Rutile Supply Is Shrinking as Titanium Demand Grows, & the Development Pipeline Cannot Bridge the Gap

Tightening rutile supply and rising demand are driving a deficit that strengthens pricing power and highlights the scarcity of investable projects.

Titanium occupies an unusual position in the critical minerals conversation. It is not priced on a terminal exchange, it does not appear often in policy announcements, and it rarely generates the investor attention that battery metals command. It is nonetheless embedded in the supply chains that Western aerospace, defence, and medical manufacturers depend on, and no commercially viable substitute exists for high-specification applications. Aircraft frames, surgical implants, naval vessels, and armoured vehicles all require titanium for properties that cannot be replicated by switching to another material.

Against that backdrop, the supply outlook for natural rutile, the highest-grade titanium feedstock, has deteriorated in a way that the market has been slow to price. According to leading titanium consultants TZ Minerals International Pty Ltd, demand for rutile from the titanium metals industry is forecast to grow 3% annually over the next decade while global supply is expected to decline by 7% per year over the same period. The arithmetic produces a widening structural deficit in the feedstock that sits at the base of the Western titanium supply chain.

Natural rutile deposits of meaningful scale are geologically rare, and the development timeline from discovery to production runs close to a decade under favourable conditions. The deficit will widen before it narrows, and the industry has not yet produced a credible development pipeline to address it.

Why Natural Rutile Has No Ready Substitute

Natural rutile is defined by its titanium dioxide content, which typically exceeds 95%. That concentration translates into lower processing costs, smaller slag volumes, and a reduced environmental footprint relative to lower-grade titanium feedstocks at the smelting and refining stage. For the segment of the market producing high-specification titanium metal for aerospace, defence, and medical applications, natural rutile is the preferred feedstock on the basis of those processing characteristics. Switching to lower-grade material is technically possible in some applications but carries cost and quality penalties that producers of high-specification alloys are not prepared to absorb.

The supply chain that connects rutile to end markets runs through a narrow geography. Japan is the world's second-largest producer of titanium sponge after China and produces the highest-quality titanium alloys for aerospace, defence, and advanced manufacturing. Toho Titanium Co., Ltd. and Osaka Titanium Technologies Co., Ltd. together account for more than 60% of aerospace and defence-grade titanium metal production outside China and Russia. The United States sourced more than 70% of its titanium sponge imports from Japan in the first half of 2025, placing Japan at the centre of the Western titanium supply chain.

Tightening feedstock availability at the base of that chain places upward pressure on natural rutile pricing relative to synthetic alternatives. Producers with access to high-grade natural material hold pricing leverage that those dependent on synthetic or lower-grade inputs do not. That dynamic reinforces the premium that natural rutile already commands, and it is likely to become more pronounced as established producing operations mature and supply volumes decline.

Policy Acceleration & the Shift in Buyer Procurement Strategy

The policy response to critical mineral supply concentration has moved quickly. In February 2026, US Secretary of State Marco Rubio hosted the inaugural US Critical Minerals Ministerial in Washington, bringing together more than 50 nations to coordinate supply chain resilience efforts. Japan's State Minister for Foreign Affairs delivered keynote remarks alongside senior US officials, citing urgency over critical mineral supply chain disruption risk. The United States government mobilised more than US$30 billion in support for critical mineral supply chain projects in the preceding six months. The United States, European Union, and Japan subsequently announced their intention to develop coordinated Action Plans covering border-adjusted price floors and a preferential trade framework for critical minerals.

At the buyer level, the response has been practical rather than declaratory. Titanium producers with direct exposure to feedstock risk have moved earlier in the development cycle, qualifying products from potential new sources and establishing commercial frameworks before production commences. In June 2025, Toho Titanium confirmed the suitability of rutile from a project in Malawi for producing high-specification titanium products, a technical qualification conducted ahead of any production commitment. Development finance institutions have adjusted their engagement posture in a similar direction, moving toward earlier collaboration agreements that allow parallel progress on financing structure and regulatory approvals rather than sequential handoffs.

Both shifts reflect a supply chain that has internalised the structural risk and is adjusting commercial and financing behaviour accordingly. Early qualification and earlier financing engagement compress development timelines at the margin. They do not resolve the underlying supply gap that the development pipeline cannot address within the projected timeframe.

Why the Pipeline Cannot Keep Pace with the Deficit

Despite policy urgency and early commercial engagement, no near-term development pipeline exists for natural rutile that could materially offset the projected 7% annual supply decline. The constraint is partly geological. Deposits with the scale, grade, and geometry to support large-scale, long-life operations are rare, and the concentration of known mineralisation in regions with declining output from established operations narrows the field of credible candidates further.

Development timelines impose a separate floor on how quickly new supply can respond to market need. Regulatory, environmental, and financing processes for a project of meaningful scale cannot be compressed below a multi-year minimum regardless of downstream urgency. A project entering the definitive feasibility study phase today faces a sequence of permitting, financing mandates, construction, and commissioning that places first production several years away at the earliest. The TZMI projections describe a deficit that deepens across that entire window before any new supply arrives.

The absence of a terminal market for natural rutile compounds the financing challenge. Rutile pricing is negotiated bilaterally, referenced to specification and end-use application rather than a published benchmark. Lenders structuring project finance for a new development require contracted revenue sufficient to support debt service modelling across the life of a facility. Assembling that contracted base requires completing multiple bilateral offtake negotiations in parallel with regulatory and study work, each on its own commercial timeline. That coordination requirement adds duration to an already extended development process.

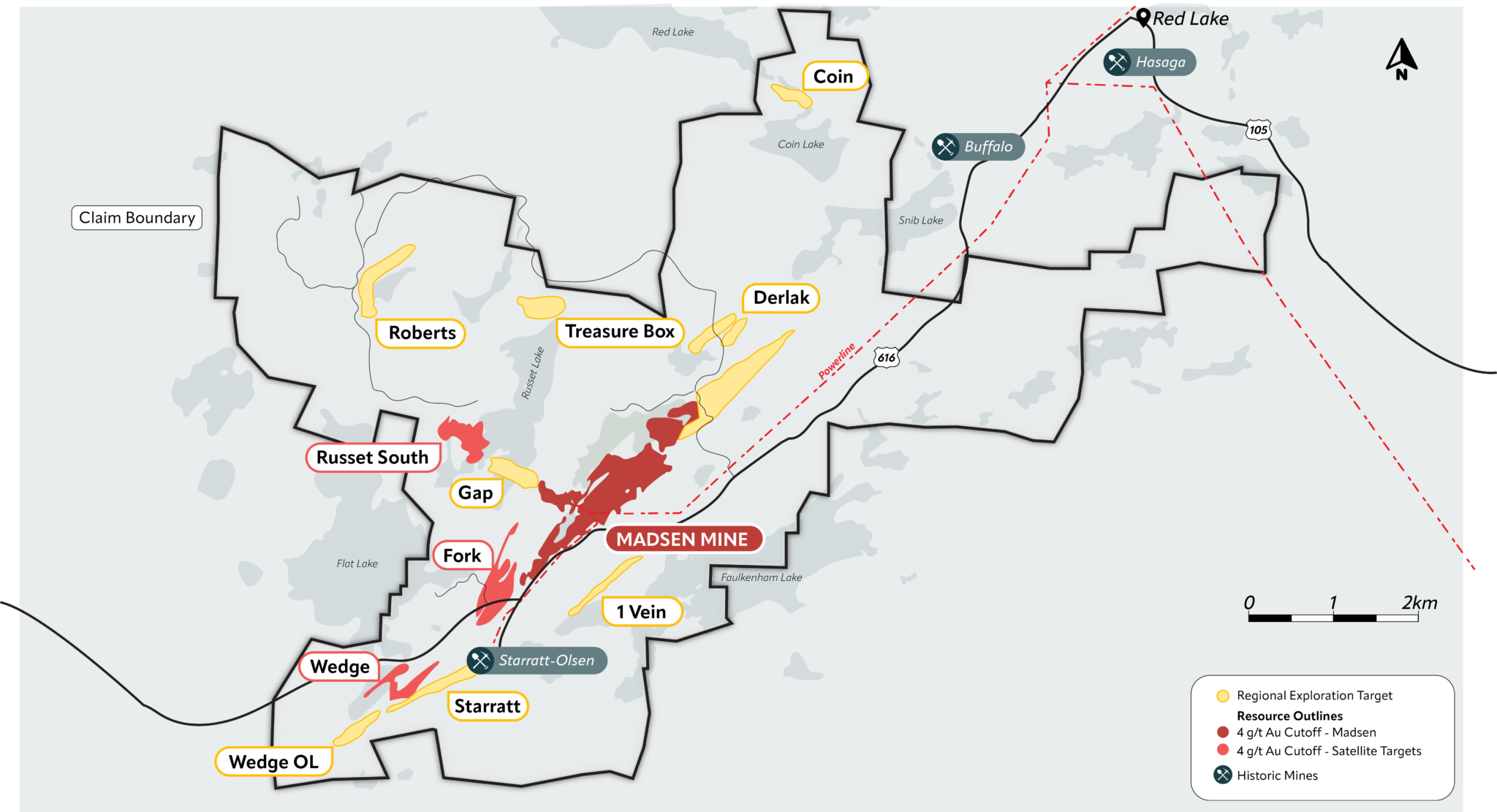

Kasiya's Position in a Thin Development Pipeline

The Kasiya Rutile-Graphite Project in Malawi, developed by Sovereign Metals (ASX: SVM; AIM: SVML; OTCQX: SVMLF), is a large-scale candidate in the current development pipeline for addressing the structural rutile deficit. A March 2026 mineral resource estimate (MRE) update established total contained rutile of 20.24 million tonnes across 2,105 million tonnes of mineralization, with 1,652 million tonnes of Measured and Indicated mineralization, representing 77% of the resource base, holding 16.1 million tonnes of contained rutile. A first Measured Resource of 107 million tonnes, designated for the first six years of planned operations, provides the highest confidence classification available under the Joint Ore Reserves Committee (JORC) code at the portion of the mine schedule that lenders and offtake counterparties evaluate most closely.

Managing Director and Chief Executive Officer of Sovereign Metals, Frank Eagar, addressed the project's position in the current supply context:

"Kasiya remains unmatched globally as a source of natural rutile, and this MRE update reinforces its potential as a long-life, low-cost supplier to critical global supply chains."

Mineralisation at Kasiya occurs in shallow, soft saprolite requiring no drilling, blasting, crushing, or grinding, which compresses the operating cost base relative to hard-rock alternatives. The resulting rutile concentrate grades above 95% titanium dioxide with a low impurity profile consistent with the requirements of Japanese titanium producers. The Optimised Pre-Feasibility Study completed in January 2025 models steady-state rutile production of approximately 246,000 tonnes per year. In March 2026, Sovereign Metals signed a memorandum of understanding (MOU) with Mitsui & Co., Ltd. covering up to 70,000 tonnes per year, following Toho Titanium's prior product qualification. Rio Tinto's 19.9% strategic stake and a collaboration agreement with the International Finance Corporation (IFC) on project finance reflect institutional recognition of the project's position in the supply chain.

How Jurisdiction Shapes the Supply Response

Established rutile production is concentrated in southern Africa and Australia, and no significant new operations in those jurisdictions are expected to offset the projected supply decline within the decade. Africa holds the largest concentration of undeveloped rutile mineralisation. Malawi's Kasiya is currently the most advanced large-scale project on the continent, operating in a jurisdiction with defined regulatory processes, relative political stability, and proximity to the Nacala corridor rail and port infrastructure that reduces logistical complexity relative to more remote deposits.

Malawi's regulatory environment requires full environmental and social impact assessment processes before a mining licence application can advance, a sequence that takes years to complete for a project operating across 201 square kilometres of agricultural land. That timeline is not unique to Malawi. Any new rutile project of scale, wherever located, faces an equivalent regulatory commitment. The difference across jurisdictions is the predictability of that process and the presence of infrastructure that reduces development cost once approvals are in hand.

The policy frameworks announced by the United States, European Union, and Japan in early 2026 create a financing advantage for projects in politically aligned jurisdictions. Malawi's engagement with Western-oriented development institutions, including the IFC's active involvement in the Kasiya project, positions that development within the scope of those frameworks. Projects in jurisdictions with contested regulatory environments or opaque governance do not carry the same access to policy-supported financing channels, which reinforces the relative position of politically stable, infrastructure-accessible deposits in the development pipeline.

A Deficit That Policy Frameworks Cannot Mine

The structural imbalance in natural rutile is not a temporary disruption that market mechanisms will resolve on a short cycle. Demand from the titanium metals industry is growing against a contracting supply base, and the development pipeline for new rutile sources is too thin and too slow-moving to close the gap within the timeframe that TZMI's projections describe. Policy commitment from the world's largest titanium-consuming nations signals the political weight now attached to supply chain security, but it does not accelerate the geological, regulatory, and commercial work that any new producing operation requires.

The practical consequence for the mining industry is that projects capable of credibly addressing the deficit carry a strategic value that goes beyond their project economics. A new rutile source of scale would be entering a market with a documented structural need for exactly what it produces, at a point when those same governments have committed policy and capital to diversifying supply. That does not change the execution requirements. It does change the institutional and commercial environment within which those requirements are navigated.

TL;DR

Natural rutile, the highest-grade titanium feedstock, faces a structural supply deficit as demand from the titanium metals industry grows at 3% annually while global supply contracts at 7% per year, according to TZMI. No credible development pipeline exists to close that gap within the projected timeframe. Sovereign Metals' Kasiya Rutile-Graphite Project in Malawi is a large-scale candidate, with a March 2026 MRE confirming 20.24 million tonnes of total contained rutile, Toho Titanium product qualification, a Mitsui MOU covering up to 70,000 tonnes per year, a 19.9% Rio Tinto stake, and active IFC engagement on project finance. Policy coordination among the United States, EU, and Japan is improving the financing environment for aligned projects but cannot substitute for the geological, regulatory, and commercial work that new production requires.

FAQs (AI-Generated)

Demand for rutile from the titanium metals industry is forecast to grow 3% annually over the next decade while global supply is expected to decline by 7% per year, according to TZMI. Geologically rare deposits and multi-year development timelines mean new supply cannot respond quickly enough to offset the shortfall.

Natural rutile typically exceeds 95% titanium dioxide content, which reduces processing costs, slag volumes, and environmental impact at the smelting and refining stage. Switching to lower-grade material is technically possible in some applications but carries cost and quality penalties that producers of high-specification aerospace, defence, and medical alloys are not prepared to absorb.

Kasiya holds a March 2026 MRE of 20.24 million tonnes of total contained rutile, with a first Measured Resource designated for the first six years of operations providing the highest JORC confidence classification. Shallow, soft saprolite mineralisation eliminates drilling, blasting, crushing, and grinding, compressing the operating cost base relative to hard-rock alternatives.

Toho Titanium completed a product qualification of Kasiya rutile ahead of any production commitment, and Mitsui signed an MOU covering up to 70,000 tonnes per year. The IFC has entered a collaboration agreement on project finance, reflecting a broader shift toward earlier engagement by development finance institutions.

Policy frameworks announced by the United States, EU, and Japan in early 2026 improve the financing environment for projects in politically aligned jurisdictions and signal the strategic priority now attached to supply chain security. They do not, however, accelerate the geological, regulatory, and commercial work that any new producing operation requires before first production.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed