Section 232 Designation: How US Trade Policy Is Repricing Uranium as a Strategic Asset

US Section 232 designation elevates uranium to strategic asset status as spot prices exceed $100/lb, reshaping investment dynamics for domestic producers.

- The January 2026 US Section 232 proclamation formally classifies reliance on foreign critical minerals, including uranium, as a national security risk, establishing a policy framework that structurally alters pricing dynamics for domestic supply.

- Spot uranium has exceeded $100/lb while term contract prices reached $88/lb, the highest levels since May 2008, materially improving net present values and internal rates of return across permitted North American assets.

- Kazakhstan's December 2025 amendment to its subsoil code tightens state control over uranium exploration, constraining foreign participation and reinforcing supply concentration risk that supports higher long-term incentive prices.

- AI-driven nuclear power demand and a utility contracting cycle that has undershot replacement levels for 13 consecutive years are tightening the supply-demand balance through the 2030s.

- US and Canadian uranium producers and developers with permitted assets, processing infrastructure, and strong balance sheets are positioned to capture structural pricing support under a reshored fuel cycle.

US Section 232 & the Reclassification of Uranium as a Strategic Asset

The mid-January 2026 Section 232 proclamation represents a structural policy inflection point for uranium markets. By formally declaring reliance on foreign critical mineral imports a national security threat, the United States has elevated uranium from a cyclical commodity to a strategic asset. The directive empowers the Secretary of Commerce to negotiate trade adjustments, including tariffs or import controls, creating the possibility of a durable domestic price floor that decouples US uranium pricing from global spot dynamics.

This policy evolution follows the March 2025 implementation of 25% tariffs on Canada and Mexico, from which uranium was initially exempted. The tone has since hardened, with subsequent statements reinforcing a long-term reshoring agenda across the nuclear fuel cycle. From an investment standpoint, the Section 232 designation shifts uranium pricing mechanics from purely supply-demand dynamics toward policy-supported incentive pricing, where domestic production capacity becomes strategically valuable independent of global cost curves.

The implications extend beyond headline tariffs. Section 232 authority allows for quotas, licensing requirements, and preferential treatment for domestic producers in utility procurement. For investors, this creates a framework where jurisdictional positioning becomes a primary valuation input, favoring companies with US operations, existing permits, and domestic processing capability.

Spot Prices Above $100 & Term Contract Economics

Spot uranium's move above $100/lb, peaking near $101.26, represents a technical breakout not sustained since early 2024. More significantly for project economics, term contract prices reached $88/lb, the highest level since May 2008. For uranium miners, term pricing anchors feasibility study assumptions and underpins financing decisions. While spot prices reflect transactional activity, term contracts determine the revenue profiles against which capital allocation decisions are made.

The economic impact at current price levels is material. Feasibility studies across the sector have typically used conservative price decks of $70 to $75/lb. At $88/lb term pricing, internal rates of return expand materially, net present values increase disproportionately due to operating leverage, financing risk declines as debt coverage ratios improve, and enterprise value per pound multiples compress relative to intrinsic asset value. The effect is particularly pronounced for assets with structurally low all-in sustaining costs.

Energy Fuels, operating conventional uranium production from Pinyon Plain, has disclosed operating costs between $23 and $30/lb, providing substantial margin at current term prices. IsoEnergy's Hurricane deposit, with its 34.5% average grade across 48.6 million indicated pounds, implies structurally low unit costs that benefit disproportionately from higher realized prices. enCore Energy's Gas Hills project shows a 54.8% pre-tax internal rate of return at $87/lb in its preliminary economic assessment. ATHA Energy's high-grade Angilak discovery offers exploration-stage torque to rising price decks.

The margin expansion at current prices is transforming cash flow profiles across US producers. Mark Chalmers, Chief Executive Officer of Energy Fuels, frames the commodity economics:

"We've said that our costs of Pinyon are between $23 to $30 per pound, if you're selling at $75 a pound plus you got a really nice margin. If you multiply that times a million and a half pounds or two million pounds, that's a lot of cash coming into the company."

Kazakhstan's Policy Shift & Jurisdictional Risk Reallocation

Kazakhstan produces approximately 38% of global uranium supply, making its policy decisions structurally significant for market balance. The December 2025 amendment to its subsoil code materially tightens state control over uranium exploration, giving Kazatomprom priority rights to new exploration blocks. Foreign partners may be forced to relinquish discoveries or accept minority stakes compressed toward 10%, fundamentally altering the risk-reward profile for greenfield investment in the jurisdiction.

The implications for supply growth are constrained. Reduced foreign direct investment into Kazakh exploration limits the pipeline of future production that has historically anchored global supply projections. This supply concentration risk supports higher long-term incentive prices required to bring on new production in alternative jurisdictions and reinforces the geopolitical premium for assets in politically secure supply chains.

Capital is responding to this reallocation. IsoEnergy maintains assets across Canada, Australia, and the United States. Energy Fuels operates in the US, Australia, and Brazil. enCore Energy is exclusively US-focused with fully licensed processing facilities. ATHA Energy holds its 7 million-plus acre land package entirely within Canada. Jurisdiction now directly influences valuation multiples, financing access, and offtake counterparty interest.

The strategic value of district control in stable jurisdictions is becoming increasingly apparent. Troy Boisjoli, Chief Executive Officer, highlights ATHA Energy’s jurisdictional advantage:

"We're a group that not only has discovery success, but from a unique perspective we're in control of an entire district, we're in control of an entire subbasin."

AI Demand Growth & the Utility Contracting Deficit

Uranium demand is no longer driven solely by traditional utility procurement cycles. AI hyperscalers including Amazon, Google, and Microsoft are entering long-term nuclear power agreements to secure reliable baseload electricity for data center operations. This demand segment introduces buyers with investment horizons and capital discipline distinct from regulated utilities, accelerating contracting activity and tightening forward supply availability.

Uranium demand has risen 17% over the past five years. Meanwhile, 2025 marked the thirteenth consecutive year of utility contracting below replacement levels. While fourth quarter 2025 saw 72 million pounds contracted, this activity represents catch-up procurement rather than structural overcoverage. 2026 is shaping up as a forced contracting year, with utilities facing inventory depletion and limited optionality on timing. This demand durability shifts the investment cycle from speculative momentum to structural supply deficit.

Operational execution in this environment requires disciplined capital allocation and production expansion capability. William Sheriff, Executive Chairman, quantifies the enCore’s operational progress:

"Our production rate on a daily basis has gone depending on what time frame you're measuring it against from up 200% to up 300%... We went from roughly a little over seven days average of getting a production or injector well into just about 1.3 now and that metric is rather profound. ."

Institutional Capital Flows & the Physical Trust Mechanism

The Sprott Physical Uranium Trust raised $386.5 million in the first 28 days of 2026, demonstrating sustained institutional appetite for physical uranium exposure. The trust mechanism creates a self-reinforcing dynamic: capital inflows fund physical uranium purchases, removing pounds from the spot market, tightening available supply, driving price appreciation, and attracting further institutional allocation. This flywheel effect has proven durable across multiple market cycles.

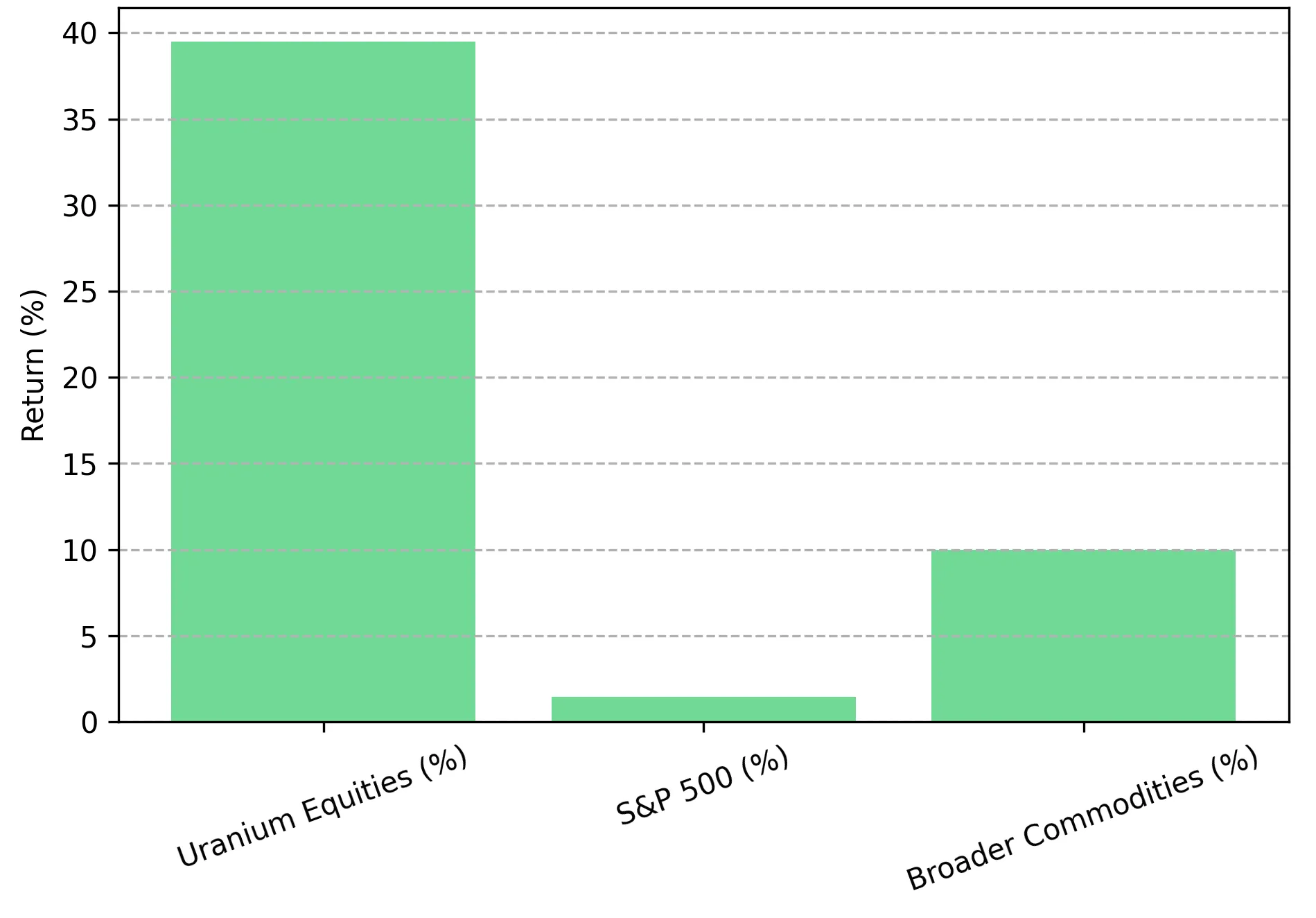

Equity markets have responded accordingly. Uranium mining equities surged approximately 39.49% in January 2026, materially outperforming the S&P 500 at 1.45% and broader commodities at 10%. This performance differential signals institutional capital rotation into upstream uranium exposure. The sector is transitioning from a retail-driven speculative vehicle to an institutional allocation receiving structured capital flows.

Asset Quality Differentiation in a Higher Price Regime

Not all uranium assets benefit equally from higher prices. The current pricing environment rewards structural cost advantages, high-grade scarcity value, and exploration torque differently across the development spectrum. Producers with established operations and low all-in sustaining costs capture immediate margin expansion. Developers with permitted high-grade deposits see net present value accretion that improves financing terms. Explorers with discovery potential offer leveraged exposure to continued price appreciation.

Producers with Structural Cost Advantages

Energy Fuels operates the White Mesa Mill in Utah, the only fully licensed and operating conventional uranium mill in the United States. With over 8 million pounds of licensed annual capacity, the mill provides toll-milling optionality that eliminates new mill capital expenditure requirements for regional producers. Pinyon Plain production costs between $23 and $30/lb create substantial margin at current term prices. enCore Energy operates two fully licensed central processing plants at Alta Mesa and Rosita with combined 2.8 million pound total design capacity. With less than 50% of production contracted, the company maintains exposure to spot market upside while generating revenue to fund expansion.

Balance sheet strength provides operational flexibility during expansion. William Sheriff, Executive Chairman of enCore Energy, describes the capital structure:

"The cost of capital is something we've never seen before in terms of a five and a half percent coupon on a non-secured note… It gives us unparalleled flexibility, doesn't tie our hands as to what we can do in terms of pursuing other business relationships… We did $115 million that was upsized from $75 million and we were still significantly oversubscribed. "

Developers with High-Grade Scarcity Value

IsoEnergy's Hurricane deposit contains 48.61 million indicated pounds at 34.5% U3O8, representing the highest-grade undeveloped uranium deposit globally. The grade implies structurally low all-in sustaining costs that compress development risk at current price levels. The company's Tony M restart pathway through White Mesa access eliminates three to five years of permitting delay typical for greenfield conventional operations.

Exploration Torque to Price Upside

ATHA Energy controls over 7 million acres across Canadian uranium districts, including the Angilak deposit with a 2013 historic mineral resource estimate of 43.3M lbs at an average grade of 0.69% U3O8. The company has invested C$115 million into its exploration portfolio with strong institutional backing, providing runway for systematic district exploration.

Balance Sheet Capacity & Capital Discipline

Strong treasuries reduce dilution risk during expansion and provide flexibility for opportunistic acquisitions. Energy Fuels maintains approximately $625 million in liquidity following a $700 million convertible raise at a 0.75% coupon, demonstrating institutional confidence in the business model. IsoEnergy holds approximately C$151.2 million cash plus C$62.3 million in equity holdings from asset divestitures. enCore Energy generates revenue while expanding drilling capacity to 30 rigs.

Companies able to self-fund drilling, final investment decisions, and restart studies will capture market share during the contracting acceleration phase. Dependency on external financing during tight credit conditions represents execution risk that current balance sheet strength mitigates.

Capital market access validates strategic positioning. Mark Chalmers, Chief Executive Officer of Energy Fuels, describes the financing dynamics:

"People saw the convertible note which had a coupon of three-quarters of a percent. The attention we got from doing that convert and this quantum that we secured to $700 million got a lot of attention."

Permitting Timelines & Policy Alignment as Valuation Inputs

Section 232 signals policy support for domestic production, but permitting timelines remain a binding constraint on supply response. Shorter permitting windows and existing infrastructure create competitive advantages that policy support alone cannot replicate. White Mesa Mill's 40-plus years of operating history, fully licensed in-situ recovery plants in Texas, and Wyoming ISR districts with historic production exceeding 100 million pounds represent permitted capacity that can respond to market conditions within operational rather than regulatory timeframes.

Permitting risk is now a valuation input. Assets with clear regulatory pathways command premium multiples relative to resources requiring extended approval processes. The combination of policy support, existing permits, and processing infrastructure creates a narrower funnel of investable assets than headline resource inventories suggest.

The Investment Thesis for Uranium

- Section 232 redefines uranium as a strategic asset, establishing policy support for domestic pricing premiums and production incentives.

- Spot uranium above $100/lb and term contracts at $88/lb validate pricing momentum and improve project economics across the development spectrum.

- Kazakhstan's supply tightening raises the geopolitical premium for Tier-1 jurisdiction assets with secure supply chain positioning.

- AI-driven nuclear demand introduces new buyer categories with long-duration contracting requirements that support forward pricing.

- Physical uranium trust institutional flows create spot market scarcity through a self-reinforcing capital allocation mechanism.

- Producers with low all-in sustaining costs capture immediate margin expansion at current realized prices.

- Developers with high-grade deposits and permitted pathways offer enterprise value per pound re-rating potential as financing risk declines.

- Explorers with district-scale land positions provide leveraged exposure through discovery cycles in secure jurisdictions.

- Balance sheet strength across the sector reduces dilution risk and provides flexibility for opportunistic consolidation.

The January 2026 Section 232 proclamation marks a turning point in uranium's investment framework. Supply concentration risk centered on Kazakhstan, contracting deficits extending into their fourteenth year, AI-driven demand growth, and institutional capital flows are aligning simultaneously. Uranium is no longer trading solely on commodity cyclicality. It is being repriced as a strategic national security input with policy support that creates pricing floors independent of global cost curves.

The key variables are jurisdictional positioning, asset grade and cost structure, permitting visibility, balance sheet strength, and contracting leverage. Companies positioned within secure supply chains and capable of delivering pounds into a tightening market are likely to command premium valuations as the policy-driven cycle progresses. The difference between assets with clear execution pathways and those facing regulatory or financing constraints will determine capital allocation outcomes across the sector.

TL;DR

The January 2026 Section 232 proclamation formally classifies foreign uranium dependence as a national security threat, shifting pricing mechanics from pure supply-demand dynamics toward policy-supported domestic incentive pricing. Spot uranium exceeded $100/lb while term contracts reached $88/lb, the highest since May 2008, materially improving project economics across permitted North American assets. Kazakhstan's December 2025 subsoil code amendment constrains foreign participation, reinforcing geopolitical premiums for Tier-1 jurisdiction assets. AI hyperscaler demand for nuclear baseload power and 13 consecutive years of utility under-contracting are tightening the supply-demand balance through the 2030s. Producers with low costs, permitted infrastructure, and strong balance sheets are positioned to capture structural pricing support.