over foreign imports that we are largely aiming to displace.”

Cost Inflation vs. Commodity Pricing

North America imports 8-10 Mtpa of de-icing salt, primarily from Chile, Egypt, and other offshore sources now facing elevated freight costs and trade route disruption. With no new domestic mines commissioned in a generation and demand growing alongside population and infrastructure expansion across Snow Belt states and Canadian provinces, the supply gap is current market reality, not a projection. Low-FOB-cost domestic entrants can displace import-priced supply at favourable margins precisely when those imports are becoming more expensive to land.

The question is not whether salt prices are rising, they are, modestly and steadily, but whether a specific asset can deliver at a cost that preserves margin across plausible price outcomes. Logistics advantage, contract structures, and operating cost discipline are the differentiating variables.

Capital Allocation & Financing in a Volatile Macro Environment

Higher interest rates and elevated geopolitical risk have increased WACC for mining project financing across the board. Infrastructure-heavy projects with long construction timelines face the most pressure, as cost escalation risk compounds with every quarter of delay. Institutional capital has shifted toward feasibility-stage or construction-ready assets with clear permitting pathways, where execution risk is quantifiable rather than open-ended.

Atlas Salt is targeting approximately 60% debt financing for the Great Atlantic project's main construction package. That structure is achievable because the project's economics are strong enough to support senior debt service without requiring a commodity price premium above current market levels. Securing debt financing is a key derisking milestone: once locked in, it reduces equity risk and positions the asset for re-rating by institutional investors who require financing certainty before committing capital at scale.

Operational Visibility & Development Timelines

Quarterly delays on construction-stage projects mean cost escalation, additional carrying costs, and extended input price uncertainty. Early work activity reduces execution uncertainty in a way pre-construction assets cannot replicate.

Atlas Salt initiated early works at the Great Atlantic site in 2026, with first production targeted around 2030. Construction-stage projects carry a different risk profile than pre-construction assets: quarterly schedule delays generate direct cost escalation, additional carrying costs, and extended input price exposure. Each construction milestone completed reduces the execution risk discount the market applies to development-stage assets, creating a sequential re-rating pathway as Great Atlantic moves from early works through to commissioning.

The Investment Thesis for Salt

- Geopolitical fragmentation of global trade is embedding a structural volatility premium into bulk commodity supply chains, increasing the value of assets insulated from trade route disruption by domestic jurisdiction and direct port access.

- Low-cost producers positioned at the bottom of the operating cost curve maintain margin integrity across a wider range of commodity price and freight cost scenarios, providing downside protection that higher-cost operations cannot offer.

- North American supply security is becoming a procurement priority for industrial buyers, creating a structural demand premium for domestically sourced bulk minerals that displaces offshore supply exposed to elevated freight and insurance costs.

- Infrastructure-linked assets with deep-water port access reduce exposure to third-party logistics risk and freight cost volatility, which is the primary transmission mechanism of the current Middle East disruption into bulk commodity margins.

- Advanced-stage projects with completed feasibility studies, government-approved environmental assessments, and initiated construction activity offer asymmetric upside as financing closure and construction milestones compress the development-stage valuation discount.

Freight rates, fertilizer costs, and energy prices have moved in response to Middle East supply chain disruption. If that disruption persists, the delivered economics of bulk commodity supply chains face sustained cost pressure, a condition that increases the relative defensibility of projects with fixed logistics infrastructure and low operating cost bases.

Assets with low operating costs, direct port access, and advanced permitting are exposed to less logistics cost risk than projects dependent on disrupted trade routes. Where North American supply gaps exist in bulk minerals, those assets also face reduced competition from imports facing elevated freight and delivery costs. Projects whose feasibility assumptions predate 2024 cost conditions may carry unpriced logistics risk that current economics do not reflect.

TL;DR

Middle East supply chain disruptions have pushed energy, freight, and fertilizer input costs higher across bulk commodity markets, compressing margins for operations exposed to those cost lines. Atlas Salt's Great Atlantic project carries a feasibility-study FOB cost of approximately $28/tonne, direct deep-water port access, and 4.0 Mtpa of permitted production capacity, with construction already underway. The North American de-icing salt market has seen no new domestic mine enter production in 25 years, leaving import-dependent buyers directly exposed to freight cost inflation. Great Atlantic's cost structure and logistics position reduce that exposure for offtake counterparties.

FAQs (AI generated)

The transmission mechanism is indirect but traceable. Disruption to Hormuz shipping has pushed crude oil and natural gas prices higher, directly inflating diesel and power costs that account for 15-30% of mining operating expenses. Natural gas price escalation has also driven a ~46% month-over-month spike in urea prices, raising costs for ammonium nitrate used in blasting and other chemical inputs tied to the fertilizer complex. Freight rerouting around the Cape of Good Hope adds 10–14 days to voyages and $1-3 per tonne in war-risk insurance premiums. Together, these pressures are compressing margins at the high end of the cost curve while producers with low FOB costs and domestic logistics face materially less exposure.

When freight rates spike 20-30% and insurance premiums double on affected trade lanes, a producer's logistics setup becomes a primary determinant of delivered cost competitiveness. A mine with direct deep-water port access loads onto vessels at a fixed, controllable cost. A mine dependent on trucking to a regional terminal and onward transshipment absorbs every layer of third-party logistics volatility. In stable freight environments, this difference is meaningful. In the current environment, it is the difference between margin integrity and margin compression. Port-linked assets are repricing accordingly.

North America imports 8-10 Mtpa of de-icing salt annually, primarily from Chile, Egypt, and other offshore sources. No new domestic mine has been commissioned in approximately 25 years, while demand has grown steadily alongside population expansion and infrastructure investment in Snow Belt states and Canadian provinces. The supply gap is not a forecast, it is current market reality. With offshore supply now facing elevated freight costs and trade route disruption, domestically produced salt with a low FOB cost can displace import-priced supply at favourable margins precisely when those imports are becoming more expensive to land.

The project combines the specific characteristics that carry a premium in the current environment: deep-water port adjacency in Newfoundland, a feasibility-study FOB cost of approximately $28 per tonne, 4.0 Mtpa of designed production capacity, a government-approved environmental assessment, and early works construction already initiated. The 2024 feasibility study supports an NPV of ~$920 million at an 8% discount rate, an IRR of 21.3%, and a payback period of roughly 4.2 years. These economics are strong enough to support approximately 60% debt financing without requiring commodity prices above current market levels, making the financing structure achievable and the derisking pathway clear.

The evidence favors structure. The supply chain fragilities exposed by the Hormuz disruption are rooted in a geopolitical fragmentation of global trade that has been accelerating since 2018 across sanctions regimes, export controls, and bilateral trade restructuring. A ceasefire would ease near-term energy prices but would not resolve the underlying vulnerabilities in bulk commodity logistics and fertilizer supply chains. Institutional capital is already rotating toward assets with quantifiable execution risk, domestic jurisdiction, and infrastructure-linked cost advantages. The supply chain assumptions embedded in pre-2024 project economics no longer hold, and assets built for the current cost environment are structurally positioned to outperform those that were not.

Analyst's Notes

Subscribe to Our Channel

Stay Informed