Refining Constraints Keep Fuel Margins Near Four-Year Highs, Repricing Light, Sweet Crude

Refining capacity constraints, not crude prices, are driving fuel markets, supporting light crude premiums and increasing mining fuel costs.

- Global refining margins reached near four-year highs even as crude oil prices fell in June 2026, indicating that refinery capacity, rather than benchmark crude prices, is driving downstream fuel pricing.

- Global refinery runs remain about 6 million barrels per day below year-ago levels as Middle East export refineries remain offline, strikes continue to limit Russian refinery throughput, and Asian refiners operate below normal utilization, keeping global refining capacity constrained.

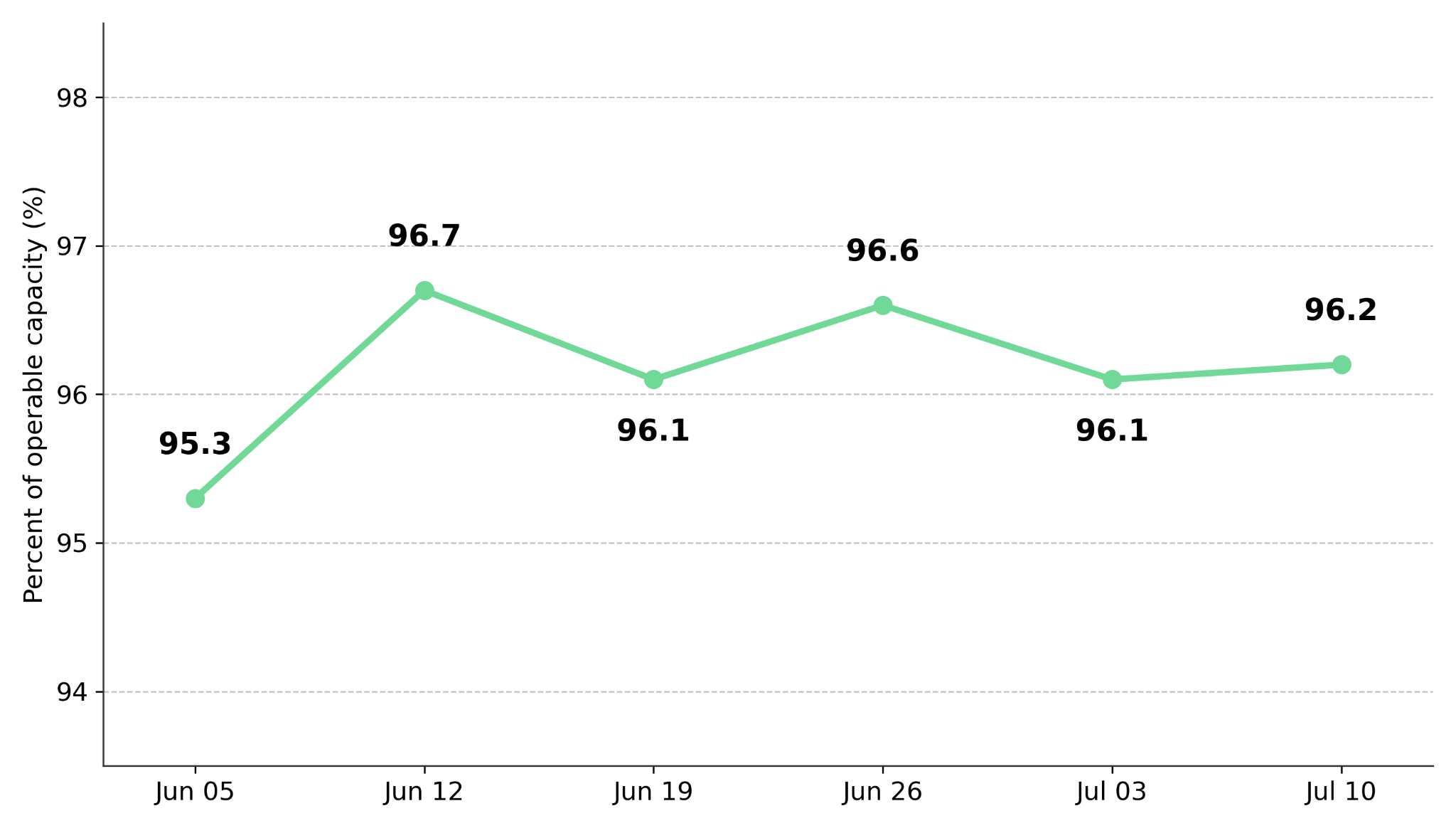

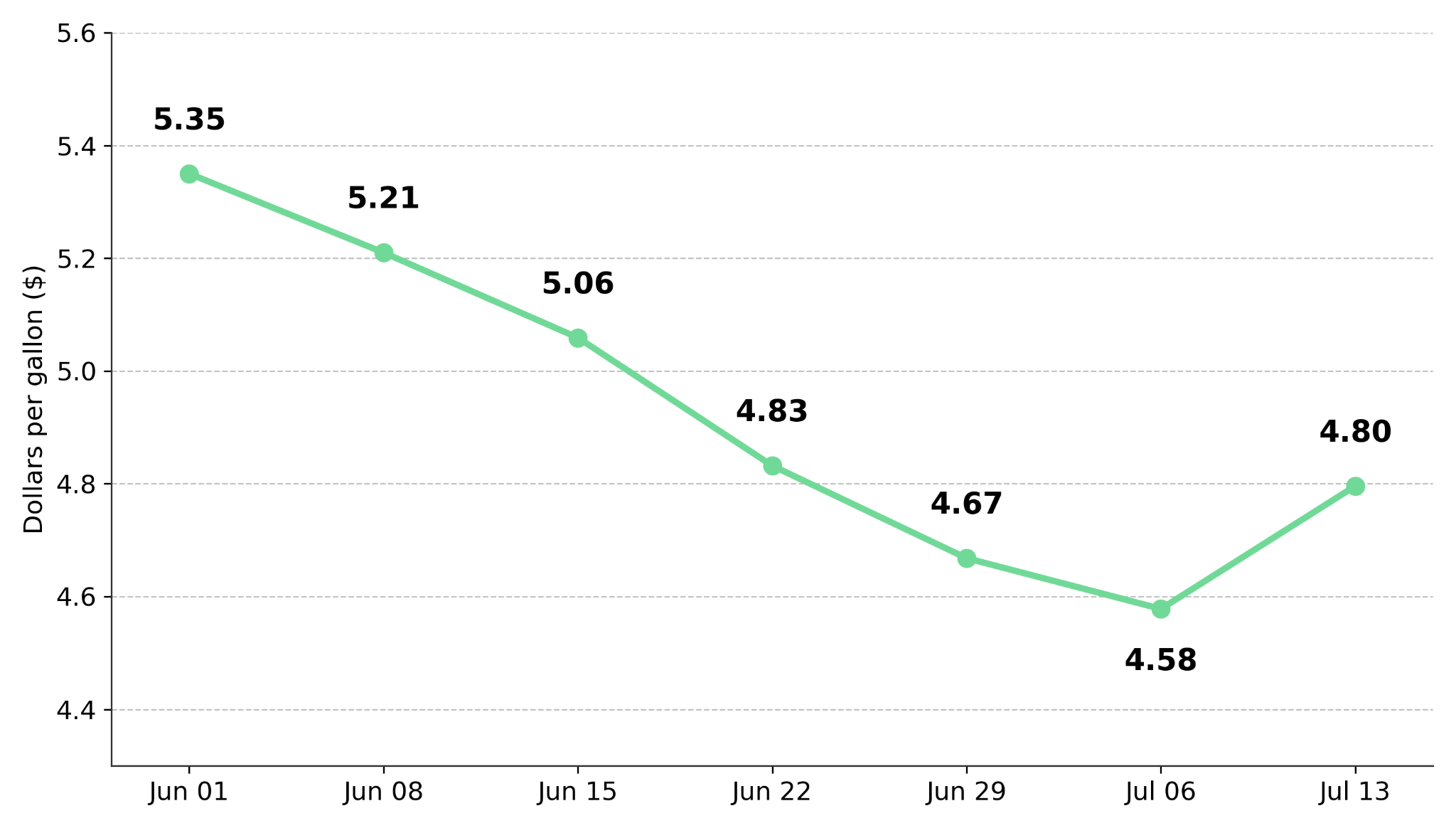

- US refinery utilization reached 96.2% for the week ending July 10, 2026, while distillate stocks increased by 4.6 million barrels. Despite the inventory build, the national average retail diesel price rose $0.218 to $4.796 per gallon, increasing fuel costs for diesel-dependent open-pit mining operations.

- Refining capacity constraints are increasing demand for light, sweet crude because it yields diesel and jet fuel with fewer processing steps and lower refining complexity.

- US Henry Hub natural gas spot prices fell to a two-month low, highlighting that oil and natural gas are following different price trends.

Lower Refinery Throughput Supports Premium Pricing & Rewards Light Crude Projects

Crude oil prices fell through June 2026 as geopolitical risk premiums unwound following earlier supply concerns. However, the IEA's July 2026 Oil Market Report found that refined product cracks and margins reached four-year highs in early July even as benchmark crude prices declined through June. OPEC's Monthly Oil Market Report placed the OPEC Reference Basket at $89.75 per barrel in June 2026, down $24.80 from May, although the year-to-date average remained $93.67 per barrel compared with the 2025 average of $72.04. Together, these trends showed that refinery capacity constraints, rather than benchmark crude prices, became the primary driver of downstream fuel pricing during the quarter.

Refining capacity, rather than crude demand, remains the primary constraint on oil market balances. According to the IEA's July 2026 Oil Market Report, global refinery runs remain about 6 million barrels per day below year-ago levels because Middle East export refineries have not yet restarted, Russian refining throughput remains curtailed following strikes on processing facilities, and many Asian refiners continue operating below typical utilization rates. As a result, refined fuel supply remains constrained despite adequate crude availability, supporting elevated refining margins and stronger demand for light, sweet crude.

Refining capacity constraints are increasing the pricing premium for higher-quality crude. Light, sweet crude commands a premium because it requires fewer refining steps to produce higher-value fuels such as diesel and jet fuel. As a result, projects producing light, sweet crude are better positioned to capture stronger realized pricing while refining capacity remains constrained.

Delayed Refinery Restarts Support Diesel & Jet Fuel Margins Despite Lower Crude

According to the EIA, refinery utilization reached 96.2% for the week ending July 10, 2026, with crude oil refinery inputs averaging 17.1 million barrels per day. Commercial crude stocks, excluding the Strategic Petroleum Reserve, fell 1.7 million barrels to 409.7 million barrels, about 6% below the five-year seasonal average. Although distillate inventories increased by 4.6 million barrels, the national average retail diesel price also rose $0.218 to $4.796 per gallon, indicating that refinery capacity constraints continued to limit effective fuel supply. That pricing strength supported elevated refining margins despite the increase in distillate inventories.

Delayed refinery restarts in the Middle East mean refining capacity is likely to recover more slowly than geopolitical risks subside. Even if regional conflict eases, refinery capacity constraints could continue supporting refined fuel margins until damaged facilities return to normal operations.

Refining Bottlenecks Raise Mining Costs & Differentiate Fuel-Exposed Assets

Higher diesel prices are increasing operating costs for diesel-intensive mining operations. At open-pit mines, diesel powers haul trucks, excavators, drill rigs, and on-site power generation, typically accounting for 15% to 30% of operating costs. With the EIA reporting retail diesel at $4.796 per gallon, higher fuel prices continue to increase operating cost pressure, particularly for mines with limited opportunities to substitute diesel consumption.

Jefferies estimates that every 10% increase in crude oil prices raises production costs at the average open-pit gold mine by about $10 per ounce. Higher fuel costs increase all-in sustaining costs (AISC), reducing operating margins unless stronger gold prices offset those additional expenses. By comparison, Jefferies estimates diesel accounts for about 5% of operating costs at copper solvent extraction and electrowinning (SX-EW) operations, versus 15% to 30% at diesel-intensive open-pit gold mines and other haulage-intensive mining operations. Greater grid electrification has reduced diesel dependence at many SX-EW sites over the past two decades, making those operations less sensitive to higher fuel prices.

Differences in fuel exposure are increasing cost differences between mining operations as diesel prices remain elevated. Mines with fuel hedges, grid-connected power, or underground operations are less exposed to higher diesel costs than diesel-intensive open-pit mines, making their operating margins less sensitive to fuel price volatility. As a result, fuel exposure has become an important consideration when evaluating project economics and the durability of future earnings.

API Gravity Reshapes Oil Valuations & Favors Higher-Quality Discoveries

API gravity, a measure of crude oil density, determines how much processing crude oil requires before it can be converted into refined products. Light, sweet crude, with high API gravity and low sulfur content, requires less processing to produce diesel and jet fuel, the products currently supporting the strongest refining margins. As long as refining capacity remains constrained, light, sweet crude is likely to command a premium over heavier, sour grades because refiners can produce more high-value fuels with lower processing complexity.

Current refining capacity constraints are increasing the valuation premium for new light, sweet oil discoveries. Compared with equivalent heavy crude discoveries, light, sweet resources can command stronger valuations because they require less complex processing and are compatible with a broader range of existing refineries.

How Light Oil Discovery Supports Stronger Project Economics

Trillion Energy is advancing exploration at its M47 Block in southeastern Türkiye following its April light oil discovery, where the C-1 well intersected 38 meters of net oil pay with 32.4° API gravity. An independent evaluation estimated 27.6 million barrels of 2C Contingent Resources at the North Discovery. In its July 16 update, the company announced that it had finalized the design and tender for a 40-kilometer 2D seismic program covering three priority exploration areas. The survey builds on a recently completed gravity study that confirmed fault-related structures across the license, with the new seismic lines positioned to tie into adjacent discoveries and identify new drilling locations ahead of the next exploration phase.

Scott Lower, President of Trillion Energy, explains why light oil remains economically competitive:

"The best thing to ever have a discovery on is light oil, onshore, conventional resource, because the margins are so good. We're estimating about $10 a barrel in production costs, compared to about $50 in North America."

Natural Gas Diverges From Oil as LNG Demand Grows

Oil and natural gas are often grouped together, but the two commodities are following different pricing paths in the US. Henry Hub spot natural gas fell to US$2.83 per million British thermal units (MMBtu) on July 13, 2026, its lowest level in two months, as record Lower 48 dry gas production of about 110.2 billion cubic feet per day and an LNG export outage at the Freeport terminal left more gas trapped in the domestic market. The resulting oversupply weighed on Henry Hub prices even as crude oil rose on international supply concerns, highlighting the different domestic and global forces driving the two markets.

European and Asian LNG markets face stronger pricing than US natural gas because robust import demand and exposure to international supply risks continue to support global LNG prices. By contrast, record US gas production and domestic oversupply have kept Henry Hub prices under pressure. As a result, oil-weighted, LNG-exposed, and US gas-focused producers face different pricing environments, creating meaningful differences in cash flow, earnings potential, and asset valuations.

Capital Allocation Shifts Toward Higher-Quality Energy Assets

Refining capacity is likely to remain the primary driver of fuel market balances because restarting refineries, restoring idled capacity, and increasing utilization take longer than increasing crude production or responding to geopolitical developments. OPEC+'s confirmed 188,000 barrel-per-day production increase effective August shows that additional crude supply alone cannot immediately increase diesel, jet fuel, or gasoline availability while refining capacity remains constrained. As a result, the pace of downstream capacity recovery is likely to have a greater influence on fuel prices than incremental increases in crude production.

The next one to two IEA Oil Market Reports will indicate whether Middle East refinery exports and Russian refining throughput are recovering. If refinery runs begin closing the current 6 million barrel-per-day year-on-year gap, refining margins should move closer to historical norms, easing diesel cost pressures for mining companies. If the gap persists or widens, premiums for light, sweet crude are likely to remain elevated, while higher diesel costs continue to pressure mining operations. Fed policy ahead of the July 29 FOMC meeting may influence energy demand expectations, but it is unlikely to alter the refining capacity constraints underpinning current fuel markets.

While Brent and WTI benchmarks reflect upstream crude pricing, they do not fully capture the impact of refining capacity constraints on downstream fuel markets. As a result, the gap between refining capacity and fuel demand is likely to have a greater influence on diesel prices, jet fuel prices, light, sweet crude premiums, and mining fuel costs than changes in crude prices.

The Investment Thesis for Oil & Gas

- Refining capacity, rather than crude prices, is currently the primary driver of downstream fuel margins. That dynamic is likely to persist while Middle East refinery restarts remain delayed and Russian refining throughput stays below historical levels.

- Quality differentiation has become an increasingly important valuation driver in a refining-constrained market. Light, sweet discoveries are likely to command stronger pricing premiums than heavier, sour crude while downstream capacity remains tight.

- Fuel cost exposure has become a key valuation variable as refining margins remain elevated. Diesel-intensive open-pit operations are likely to exhibit greater earnings sensitivity than grid-connected or underground mines, where fuel accounts for a smaller share of operating costs.

- For exploration-stage companies, completing seismic interpretation and defining the next drilling locations are often more important valuation catalysts than individual exploration results because they determine whether an initial discovery can be expanded into a larger resource.

- Resource classification should remain a key due diligence consideration because Contingent and Prospective Resources carry different levels of certainty under NI 51-101. Likewise, unrisked NPV estimates should be evaluated alongside their Chance of Development rather than treated as a base-case valuation.

- Gas-weighted and oil-weighted exposure should be evaluated separately because Henry Hub natural gas and crude oil are being driven by different market fundamentals. Treating energy producers as a single investment theme risks overlooking commodity-specific pricing drivers.

- Jurisdiction and proximity to existing infrastructure remain important valuation drivers. Discoveries located near established production and export networks are generally better positioned for lower development costs and shorter timelines than assets in frontier basins.

While downstream capacity remains constrained, asset quality, infrastructure access, fuel cost exposure, and commodity-specific fundamentals are likely to have a greater influence on project economics and equity performance than benchmark crude prices alone. For exploration-stage companies, disciplined evaluation of resource quality, development risk, and proximity to existing infrastructure remains essential, while the differences between oil and natural gas markets reinforce the need to assess each commodity on its own fundamentals. Together, these factors provide a more durable framework for capital allocation than short-term movements in crude prices. Until downstream capacity recovers, refining capacity, rather than crude prices alone, is likely to remain the primary driver of valuation across the energy value chain.

TL;DR

Refining capacity constraints have become the main driver of fuel markets, keeping refining margins near four-year highs despite lower crude prices. Delayed refinery restarts in the Middle East, reduced Russian throughput, and lower utilization in Asia have limited fuel supply, supporting premiums for light, sweet crude that requires less processing. Higher diesel prices are increasing costs for diesel-intensive mining operations, while natural gas follows a different price path because of US oversupply. Until downstream capacity recovers, refining constraints are likely to remain a more important valuation driver than benchmark crude prices across the energy sector.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed