Uranium Has Become a Strategic Asset: Energy Security Fears Explain Why the Shift Is Accelerating

Uranium spot prices are up 33% year-over-year as energy security policy, AI power demand, and Kazatomprom supply constraints reshape global uranium markets in 2026.

- Uranium is increasingly treated as a strategic energy asset rather than solely a climate-transition fuel, following geopolitical shocks that exposed fossil fuel supply chain vulnerabilities across major trade routes.

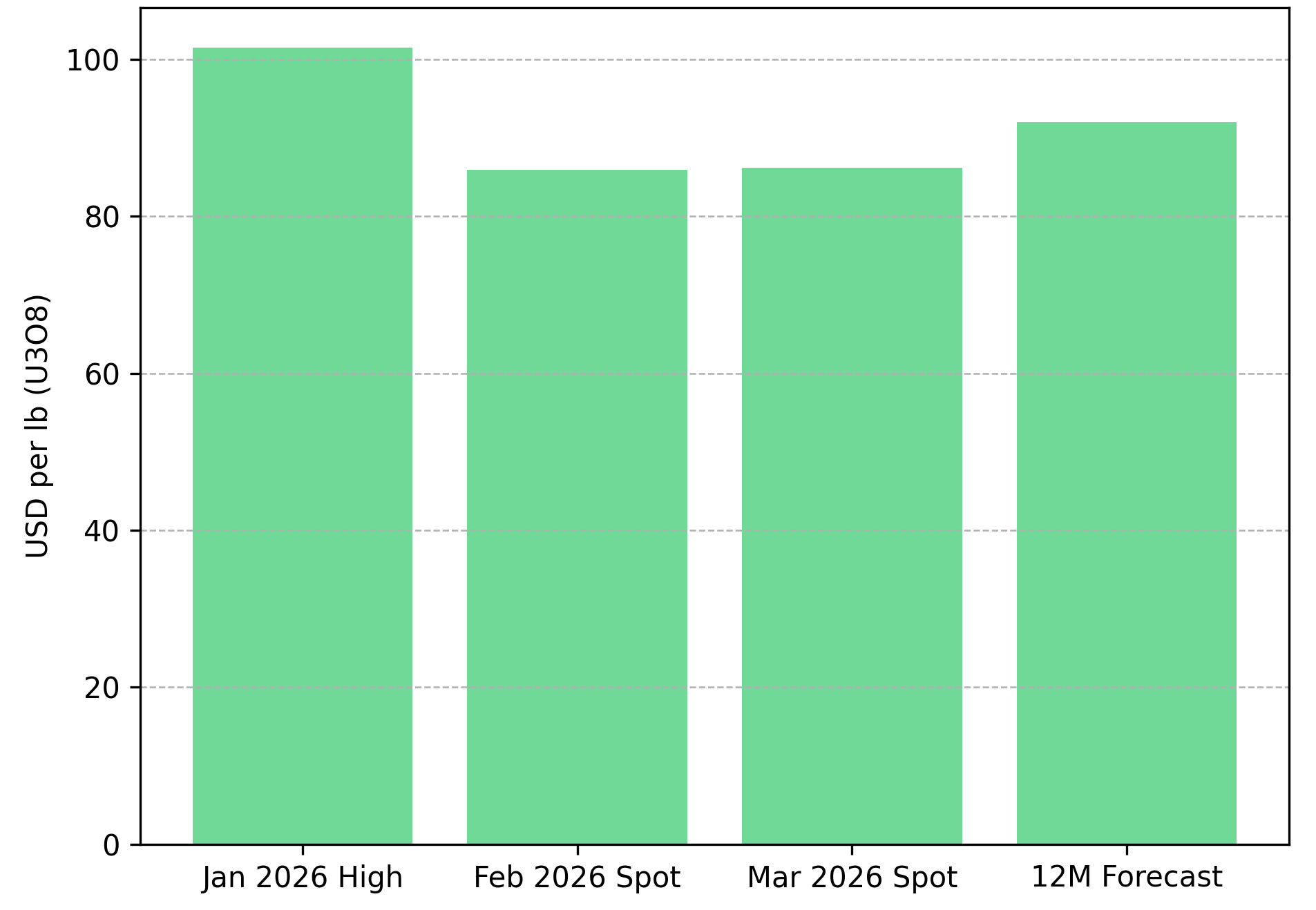

- The uranium spot market is trading near $86.20 per pound as of early March 2026, up more than 33% year-over-year, with structural supply deficits supporting macro model projections toward $92 per pound within twelve months.

- Kazakhstan's production challenges and Central Asian logistical risks are concentrating investor attention on uranium supply from politically stable jurisdictions, including Canada and the United States.

- Expanding electricity demand from artificial intelligence infrastructure is reinforcing the case for nuclear baseload generation at a time when reactor construction pipelines are extending across North America, Europe, and Asia.

- Western uranium developers and in-situ recovery producers operating in the Athabasca Basin and US uranium districts are increasingly positioned as strategic alternatives to geopolitically exposed supply chains.

A New Energy Security Framework Is Taking Shape

The Strait of Hormuz carries approximately 20% of the world's traded oil. When escalating Middle East tensions raised the prospect of supply disruptions in early 2026, governments across Europe, Asia, and North America were reminded of a persistent vulnerability in their energy architecture. The immediate concern was oil. The structural consequence was a sharper policy focus on nuclear power.

Nuclear energy's appeal in an energy security context is straightforward: reactors operate independently of fossil fuel trade routes, generate baseload electricity with capacity factors exceeding 90%, and require long-term fuel supply agreements that create predictable procurement timelines. These characteristics have elevated uranium from a climate-transition commodity into something closer to a strategic resource under active government procurement strategies.

As of early March 2026, uranium spot prices are trading near $86.20 per pound, representing a pullback from a late January 2026 high of approximately $101.50 per pound but still up more than 33% year-over-year. Macro models indicate prices could rise toward $92 per pound within twelve months, reflecting tightening supply fundamentals rather than speculative positioning.

Electricity Demand Growth & Reactor Pipeline Expansion

The surge in electricity consumption associated with artificial intelligence infrastructure represents a demand signal that was not fully priced into uranium markets as recently as two years ago. Modern data centers require continuous, uninterrupted power. Solar and wind generation, given their intermittency, cannot meet those reliability requirements on their own. Nuclear power, operating at capacity factors exceeding 90%, is increasingly considered among the preferred technical solutions for large-scale computing infrastructure.

The World Nuclear Association estimates that more than 60 reactors are currently under construction globally, with hundreds more at various stages of planning and permitting. Technology companies have begun negotiating long-term power agreements tied to small modular reactors, signaling that private sector demand may supplement government-led nuclear expansion. For uranium markets, the implication is higher sustained reactor demand at a time when global mine production remains structurally constrained.

Geographic Concentration & Supply Chain Risk

A defining structural feature of the uranium market is its geographic concentration. Kazakhstan alone accounts for approximately 43% of global uranium production, with Namibia, Canada, and Australia comprising most of the remainder. This degree of concentration means that production disruptions at a single major supplier can affect global supply balances in ways that few other commodity markets face.

Kazatomprom, Kazakhstan's state uranium producer, is facing ongoing production challenges linked to shortages of sulfuric acid, a critical input for in-situ recovery operations. Separately, export routes from Central Asia increasingly rely on the Caspian Sea "Middle Corridor," a logistics network that passes near several geopolitical flashpoints. For Western utilities operating under decade-long fuel procurement contracts, these are not theoretical risks, they are variables that supply chain managers are now factoring directly into sourcing strategies.

The shift in utility behavior is reflected in contracting activity. Procurement interest in Canadian and US production has increased, with buyers increasingly receptive to domestic supply agreements that prioritize jurisdictional security. This repricing of supply risk has become one of the more significant valuation developments in the sector over the past eighteen months.

Canada's Athabasca Basin & the Case for Jurisdictional Premium

Deposits in the Athabasca Basin contain grades that can exceed 10% U3O8, compared to a global average often below 0.2%. That grade differential directly influences project economics across all-in sustaining costs, processing requirements, and capital intensity, translating into significantly lower resource extraction volumes for equivalent uranium output.

Canada's regulatory framework and long-standing commercial relationship with uranium development, the country has produced uranium commercially since the 1940s, provide the policy stability that institutional investors now weigh explicitly in due diligence.

ATHA Energy holds one of the largest uranium land positions in the country, with more than 7 million acres of exploration ground including 3.8 million acres within the Athabasca Basin across its Gemini, Ridge, Pinnacle/Wares, and Zenith projects. The company also holds 3.1 million acres in Nunavut, where its Angilak Project features a mineralized trend extending over 31 kilometers, with exploration drilling intersecting grades up to 5.85% U3O8. Troy Boisjoli, Chief Executive Officer of ATHA Energy, frames the company's strategic positioning within the Athabasca Basin context:

"We're in control of an entire district, an entire sub-basin of the Athabasca, so we like where we're positioned from a market perspective."

On the continuity of mineralization intersected at Angilak, Boisjoli highlights the geological parallels informing the resource thesis:

"We're seeing very thick grade thicknesses of mineralization over 26 meters of continuous mineralization, combined downhole with 13 meters of continuous with about 1.9 meters of high grade within it… We're recognizing this as part of an analogous setting to what we see in the Athabasca."

US Policy & the Rebuilding of Domestic Uranium Supply

The United States spent much of the past decade drawing down domestic uranium production capacity in favor of lower-cost imports. The Nuclear Fuel Supply Act, a bipartisan measure appropriating $2.7 billion for domestic production of low-enriched and high-assay low-enriched uranium, consolidates the Uranium Reserve into the American Assured Fuel Supply Program, signaling a durable shift in procurement policy toward domestic supply chains.

The regulatory environment is becoming more accommodating of project development, and utility buyers are increasingly receptive to agreements that prioritize jurisdictional security alongside price.

Energy Fuels operates the White Mesa Mill in Utah, the only conventional uranium processing facility currently operating in the United States. The mill represents a critical bottleneck in the domestic nuclear fuel cycle, processing capacity that would take years and significant capital to replicate. The company's Pinyon Plain Mine produced ore grading 1.62% equivalent U3O8 in 2025, placing it among the highest-grade uranium mines operating in US history. Mark Chalmers, Chief Executive Officer of Energy Fuels, describes the company's positioning at White Mesa as extending beyond uranium into adjacent critical minerals:

"We're building a critical minerals hub focused in Utah around our White Mesa Mill, built around our uranium business… But we also have rare earth, and we're expanding that leaps and bounds… We identified some time ago that we wanted to have the metals and alloys capability, which are in short supply globally."

On the financial impact of that critical minerals integration, Chalmers is direct about the magnitude:

ISR Production Methods & Capital-Efficient Supply Growth

In-situ recovery mining has emerged as the dominant production method for uranium development within the United States. Unlike conventional open-pit or underground operations, ISR injects chemical solutions directly into uranium-bearing sandstone formations to dissolve and extract uranium without physical ore removal. The approach requires substantially less capital expenditure and carries a significantly reduced surface disturbance profile compared to conventional extraction methods.

enCore Energy operates the Alta Mesa and Rosita central processing plants in South Texas, both currently operational, and maintains a development pipeline spanning Texas, Wyoming, and South Dakota. The Gas Hills Project in Wyoming carries a projected pre-tax internal rate of return of 54.8% on approximately $55.2 million in initial capital, based on a long-term uranium price assumption of $87 per pound, according to a preliminary economic assessment by WWC Engineering dated February 2025. William Sheriff, Executive Chairman of enCore Energy, addresses the environmental profile of ISR that is reshaping regulatory and community engagement:

"Uranium mining now, in terms of in-situ, is not your predecessor uranium. It's as different as day and night. Being so environmentally friendly and so short timeline, short cost to reclaim them."

High-Grade Conventional Deposits & Long-Term Supply Optionality

While ISR operations address near-term domestic supply requirements, high-grade conventional deposits remain central to the long-term global uranium supply picture. Deposits of exceptional grade concentrate uranium into smaller mining volumes, improving extraction economics at any given commodity price and providing project resilience across price cycles.

IsoEnergy holds the Hurricane deposit in the Athabasca Basin, which carries an indicated resource of approximately 48.6 million pounds grading 34.5% U3O8 and an inferred resource of 2.7 million pounds grading 2.2% U3O8, per an NI 43-101 technical report effective July 2022. The company is simultaneously advancing a 2,000-tonne bulk sample program at the Tony M Mine in Utah, with completion targeted for April 2026. The mine holds existing state and federal operating permits, which IsoEnergy estimates could reduce development timelines by three to five years relative to a new permit application. A production restart decision is anticipated following completion of technical and economic evaluations. Phil Williams, Chief Executive Officer of IsoEnergy, characterizes Hurricane's geological standing:

"Unquestionably, there's a lot more to be found, and we have two spectacular opportunities to do that. The first is, of course, Hurricane, the highest-grade uranium resource in the world."

On the Tony M bulk sample and the decision it is informing, Williams outlines the path forward:

"We are doing the bulk sample at Tony M. This has given us all the information we need about mining rates, costs… Ultimately putting us in a position to make a full restart decision."

Beyond the Athabasca Basin, uranium development activity is expanding in emerging jurisdictions. Atomic Eagle is advancing the Muntanga Uranium Project in Zambia, which holds a JORC-compliant resource totaling 47.4 million pounds of U3O8 at 344 parts per million, with 40.0 million pounds in the measured and indicated categories. The project's shallow mineralization supports open-pit mining, and Zambia's current fiscal regime for the project includes a 5% royalty and 30% corporate tax. For applying enterprise value per pound of uranium resource as a comparative metric, Muntanga represents one of the larger undeveloped resource inventories in its peer group.

Risks & Key Considerations

Despite the structural clarity of the long-term investment case, uranium markets remain subject to significant volatility. A rapid resolution of Middle East geopolitical tensions could reduce the urgency of energy security policy programs and slow the pace of government support for nuclear expansion. A resolution of Kazatomprom's sulfuric acid supply constraints, or unexpected production growth from emerging producers, could materially ease the supply deficit that has supported recent price appreciation.

Discovery outcomes are uncertain, permitting timelines are subject to regulatory variability, and junior companies often rely on equity capital markets to fund operations, with associated dilution risk. Evaluations should incorporate discounted cash flow modeling, net present value sensitivity analysis across uranium price ranges, and explicit jurisdictional risk scoring.

The Investment Thesis for Uranium

Several structural factors are converging to reshape uranium markets and sustain investor interest beyond the near-term price cycle.

- Energy security policy is now a primary driver of nuclear power development, as governments in North America, Europe, and Asia accelerate reactor construction and fuel procurement programs in direct response to demonstrated vulnerabilities in fossil fuel supply chains.

- A structural supply deficit remains unresolved, with global uranium demand from operating reactors continuing to exceed annual primary mine production and requiring sustained drawdown of utility inventories and secondary market supply.

- Jurisdictional stability has become an explicit valuation input, with producers and developers in Canada, the United States, and allied nations commanding premiums that reflect lower geopolitical and permitting risk relative to Central Asian supply sources.

- ISR producers operating in US uranium districts offer capital-efficient production growth with favorable project-level economics supported by domestic policy incentives, including the Nuclear Fuel Supply Act's appropriation of $1.6 billion for domestic enriched uranium programs.

- High-grade conventional deposits in the Athabasca Basin provide long-duration supply optionality with project economics that remain robust across a wide range of uranium price scenarios.

- The integration of critical minerals processing alongside uranium production creates margin expansion pathways that are independent of uranium price movements and align with government procurement priorities for rare earth supply.

- District-scale exploration positions spanning the Athabasca Basin and Nunavut provide optionality on future resource discovery, with value inflection achievable at exploration capital rather than full development cost.

Uranium has become a strategic asset, subject to government procurement priorities, energy security policy frameworks, and long-term fuel supply agreements that create demand visibility extending well beyond the near-term commodity price cycle.

TL;DR

Uranium is transitioning from a climate-transition commodity into a strategic government procurement priority, driven by energy security fears, AI-driven electricity demand, and structural supply deficits. Spot prices sit near $86.20/lb as of early March 2026, up more than 33% year-over-year, with macro models pointing toward $92/lb. Supply remains geographically concentrated, with Kazakhstan accounting for roughly 43% of global output and facing ongoing production constraints. Canadian Athabasca Basin deposits, US ISR producers, and allied-jurisdiction developers are attracting premiums as utilities reprice jurisdictional risk and governments deploy legislation, including the $2.7 billion Nuclear Fuel Supply Act, to rebuild domestic fuel supply chains.

FAQs (AI-Generated)

Governments across North America, Europe, and Asia are prioritizing nuclear power as a response to demonstrated vulnerabilities in fossil fuel supply chains. Unlike oil and gas, nuclear reactors operate independently of trade routes such as the Strait of Hormuz, deliver baseload power at capacity factors exceeding 90%, and run on long-term fuel contracts that provide procurement predictability — characteristics that have repositioned uranium within national energy security frameworks.

Artificial intelligence infrastructure is a significant new demand driver. Modern data centers require uninterrupted, high-reliability power that intermittent renewables cannot consistently supply. Nuclear power is increasingly viewed as the preferred technical solution, with technology companies beginning to negotiate long-term power agreements tied to small modular reactors. The World Nuclear Association estimates more than 60 reactors are currently under construction globally, with hundreds more in planning.

Kazakhstan's state producer, Kazatomprom, accounts for approximately 43% of global uranium output and is experiencing production challenges linked to shortages of sulfuric acid, a critical input for in-situ recovery operations. Central Asian export routes also rely on logistics corridors near geopolitical flashpoints. This concentration means a disruption at a single major supplier can materially affect global supply balances, which is why Western utilities are increasingly prioritizing Canadian and US supply agreements.

The Athabasca Basin in Canada hosts deposits grading above 10% U3O8, compared to a global average typically below 0.2%. That grade differential compresses extraction volumes, lowers all-in sustaining costs, and improves project economics across price cycles. Canada's stable regulatory environment and its commercial uranium production history dating to the 1940s provide the jurisdictional reliability that institutional investors are now explicitly weighting in due diligence processes.

ISR mining injects chemical solutions directly into uranium-bearing sandstone formations to dissolve and extract uranium without physical ore removal. Compared to conventional open-pit or underground mining, ISR requires substantially less capital expenditure and produces a significantly smaller surface disturbance footprint. In the US context, ISR is the dominant production method and is central to rebuilding domestic supply capacity under the Nuclear Fuel Supply Act, which appropriates $2.7 billion to support domestic low-enriched and high-assay low-enriched uranium production.

Analyst's Notes

Subscribe to Our Channel

Stay Informed