Strong DFS Economics and Permits Support US Gold’s CK Gold Development Path

US Gold's $635M NPV CK Gold project fully permitted in Wyoming; $1.4B NPV at spot gold; 300K oz tailings upside; financing underway for 2026 development decision.

- US Gold Corp's CK Gold Project DFS shows after-tax NPV of $635M and IRR of 27% at $3,250/oz gold. At current spot prices (~$4,500/oz), NPV reaches $1.4B with 50% IRR

- Project holds all required permits including mine permit, industrial siting, and environmental approvals; permits are non-revocable under Wyoming state law, eliminating a major development risk

- Significant upside from 300,000 oz of gold in tailings (30% of production), $800M-$1B in aggregate waste rock value, and potential to add 1M oz to reserves through additional drilling

- Recovery rates at 70% (industry average 97-98%), opportunities for capex reduction through used equipment purchases, and contractor negotiations on mining costs provide optimisation potential

- Capex of $400M with strong contractor availability, received indicative term sheets for up to 80% debt financing, positioned in favourable market for mining project finance

US Gold Corp (NASDAQ:USAU) has released its definitive feasibility study for the CK (historically known as Copper King) Gold Project in Wyoming, marking a significant milestone toward production. Executive Chairman Luke Norman discussed the study's results and development pathway in a detailed interview, revealing economics that substantially improve on earlier assessments while highlighting multiple value enhancement opportunities ahead of final investment decision.

Robust Economics with Significant Gold Price Leverage

The Definitive Feasibility Study (DFS) demonstrates compelling project economics at conservative metal price assumptions. At a base case gold price of $3,250 per ounce, the project generates an after-tax net present value of $635 million and an internal rate of return of 27%. What sensitivity analysis shows that at $4,500 gold, notably below current spot prices, the NPV expands to almost $1.4 billion with an IRR approaching 50%. Norman emphasised this leverage:

"This project's so well leveraged to the price of gold, but again, at the base case price, it does tremendously well as well."

The 11-year mine life targets production of approximately 90,000 ounces gold equivalent annually, though this figure is expected to increase as copper prices have risen significantly from the base case assumptions to current levels around $6 per pound.

Capital Cost Management with Contingency Planning

Total capital expenditure is estimated at over $400 million, representing an increase from the $277 million forecast in the pre-feasibility study. This adjustment reflects more detailed engineering, current equipment costs, and the impact of tariffs on Scandinavian equipment specified in the study. Importantly, the capital estimate includes substantial contingency of approximately $40-45 million, representing roughly 17.5% of total capex. The company has identified opportunities to reduce these costs through procurement of quality used equipment currently available in the market, potentially lowering lead item costs while accelerating delivery timelines.

Operational Simplicity

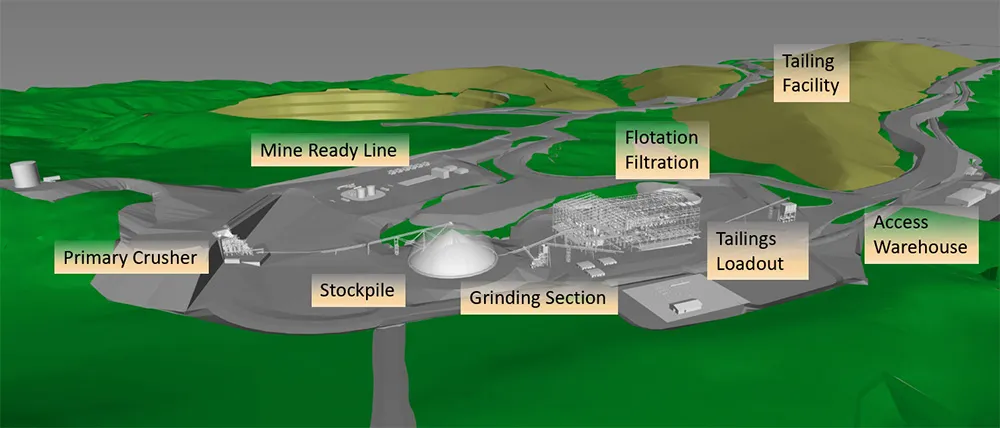

The project benefits from straightforward mining operations with ore exposed at surface and a strip ratio of less than 1:1. The metallurgical process involves crushing, grinding, and flotation to produce a high-quality copper-gold concentrate with strong international demand.

US Gold has opted for contract mining rather than building its own fleet, leveraging the abundance of heavy equipment and qualified contractors in Wyoming. This approach reduces capital requirements and operational complexity while taking advantage of local expertise. The project's location being 20 miles from an established township provides access to a stable workforce that can commute daily rather than requiring remote camp infrastructure.

Interview with Luke Norman, Executive Chairman of US Gold Corp.

Operation and Processing Enhancements

Current recovery rates stand at 70% for gold, with 30% remaining locked in tailings. The company has conducted metallurgical testing showing that adding a carbon-in-leach (CIL) circuit could increase overall recovery to 97-98%. Norman explained,

"There is close to 300,000 ounces of gold in the tailings that's not going to be left behind. It's pulverised rock sitting on a fully lined containment area."

Additionally, US Gold is exploring cyanide-free alternatives, including iodine-based processing, which is reusable and already employed at operations in Nevada. These improvements could significantly reduce all-in sustaining costs, currently estimated around $1,785 per ounce.

Waste Rock Monetisation Opportunity

The definitive feasibility study treats certain material as waste rock that actually represents high-value construction aggregate. Located near the Colorado border with strong demand from data center construction and infrastructure development, this material has an estimated in-situ value of $800 million to $1 billion under the current reserve alone.

US Gold is in discussions with potential partners, including Burlington Northern Santa Fe (BNSF), regarding aggregate sales or partnership arrangements. Monetising this resource could substantially reduce net mining costs and add significant value beyond the DFS base case.

Permitting

Perhaps the most significant de-risking element is the project's complete permitting status. US Gold holds all required federal and state permits, including mine permits, industrial siting, wastewater management, and air quality approvals. The company has already initiated construction of the access road, formally activating the mine permit.

Under Wyoming state law, these permits cannot be challenged or revoked once awarded, following public comment periods and town hall processes. Norman noted the rarity of this status:

"Permits were laid to bear to the public through 30-day periods, then rest periods and town halls and everything. The permits that are awarded to us are not reversible or revocable. We're ready to go."

This complete permitting substantially reduces development risk and timeline uncertainty that typically plague mining projects, making the project more attractive to potential financiers.

Strategic Financing Pathway to Development

US Gold has received multiple indicative term sheets over the past 18 months, including structures offering up to 80% debt financing at 20% equity, with equity priced at premiums to current market levels. The $400 million capital requirement sits in a "sweet spot" for project finance large enough to be meaningful but not requiring billion-dollar commitments.

Favourable financing conditions include fully locked-in power costs at 7.6 cents per kilowatt hour, established contractor pricing, and proximity to infrastructure. The combination of complete permitting, conservative DFS economics, and multiple value enhancement opportunities positions the company well for competitive financing terms.

The Investment Thesis of U.S. Gold Corp.

- Exceptional project economics with gold price leverage: The CK Gold Project's Definitive Feasibility Study delivers an after-tax NPV of $635 million and a 27% IRR at a conservative base case of $3,250 per ounce gold, expanding dramatically to $1.4 billion NPV and a near-50% IRR at current spot prices around $4,500 per ounce, demonstrating the project's strong torque to the prevailing gold price environment.

- Fully permitted and shovel-ready in a mining-friendly jurisdiction: US Gold Corp holds all required federal and state permits for the CK Gold Project including mine, industrial siting, wastewater, and air quality approvals with Wyoming state law rendering these permits non-revocable once awarded, eliminating the permitting risk that derails the majority of development-stage mining projects.

- Straightforward open-pit operations with a clear path to production: The project benefits from ore exposed at surface, a strip ratio of below 1:1, and a well-understood flotation process, use of contract mining and proximity to an established local workforce further reduces both operational complexity and capital requirements.

- Multiple value enhancement opportunities beyond the DFS base case: Recovery rates currently stand at 70%, but metallurgical testwork confirms that adding a carbon-in-leach circuit could lift recoveries to industry-standard levels of 97–98%, unlocking approximately 300,000 ounces of gold currently reporting to tailings and materially reducing all-in sustaining costs from their present estimate of around $1,700 per ounce.

- A billion-dollar aggregate opportunity that the market has yet to price in: Waste rock classified under the DFS as a mining cost actually represents high-quality construction aggregate with an estimated in-situ value of $800 million to $1 billion, situated near the Colorado border where data centre construction and infrastructure development are driving strong regional demand.

- Attractive and well-structured financing pathway: The $400 million capital requirement sits at a scale that is meaningful yet accessible for project finance, and the company has already received indicative term sheets offering up to 80% debt financing at a 20% equity contribution priced at a premium to current market levels.

- Significant reserve growth potential in a supply-constrained market: The company has identified the potential to add up to one million ounces to its existing reserve base through additional drilling, offering organic growth upside at a time when domestic gold production is in structural decline and fully permitted, de-risked development assets of this quality are exceptionally scarce globally.

Macro Thematic Analysis

Gold and copper are simultaneously commanding record or near-record prices for structurally distinct yet complementary reasons. Gold has been propelled to all-time highs by a confluence of monetary uncertainty, central bank accumulation, and a broad reassessment of the U.S. dollar's reserve currency status, with sovereign and institutional buyers treating the metal as a hedge against fiscal excess and geopolitical fragmentation. Copper, meanwhile, is being re-rated as an essential industrial input for the energy transition, with electrification demand from data centres, EV infrastructure, and grid modernisation driving projections of a structural supply deficit that the mining industry's decade-long underinvestment cannot quickly resolve.

US Gold Corp sits at the intersection of both thematics in a way that few development-stage companies can claim. The company's achievement of securing complete, non-revocable permits in an era of increasing regulatory complexit positions it uniquely among development-stage miners. The project addresses critical supply constraints: domestic gold production has declined while copper demand for energy transition accelerates. Wyoming's mining-friendly regulatory environment, combined with proximity to infrastructure and skilled labor, creates advantages unavailable in traditional mining jurisdictions. As Norman emphasised:

"There's a lot of money out there right now chasing mining opportunities with not a lot of projects like ours that are shovel ready, ready to go."

The convergence of favourable commodity prices, complete permitting, and strong project economics creates a compelling opportunity in a market starved for de-risked development assets.

TL;DR

US Gold Corp's CK gold project DFS delivers $635M NPV and 27% IRR at conservative gold prices, expanding to $1.4B NPV at current spot levels. The fully permitted Wyoming project (rare non-revocable status) eliminates major development risk while offering multiple value catalysts: 300,000 oz recoverable tailings gold, $800M-$1B aggregate opportunity, and potential to add 1M oz reserves. With $400M capex, strong financing interest (80% debt terms received), and simple open-pit operations, the company is positioned for near-term development decision in favourable market conditions.

FAQs (AI Generated)

The increase reflects detailed line-item engineering versus earlier permitting-focused estimates, equipment cost inflation, tariff impacts on Scandinavian equipment, and conservative contingency planning (17.5% of capex).

Contract mining eliminates $100M+ in fleet capital, leverages Wyoming's abundant heavy equipment contractors, reduces operational complexity, and provides flexibility while maintaining cost competitiveness in this location.

US Gold holds every required federal and state permit with construction already initiated. Under Wyoming law, permits are non-revocable once awarded - eliminating challenge risk that plagues most projects.

Highly realistic. The gold is in pulverised rock in lined containment. Metallurgical testing confirms 97-98% recovery using proven CIL technology, though alternative methods like iodine processing are being evaluated.

The $800M-$1B in-situ aggregate value could reduce net mining costs through partnerships with construction companies or sale to infrastructure projects, improving economics beyond DFS base case.

Analyst's Notes

Subscribe to Our Channel

Stay Informed