Undervalued? ValOre Metals Advances 2.2Moz PGE Asset at $26M Cap as Platinum Supply Falls

ValOre Metals targets a 2026 PEA for its 2.2Moz Pedra Branca PGE project in Brazil, trading at ~$26M vs peers at $100–200M amid structural platinum supply decline.

- ValOre Metals is developing the Pedra Branca platinum-palladium project in northeast Brazil, a 2.2 million ounce resource that trades at approximately $26 million market capitalisation which is a fraction of the $100–200 million valuations commanded by development-stage PGE peers with comparable resource sizes and grades.

- Global platinum supply has declined since a 2021 peak even as the platinum price has roughly doubled over the same period illustrating the structural inelasticity of PGE supply and the geopolitical risk embedded in a market.

- CEO Nick Smart joined ValOre in October 2024 and has since divested the company's uranium assets to establish an unambiguous 100% PGE focus, addressing a key source of historical market confusion that contributed to the valuation discount.

- Metallurgical test work conducted with the University of Cape Town is returning palladium and platinum extractions of 73–74% from a hydrometallurgical leaching route designed for Pedra Branca's weathered near-surface ore, with additional optionality from high-grade chromitite material to enhance early mine-life economics.

- A Preliminary Economic Assessment targeting delivery within 2026 represents the primary near-term catalyst, with a series of interim metallurgical and engineering updates expected to progressively build the investment case ahead of formal publication.

ValOre Metals (TSXV:VO) is a Canadian-listed junior developer focused exclusively on platinum group elements (PGEs), specifically platinum and palladium, through its flagship Pedra Branca project in northeast Brazil. With a resource base of 2.2 million ounces and a market capitalisation of approximately $26 million, the company is operating at a fraction of the valuations commanded by comparable development-stage PGE peers. CEO Nick Smart, a chemical engineer with 21 years of experience at Anglo American in platinum and palladium operations, joined the company in October 2024 with a clear mandate: demonstrate project credibility, build market awareness, and deliver a Preliminary Economic Assessment within the year.

A Sector Under Supply Pressure

The broader context for ValOre's investment case begins at the commodity level. Platinum and palladium supply is highly concentrated geographically, with approximately 80% of global PGE production coming from South Africa and Zimbabwe. Russia accounts for a significant share of palladium supply. This concentration creates both structural fragility in supply and increasing geopolitical risk for the industrial consumers predominantly automotive manufacturers that depend on these metals for catalytic converters and, increasingly, hybrid vehicle components.

Supply has not responded to price signals in the way conventional economics might predict. Primary platinum mine production remained tight in 2025 with an anticipated further declines in above-ground inventories. The reasons are structural: South African mines are aging, deep-level operations facing rising input costs. Electricity costs in the region have increased by approximately 60% since 2021, and diesel supply which around 60% transits through the Strait of Hormuz is increasingly constrained and expensive.

Smart summarised the supply-side challenge directly:

"The primary mine production of platinum has been in decline in the last 5 years. That's in the context of a metal price which has doubled over the course of the last year. That tells you something around the elasticity around supply and the difficulty of bringing new metals into the market."

The takeaway for investors is that additional PGE supply is not arriving simply because prices have risen. The geological, operational, and geopolitical barriers to expanding output from the existing production base are significant, and the pipeline of credible development-stage projects outside southern Africa and Russia is extremely thin.

What's Driving The Valuation Gap?

ValOre's market capitalisation of approximately $26 million sits in stark contrast to peers with comparable or only modestly larger resource bases. Companies such as Stillwater Critical Minerals, developing its Stillwater West project in Montana with approximately 3 million ounces, and Generation Mining, advancing an Ontario project of similar scale, are both trading at $100–200 million market capitalisations. Pedra Branca's 2.2 million ounce resource at 1.08 g/t 2P+gold compares reasonably to these assets on both size and grade metrics.

Smart attributes the disconnect to two factors. The first is market awareness and historical confusion about the company's identity. ValOre previously held uranium assets, which created ambiguity about whether the company was a committed PGE developer. That ambiguity has now been addressed through the completed sale of the Hatchet uranium properties to Future Fuels, leaving the company 100% focused on Pedra Branca. The second factor is the absence of a demonstrated economic case. Without a PEA, investors have limited ability to underwrite the project on a fundamentals basis. Closing that gap is the primary objective for 2026.

Interview with Nick Smart, Director & CEO of ValOre Metals

Metallurgical Progress at University of Cape Town

Pedra Branca presents a near-surface, open-cast mineable orebody, which carries inherent cost advantages over the deep-level underground mines that characterise South African PGE production. However, near-surface mineralisation often comes with a weathered or oxidised upper zone which complicates the standard flotation-based processing route used for PGE ores. Flotation relies on the sulfide association of PGEs and oxidation degrades that association and reduces recovery efficiency.

To address this, ValOre and University of Cape Town's Department of Chemical Engineering have been developing a hydrometallurgical leaching route tailored to the weathered material at Pedra Branca. Initial shake-flask testing is returning palladium extractions of 73% and platinum extractions of 74% which Smart describes as encouraging at this early stage of the test programme. Further improvements are expected as testing scales up to stirred-tank reactors and column tests that more closely simulate heap leach conditions.

Smart noted, "When we look at the early years of the life of mine, going in and collecting that chromitite material, processing it, and getting really high grades, we're looking at that as part of our early-year mine plan, and it'll form part of the preliminary economic assessment (PEA)."

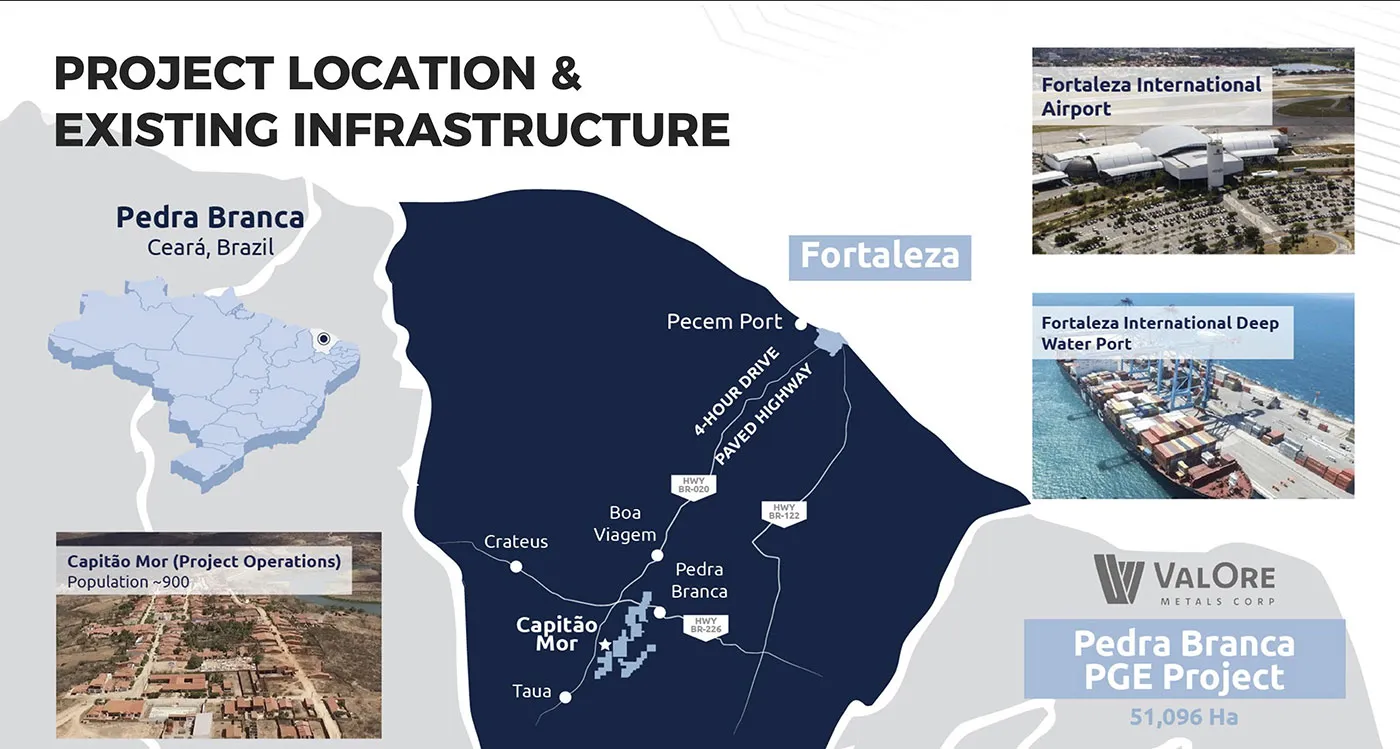

Project Infrastructure & Cost Positioning

Capital intensity and operating cost positioning are central to the investment case at Pedra Branca. Smart outlined several factors that he believes support a low-cost development profile. The project site sits approximately four hours by paved highway from a deep-water port. Electrical infrastructure is available in proximity to the site, removing the need for self-generated power capacity. The near-surface, open-cast mining method eliminates the substantial upfront capital associated with underground development.

Together, these factors are intended to position Pedra Branca toward the lower end of the PGE cost curve but particularly relevant as a differentiator when the company is making its case to investors ahead of a PEA.

2026 Milestones

The PEA is the stated year-end target and will represent the first formal economic demonstration of the project. Leading into that, the company has committed to publishing interim results from the ongoing metallurgical test programme as it scales through successive phases, along with early-stage engineering outputs that will feed into the PEA model. Smart described the expected flow of news as incremental but directionally significant, with the PEA representing a binary event in terms of investor underwriting.

Following the PEA, the company intends to move into the licensing process in Brazil, which Smart described as a jurisdiction with favourable project development conditions, community support, and no major impediments identified to date.

The Investment Thesis for ValOre Metals

- Significant valuation discount to peers. At approximately $26 million market cap versus $100–200 million for comparable PGE developers with similar resource sizes, the company presents a clear valuation gap that management is actively working to close.

- Structural supply constraints support PGE prices. Declining primary production from aging southern African mines, rising input costs, and geopolitical concentration risk underpin a favourable long-term demand-supply backdrop for platinum and palladium.

- Near-surface, open-cast project reduces capital intensity. Pedra Branca's mining method, existing infrastructure access, and Brazil logistics profile support a potential low-cost production case relative to deep-level peers.

- Metallurgical progress de-risks processing. UCT test work is demonstrating viable extraction rates for weathered material, with high-grade chromitite optionality providing additional early-year economic upside.

- PEA delivery within 2026 is a clear binary catalyst. The first economic study will allow investors to underwrite the project on fundamentals for the first time, with a series of interim technical releases expected to build confidence ahead of publication.

- 100% PGE focus removes historical ambiguity. The sale of uranium assets has resolved prior market confusion about the company's identity and strategic direction.

- Experienced CEO with direct PGE sector background. Nick Smart brings 21 years of Anglo American platinum and palladium experience, providing operational credibility in a technically complex commodity.

- Actionable consideration: Investors monitoring the stock should track interim UCT metallurgical updates and early engineering releases as leading indicators of PEA quality ahead of the formal publication.

Platinum and palladium occupy a structurally unique position in the critical minerals landscape. Unlike many metals where elevated prices eventually stimulate new supply, the PGE sector has demonstrated over the past five years that price alone is insufficient to meaningfully expand production. The reasons are geological, operational, and geopolitical in combination.

Approximately 80% of global platinum and palladium production originates in South Africa and Zimbabwe, with Russia accounting for a significant portion of global palladium supply. These are not young, low-cost operations. South African PGE mines are mature, deep-level assets requiring substantial ongoing capital to maintain production, with electricity and diesel costs rising sharply over recent years. On the demand side, the narrative is increasingly driven not just by traditional catalytic converter applications but by the continued relevance of hybrid and internal combustion engine vehicles, where PGE demand remains structurally durable. Industrial and investment demand add further layers to a market already contending with supply inelasticity.

The scarcity of credible development-stage PGE projects outside the traditional producing regions amplifies the potential value of those that do exist. As Smart articulated:

"You've got this growing demand but real limitations are in terms of bringing more metal on. So, if you've got a viable good project, that will give you a strong tailwind to be able to get that into production."

The geopolitical dimension compounds the supply picture. Automotive and industrial consumers reliant on PGEs sourced from South Africa and Russia face a concentration risk that is becoming harder to ignore in a world of escalating supply chain scrutiny. The incentive to develop credible projects in stable, diversified jurisdictions in Brazil, Canada, the United States are growing.

For investors, the macro case for PGE exposure is compelling. The challenge and the opportunity lies in identifying the handful of development-stage companies with the project quality, jurisdiction, and technical capability to navigate from resource to production.

TL;DR

ValOre Metals is a PGE developer trading at approximately $26 million, well below the $100–200 million valuations of its closest peers, with a 2.2 million ounce platinum-palladium resource in Brazil, a technically credentialed CEO, improving metallurgical results, and a Preliminary Economic Assessment due in 2026 that should allow investors to underwrite the project on fundamentals for the first time. The macro backdrop of declining primary PGE supply, rising prices, and geopolitical concentration risk adds further weight to the case for early positioning.

Frequently Asked Questions (FAQs) AI-Generated

Two factors are primarily responsible. First, the company's historical ownership of uranium assets created market confusion about whether ValOre was a serious PGE developer. That ambiguity has been resolved through the sale of the Hatchet uranium properties to Future Fuels. Second, the absence of a Preliminary Economic Assessment has limited investors' ability to value the project on a fundamentals basis. With the company now 100% focused on Pedra Branca and a PEA targeted for 2026, management is working directly to close both gaps.

Pedra Branca is a near-surface orebody amenable to open-cast mining — a significant structural advantage over the deep-level underground mines that dominate South African PGE production, where development costs are substantially higher. The project is located approximately four hours by paved highway from a deep-water port in northeast Brazil, with electrical infrastructure accessible near the site, reducing the upfront capital required to establish basic operational utilities. The project also benefits from community support and no identified major licensing impediments.

The test work is currently at shake-flask stage — the first step in a phased programme — being conducted with the University of Cape Town's Department of Chemical Engineering. Results to date show 73% palladium and 74% platinum extractions via a hydrometallurgical leaching route with a pre-treatment step, developed to address the weathered, oxidised nature of the near-surface ore at Pedra Branca. These figures are expected to improve as testing scales to stirred-tank reactors and column tests simulating heap leach conditions. Importantly, a separate line of UCT test work has demonstrated the ability to unlock high-grade chromitite-hosted PGEs (6.5–8.5 g/t) through a hot caustic pre-treatment, creating potential for high-grade feed in the early years of mine production.

The PEA will be the first formal economic study of Pedra Branca and the first opportunity for investors to assess the project's capital requirements, operating cost profile, and net present value on a documented basis. Prior to the PEA, the investment case rests on resource size, grade, and metallurgical indications — all of which are positive, but which stop short of a full economic underwriting. The PEA changes that, and given the valuation gap between ValOre and its peers, a credible positive economic study could represent a meaningful re-rating event.

Demand for platinum and palladium remains structurally supported by catalytic converter production for internal combustion and hybrid vehicles, as well as industrial applications. On the supply side, primary platinum production has been declining since 2021 despite significantly higher prices, illustrating that the market cannot easily bring new supply forward. With 80% of production concentrated in South Africa, Zimbabwe, and Russia, geopolitical risk is a growing concern for industrial consumers seeking supply chain diversification. These conditions collectively support a favourable long-term price environment for PGE producers and developers in politically stable, well-located jurisdictions such as Brazil.

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

Stay Informed