Thunder Gold Maps Path to 5 Million Ounces as Ontario Deposit Draws Industry Attention

Thunder Gold targets 5Moz resource and preliminary economic assessment by year-end, banking on cost discipline and conversion drilling to close valuation gap.

Wes Hansen spent 45 years building gold mines before retiring to keep bees and chickens two hours east of Toronto. Then a former colleague called about a drill dataset from a property near Thunder Bay. Hansen looked at the numbers for two days and came out of retirement.

What he saw was unusual: 180 drill holes, drilled to depths ranging from 100 to 500 metres, all returning essentially the same grade - between 0.33 and 0.37 grams per tonne gold - from collar to bottom. No matter the rock type. No matter the distance from the intrusive core. Just consistent, predictable mineralisation across a footprint that hasn't been fully tested.

"It's like the most well-behaved data set I've looked at in 45 years… [Now] this is all about how you engineer it."

That consistency is now the foundation of Thunder Gold's 2026 game plan: convert roughly 3 million inferred ounces into measured and indicated resources, expand the pit, and deliver both an updated resource estimate and a preliminary economic assessment before year-end. It's an aggressive timeline, but Hansen - who built the first heap-leach gold mine in the Yukon and managed a billion-dollar plant expansion in Brazil - isn't worried about the geology cooperating.

A Different Kind of Canadian Gold Deposit

Tower Mountain sits in an Archean greenstone belt, the same geological setting that hosts Ontario's historic gold camps. But it doesn't follow the script. Most Canadian greenstone gold deposits are narrow, high-grade veins hosted in shear zones - spectacular assays, unpredictable geometry, difficult to mine at scale. Tower Mountain is interpreted as intrusion-related, with gold distributed through a broad halo of disseminated pyrite surrounding a central intrusive body.

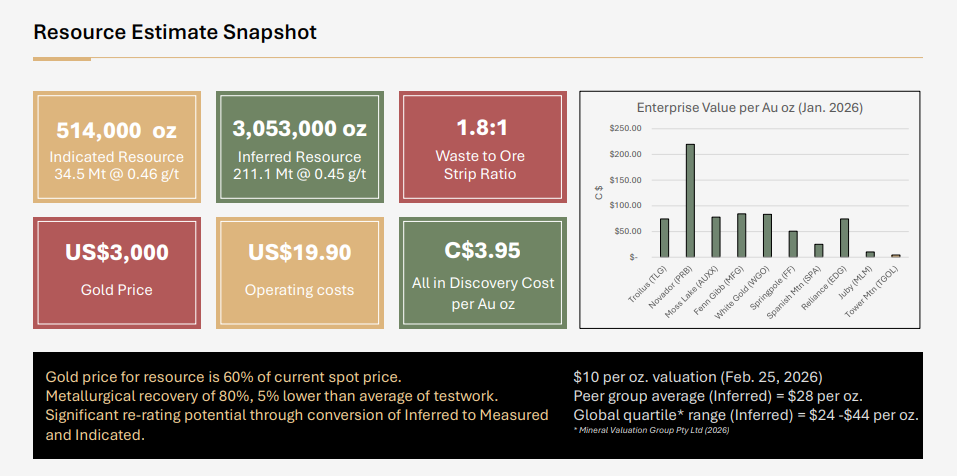

The mineralisation starts at surface and extends to depth with no meaningful grade variation. The current resource - 3.5 million ounces at a 1.8:1 strip ratio - sits entirely on the western contact of the intrusion. Three other contacts remain untested, each carrying geophysical signatures that mirror the known zone. Hansen's long-term thesis is straightforward: if the west side holds 3.5 million ounces, the other three sides probably do too. That would put the system north of 12 million ounces, though proving it will take years and capital the company doesn't yet have.

For now, the focus is tighter: prove up 5 million ounces on the western contact, wrap it in a preliminary economic assessment, and position it as a standalone starter project for a mid-tier looking to add two decades of mine life in a tier-one jurisdiction.

Forty Minutes from Thunder Bay

What makes Tower Mountain unusual isn't just the geology. It's 40 kilometres from Thunder Bay, with paved highway access, rail connections, and power infrastructure within three kilometres of the pit. Future mine employees could drive home every night. For a large-tonnage open-pit project, that's a material advantage.

Hansen's pitch is blunt: no roads to build, no transmission lines to run, no fly-in camp to staff. Ontario ranks second in Canada for mining jurisdiction (per the Fraser Institute), and the province has been working to streamline permitting. Thunder Gold isn't fighting accessibility or infrastructure - it's fighting market indifference.

The company trades at roughly $10 per ounce of resource. Peer group averages for inferred ounces sit closer to $28. The global quartile range runs between $24 and $44 per ounce. That gap represents either mispricing or skepticism, and management is betting on the former.

Part of the discount is self-inflicted. Thunder Gold has kept overhead lean and marketing minimal - PDAC, Beaver Creek, a handful of others. The focus has been on drilling, not promotion. Discovery costs have stayed at C$3.95 per ounce, well below industry averages, but the company has flown under the radar. The thesis for re-rating is simple: resource conversion. Moving ounces from inferred to indicated typically triples or quadruples the market valuation. With $5 million in treasury and 80 million warrants outstanding at 10 cents - representing a built-in $8 million financing if the share price triggers the early acceleration clause - the company has the capital to execute this year's drill program without immediate dilution.

Interview with Wes Hanson, President & CEO of Thunder Gold Corp.

Timing the Market

Hansen's return to the industry coincides with a gold price environment that has rewritten the economics of large-tonnage, lower-grade deposits. At sustained prices above $5,000 per ounce, projects carrying grades in the 0.4 to 0.6 g/t range - once marginal - now generate returns that meet institutional thresholds.

The shift is already visible in deal flow. Mid-tier and senior producers are generating record cash but facing a reserve replacement problem. The pipeline of large, permitted, shovel-ready gold projects has thinned.

"These smaller producers in the 100 to 500,000 ounce a year range - they have more cash than they've ever had and dwindling reserves. They're going to be looking for projects that give them security for 20 years or more."

Thunder Gold's strategy is to position the western contact as a standalone asset - economically viable, low-risk, build-ready - while retaining the exploration upside on the remaining contacts as future optionality. It's a package designed for a mid-tier looking to add duration without taking greenfield risk.

The Drills Are Turning

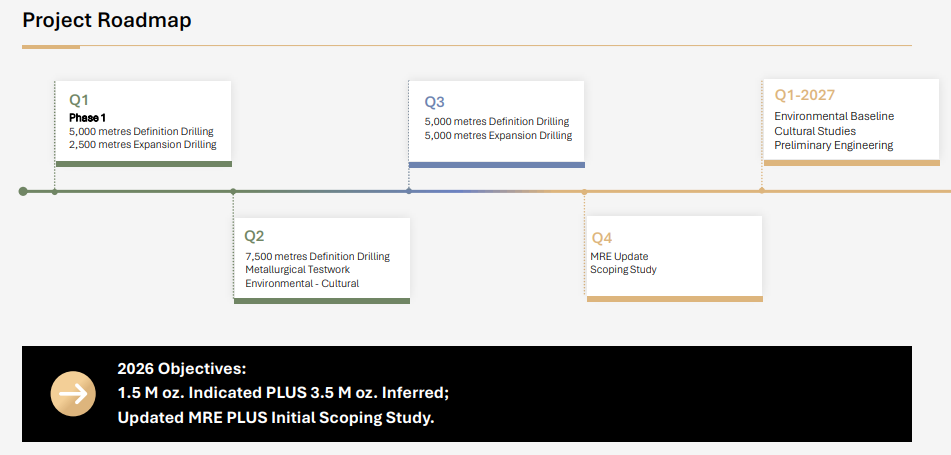

The 2026 work program front-loads 7,500 metres of infill drilling in Q1, followed by another 7,500 metres in Q2, alongside metallurgical testwork and environmental baseline studies. The goal is a Q4 resource update and PEA, giving the market its first look at project-level economics.

If the infill drilling performs, the year-end resource could hit 5 million ounces, with a significantly higher proportion in the indicated category. That would improve the valuation multiple and provide the technical foundation for a pre-feasibility study - assuming the PEA confirms viable economics.

Hansen has spent four and a half decades evaluating deposits from Nevada to Russia. He's seen high-grade narrow veins fail because they were unpredictable. He's seen low-grade bulk tonnage projects succeed because they were engineered correctly. Tower Mountain, in his view, is the latter. The geophysics are holding up. The drill results are consistent. And the path to 5 million ounces looks increasingly well-defined.

Whether the market closes the valuation gap before a strategic buyer steps in will depend on the next 25,000 metres of drilling. But the setup is clear: a large, predictable gold system in a tier-one jurisdiction, 40 minutes from a resource town, with year-round access and existing infrastructure. The kind of asset that gets harder to find every year - and the kind that cash-rich producers are starting to circle.

Analyst's Notes

Subscribe to Our Channel

Stay Informed