Vista Gold's 2026 Playbook: Permits, People, and a Path to Production

After two decades and multiple owners, Vista Gold's Australian gold project enters execution mode with a leaner design, oversubscribed financing, and a CEO convinced the market is mispricing the opportunity.

Frederick Earnest has heard the skepticism before. Mt Todd has had multiple owners over its roughly two-decade history. One tried heap leaching and achieved only 52% recovery. Another built a conventional mill but faced falling gold prices and crushing equipment failures. When Vista Gold acquired the project in 2006, it inherited both the geology and the baggage.

Twenty years later, Earnest believes the timing has finally aligned. Gold prices are at record highs. The project has been rightsized for capital efficiency. Permits are substantially in place. And institutional investors just voted with their wallets, oversubscribing a $39 million financing by two-to-one.

Yet Vista's market capitalisation sits at roughly $350 million - a third of what comparable Australian junior gold producers command, even those with lower production profiles. Earnest said at PDAC 2026,

"Our valuation today, it's about $350 million. And the lowest valued junior producer, somebody producing less than 150,000 ounces of gold per year, is like a billion dollars."

Closing that gap is the investment case. And Vista's plan for 2026 is designed to trigger the re-rating.

The Rescoping

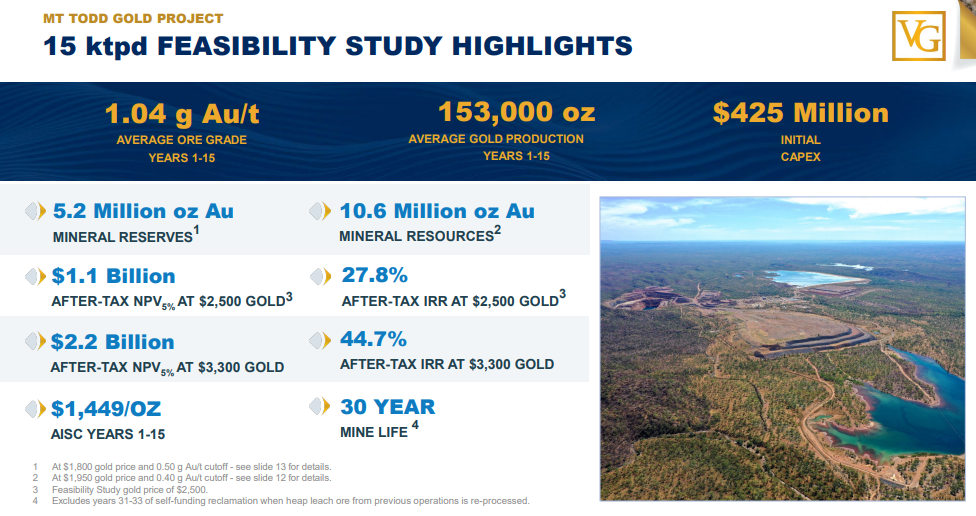

Vista's 2025 feasibility study was an exercise in discipline, not ambition. The company took a 50,000-tonne-per-day design requiring $1.03 billion in upfront capital and rescoped it to 15,000 tonnes per day at $425 million - a 59% reduction. The trade-off was straightforward: prioritise grade over tonnage, accept a longer mine life, and eliminate capital that doesn't directly contribute to getting gold out of the ground.

The revised plan targets 153,000 ounces annually over the first 15 years at an average grade of 1.04 grams per tonne, feeding a conventional mill with contract mining and third-party power. The operation carries 5.2 million ounces of proven and probable reserves across a 30-year mine life. All-in sustaining costs are estimated at $1,449 per ounce, leaving substantial margin at current prices.

Mid-tier and senior producers who've reviewed the design told Vista the same thing: 15,000 tonnes per day is exactly the right approach to get Mt Todd built. But it's also below the threshold for immediate acquisition appeal. Vista anticipated that. The company designed expansion capacity into the flowsheet, allowing future scaling to 22,500, 30,000, or even 45,000 tonnes per day without significant re-engineering. Earnest sees two value pathways: organic execution through to production, or strategic interest once the project de-risks and expansion potential becomes concrete.

"We've done our homework. We've selected the equipment and it's all about right sizing it and moving forward," Earnest said, noting that the crushing circuit mirrors those at Boddington and Cadia Valley - two of the world's most reliable large-scale gold operations.

The 2026 Workplan

Vista has three priorities this year, each feeding into a 2027 detailed engineering start. Permitting comes first. The original approvals were based on the 2018, 50,000-tonne-per-day design. Subsequent drilling, higher gold prices, and design changes require amendments. Northern Territory permits are expected by year-end. A federal authorisation will take 14 to 16 months. An approvals manager has been hired and is relocating to the Northern Territory to run the process.

Simultaneously, Vista is building an executive team in Perth - 8 to 10 people to manage development and operations. Three of the first six hires have already started. The broader operational workforce will be based in the Northern Territory on a fly-in, fly-out basis, consistent with Australian mining norms.

On the technical side, metallurgical testing is underway with core drilled in January now at the lab. A geotechnical program launching within weeks could support steepening the west pit wall, potentially reducing the strip ratio and improving economics. GR Engineering Services, the lead feasibility consultant, estimates 27 months from detailed engineering start to first gold pour. If Vista hits its 2027 target, production could begin in 2029.

Interview with Frederick H. Earnest, President & CEO of Vista Gold

Capital and Conviction

The oversubscribed financing wasn't just about raising money - it was a market signal. Approximately a dozen large U.S. and Canadian institutions participated, including both existing shareholders and new names. The share price closed up 9 cents the day pricing was announced.

"We announced the plan, people knew that we needed money to execute. Now we have the money. And does that start us on the next step of the re-rate?"

For construction financing, Vista is working with Endeavour Financial on a debt structure that could include conventional bank loans, the Northern Australia Infrastructure Fund (a quasi-government vehicle offering longer-tenor capital), and potentially a streaming arrangement with Wheaton Precious Metals, with whom Vista already has a relationship. Earnest indicated the project could support 60–65% debt-to-total-capital, though the company is keeping options open. An ASX listing is also under evaluation to broaden the investor base and improve liquidity.

The economics have improved materially since the feasibility study, which was modeled at a conservative $2,500 per ounce gold price. At current spot prices, Vista estimates construction debt payback in roughly 18 months. After-tax NPV at $2,500 gold is $1.1 billion with a 27.8% IRR. At $3,300 gold, those figures jump to $2.2 billion and 44.7%.

What Comes Next

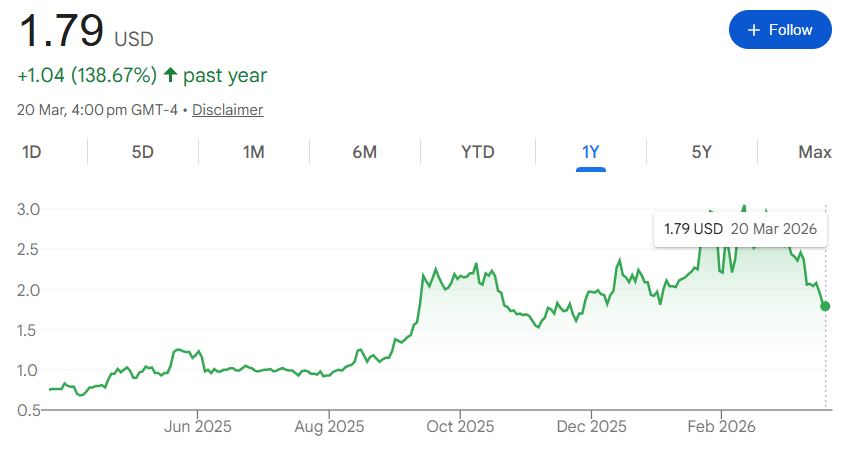

Vista's share price is up 138% over the past year, ranking fourth among 15 peer developers over the two-year period leading into PDAC 2026. The market is starting to pay attention, but Earnest believes the real inflection point comes when Vista transitions from developer to builder.

The catalysts are lined up: Northern Territory permits by year-end, geotechnical results mid-year, federal authorisation in early 2027, and a construction financing package to follow. Each milestone reduces execution risk. Each de-risking step historically triggers valuation multiple expansion for projects of this scale in tier-one jurisdictions.

Mt Todd has been around for two decades, but Vista's current iteration has been in place for less than a year. The feasibility study is complete. The capital stack for 2026–2027 is funded. The team is being assembled. The permits are advancing. For the first time, the company isn't optimising for size - it's optimizing for speed.

Whether the valuation gap closes before construction or after first gold depends on how cleanly Vista executes. But after 20 years of false starts and ownership changes, the project finally has a plan built not for headlines, but for delivery.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed