South Africa's Mine Closures Deepen the Platinum Deficit: Can New Supply Close the Gap?

South Africa's mine closures and limited new PGM supply keep the platinum deficit intact, strengthening the case for geographically diversified supply.

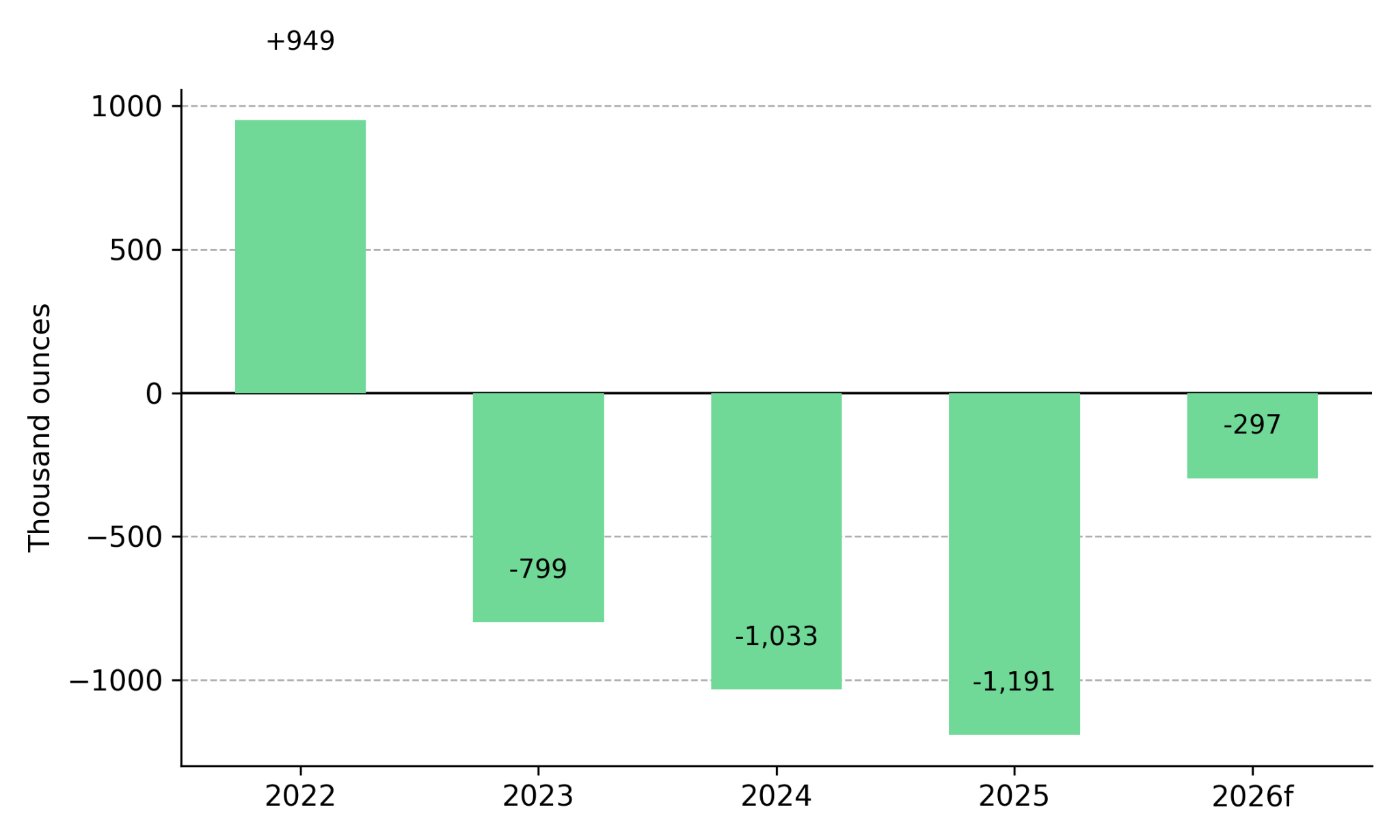

- The World Platinum Investment Council (WPIC) forecasts a fourth consecutive annual platinum deficit of 297,000 ounces in 2026, reducing above-ground stock cover to less than three months of global demand.

- South Africa still supplies roughly 70 to 80 percent of the world's platinum and rhodium, but mine closures since 2016 have reduced production capacity, limiting the market's ability to respond to continued demand.

- New South African supply is coming mainly from brownfield expansions of existing operations, increasing output without reducing the market's reliance on a single mining jurisdiction.

- Few platinum group metal development projects exist outside South Africa, leaving geographically diversified deposits among the limited sources of potential new supply if global deficits continue.

- Platinum and rhodium face a stronger long-term demand outlook than palladium, whose autocatalyst demand continues to decline as battery electric vehicles replace internal combustion engine vehicles.

Consecutive Platinum Deficits & Constrained New Supply Leave Geographic Diversification in Focus

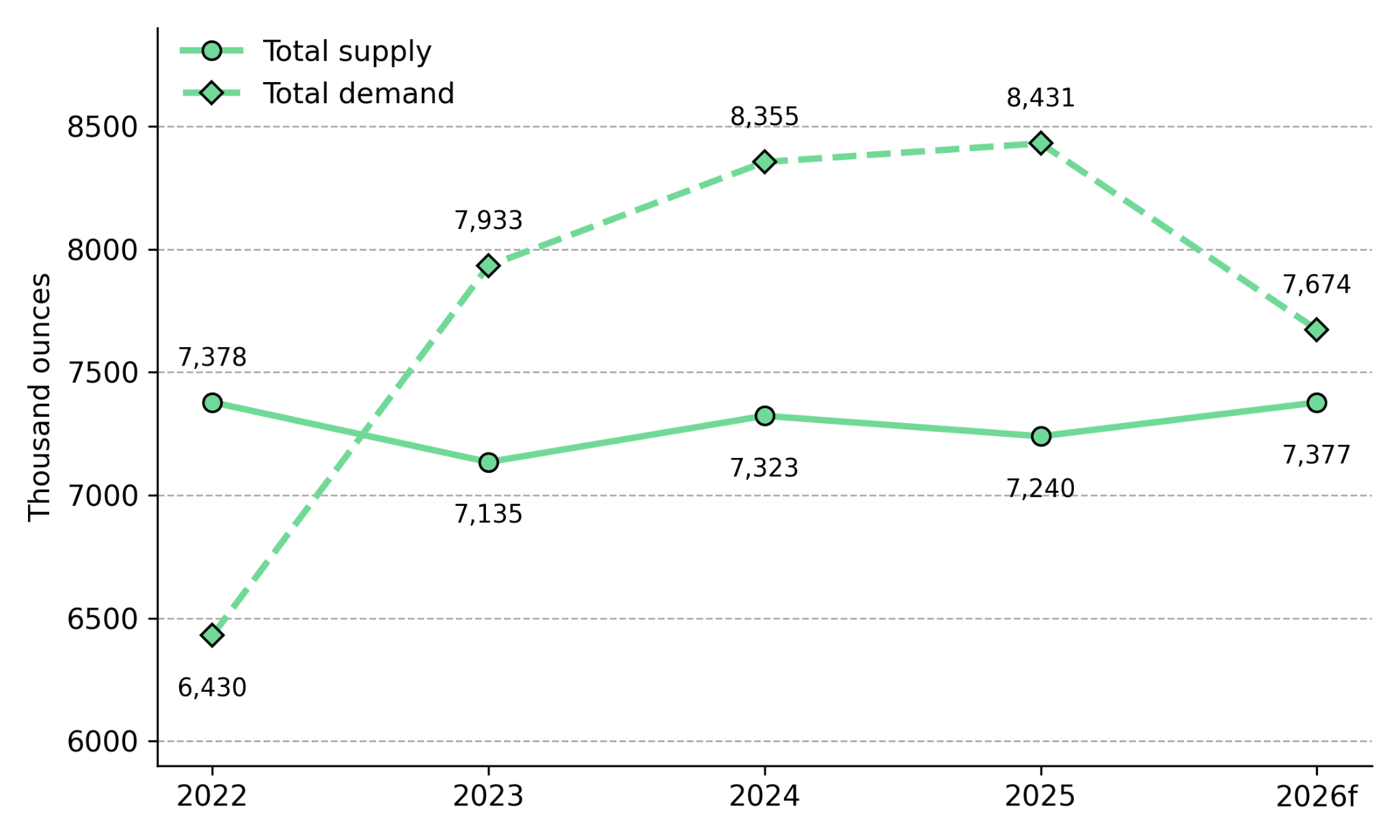

The WPIC's Q1 2026 Platinum Quarterly forecasts a 2026 platinum deficit of 297,000 ounces, marking a fourth consecutive annual shortfall. Above-ground stock cover, the stored metal available to meet demand when mine and recycled supply fall short, is expected to drop below three months of global demand by year-end. Higher prices would normally encourage new mine development and increase supply. Instead, new platinum production has remained constrained despite a fourth consecutive annual deficit.

South Africa still supplies roughly 70 to 80 percent of the world's platinum and rhodium, but its primary production base has been shrinking since 2016, limiting the market's ability to increase supply. The key issue is whether enough new PGM supply can be developed outside South Africa. Few development projects outside South Africa are capable of adding meaningful new PGM supply. The platinum deficit reflects South Africa's production constraints, the limited pipeline of new projects, and the different supply and demand outlooks across the PGMs.

Widening Platinum Deficit & Diverging Supply-Demand Outlooks Require a Metal-Specific View

The WPIC raised its 2026 platinum deficit forecast to 297,000 ounces from 240,000 ounces in its Q1 2026 Platinum Quarterly. The higher forecast assumes early-year investment outflows reverse during the second half of 2026, increasing platinum demand and widening the projected fourth consecutive annual deficit. As above-ground stock cover declines, less metal remains available to bridge short-term gaps between supply and demand. Tightening physical availability is reflected in elevated lease rates and backwardation, where near-term delivery trades at a premium to future delivery because buyers are willing to pay more for immediate access to metal.

Rhodium, like platinum, remains in market deficit but has less capacity to absorb supply disruptions. Without a formal futures market and with South Africa accounting for the large majority of global output, operational disruptions can trigger sharp price movements with limited hedging options. Palladium, by contrast, is expected to remain in surplus rather than deficit. Automakers continue substituting platinum for palladium in gasoline catalytic converters, while rising BEV adoption reduces demand for autocatalysts. Heraeus's 2026 Precious Forecast projects palladium to trade between $950 and $1,500 per ounce, reflecting weaker demand growth and available supply.

PGMs should not be viewed as a single market because each metal is driven by different supply and demand fundamentals. Platinum and rhodium remain supported by market deficits, while palladium is expected to remain in surplus as supply continues to outpace demand. In a typical commodity cycle, a deficit of this size would encourage new mine development as higher prices improve project economics. Instead, new PGM supply has remained constrained despite tighter market conditions, shifting attention to South Africa's production base.

South Africa's Aging Mines & Brownfield Expansion Keep Supply Concentrated

Several major South African platinum operations have closed or been suspended since 2016, reducing the country's production capacity despite four consecutive annual platinum deficits. The remaining mines are generally older and deeper, increasing the cost of producing additional ounces and limiting the industry's ability to expand supply through existing operations.

Brownfield Expansion Stabilizes Production, Not Supply Diversification

Sibanye-Stillwater's expansion projects show how South African producers are adding new PGM supply through brownfield developments rather than new mining districts. The company is advancing seven shallow, largely mechanized UG2 reef projects across its Rustenburg and Marikana operations, with first production targeted for March 2027. Its K4 brownfield extension is 77 percent complete, supported by a R4.4 billion capital budget, including R964 million allocated for 2026 and 2027. Even so, steady-state production is not targeted until 2033, highlighting the long lead times required to expand supply from existing operations.

Both projects expand existing South African mining operations rather than develop new mining districts. By extending mines with established infrastructure and permits, they can be developed more efficiently than greenfield projects. However, they support near-term PGM production without reducing the market's reliance on South Africa as its dominant source of supply.

Currency Moves & SARB Policy Shape South African PGM Production Costs

Exchange rate movements also affect South African platinum production costs. The rand traded near 16.49 per US dollar in mid-July after weakening over the previous month, while the SARB signaled further monetary tightening to contain inflation expectations above its target range. A weaker rand reduces US dollar-denominated operating costs for South African producers, but tighter monetary policy could offset some of that benefit by increasing financing and operating costs.

Limited Global PGM Project Pipeline & Geographically Diversified Supply Gains Value

Outside South Africa, few PGM development projects are advancing toward production. Economically significant PGM deposits are concentrated in Southern Africa, Russia, North America, and Brazil, limiting the pipeline of new supply outside those established mining regions.

ValOre Metals is advancing the Pedra Branca PGE project in Ceará State, Brazil, as an exploration-stage source of geographically diversified supply. The project hosts a 2022 NI 43-101 Inferred Resource of 2.2 million ounces of platinum, palladium and gold within 63.3 million tonnes grading 1.08 grams per tonne across seven near-surface resource zones.

Nick Smart, Chief Executive Officer of ValOre Metals, outlines platinum's constrained global supply outlook:

"You've got real structural supply constraints in a space of continued, and in many cases growing demand. Primary mine production of platinum has been in decline over the last five years, despite a metal price which has doubled over the last year. That tells you something around the inelasticity around supply and the difficulty of bringing new metal into the market."

Brazil strengthens Pedra Branca's investment case by providing a geographically diversified jurisdiction for future PGM development. The country ranks among the world's top ten gold-producing nations, generating an estimated $3.8 billion annually and targeting more than $6 billion by 2030. Brazil also combines an established mining industry, a stable regulatory framework, and a large mining engineering workforce. Together, these advantages broaden the pipeline of potential PGM supply beyond South Africa's established mining districts.

Brownfield Projects & Greenfield Development Serve Different Roles in Future PGM Supply

The South African and Brazilian development strategies serve different roles in the future PGM supply pipeline. The South African brownfield pipeline is targeting production from 2027 with lower technical risk, but it does not diversify global PGM supply. The Brazilian project has a longer development timeline but offers one of the few opportunities to expand future PGM supply outside South Africa.

A peer comparison shows how project advancement influences valuation across TSX-listed PGM developers. Market capitalizations range from about $27 million at the mineral resource stage to $440 million at the PEA stage and $389 million at the definitive feasibility study stage, indicating that project advancement can have as much influence on valuation as resource size.

Persistent Platinum Deficit & Concentrated Supply Keep Geographic Diversification in Focus

A fourth consecutive annual platinum deficit, tightening rhodium fundamentals, and a palladium market expected to remain in surplus point to the same conclusion: the PGM market is constrained by the limited availability of geographically diversified supply rather than demand. Brownfield projects within South Africa can stabilize production over the next several years, but they do not reduce the market's reliance on a single producing jurisdiction. Until a meaningful share of new PGM supply comes from outside South Africa, the deficit described by the WPIC will remain as much a function of geographic concentration as production volume.

The Investment Thesis for Platinum Group Metals

- A fourth consecutive annual platinum deficit supports a stronger platinum price floor, with the WPIC forecasting a 297,000-ounce shortfall in 2026 and above-ground stock cover falling below three months.

- Brownfield supply stabilizes production rather than diversifies supply, as South Africa's expansion projects increase output without reducing the country's roughly 70 to 80 percent share of global platinum and rhodium supply.

- Rhodium prices remain highly sensitive to supply disruptions because South Africa dominates global production and no futures market exists to absorb price shocks.

- Palladium warrants a different outlook because battery electric vehicle adoption continues to reduce catalytic converter demand, limiting upside despite South African supply constraints.

- US critical minerals policy remains a key variable as Section 232 negotiations on potential price floors and trade measures for platinum, palladium, and rhodium remain unresolved, leaving future trade policy uncertain.

- Early-stage, geographically diversified PGM projects represent future supply potential rather than today's supply solution, with a PEA marking the first stage at which the market can evaluate project economics on a comparable basis.

- This thesis would weaken if the WPIC's platinum deficit forecast moved closer to market balance or if South African brownfield projects delivered production significantly ahead of current schedules.

The platinum deficit described by the WPIC is persisting because expanding supply from South Africa's existing mines is becoming more difficult, even though the country remains the world's dominant source of platinum and rhodium. Brownfield projects extend the life of existing mining operations but do not diversify global PGM supply. The pipeline of geographically diversified PGM projects remains limited, increasing the strategic importance of early-stage deposits outside South Africa. Two developments will test that thesis over the next two quarters: whether South Africa's brownfield projects meet their targeted 2027 production schedules, and whether Pedra Branca's fourth-quarter PEA establishes the project's first economic benchmarks.

TL;DR

The WPIC forecasts a fourth consecutive platinum deficit in 2026 as South Africa's aging mines and earlier closures continue to limit the market's ability to increase supply despite higher prices. Brownfield expansions will add production but will not reduce reliance on South Africa, leaving geographically diversified PGM projects in short supply. Platinum and rhodium remain supported by supply deficits, while palladium faces weaker demand from rising battery electric vehicle adoption. The article concludes that future PGM supply outside South Africa will be the key factor determining whether the platinum deficit persists over the coming years.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed