Undervalued? Atlas Salt 90% Valuation Discount Despite Eliminating Major Mining Risks

Atlas Salt CEO argues company trades at 0.1x NAV despite lower risks than typical mining, offering stable 25-yr cash flows to government customers with $1.9B-$3B valuation potential.

- Atlas Salt currently trades at approximately 0.1x its net asset value (NAV), which CEO Nolan Peterson argues represents significant undervaluation compared to typical mining projects at similar development stages.

- The company claims to have eliminated three major mining risks: metallurgical, block model/geology, and permitting due to the nature of salt deposits and their advanced environmental assessment approval.

- Unlike typical gold mines with front-loaded cash flows and shorter mine lives, Atlas Salt's project features more than a 25-year mine life with 50 years of defined resources, creating more stable, annuity-like cash flows.

- Peterson presents multiple valuation approaches beyond traditional P/NAV ratios, including free cash flow yield suggesting $1.9B valuation and EBITDA multiples of up to $3B valuation, contending salt companies trade differently than conventional miners.

- The project targets de-icing salt sales to North American cities and governments, which Peterson characterises as contractually or legally obligated purchasers, reducing market risk compared to commodity-driven mining projects.

Nolan Peterson, CEO of Atlas Salt, recently outlined his company's investment thesis in a detailed presentation focused on valuation methodologies for the Great Atlantic Salt Project in western Newfoundland. The project aims to become the first new salt mine built in North America in 25 years, targeting the de-icing road salt market. Peterson's central argument revolves around a fundamental disconnect between the company's current market valuation and what he views as its intrinsic value, complicated by investor unfamiliarity with the salt sector and its distinct characteristics compared to traditional precious metals mining.

Current Valuation Framework

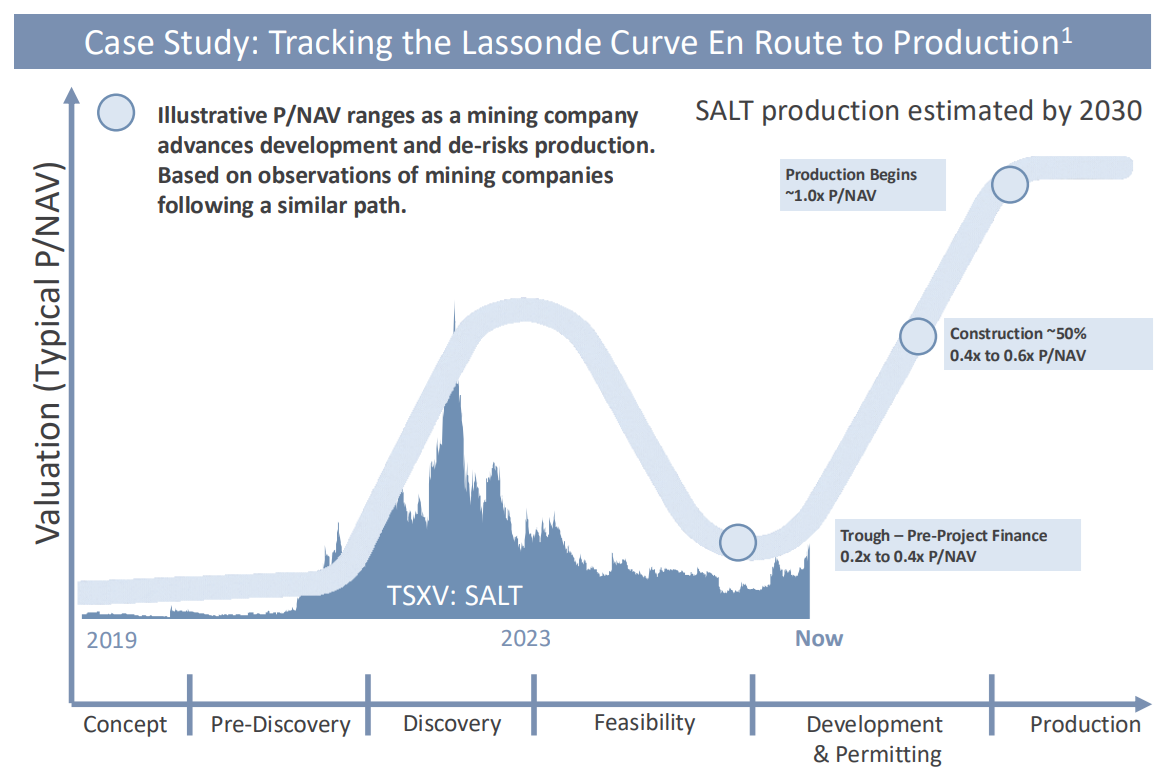

Atlas Salt (TSXV:SALT) currently trades at approximately 0.1 times its forward-looking net asset value, a significant discount that Peterson attributes to several factors. He frames this using the Lassonde Curve, a visualisation tool that maps how mining projects typically re-rate toward their intrinsic NAV as they advance through development milestones and reduce risk.

Peterson acknowledges that all mining projects face typical discount factors including execution risk, financing risk, metallurgical uncertainty, block model and geological risk, and stakeholder and permitting challenges. However, he argues that Atlas Salt has already eliminated several of these risk categories. According to Peterson, salt deposits require no metallurgical processing, are straightforward to define geologically, and the Great Atlantic project has already secured an approved environmental assessment, addressing permitting concerns. Peterson stated:

"If you remove those risks from the equation, the valuation should be much higher. We should be further advanced on the Lassonde curve as a visual representation."

Despite this risk reduction, Peterson acknowledges remaining financing and execution risks, while attributing the valuation gap to salt being a niche commodity with limited investor familiarity, lack of marketing support, and absence of comparable investment options in the sector.

Cash Flow Profile: Salt Versus Precious Metals

A substantial portion of Peterson's argument centers on fundamental differences between salt projects and typical precious metals mining operations. He presented a comparative analysis using New Found Gold's Queensway mine as a reference point for gold mining economics.

As Peterson explained, traditional gold projects exhibit front-loaded cash flow profiles with peak net present values occurring shortly after construction as capital expenditures are recouped. These projects typically feature shorter mine lives, with value declining as reserves are extracted. This creates what Peterson describes as "capital recycling," where companies continuously invest in new projects to replace depleted reserves. Additionally, commodity price volatility introduces uncertainty about future project values.

In contrast, Atlas Salt's project presents more than a 24-year mine life with a shallower decline curve in NAV over time. The company has already defined 50 years of resources through drilling, though Peterson notes these are not yet classified as reserves. The critical distinction, according to the CEO, is that mining one year of salt production does not significantly impact the project's overall NAV due to the extensive resource base and lower discount rate (NPV8 versus typical higher rates for precious metals).

Peterson argues this fundamental difference means traditional NPV-based valuation approaches may systematically undervalue salt projects:

"If you're valuing Atlas Salt just based on its NPV like you would any other resource project, you are in my view, undervaluing us."

Alternative Valuation Methodologies

Beyond traditional price-to-NAV ratios, Peterson presented several alternative valuation frameworks that he suggests are more appropriate for salt projects, given their stable cash flow characteristics.

Using Artemis Gold as a benchmark for typical resource company valuations, Peterson outlined potential value inflection points: from initial construction at 0.3x P/NAV, implying C$300M market value for Atlas, to secured project financing, construction completion, and up until commercial production approaching 1.0x P/NAV, implying C$750M.

However, Peterson argues these conventional metrics still undervalue salt projects. He points to free cash flow yield as an alternative framework more suitable for financial instruments like "coupons" or annuities that are based heavily on established cash flows or steady state cash flows. Using a 10% free cash flow yield benchmark, Peterson suggests a potential $1.9 billion valuation.

Additionally, Peterson references publicly traded salt producers that trade primarily on EBITDA multiples rather than NPV. Based on Atlas Salt's projected life-of-mine average EBITDA of $325 million and comparable trading multiples, he suggests valuations approaching $3 billion are plausible if the market applies similar methodologies. He also notes precedent transactions in the salt sector have shown heavy valuations based on EBITDA and not based on NPV or NAV.

Interview with Nolan Peterson, CEO of Atlas Salt

Market Dynamics & Customer Characteristics

A key component of Peterson's risk reduction argument centers on the nature of salt market customers and dynamics. The primary customers for de-icing road salt are municipal governments and state/provincial authorities responsible for winter road maintenance. Peterson emphasised:

"The primary customer for our salt is cities and governments. And they are, as I've said before, in many cases legally obligated to purchase salt to de-ice roads for liability reasons."

This creates what he characterises as exceptional customer quality which are entities with legal mandates to purchase the product, reducing market risk substantially compared to commodity markets.

According to Peterson, salt markets have demonstrated stability with downside risk limited by this structural demand, while upside potential exists during severe winters or supply disruptions. He noted current fuel shortages creating price pressure due to North America's reliance on imported salt. The CEO acknowledged that convincing investors of market stability takes time as it takes an education piece, but encouraged investors to conduct independent research, noting that the company's pricing model and feasibility study reflect conservative assumptions incorporating market risks.

Risk-Reward Profile & Portfolio Construction

Peterson framed the investment opportunity through a risk-adjusted returns lens, drawing on portfolio theory to argue that Atlas Salt offers superior risk-reward characteristics compared to typical resource sector investments. He stated:

"I would say that you are definitely taking on less risk with Atlas Salt, but the expected returns could be at a higher ratio than a higher risk resource sector play."

Using hypothetical units of risk and return, Peterson suggested that while Atlas Salt represents lower absolute risk than high-volatility commodity plays, the potential return relative to risk taken could exceed that of traditional mining investments.

This positioning attempts to address investor concerns that stable, long-life projects might lack the torque or leverage that attracts speculative capital to the resource sector. Peterson's argument is that even risk-averse investors allocating modest portfolio weight to Atlas Salt could achieve meaningful return enhancement due to favorable risk-adjusted characteristics, while more aggressive investors might find the absolute return potential compelling despite lower volatility.

Closing the Valuation Gap

Peterson outlined a multi-pronged strategy for narrowing the discount to intrinsic value: advancing the project through development milestones to trigger natural re-rating, educating the market about the salt project's unique risk profile, demonstrating reduced risk through financing terms, helping investors understand alternative valuation frameworks applicable to salt companies, continuing institutional investor outreach, and securing research coverage to improve market visibility.

The company recently obtained research coverage, which Peterson noted as a step toward improved market communication. He emphasised that securing project financing would serve as external validation of the risk profile, as lender due diligence would independently verify the stability and predictability of cash flows that underpin the company's valuation arguments.

The Investment Thesis for Atlas Salt

- Atlas Salt trades at approximately 0.1x its net asset value, a steep discount that management attributes to investor unfamiliarity with the salt sector rather than genuine project risk, creating a potential opportunity for investors who take the time to understand the asset.

- The company has already eliminated metallurgical, geological, and permitting which are risks that suppress mining valuations after securing an approved environmental assessment and demonstrating the inherent simplicity of salt deposit development.

- The Great Atlantic Salt Project's 24-year mine life, supported by 50 years of defined resources, produces stable, long-duration cash flows that behave more like an infrastructure or annuity-style asset than a conventional depleting mining operation, making traditional NAV-based valuation metrics an inadequate measure of the company's true worth.

- The project's primary customers are municipal and state or provincial governments that are in many cases legally obligated to purchase de-icing salt, providing a structurally mandated demand profile that insulates revenue from the price volatility and demand destruction common to commodity markets.

- Alternative valuation frameworks more suited to stable, cash-generative businesses including a free cash flow yield methodology and EBITDA multiples in line with publicly traded salt producers that imply potential valuations ranging from $1.9 billion to $3 billion, against a current market capitalisation that reflects a fraction of either figure.

- Securing project financing represents the single most important near-term catalyst, as lender due diligence would provide independent, third-party validation of the reduced-risk thesis and is widely expected to trigger a meaningful re-rating toward intrinsic value.

- Across conservative, moderate, and aggressive return frameworks, Atlas Salt presents a risk-adjusted case that management argues is superior to most resource sector alternatives with lower absolute risk and an upside potential that may substantially exceed what that risk level would ordinarily command.

TL;DR

Atlas Salt trades at ~0.1x NAV despite having eliminated major mining risks in metallurgical, geological, permitting, and offering stable, 25-year cash flows backed by legally-obligated government customers. Alternative valuation methodologies, free cash flow yield and EBITDA multiples, suggest potential values ranging from $1.9B to $3B versus current market cap, with the disconnect attributed to investor unfamiliarity with the salt sector. Key catalyst is securing project financing that would validate the reduced risk profile and trigger re-rating toward intrinsic value.

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed