Prevailing Over 30 Years with Zero Rollbacks: Eagle Plains' 2026 Drilling Offers Exploration Leverage Without Dilution

Eagle Plains Resources runs a five-pillar mining model — exploration, project gen, incubation, contracting & royalties — with $8M cash, 29 projects & 7 drills planned for 2026.

- Eagle Plains Resources has operated for over 30 years as the oldest company on the TSX Venture Exchange never to have undergone a share consolidation, underpinning its reputation for financial discipline and long-term capital stewardship.

- The company's five-pillar business model - spanning mineral exploration, project generation, corporate incubation, geological contracting, and royalty generation - provides multiple independent revenue streams that insulate the company from dependence on any single commodity price or exploration outcome.

- Eagle Plains is scaling its 2026 exploration programme significantly, targeting 29 projects with approximately $13 million in combined expenditures and seven drill programmes, the majority of which are funded by option partners rather than the company's own treasury.

- Through three completed spinout transactions - including Copper Canyon (sold to NovaGold for over $60 million) and Taiga Gold (acquired by SSR Mining) - Eagle Plains has returned approximately $115 million to shareholders while allowing investors to retain their original Eagle Plains shares throughout each event.

- With just over $8 million in cash, approximately $2.1 million in equity holdings, and only 12 million shares issued over the last six years, Eagle Plains maintains one of the most disciplined balance sheets and capital structures in the junior mining sector.

In a sector where many junior mining companies live and die by a single commodity price move or a binary drill result, Eagle Plains Resources (TSXV: EPL) presents a notably different proposition as the company has spent more than 30 years developing a multi-revenue-stream model that generates value across market cycles, rather than being wholly dependent on the fortunes of any one project or commodity. Eagle Plains is the fourth-oldest company listed on the TSX Venture Exchange and, notably, the oldest that has never undergone a share consolidation - a record that speaks to the financial discipline underpinning its long-term management approach.

President and CEO Charles C. Downey outlined the company's strategic priorities for 2026, the mechanics behind its shareholder return framework, and how improved capital availability across the junior mining sector is beginning to accelerate activity across its extensive project portfolio.

The Five Pillars: How Eagle Plains Creates Value

Eagle Plains operates across five distinct business lines, each contributing to the company's overall financial position and risk profile:

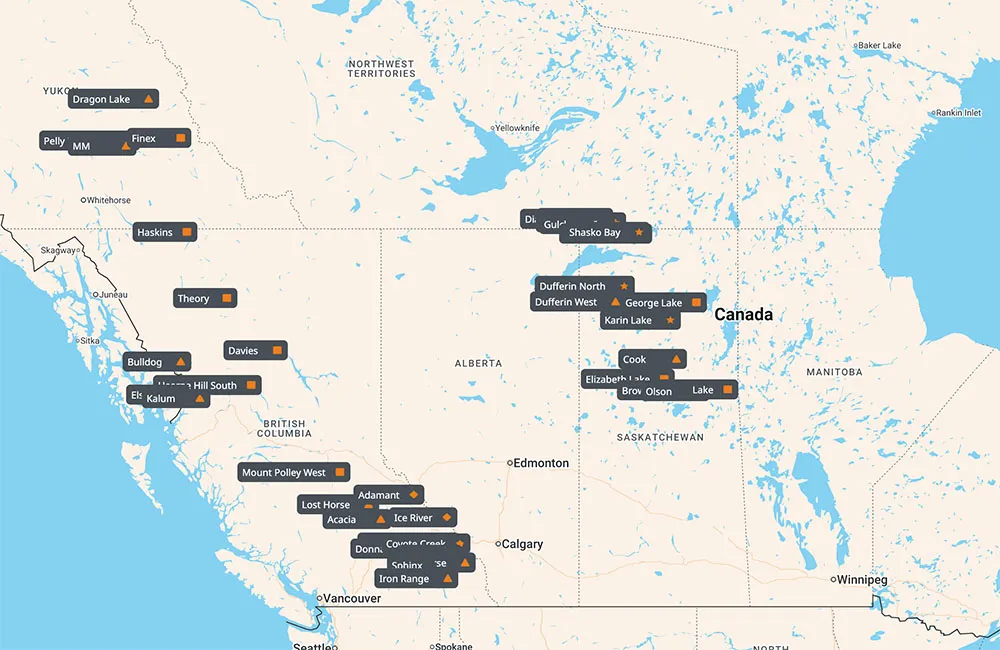

The first and most fundamental is mineral exploration. Eagle Plains holds more than 100 projects at various stages of development, spanning grassroots targets through to properties with historical resources and early drill intercepts. Approximately 60 of those projects are located in British Columbia, with around 40 in Saskatchewan and additional assets emerging in the Yukon.

The second pillar is project generation. Eagle Plains identifies, stakes, and acquires projects at 100% ownership, conducts early-stage exploration work using its own capital, and then seeks option partners to fund further development. Partners can earn either a 60% - 80% interest by completing exploration expenditures, making modest cash payments, and issuing shares, giving Eagle Plains leveraged exposure to multiple simultaneous exploration programmes without bearing the full cost.

The third pillar is corporate incubation. Eagle Plains packages particularly prospective assets into standalone spinout companies, distributing shares to existing Eagle Plains shareholders on a ratio basis - typically one new share for every two or three Eagle Plains shares held. These companies are then financed and built independently with the intention of being sold to larger acquirers. To date, the company has completed four spinouts, three of which have been sold, generating approximately $115 million for shareholders.

The fourth pillar is geological contracting through wholly owned subsidiary TerraLogic Exploration, which provides geological services both to Eagle Plains and to third-party clients. This segment generates between $1 million and $2 million in annual revenue and effectively subsidises the company's in-house technical capacity.

Lastly, the fifth pillar is royalty generation. Eagle Plains retains a net smelter royalty interest on all optioned and sold properties, steadily building a portfolio of royalty assets across its project network. The most recent expression of this strategy was the Eagle Royalties spinout, which was sold to Summit Royalties for approximately $13 million - assets that had been carried on the company's books at zero value.

Interview with Charles C. Downie, President & CEO of Eagle Plains Resources

2026 Exploration Programme: Significant Scale-Up Underway

One of the most material developments disclosed in the interview is the significant increase in planned exploration activity for 2026. After working on 22 projects in the prior year, Eagle Plains is targeting 29 projects this year with combined expenditures of approximately $13 million - the majority of which will be funded by option partners rather than the company's own treasury.

Seven drill programmes are planned across the portfolio. Two will be self-funded by Eagle Plains, with the remaining five funded by partners. Downey was direct about the commercial rationale underpinning this model:

"We've got 20 geologists and 20 technical people that somebody else pays their salary for three-quarters of the year. So they're pretty much free employees for us and they're generating revenue."

Eagle Plains will also carry out evaluation work on new and pipeline projects, with an estimated $500,000 to $600,000 budgeted for assessment activity alongside the drilling expenditures.

Uranium Exposure in the Athabasca Basin

Beyond gold and base metals, Eagle Plains has been active in Saskatchewan's Athabasca Basin uranium district for approximately 15 years. Two option partnerships are now advancing uranium-focused projects in the region. The first, with Refined Energy, is targeting the Duffer and Duffer West project with a drill programme commencing imminently at the time of the interview. The second, with Excite Resources, is focused on the northern portion of the Athabasca Basin near Athabasca Lake.

The uranium exposure sits within Eagle Plains' broader commodities framework, with Downey confirming the company holds positive sentiment toward the uranium market. Both programmes are partner-funded, consistent with the project generation model.

Spinout Track Record: The Case Studies

Two historical case studies illustrate the potential return profile of the spinout model. Copper Canyon, a project acquired from a prospector for a modest cash and share consideration on which Eagle Plains spent negligible exploration capital was ultimately sold to NovaGold for over $60 million in value, with Eagle Plains shareholders receiving NovaGold shares in the transaction.

The second is a collection of gold projects assembled in Saskatchewan portfolio, Taiga Gold, which was spun out and subsequently acquired by SSR Mining, again delivering a significant return to Eagle Plains shareholders. The most recent spinout, Eagle Royalties, was built around the Banyan Gold AurMAC royalty - a property now hosting a seven-million-ounce gold deposit in the Yukon - alongside a basket of other royalty interests. It was sold to Summit Royalties for approximately $13 million.

Eagle Plains retained one million shares in Summit Royalties following the transaction, which were trading at approximately $1.60 at the time of the interview, adding approximately $1.5 million to the company's anticipated balance sheet position.

Balance Sheet and Capital Discipline

Eagle Plains entered 2026 with just over $8 million in cash and approximately $2.1 million in equity holdings across around 20 companies, as reported in its 2025 financial statements. The company has issued only approximately 12 million shares over the last six years - a figure that underscores the low-dilution discipline embedded in its operating model.

Downey was explicit about the company's self-funding capacity and its intention to avoid returning to equity markets for capital in the near term, stating:

"Another thing I might point out too is the another reason we're kind of different from other juniors is we we don't have to issue any stock. You know, when you look at us, we've been around for 30 years [...] We don't have to issue shares. We don't, I don't see any reason to go to the market in the near future."

The combination of geological contracting revenue, option deal payments, and portfolio monetisation events provides the company with sufficient cash generation to sustain operations and fund its self-directed exploration programmes without shareholder dilution.

The Investment Thesis for Eagle Plains Resources

- Diversified revenue model reduces single-point risk. Unlike most junior explorers, Eagle Plains generates ongoing cash from geological contracting, option deal payments, and royalty interests - meaning the company is not exclusively dependent on capital markets or commodity price moves to sustain operations.

- $13 million exploration programme in 2026 - mostly partner-funded. The majority of the $13 million in planned 2026 expenditures is being funded by option partners. Eagle Plains gains exploration exposure across 29 projects while deploying a fraction of that capital itself.

- Proven shareholder return mechanism. Three completed spinout transactions have returned approximately $115 million to shareholders. Eagle Plains shareholders retain their original shares through each event, providing cumulative return potential without dilution.

- Low share count and minimal dilution. With 115 million shares outstanding after more than 30 years - and only 12 million shares issued over the last six years - Eagle Plains offers a structurally disciplined capital structure relative to the junior mining peer group.

- Strong cash position provides cycle resilience. With over $8 million in cash plus equity holdings, Eagle Plains is not reliant on a buoyant market to fund operations. This allows opportunistic project acquisition during sector downturns.

- Uranium and gold exposure across multiple jurisdictions. The company holds projects across gold, uranium, copper, and other commodities in BC, Saskatchewan, and the Yukon, offering commodity diversification within a single investment.

- Actionable consideration for investors: Eagle Plains is best assessed as a long-duration, compounding vehicle rather than a near-term discovery play. Investors should monitor annual spinout pipeline developments and partner-funded drill results as the primary near-term catalysts, while the royalty portfolio and balance sheet provide downside support.

Project Generators in a Rising Commodity Cycle

The project generator model has historically been one of the more overlooked structures in junior mining, but it is arguably one of the most rational responses to the inherent volatility of exploration-stage investing. Rather than concentrating capital into a single asset and a single discovery outcome, project generators build diversified optionality across multiple targets, commodities, and jurisdictions - monetising value through option payments, spinouts, and royalties rather than through direct development. As Downey summarised:

"It doesn't really matter what commodity prices are. We've got lots of cash. So even when commodity prices are low and people are having trouble financing, it doesn't really matter to us - we can go out and acquire projects, work projects up, and get ready for the next cycle."

The current macro environment strengthens the case for this model considerably. Gold prices have moved materially higher from the lows of prior years, financing conditions for junior explorers are beginning to ease after an extended period of constraint, and policy support for domestic critical minerals supply chains is directing capital toward North American mining jurisdictions. Uranium adds a second macro dimension. The structural supply deficit in the uranium market, combined with renewed government interest in nuclear energy as a baseload power source, has reactivated exploration interest in the Athabasca Basin - one of the highest-grade uranium districts in the world.

The precise condition that enables a project generator like Eagle Plains to scale its activity without proportional increases in its own capital deployment. Eagle Plains' 15-year presence in the region positions it with an established portfolio of staked and evaluated targets at a time when partner interest in Athabasca exploration is rising. The combination of rising commodity prices, improving junior market liquidity, and growing government support for domestic resource development creates a context in which a diversified, low-dilution project generator with a strong balance sheet is particularly well positioned.

TL;DR

Eagle Plains Resources is a Canadian project generator with over 30 years of operating history, more than 100 mineral projects across British Columbia, Saskatchewan, and the Yukon, and a five-pillar business model that generates revenue from geological contracting, option deals, royalties, and spinout transactions - not just exploration results. The company has returned approximately $115 million to shareholders through three completed spinouts while maintaining a strong cash position and issuing minimal shares. In 2026, it is advancing 29 projects with approximately $13 million in planned expenditures - mostly funded by partners - including uranium drill programmes in the Athabasca Basin. For investors seeking diversified exposure to a rising commodity cycle without excessive dilution risk, Eagle Plains represents an unusual and disciplined vehicle in the junior mining space.

Frequently Asked Questions (FAQs) AI-Generated

Eagle Plains generates revenue through several mechanisms that do not depend on reaching production. Its geological contracting subsidiary, TerraLogic Exploration, earns between $1 million and $2 million annually by providing services to both Eagle Plains and third-party clients. Option partners make annual cash and share payments to maintain their earn-in rights on Eagle Plains projects. The company also receives proceeds from royalty portfolio sales and spinout transactions. This structure means Eagle Plains can sustain operations and build its asset base across commodity cycles without relying solely on equity markets or exploration success.

A spinout occurs when Eagle Plains packages a group of assets — typically exploration projects or royalty interests — into a new standalone company. Existing Eagle Plains shareholders receive shares in the new entity on a fixed ratio basis, often one new share for every two or three Eagle Plains shares held. Eagle Plains retains a portion of shares in the new company as well. The new entity is then financed and developed independently, with the objective of being sold to a larger acquirer. Crucially, Eagle Plains shareholders retain their original shares throughout this process, meaning each successful spinout represents an additional return layered on top of their existing investment rather than a dilutive restructuring.

Of the approximately $13 million in planned 2026 exploration expenditures, the substantial majority is being funded by Eagle Plains' option partners — companies that have agreed to spend capital on Eagle Plains projects in exchange for earning a 60% or 80% interest. Eagle Plains itself plans to directly fund two of the seven drill programmes, with the remainder financed by partners. The company has separately budgeted approximately $500,000 to $600,000 for evaluation work on new and pipeline projects. This structure allows Eagle Plains to participate in a materially larger exploration programme than its treasury alone could support.

Eagle Plains has been active in Saskatchewan's Athabasca Basin — one of the world's premier uranium jurisdictions — for approximately 15 years. The company currently has two partner-funded uranium drill programmes underway: one with Refined Energy targeting the Duffer and Duffer West project, and one with Excite Resources focused on the northern Athabasca Basin near Athabasca Lake. Both programmes are consistent with the project generation model and carry no direct exploration cost to Eagle Plains. Uranium is relevant to the investment case because renewed global interest in nuclear energy as a baseload power source has increased exploration activity and partner appetite in the Athabasca Basin, potentially accelerating the monetisation of Eagle Plains' uranium project inventory.

Eagle Plains' business model is designed to generate sufficient cash through contracting revenue, option payments, and asset sales to fund operations without frequent recourse to equity markets. Over its entire 30-year history, the company has issued approximately 115 million shares in total — an average of roughly four million shares per year — and has issued only approximately 12 million shares over the last six years. Management has indicated no intention to raise equity capital in the near term. This low-dilution approach is structurally significant for investors, as it means per-share value is not being systematically eroded by repeated capital raises, which is a common challenge across the junior mining sector.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed