US Acquisition in the DRC Forces a Repricing of Geopolitical Risk Across the Copper Supply Chain

The US buys DRC copper assets, rewiring global supply chains. What it means for copper prices, Tier-1 mining stocks, and the long-term critical minerals investment case.

- The US-backed $700 million acquisition of Congolese copper-cobalt assets through Virtus Minerals secures approximately 5% of global cobalt supply and represents the most significant Western intervention in DRC mining since the 2025 Washington Peace Agreement.

- China retains dominant control over copper refining capacity and upstream DRC assets, and the partial displacement of that position is fragmenting global commodity pricing into politically segmented tiers.

- Near-term copper prices remain range-bound near $12,600 per tonne, constrained by a 25% year-over-year decline in Chinese imports in early 2026 and elevated London Metal Exchange inventory levels.

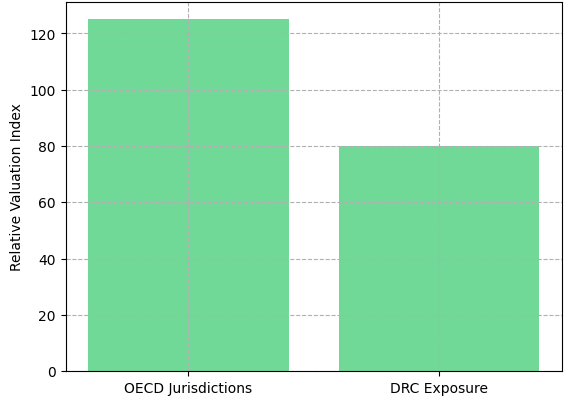

- Institutional capital is applying higher discount rates to politically exposed assets and premium valuations to projects in Organisation for Economic Co-operation and Development jurisdictions, creating a measurable jurisdiction premium.

- High-grade development assets in stable jurisdictions, including Abitibi Metals' B26 polymetallic deposit in Quebec, are gaining relevance as scalable alternatives to supply chains exposed to DRC political risk.

Geopolitics, Global Copper & Cobalt Supply Chain

The Democratic Republic of Congo holds approximately 70% of global cobalt supply and a growing share of copper production, a concentration China recognized early. Chinese state-backed entities have controlled significant upstream DRC assets for over a decade while dominating refining capacity across both supply chains.

The $700 million Virtus Minerals acquisition establishes a Western stake in this domain, securing roughly 5% of global cobalt supply under US-aligned ownership, a narrow foothold, but a meaningful precedent: the US government is now willing to deploy capital directly into asset acquisitions. The Washington Peace Agreement, signed December 2025, explicitly ties resource access to regional stabilization, making mining assets in the DRC function as instruments of foreign policy in a way that has no modern parallel outside of oil.

China’s advantage is structural, controlling the refining bottleneck for most DRC material, so Western acquisitions address origin but not processing. This is driving two pricing tracks: “clean chain” versus conventionally refined copper, with widening long-term price gaps. Markets are adjusting, DRC-linked assets face higher discount rates due to geopolitical and operational risks, while OECD assets command valuation premiums.

Copper Markets Show Short-Term Surplus but Long-Term Structural Tightness

Despite the strategic importance of DRC asset-level developments, near-term copper price signals are not uniformly bullish. The physical market is carrying more inventory than the financial market's scarcity narrative implies, creating a dislocation that is a source of near-term volatility risk.

Chinese copper imports fell approximately 25% year-over-year in early 2026 as spot prices above $12,000 per tonne triggered demand destruction at the margin, while LME warehouse stocks reached multi-year highs, reflecting a physical market that is, for now, adequately supplied. This is consistent with prior price cycles: at elevated levels, Chinese end-users in residential construction and consumer electronics defer purchases, creating temporary inventory builds that suppress spot prices. Structural demand from electrification is not disappearing; it is being deferred at the margin by price sensitivity.

Macro Volatility from Energy & Geopolitics

The Iran conflict and subsequent ceasefire negotiations contributed to copper price volatility around the $12,600 per tonne range in Q1 2026, as energy cost uncertainty propagated through mining cost curves. Diesel and electricity are the two largest variable cost inputs in open-pit copper mining, a 10% increase in energy prices adds approximately $0.08 to $0.12 per pound to all-in sustaining costs at a median-grade asset. This sensitivity falls disproportionately on lower-grade, higher-strip-ratio operations, reinforcing the investment case for high-grade deposits where unit economics are more resilient to input cost inflation.

Fitzroy Minerals' Chief Executive Officer Merlin Marr-Johnson has observed that the supply side of the market is structurally constrained in ways that are not fully reflected in near-term pricing. On the challenge of growing production from the existing base:

"Production growth is difficult. It's a very mature industry, one struggling just to maintain output. Vast amounts of capital are being deployed simply to hold production flat, so metal prices have to rise as demand remains strong."

The Disconnect Between Physical & Financial Markets

The financial market for copper is pricing a multi-year scarcity thesis driven by electrification demand, while the physical market is currently registering surplus conditions. That gap creates a range-bound pricing environment in the near term, likely $11,500 to $13,500 per tonne through 2026, before structural deficit conditions reassert. The relevant implication is that entry timing matters: projects that reach construction-readiness in 2027 and 2028 are positioned to benefit from a tighter physical market, while those requiring 5-plus years to production face greater price uncertainty on both the upside and downside.

Capital Rotation Toward Tier-1 Jurisdictions & High-Grade Assets

The geopolitical repricing of supply-chain risk is translating into observable capital allocation behavior. Institutional mining mandates are increasingly specifying jurisdictional screens, excluding or discounting assets in Tier-3 jurisdictions, and major mining companies are replacing the lowest-cost-at-any-jurisdiction approach with risk-adjusted return frameworks that weight permitting timelines, ESG compliance costs, and political stability as first-order variables.

Historically, grade was the dominant determinant of mine economics, a 2% copper equivalent deposit in a difficult jurisdiction would attract capital over a 1% deposit in a stable one. That relationship is under pressure. Permitting timelines in several Latin American and African jurisdictions have extended to 7-12 years due to social license requirements and regulatory complexity, materially increasing NPV sensitivity to discount rate assumptions.

A project yielding a 25% IRR at a 4-year permitting timeline may fall below a 15% IRR threshold at 8 years, rendering the asset economically uninvestable regardless of grade. Predictability of development schedule is now as important to project economics as the deposit's intrinsic quality.

B26 Polymetallic Deposit: Scale & Capital Efficiency in a Tier-1 Jurisdiction

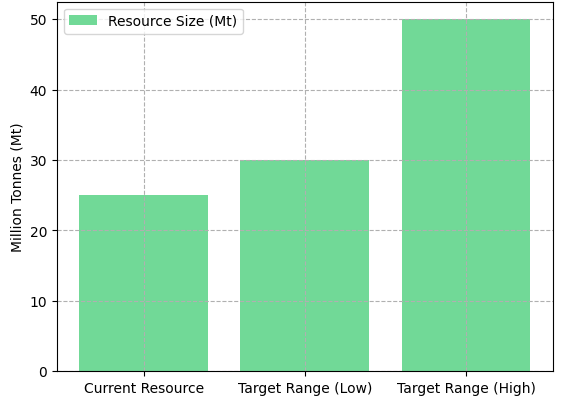

Abitibi Metals' B26 polymetallic deposit in Quebec offers a quantifiable illustration of how Tier-1 positioning interacts with project economics. The current resource stands at 13 million indicated tonnes grading 2.1% copper equivalent and 12.3 million inferred tonnes grading 2.2% copper equivalent, a 25-plus million tonne resource at grades placing it in the upper quartile of undeveloped VMS systems globally. The deposit has been built at a discovery cost of 2.5 cents per pound of copper equivalent, benchmarking favorably against peer explorers and reflecting disciplined capital deployment.

Chief Executive Officer Jonathon Deluce has framed the scale thesis as the central question for the project's valuation trajectory. On the deposit's potential size:

"One of the key questions has always been: how big can this deposit get? Our thesis is that it could very well be a 30 to 50 million tonne deposit."

The company's 40,000-metre drill program in 2026 is targeting both resource expansion within the known deposit and step-out exploration along the broader volcanic belt. For major copper producers seeking to replenish depleted reserve pipelines with jurisdictionally secure assets, a 30 to 50 million tonne VMS system in Quebec represents exactly the category of asset that commands acquisition premium.

Development Economics in a Volatile Macro Environment

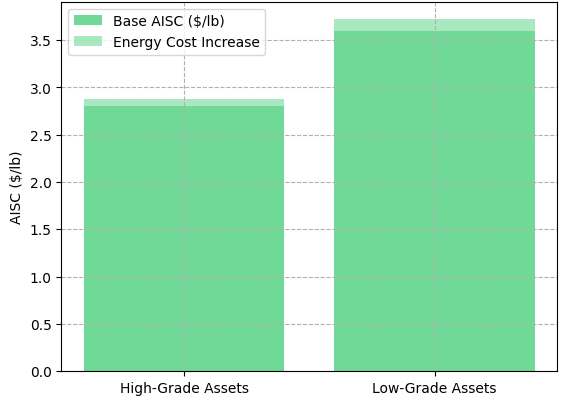

The macro environment of 2026, elevated energy costs, persistent cost inflation, and a higher-for-longer interest rate structure, has materially changed copper project economics. All-in sustaining costs have risen to $2.80-$3.60 per pound at feasibility base cases, up from $2.20-$2.80 per pound at the prior cycle peak, with project finance now priced 200-300 basis points above prior-cycle levels. Only projects in the lower quartile of the cost curve, high grade, simple metallurgy, proximate to infrastructure, retain investment-grade economics.

Those in the second and third quartiles face IRR compression that may not be recoverable without copper prices above $4.50 per pound, narrowing the universe of viable near-term development projects and strengthening the competitive position of assets with both grade and infrastructure advantages.

Feasibility Strength & Capital Discipline at Marimaca

Marimaca Copper's definitive feasibility study for its Marimaca oxide copper project in Chile provides a concrete data point on what investor-grade project economics look like in the current environment. The study confirmed industry-leading capital cost intensity and operating cost competitiveness, with a base-case copper price assumption of $4.30 per pound, a deliberate choice to stress-test the project against a conservative price scenario rather than optimize returns at spot.

President and Chief Executive Officer Hayden Locke has articulated both the feasibility results and the company's approach to managing execution risk:

"We delivered the DFS and confirmed industry-leading capital costs, competitive operating costs, and industry-leading return on invested capital metrics. We ran the study at $4.30 per pound copper, and we'll continue to think about this business in the mid-to-low fours."

Marimaca has now received the primary permits required to commence construction and is targeting construction start during the course of 2026, positioning the project for first production in the 2027 to 2028 window when structural deficit conditions in the physical copper market are expected to reassert.

Financing Constraints & the Narrowing Development Pipeline

Rising interest rates have increased the cost of project finance debt to the point where only projects with internal rates of return above 20% at base-case copper prices can attract institutional debt capital on terms that preserve equity returns. This threshold is being met by a smaller number of projects than at any point in the prior decade, which, paradoxically, is a constructive signal for the long-term copper supply outlook. A constrained development pipeline today is a supply deficit 7 to 10 years from now. Investors who can identify the subset of projects that will clear the financing hurdle are accessing the supply chain before the scarcity premium is fully reflected in spot prices.

Supply Chain Security is Reshaping Valuation Frameworks

The classification of copper and cobalt as critical minerals by the US, EU, Japan, and Australia has shifted their economic treatment from purely market-determined to partially policy-administered. Government-backed financing, production incentives, and direct acquisition activity, exemplified by the Virtus Minerals transaction, are introducing non-market price supports that conventional valuation models do not capture. Projects qualifying for government-backed financing or offtake agreements carry lower effective cost of capital than market rates imply, improving NPVs by a factor that can exceed 15-20% at a discount rate sensitivity.

Assets positioned as future supply sources for Western-aligned industrial consumers, automotive, power generation, defense, are increasingly being evaluated as acquisition targets by majors seeking to secure supply chains ahead of the anticipated physical deficit.

The M&A environment for copper assets is being reshaped by the same dynamics. Major producers are carrying reserve-to-production ratios at decade lows, while organic exploration is yielding fewer large discoveries per dollar spent than at any point since the 1990s. Depleted pipelines, geopolitical pressure on DRC-origin supply, and an accelerating electrification demand curve are creating conditions in which premium M&A multiples are paid for assets that are jurisdictionally secure, scalable, and at advanced stages of de-risking.

The Investment Thesis for Copper

- Geopolitical supply risk from the DRC-China axis is now a durable structural premium in copper and cobalt pricing, as Western government capital is deployed to secure supply chains rather than rely on open-market mechanisms.

- Structural demand from electrification, covering electric vehicles, grid-scale storage, and transmission infrastructure, remains intact and is projected by the International Energy Agency to drive multi-decade copper demand growth that the existing development pipeline cannot accommodate.

- Jurisdictional re-rating is creating a measurable premium for assets in Organisation for Economic Co-operation and Development mining jurisdictions, with Quebec's 7th-place ranking on the 2025 Fraser Institute Policy Perception Index providing a quantified basis for discount rate differentiation versus politically exposed assets.

- High-grade deposits offer disproportionate margin protection in a cost-inflationary environment, as the 20 to 35% increase in all-in sustaining costs since 2021 is compressing returns at median-grade assets while leaving first-quartile projects with robust economics above $4.00 per pound copper.

- Exploration upside in assets such as Abitibi Metals' B26 deposit provides asymmetric return potential, as resource growth from the current 25-plus million tonne base toward the 30 to 50 million tonne target would trigger valuation re-ratings consistent with the threshold scale required by major producers for acquisition interest.

The $700 million US acquisition of Congolese copper-cobalt assets is a signal, not an isolated transaction, confirming that Western governments have concluded asset ownership is the only reliable hedge against critical mineral supply chain risk. That conclusion, once operationalized through government capital, changes the investment calculus for every institution allocating to the copper sector.

The near-term price environment will remain volatile as Chinese demand elasticity and elevated inventories cap upside through 2026. But the structural argument for copper is not a near-term trade; it is a multi-decade realignment between the energy transition's material requirements and a supply pipeline that is jurisdictionally constrained, geopolitically fragmented, and financially under-resourced. Investors positioning now in Tier-1 assets with scalable resources, confirmed feasibility economics, and alignment with Western supply-chain security mandates are not speculating on a commodity cycle, they are allocating ahead of a structural deficit the existing project pipeline cannot resolve.

TL;DR

The US-backed $700 million acquisition of Congolese copper-cobalt assets marks a decisive shift in how Western governments approach critical mineral security, moving from market reliance to direct asset ownership. While near-term copper prices remain range-bound around $12,600 per tonne due to softening Chinese demand and elevated inventories, the structural case for copper is intact, driven by electrification demand, a constrained development pipeline, and accelerating capital rotation toward high-grade assets in stable jurisdictions like Quebec. Investors aligned with Tier-1, scalable, and feasibility-ready projects are positioning ahead of a structural deficit the existing supply pipeline cannot resolve.

FAQs (AI-generated)

The $700 million Virtus Minerals deal reflects a strategic conclusion by the US government that open-market mechanisms are no longer a reliable hedge against critical mineral supply chain risk. The DRC holds roughly 70% of global cobalt supply and a growing share of copper production, assets that China's state-backed entities have controlled for over a decade. By deploying capital directly into asset acquisition and tying resource access to the December 2025 Washington Peace Agreement, the US is treating mining stakes as instruments of foreign policy. The acquisition secures approximately 5% of global cobalt supply under Western-aligned ownership, a narrow foothold, but a meaningful precedent that is already reshaping how institutional capital prices geopolitical risk across the entire copper sector.

The financial market is pricing a multi-year scarcity thesis driven by electrification demand, but the physical market is currently registering surplus conditions, a dislocation that is capping near-term upside. Chinese copper imports fell approximately 25% year-over-year in early 2026 as spot prices above $12,000 per tonne triggered demand destruction at the margin, while LME warehouse stocks reached multi-year highs. This pattern is consistent with prior cycles: elevated prices cause Chinese end-users in construction and electronics to defer purchases, creating temporary inventory builds that suppress spot prices. Structural electrification demand is not disappearing, it is being deferred at the margin, and analysts expect the physical market to tighten meaningfully once the development pipeline's constraints become apparent, likely from 2027 onward.

Capital markets are applying higher discount rates to politically exposed assets and premium valuations to projects in OECD jurisdictions, a measurable jurisdiction premium that is reshaping investment frameworks across the sector. Permitting timelines in several Latin American and African jurisdictions have extended to 7-12 years, which can compress a project's IRR from 25% to below the 15% institutional threshold purely on schedule risk, regardless of underlying grade. The practical consequence is that predictability of the development timeline now carries as much weight in project economics as the deposit's intrinsic quality. Assets in stable jurisdictions like Quebec, which ranked 7th on the 2025 Fraser Institute Policy Perception Index, are gaining a structural valuation advantage that is unlikely to reverse given the trajectory of US, EU, and allied critical minerals policy.

All-in sustaining costs have risen to $2.80-$3.60 per pound at feasibility base cases, up from $2.20-$2.80 per pound at the prior cycle peak, and project finance is now priced 200-300 basis points above prior-cycle levels. In this environment, only projects in the lower quartile of the cost curve, high grade, simple metallurgy, proximate to infrastructure, retain investment-grade economics. Projects in the second and third quartiles face IRR compression that may not be recoverable without copper prices above $4.50 per pound. Marimaca Copper's definitive feasibility study, stress-tested at a conservative $4.30 per pound base case, illustrates what investor-grade economics look like today: confirmed industry-leading capital cost intensity, primary permits secured, and a construction start targeted for 2026, positioning first production squarely in the 2027-2028 window when physical market tightness is expected to reassert.

Major copper producers are carrying reserve-to-production ratios at decade lows, while organic exploration is yielding fewer large discoveries per dollar spent than at any point since the 1990s. Against that backdrop, a scalable, high-grade deposit in a stable jurisdiction represents exactly the category of asset that commands acquisition premium; it solves the reserve replenishment problem without adding geopolitical or permitting risk. Abitibi Metals' B26 polymetallic deposit in Quebec, currently sitting at 25-plus million tonnes grading 2.1-2.2% copper equivalent, with a potential resource target of 30-50 million tonnes, is a case study in how exploration upside interacts with jurisdictional security to create asymmetric return potential. A deposit reaching the 30-50 million tonne threshold would cross the scale threshold major producers typically require for serious acquisition interest, making the 2026 drill program a meaningful value catalyst.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed