Sovereign Metals: Kasiya Advances as Permitting, Financing, & Offtake Define Next Steps

Sovereign Metals lifted Kasiya resources 38% and signed a Mitsui rutile MOU, but permitting, financing, and binding offtake remain key hurdles.

Sovereign Metals (ASX: SVM; AIM: SVML; OTCQX: SVMLF) closed the first quarter of 2026 with two material announcements: a Memorandum of Understanding (MOU) with Mitsui & Co., Ltd. for up to 70,000 tonnes per year of natural rutile concentrate, and a mineral resource estimate update that lifted Measured and Indicated tonnage 38% to 1,652 million tonnes, declaring a first Measured Resource of 107 million tonnes designated for the first six years of planned operations.

The project still requires a mining licence from Malawi's regulatory authorities, a project finance package structured around US$665 million in capital expenditure (capex), and contracted offtake volumes sufficient to underwrite that financing. Each of those requirements involves external parties, defined processes, and timelines that cannot be compressed solely through geological work.

Why Permitting Is Not Just a Procedural Step

In many project discussions, the instinct is to treat permitting as administrative work that follows the technical work. Kasiya spans 201 square kilometres of the Lilongwe Plain and carries a capital requirement of US$665 million, placing it in a category where regulatory approval is a gating condition on financing, not a formality that follows it. At Kasiya's scale, that framing is misleading. Malawi's regulatory sequence requires the completion and submission of a full Environmental and Social Impact Assessment (ESIA) before a mining licence application can advance. That assessment encompasses environmental baseline data, hydrological studies, community consultation, evaluation of acid mine drainage through kinetic leach testing, and engagement with multiple government agencies. Baseline specialist studies have now been completed, informing the project design as modifying factors. Completion of fieldwork is not the same as submission, and submission is not the same as approval.

Kasiya's in-situ sulphide levels fall below the standard acid-generating threshold. However, the absence of meaningful neutralising capacity means kinetic testing is still required to validate drainage behaviour over the life of the mine. Because kinetic testing models drainage behaviour over years and decades rather than at the point of extraction, results indicating risk at any stage of operations require mitigation planning that feeds back into both the mine design and the ESIA. If mitigation requirements are substantive, they carry capital cost implications that must be reflected in the definitive feasibility study (DFS).

The pit design has already been adjusted to avoid direct community impact, indicating that the baseline process has identified real constraints. The broader engagement involves a project operating across one of Malawi's most agriculturally productive areas. The quality and depth of that engagement will determine how smoothly the regulatory review proceeds. A licence application submitted but contested extends the timeline in ways that are difficult to model in a development schedule.

What Still Needs De-Risking

Project financing at the scale Kasiya requires does not begin in earnest until a specific set of preconditions is met. Understanding those preconditions clarifies what the International Finance Corporation (IFC) collaboration agreement actually represents at this stage and what remains to be done before it can translate into a committed facility.

A bankable feasibility study with independently verified cost estimates, a mining licence or a credible regulatory pathway to one, and a contracted revenue base sufficient to model debt service coverage ratios across the life of the financing is a must in evaluating a project of this size. The current DFS will produce the first of those inputs. The mining licence process addresses the second. The offtake programme addresses the third. All three need to be substantially advanced before a formal financing mandate can be structured.

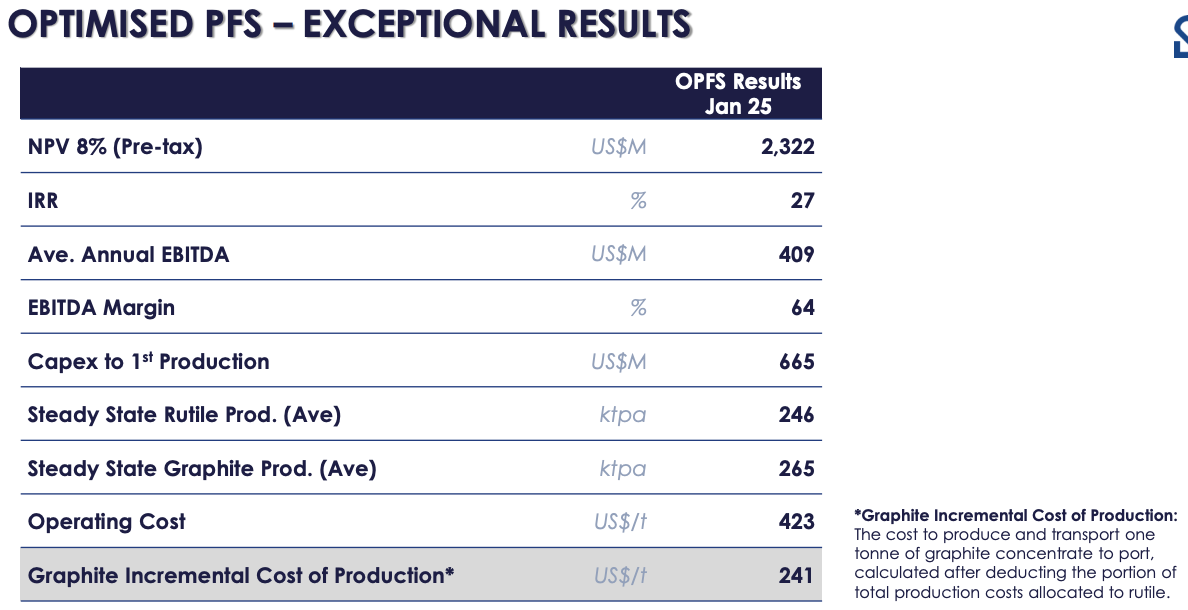

The Optimised Pre-Feasibility Study (OPFS) models a pre-tax net present value at an 8% discount rate (NPV8%) of US$2,322 million and an internal rate of return (IRR) of 27%. Those figures are based on long-term graphite basket, and rutile received prices of US$1,290 and US$1,490 per tonne, respectively. The DFS will reset those assumptions, and the direction of any revision to the US$665 million capital estimate is a critical unknown that will not be resolved until the study is complete. An increase in that figure raises the financing threshold and affects debt service modelling across the life of the project.

The path to funded development follows a defined sequence: mining licence application, ESIA submission, regulatory approval, and then transition to committed financing and offtake. Each step depends on the one before it, and slippage in any workstream carries downstream consequences for the others. The IFC collaboration agreement is a meaningful signal of institutional engagement. It is not a substitute for the regulatory and commercial conditions that lenders require before committing capital at this scale.

The Structural Difficulty of Placing Kasiya's Production at Scale

The offtake challenge at Kasiya is not primarily about finding offtake partners. It is about the structural characteristics of the markets into which Kasiya's production must be placed. At steady state from year six, the project is modelled to produce approximately 246,000 tonnes of rutile per year and approximately 265,000 tonnes of graphite per year. The Mitsui MOU covers up to 70,000 tonnes of rutile per year, and a separate agreement with Traxys, a company selected for the US government's Project Vault critical minerals supply programme, covers up to 80,000 tonnes of graphite per year. Both are non-binding. Both rutile and graphite are commodities without terminal markets, meaning full placement requires concluding multiple separate bilateral negotiations across different geographies and end-use segments, each on its own timeline.

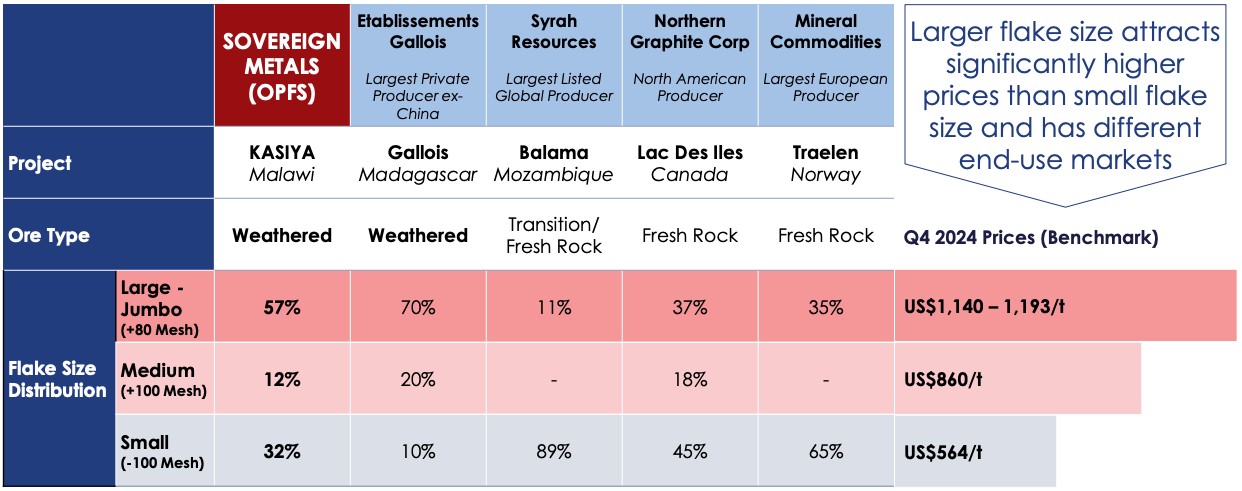

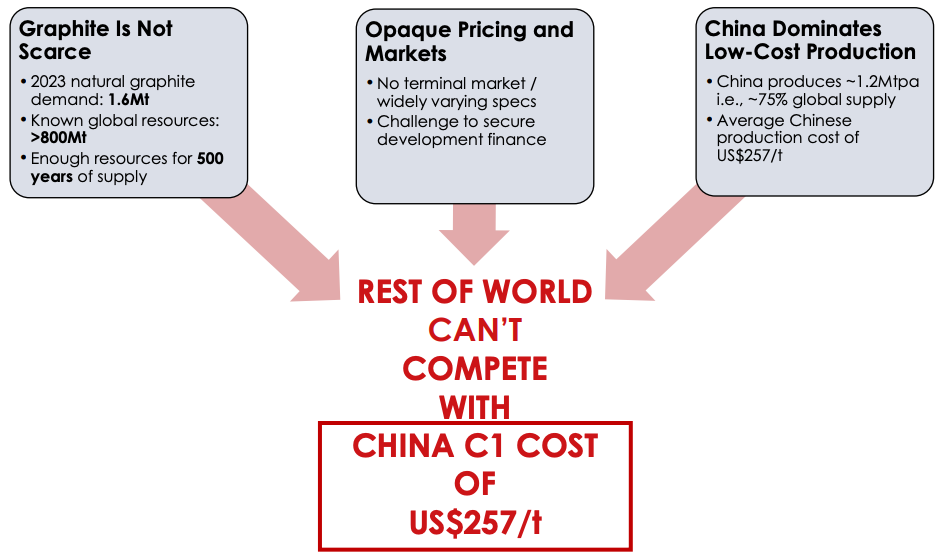

Graphite introduces an additional layer of complexity. Kasiya's flake-size distribution, with 57% in the large-to-jumbo category, positions its concentrate toward the refractory, expanded graphite, and expandable graphite markets rather than the battery anode market. Large- to jumbo-flake graphite achieved benchmark prices of US$1,140 to US$1,193 per tonne in the fourth quarter of 2024, compared with US$564 per tonne for small-flake battery anode material. That pricing differential is commercially meaningful, but the refractory and expanded graphite markets together represent approximately 31% of global natural graphite demand by volume. Placing approximately 265,000 tonnes per year into those segments requires Kasiya to capture a substantial share of existing market demand, not simply supply a growing demand pool. The incremental graphite production cost of US$241 per tonne sits below China's weighted average of approximately US$257 per tonne.

Managing Director and Chief Executive Officer of Sovereign Metals, Frank Eagar, is direct about what that cost position means competitively.

“They can't compete at that price. So we almost have the ability to take Chinese market share, with that operating cost.”

The current offtake position covers a portion of projected steady-state output. The Mitsui MOU accounts for up to 70,000 tonnes of rutile per year, and the Traxys agreement covers up to 80,000 tonnes of graphite per year, against steady-state production targets of approximately 246,000 tonnes and approximately 265,000 tonnes respectively. Both agreements are non-binding. The remaining production volume still requires placement, and further bilateral negotiations are ongoing across different geographies and end-use segments.

What to Watch Next

The DFS completion is the single most consequential near-term milestone. Eagar puts the expected timeline plainly.

“We're hoping to get that done within the next quarter. Or in the next two quarters, I would say.”

Its outputs, updated capital costs, a refined mine plan built on the upgraded resource base, and detailed environmental and social study findings, will determine how the financing and permitting workstreams can realistically proceed.

On permitting, the transition from completed fieldwork to a formal ESIA submission is the near-term indicator to monitor. Once submitted, the regulatory review timeline in Malawi will begin to define the outer boundary of when a mining licence could realistically be in hand.

Commercially, the pace at which the Mitsui and Traxys MOU moves toward binding agreements, and whether additional counterparties are added for the unplaced production volumes, will indicate whether the commercial programme is keeping pace with the project's financing requirements. The proportion of production under binding agreement at the point when DFS and regulatory work converge will be the defining commercial input to the financing conversation.

FAQs (AI-Generated)

Sovereign Metals updated its mineral resource estimate, lifting Measured and Indicated tonnage 38% to 1,652 million tonnes and declaring a first Measured Resource of 107 million tonnes for the initial 6 years of planned operations. The company also signed an MOU with Mitsui & Co., Ltd. for up to 70,000 tonnes per year of natural rutile concentrate.

The project still requires a mining licence from Malawi's regulatory authorities, a project finance package structured around US$665 million in capex, and contracted offtake volumes sufficient to support that financing. These risks are regulatory, financial, and commercial in nature and cannot be resolved through further geological work.

The DFS will produce updated capital cost estimates, a refined mine plan based on the upgraded resource, and detailed environmental and social findings. Its outputs will directly shape both the financing structure and the permitting timeline, making it the single most consequential near-term milestone for the project.

Kasiya's graphite concentrate is positioned toward the refractory, expanded, and expandable graphite markets, where large- to jumbo-flake material commands significantly higher prices than battery anode material. However, those markets represent approximately 31% of global natural graphite demand by volume, meaning Kasiya would need to capture a substantial share of existing demand to place its full projected output of approximately 265,000 tonnes per year.

The IFC collaboration agreement signals meaningful institutional engagement with the Kasiya project, but it does not represent a committed financing facility. A formal financing mandate will require a completed bankable feasibility study, a mining licence, or a clear regulatory pathway.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed