Mine Supply Disruptions & Section 232 Tariff Risk Tighten Copper Markets Ahead of a Forecast 600,000-Tonne 2026 Deficit

Mine disruptions, US tariff risk, and sulfuric acid shortages are tightening copper supply as banks forecast a 600,000-tonne 2026 deficit.

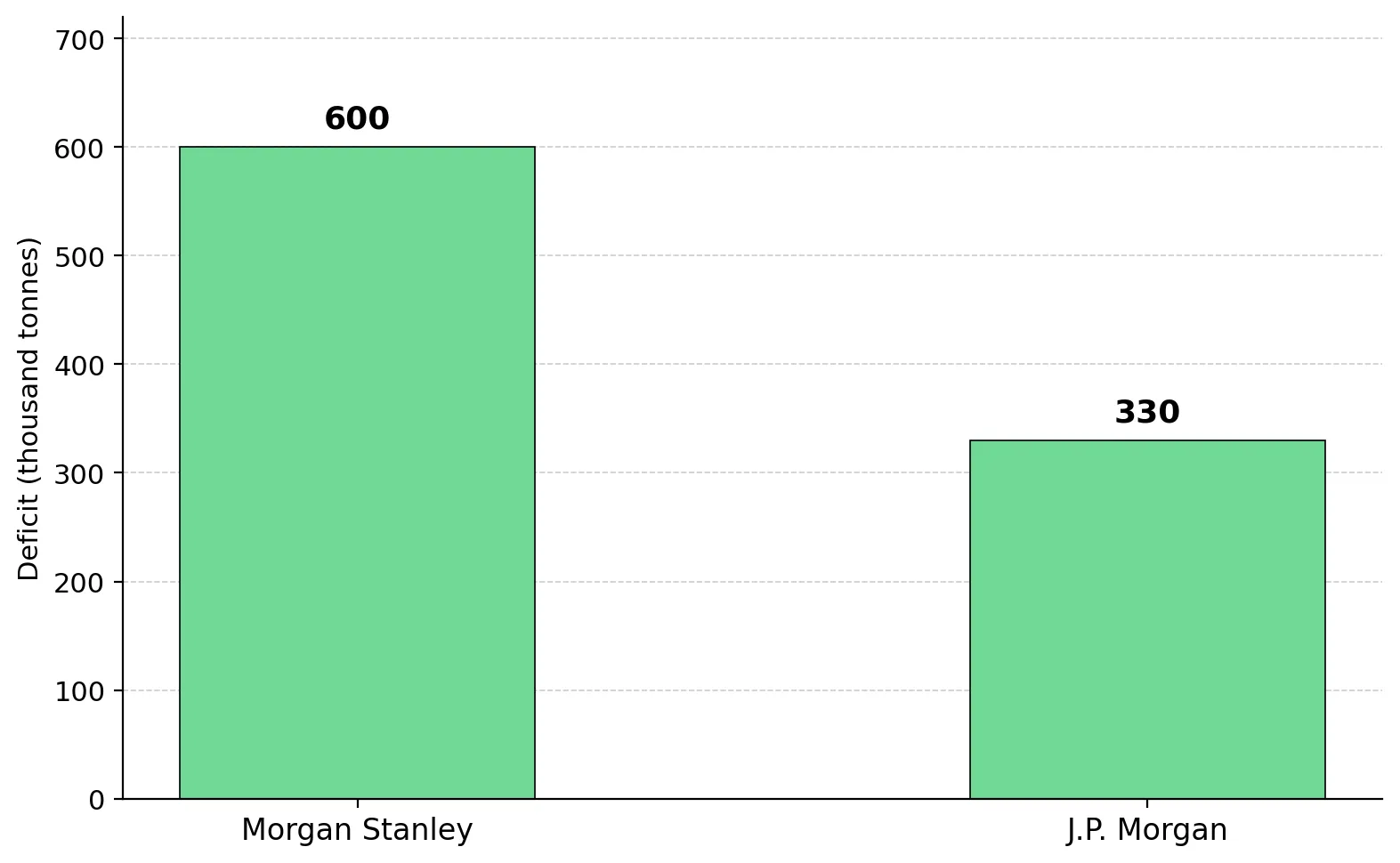

- Morgan Stanley forecasts a 600,000-tonne refined copper deficit in 2026, the largest in more than 20 years. J.P. Morgan forecasts a 330,000-tonne deficit, while the International Copper Study Group revised its 2026 balance from a 209,000-tonne surplus in October 2025 to a 150,000-tonne deficit in May 2026, reinforcing the institutional view that mine supply can no longer meet demand growth.

- Chile's national copper output fell 9.04% year-on-year in March 2026 to 434,314 tonnes, according to Cochilco. Codelco output declined 10%, BHP's Escondida fell 15.75%, and the Glencore-Anglo American Collahuasi joint venture declined 10.80%, reducing supply from the world's largest copper-producing country and reinforcing the 2026 global deficit outlook.

- COMEX three-month copper reached a record $6.65 per pound on May 13, 2026, equivalent to $13,650 per tonne on the LME, before consolidating around $13,100 to $13,400 per tonne as traders repositioned ahead of the US Section 232 copper tariff decision.

- Major investment banks now forecast copper prices above historical averages as supply disruptions tighten the 2026 market balance. J.P. Morgan targets average Q2 2026 prices of $12,500 per tonne, Citigroup sees a path to $15,000 per tonne if the Strait of Hormuz reopens, and Goldman Sachs forecasts $10,000 to $11,000 per tonne in H1 2026.

- The projected copper deficit is directing investor capital toward developers and explorers with near-term production growth, resource expansion potential, or exposure to multiple critical minerals jurisdictions.

Mine Disruptions, US Tariffs & Energy Costs Tighten the Copper Market

Copper prices remained near record highs in late May 2026 as traders weighed supply disruptions against uncertainty around US copper tariffs. COMEX three-month copper settled near $6.43 per pound on May 25, 2026, equivalent to approximately $13,100 to $13,400 per tonne on the London Metal Exchange (LME). COMEX copper is up roughly 33.9% year-to-date versus the same period in 2025 as mine disruptions tightened global supply expectations. Prices are being driven simultaneously by mine supply disruptions, US tariff risk, and higher sulfuric acid and energy costs tied to the Middle East conflict.

The first driver is supply disruption in Chile, Indonesia, and the Democratic Republic of Congo, which together account for a large share of global copper production. Chile's copper output declined 9.04% year-on-year in March 2026, according to Cochilco. Freeport-McMoRan's Grasberg mine in Indonesia delayed its full restart from 2027 to 2028, extending supply losses from one of the world's largest copper operations. Ivanhoe Mines' Kamoa-Kakula recovery in the Democratic Republic of Congo is being limited by sulfuric acid shortages needed for processing operations. Goldman Sachs Research forecasts a US refined copper tariff of at least 25% before mid-June 2026 under the Section 232 review, increasing the risk of further US inventory hoarding and higher domestic premiums. Higher energy costs linked to the Middle East conflict and China's May 2026 halt on sulfuric acid exports are increasing processing costs for copper producers. J.P. Morgan estimates the sulfuric acid shortage affects about 15% of global copper production.

Multi-Year Mine Disruptions Tighten Global Copper Supply

Copper supply disruptions are extending over multiple years rather than quarters, tightening global copper balances and pushing smelter treatment and refining charges toward zero or negative levels. Freeport-McMoRan's Grasberg mine in Indonesia delayed its return to full production from 2027 to 2028 after the September 2025 mudslide, while CNBC reported in March 2026 that the company cut 2026 production guidance by 35%. Ivanhoe Mines' Kamoa-Kakula project in the Democratic Republic of Congo is still recovering from 2025 flooding and also faces sulfuric acid shortages, with J.P. Morgan Global Research estimating the DRC imports about 80% of its sulfur supply through Middle East trade routes. Wood Mackenzie has increased its 2026-2028 copper supply disruption assumptions as confidence in near-term mine recovery timelines declines.

Sulfuric Acid Shortages Raise Costs for Oxide Copper Projects

J.P. Morgan Global Research estimates that China's May 2026 halt on sulfuric acid exports affects about 15% of global copper production that depends on acid-based processing, while spot sulfuric acid prices in Chile have risen to approximately $400 per tonne, increasing operating costs for oxide leach projects. On May 19, 2026, Marimaca Copper signed a non-binding MOU in Mejillones to evaluate a joint-venture sulfuric acid supply agreement using the Dos Amigos Acid Plant. The company's 2025 Definitive Feasibility Study valued the Marimaca Oxide Deposit at a pre-tax NPV8 of $1.1 billion using a $5 per pound copper assumption and planned annual production of 50,000 tonnes of copper cathode. Lower-cost acid supply could improve operating margins and project financing ahead of Marimaca's targeted final investment decision in early 2027.

Hayden Locke, President and Chief Executive Officer of Marimaca Copper, explained how self-supplied sulfuric acid could reduce operating costs versus spot market pricing:

“Today the spot price for sulfuric acid, because of what’s happening around Iran and the Strait of Hormuz, is more than $400 per tonne. On a self-produced basis, we believe we can produce acid for less than $250 per tonne.”

AI Infrastructure, Electrification & Defense Spending Support Copper Demand

Major investment banks continue to forecast large copper deficits despite weaker industrial activity in parts of China and Europe, with Morgan Stanley projecting a 600,000-tonne deficit in 2026, J.P. Morgan projected 330,000 tonnes, and Citigroup seeing prices reach $15,000 per tonne if shipping flows through the Strait of Hormuz stabilise, while Goldman Sachs Research forecasts a lower $10,000 to $11,000 per tonne range for H1 2026.

S&P Global Market Intelligence reported in April 2026 that AI data center construction is increasing copper demand because higher rack power density requires more electrical infrastructure, while defense spending and electrification demand continue to offset weaker industrial activity in China and Europe. The World Bank also maintained its energy-transition copper demand outlook through 2030 despite lowering near-term global GDP forecasts, while copper prices remain near record highs despite elevated US interest rates and a stronger US dollar.

Copper Supply Deficits Shift Investor Capital Toward Developers & Explorers

Forecast copper shortages are pushing investors toward developers and explorers that could add new supply over the next several years. Construction-stage developers, resource-conversion explorers, and maiden-resource companies all offer exposure to higher copper prices, but each group carries different financing, permitting, and geological risks. The Section 232 tariff review is also increasing investor preference for projects in North American and allied mining jurisdictions.

Chile Output Declines Increase Focus on Mid-Tier Copper Developers

Chile's production decline is increasing investor interest in mid-tier copper developers that can advance without major mining company funding. Marimaca Copper is progressing permitting, financing, and engineering work ahead of a targeted construction decision, with Environmental Approval secured in November 2025, Sectorial Permit approvals targeted for Q4 2026, and approximately $160 million in cash following a C$409 million financing completed in February 2026.

Fitzroy Minerals is advancing drilling and economic studies at the Buen Retiro Copper Project near Copiapó, where 39 drill holes totaling 6,885 metres since February 2026 support a maiden resource estimate and drill hole BRT-DDH059 returned 78 metres grading 1.70% copper, including 40 metres grading 3.02% copper. Fitzroy's partnership with Pucobre could support a heap leach operation that generates early cash flow without requiring a standalone mine build.

Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, explained how the partnership with Pucobre could lower development costs and accelerate cash flow generation:

“We’re looking at a heap leach joint venture with Pucobre, which is a proven operator with existing infrastructure advantages. The structure could generate non-operated cash flow with very low capital intensity.”

Section 232 Tariff Risk Increases Interest in North American Copper Projects

The Section 232 tariff review is increasing investor interest in North American copper projects, particularly in Quebec and Yukon. Abitibi Metals' B26 Copper-Gold Project in Quebec hosts 25 million tonnes grading 2.1% copper equivalent, while Phase 4 drilling returned a 150-metre step-out intercept grading 2.71% copper equivalent over 7 metres. The 2026 drilling program is focused on resource expansion and upgrading inferred resources ahead of a Preliminary Economic Assessment. Abitibi also closed a C$30.75 million financing in May 2026, with Discovery Silver taking a 9.9% stake, leaving the company with more than C$45 million in cash to fund over 80,000 metres of drilling.

Jonathon Deluce, President and Chief Executive Officer of Abitibi Metals, explained how the company's drilling program balances near-term economic studies with long-term resource expansion:

“Our goal is to deliver both a PEA and an updated resource. The PEA work is focused on near-surface material and early project payback, while the broader drilling program is testing how large the deposit can become and how that supports long-term mine life.”

Yukon Copper Resource Expansion Advances Toward Updated Resource Estimate & PEA

Selkirk Copper is expanding resources and advancing economic studies at the Minto Project in Yukon, where Phase 1 drilling intersected copper-gold-silver mineralisation in 87% of holes, including the discovery of the 117 Lens beneath the historic Area 2 open pit. The 2025 Mineral Resource Estimate includes 12.59 million tonnes of Indicated resources grading 1.20% copper and 23.66 million tonnes of Inferred resources grading 1.05% copper. Selkirk is targeting an updated Mineral Resource Estimate and Preliminary Economic Assessment in mid-2026, while Phase 2 drilling launched on May 1, 2026 with a target of up to 50,000 metres by November.

M. Colin Joudrie, President and Chief Executive Officer of Selkirk Copper Mines, explained why Selkirk is prioritising technical validation and permitting work before accelerating development plans:

“Our approach is to measure twice, cut once. We are not going to compromise the long-term viability of the project by missing permitting requirements or underground technical issues during the early study phase.”

Rare Earth Supply Concentration Expands Interest in Australian Critical Minerals Projects

Copper and rare earth supply shortages are increasing Western interest in non-Chinese critical minerals projects, particularly as China controls more than 90% of global dysprosium and terbium supply according to Shanghai Metals Market data. Cobra Resources is advancing rare earth and copper projects in South Australia, where in-situ recovery testing at the Boland Rare Earth Project achieved 66% heavy rare earth recovery with the lowest acid consumption among six peer projects and a mixed rare earth carbonate basket value of $65.22 per kilogram, the highest among 10 benchmarked ionic rare earth projects. Cobra's Manna Hill Copper Project adds copper exposure alongside its rare earth assets, while the company maintains a market capitalization of approximately £50 million.

The Investment Thesis for Copper

- Major financial institutions now forecast copper deficits in 2026, with Morgan Stanley projecting a 600,000-tonne shortfall, J.P. Morgan projecting 330,000 tonnes, and the International Copper Study Group projecting 150,000 tonnes. Goldman Sachs remains more conservative on copper prices than its peers despite the tightening supply outlook.

- Copper supply disruptions are concentrated in Chile, Indonesia, and the Democratic Republic of Congo, with recovery timelines now extending over several years rather than quarters. Simultaneous disruptions across major mines reduce the market's ability to offset production losses from individual operations.

- The US Section 232 tariff decision due before mid-June 2026 could sharply affect copper prices and increase investor interest in North American copper projects. Goldman Sachs Research estimates that tariffs of 25% or higher would widen the CME-to-LME spread by $0.30 to $0.80 per pound.

- Investors are valuing copper companies differently based on project stage, with construction-ready developers, resource-conversion explorers, and maiden-resource explorers each carrying different financing, permitting, and exploration risks.

- Higher sulfuric acid and energy costs are increasing the advantage of copper developers that control acid supply or already own processing infrastructure. Companies with brownfield assets or self-supply capacity may achieve lower operating costs and stronger project financing terms than developers that rely on third-party infrastructure.

Mine supply disruptions, the pending Section 232 tariff decision, and sulfuric acid shortages linked to the Middle East conflict are simultaneously tightening the copper market. Major banks now forecast some of the largest copper deficits in more than a decade. Investors are differentiating copper companies by project stage, with construction-ready developers, economic-study-stage companies, and early exploration projects each carrying different financing, permitting, and geological risks. The Section 232 tariff decision before mid-June 2026 is the next major catalyst for copper prices and mining equities. The decision will help determine whether supply shortages and regional trade disruptions continue to tighten the copper market through 2026.

TL;DR

Mine disruptions in Chile, Indonesia, and the Democratic Republic of Congo, combined with US Section 232 tariff risk and sulfuric acid shortages linked to the Middle East conflict, are tightening the global copper market and pushing prices near record highs. Morgan Stanley forecasts a 600,000-tonne copper deficit in 2026, while banks including J.P. Morgan and Citigroup expect supply shortages to support elevated prices despite weaker industrial activity in China and Europe. Investors are increasingly shifting toward copper developers and explorers with near-term production growth, resource expansion potential, and exposure to stable mining jurisdictions such as Canada, Chile, and Australia.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed