What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 5

Uranium demand rising 5.3-7.6% annually to 2040 while existing mines cover only 40% of 2035 demand. Geopolitical shifts favor Western jurisdictions and SMR growth.

- Global uranium demand is set to rise 5.3–7.6% annually to 2040, driven by reactor buildouts in Asia and the accelerating rollout of Small Modular Reactors (SMRs).

- Primary supply is unable to keep pace, with existing mines covering just 40% of reactor demand by 2035, leaving a deepening unspecified supply gap.

- Geopolitical tensions from the Niger junta to Russian enrichment restrictions have fractured global uranium supply chains, amplifying price volatility and reshaping sourcing strategies.

- Companies with Tier-1 projects in stable jurisdictions and near-term production or permitting visibility are positioned to capture premium valuations.

- The next uranium bull phase will likely reward jurisdictional safety, permitting readiness, and exposure to Western fuel cycles over pure resource scale.

Demand Expansion Meets Energy Security: The Repricing of Nuclear Power

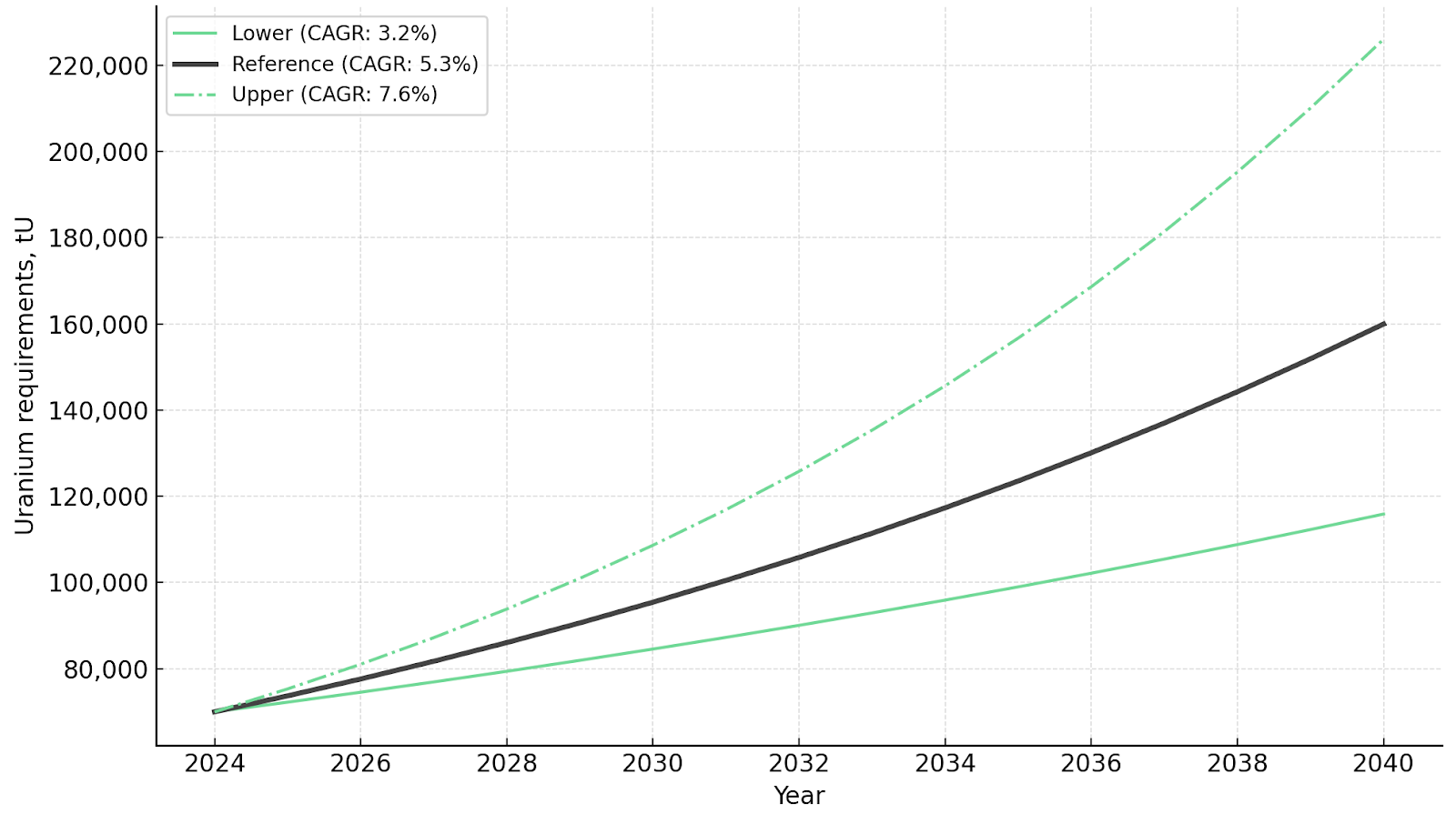

Global uranium demand is entering a structural growth phase. The World Nuclear Association (WNA) projects reactor requirements to expand at a 5.3% compound annual growth rate (CAGR) under its Reference Scenario, and up to 7.6% CAGR under its Upper Scenario through 2040. The majority of this growth is concentrated in East Asia (China, South Korea), South Asia (India), and North America, reflecting both energy transition targets and domestic supply security policies.

SMRs introduce a new layer of demand elasticity. By 2040, up to 35,800 tonnes of uranium (tU) per year could be attributed to SMR deployment, a figure not included in legacy demand models. SMRs' smaller footprint and modular design lower entry barriers for new markets, extending uranium's demand profile beyond traditional power economies. The Reference Scenario projects SMR-related uranium demand reaching 17,000 tU per year by the end of the next decade, with the Upper Scenario envisaging even more rapid deployment from 2030 onward.

The combination of traditional reactor expansion and emerging SMR deployment creates a bifurcated demand profile that requires exploration across multiple jurisdictions to meet long-term fuel requirements. ATHA Energy holds the largest exploration land position in Canada, with projects across the exploration risk curve in the Athabasca Basin. Troy Boisjoli, Chief Executive Officer of ATHA Energy, emphasizes the unprecedented market conditions:

"The macro environment in the uranium sector is unequivocally unlike any time I've seen in my career. The sentiment, the real demand that's being built up coupled with some of the supply side risk is a setup, a structural setup like we have not seen in the uranium space."

As nations prioritize energy independence and grid stability, nuclear's baseload reliability and zero-carbon footprint have become strategic imperatives. For investors, this is not merely a policy story but a supply-chain recalibration that redefines long-term uranium pricing floors.

The Supply Crunch Deepens: Declining Production Meets Depletion Risk

While demand accelerates, primary production is falling behind. WNA data shows that existing mines currently meet over 90% of demand, but this figure drops to just 40% by 2035 as legacy assets deplete. The global production of 60,213 tU in 2024 represents a recovery from the 2020 trough, yet remains 5% below the 2016 output of 63,207 tU. In the Reference Scenario, production from existing mines declines from 62,642 tU in 2025 to 46,834 tU by 2035.

Many of the world's largest producers, including Cameco, Kazatomprom, and Orano, have reduced guidance due to operational delays, cost inflation, and regulatory friction. The sharp rise in input and capital costs post-COVID has widened the gap between project feasibility and profitability. Global exploration and mine development expenditure declined by 88% from 2014 to 2020, bottoming at $377 million before recovering to $840 million in 2023.

This structural undersupply introduces the concept of unspecified supply, the material gap between identified sources and actual reactor requirements. It encompasses potential mine restarts, secondary inventories, re-enrichment of tails, and yet-to-be-developed projects. In the Reference Scenario, unspecified supply needs reach 74,507 tU by 2040, while the Upper Scenario projects this gap at 122,853 tU. Global Atomic's Dasa Project in Niger represents one such near-term production catalyst. Stephen Roman, Chief Executive Officer of Global Atomic, quantifies the timeline:

"They're burning 50 million pounds a year, they're making with everything ramped up maybe four or five million pounds a year in the United States. So there's a big delta there."

It should be recognize that uranium mining projects typically require 10–20 years from discovery to commercial production, creating a prolonged lag in supply response even as prices rise. The development pipeline remains shallow relative to forecast demand, showing mines under development representing only 3,594 tU of expected capacity, while planned and prospective mines add 10,153 tU and 20,186 tU respectively.

Geopolitical Realignment: The Fracturing of the Global Uranium Market

The uranium trade, once relatively insulated from geopolitics, is now exposed to systemic fragmentation. The Russia-Ukraine war disrupted underfeeding and tails re-enrichment flows, removing a key source of flexible secondary supply. Simultaneously, Niger's 2023 coup introduced sovereign risk into 25% of the European Union's uranium imports, triggering procurement diversification across Western utilities.

Meanwhile, Kazakhstan accounts for over 40% of global uranium production, has shifted to a value-over-volume strategy, intentionally curbing output to support market stability. This strategic discipline mirrors Organization of the Petroleum Exporting Countries-like coordination, adding further rigidity to global supply. Kazakhstan's uranium production is expected to rise in the near term, mostly driven by the ramp-up of Budenovskoye 6 & 7, but projections indicate a decline through the 2030s as several major sites face resource depletion.

The strategic advantage of domestic processing capacity becomes particularly pronounced as Western nations seek to reduce dependence on geopolitically volatile supply sources. Energy Fuels holds two uranium processing facilities, including the only conventional uranium mill operating in the United States. Mark Chalmers, President and Chief Executive Officer of Energy Fuels, addresses market dynamics and demand urgency:

"It shows that they're starting to panic. It shows that they're trying to take a position before somebody else takes a position… It's the tech companies that realize they need the power, they need the base of energy."

These developments have prompted the United States, European Union, and allied nations to accelerate domestic enrichment and conversion initiatives, reshaping the global uranium trade network. The ban on imports of Russian uranium to the United States, coupled with continued bipartisan support for domestic front-end fuel production capacity, reflects the strategic imperative to secure supply chains. Companies with assets in Canada, the United States, and Australia, backed by stable regulatory regimes, are increasingly seen as strategic suppliers of last resort.

Cost Inflation & Operational Discipline: The Price Floor Rises

Sustained cost inflation in diesel, reagents, steel, and labor has redefined uranium's economic floor. Inflationary input costs and disciplined producer strategies push long-term prices sustainably higher, due to the significant increase in mining and capital costs observed globally since the Covid-19 pandemic. The OECD Nuclear Energy Agency and International Atomic Energy Agency identify recoverable resources in cost categories ranging from under $40 per kilogram of uranium (kgU) to above $260 per kgU, with identified resources totaling approximately 7.9 million tU as of 2023.

At the same time, industry leaders like Kazatomprom and Cameco have prioritized supply discipline over rapid expansion, adopting capital allocation frameworks reminiscent of post-2014 gold producers. This emphasis on shareholder returns and project optionality rather than volume maximization has contributed to supply rigidity. In-Situ Recovery (ISR) mining has increased significantly to over 50% of industry production, compared to 15% in 2000, with Kazakhstan developing and expanding the technique to achieve scalable economics and low operating costs.

These dynamics suggest uranium's cyclical lows will remain structurally higher. Cost floors have moved upward, while geopolitical risk premiums have expanded the incentive price band for new projects. The rising cost environment reinforces the value proposition of assets in jurisdictions with proven permitting pathways and existing infrastructure access.

Long Lead Times & Project Maturity: Where the Bottlenecks Lie

The development pipeline remains shallow relative to forecast demand. WNA data categorizes projects into distinct maturity stages, each with different probability profiles and timelines. Existing mines, currently operating, face near-term depletion at many sites. Idled mines remain technically ready but economically challenged at prevailing price levels. Mines under development have reached construction or pre-strip phases post-Final Investment Decision (FID). Planned mines have completed feasibility but await permits or funding. Prospective mines require significant feasibility and permitting work, representing 10–20-year development horizons.

This structure underscores why advanced-stage developers hold outsized strategic value. Permitting-ready projects and licensed ISR operations are now rare assets in a supply-constrained market. The United States uranium mining industry is expected to recover in the near future, with several further idled mines returning to production and new projects starting throughout the forecasting period.

Domestic policy support for uranium production has intensified as energy independence becomes a national security priority alongside decarbonization commitments. The scarcity of operating production capacity globally amplifies the strategic value of companies with functioning infrastructure.

enCore Energy operates two Central Processing Plants (Rosita and Alta Mesa) in Texas, with ISR operations. The company's infrastructure advantage and restart readiness position it to respond quickly to market demand in a supply-constrained environment. William Sheriff, Executive Chairman of enCore Energy, describes the producer supply constraint:

"The entire world's nuclear utility business is here at least in some form or fashion with few exceptions… There aren't too many producers, so in fact there's a real shortage of them."

Laramide Resources holds active Nuclear Regulatory Commission (NRC) licenses and late-stage, low technical-risk assets acquired for their size and production potential. The company's Churchrock-Crownpoint project benefits from NRC license renewal, shortening its path to production.

IsoEnergy's Utah portfolio includes key permits in place, enabling near-term restart optionality across multiple sites. The company's diversified asset base spans the risk curve from advanced exploration in the Athabasca Basin, which hosts one of the highest-grade published indicated uranium resources in Canada, to restart-ready ISR operations in the United States. This multi-horizon approach provides exposure to both near-term production economics and long-term exploration upside across Tier-1 jurisdictions.

Global Atomic's Dasa Project in Niger demonstrates the leverage available in advanced-stage development assets, with a 57% IRR and net present value at 8% discount rate (NPV8%) of $917 million, highlighting the project's sensitivity to price normalization. However, the recent political instability in Niger underscores jurisdictional risk, even for technically strong projects.

Jurisdictional Realignment: Premium on Predictability

As geopolitical volatility increases, investors are applying jurisdictional premiums to stable regions like Canada, the United States, and Australia. This shift mirrors trends seen in copper and gold markets, where security of tenure and permitting certainty now outweigh resource size in valuation models. The distribution of uranium resources by country shows Australia hosting the largest volume (24% of total), followed by Kazakhstan (11%) and Canada (11%).

ATHA Energy is Canada's largest uranium exploration landholder with over 7 million acres strategically positioned across the Athabasca Basin, Thelon Basin, and Central Mineral Belt. The company's Angilak Project features the Lac 50 Deposit, one of the highest-grade deposits globally outside of the Athabasca Basin, with a 31-kilometer structural corridor identified with potential for multiple discoveries.

F3 Uranium is expanding the Tetra Zone in Saskatchewan, reinforcing the Athabasca Basin's reputation for world-leading grades. The grades in the Athabasca Basin are approximately 10 to 20 times the global average, making exploration discoveries in this jurisdiction particularly valuable from a resource quality perspective.

American Uranium holds a portfolio of assets in two of the top United States uranium districts: Wyoming and Utah. The company’s strategy centers on developing low-cost in-situ recovery (ISR) uranium projects in Wyoming, leveraging existing infrastructure, past production, and historical resources. Its flagship Lo Herma project in the Powder River Basin hosts a JORC resource of 8.57 million pounds of U₃O₈, contributing to a total uranium inventory of 10.23 million pounds across its holdings at Great Divide Basin and Green Mountain areas of Wyoming, alongside early-stage conventional uranium–vanadium assets in Utah. Positioned within a supportive regulatory environment and amid a growing U.S. uranium supply deficit, the company is well placed to benefit from strong bipartisan backing for domestic uranium production.

Myriad Uranium's Copper Mountain project in Wyoming leverages historic resources and proven permitting pathways. The company benefits from decades of historical work and extensive data, including the $86 million in historic spend (in 2024 dollars) at the project, providing a low-risk path to significant uranium resources in the United States.

This jurisdictional reshuffling suggests that long-term capital will favor predictability and Environmental, Social, and Governance (ESG) alignment, both of which underpin premium valuations in Western markets. Projects in mining-friendly jurisdictions with transparent regulatory frameworks and established infrastructure increasingly command higher multiples relative to resource scale alone.

Diversification & Secondary Supply: Expanding the Value Chain

The uranium ecosystem is widening beyond mining. Companies like Energy Fuels are vertically integrating into rare earths, titanium, zircon, and medical isotopes, leveraging processing infrastructure at White Mesa Mill. This diversification positions them to capture additional critical mineral incentives from United States policy frameworks, including support for domestic rare earth element production and processing capabilities.

Secondary supply sources, including enrichment tails, inventory drawdowns, and recycling, are finite and face increasing constraints. The post-2022 sanctions environment has constrained Western access to Russian enrichment capacity, emphasizing the scarcity of re-enrichment options. Specified secondary supply forms a small portion of uranium supply in the period 2024 to 2040 in all three WNA scenarios, composed of United States Department of Energy material inflows (including re-enriched tails from Global Laser Enrichment), global excess uranium and mixed oxide inventories, and Japanese fresh fuel stocks drawdown.

Integrated uranium producers are expanding beyond traditional mining to capture value across multiple critical mineral supply chains. As these parallel markets mature, integrated uranium producers are expected to trade at valuation premiums due to their exposure to multiple energy transition commodities.

The Investment Thesis for Uranium

- Structural demand certainty is established through reactor construction pipelines and SMR deployment, creating durable multi-decade uranium requirements projected to reach 150,525 tU annually by 2040 in the Reference Scenario.

- Primary mine depletion and 10–20-year development cycles create persistent undersupply, with existing mine production expected to decline from over 90% of current demand to just 40% by 2035.

- Supply concentration in high-risk regions increases premiums for North American and Australian assets, as geopolitical fragmentation reshapes procurement strategies and utilities seek supply chain resilience.

- Inflationary input costs and disciplined producer strategies push long-term prices sustainably higher, due to the significant increase in mining and capital costs observed globally since the Covid-19 pandemic.

- Projects in Canada, the United States, and Australia benefit from ESG transparency and political stability, commanding jurisdictional premiums as investors prioritize permitting certainty and regulatory predictability.

- Developers with permitted or near-production assets such as IsoEnergy, Global Atomic, F3 Uranium, and Laramide Resources offer asymmetric upside through reduced development risk and accelerated production timelines.

- Vertically integrated producers like Energy Fuels and large landholders like ATHA Energy are positioned for multi-commodity leverage, capturing value across the nuclear fuel cycle and related critical mineral markets.

The Next Phase of Uranium's Repricing Cycle

The uranium sector has transitioned from a recovery narrative to a structural revaluation story. Demand acceleration, geopolitical bifurcation, and supply immobility have aligned to elevate uranium's long-term price floor and strategic importance. The convergence of reactor buildouts in Asia, SMR deployment across diverse markets, and Western energy security initiatives creates a demand profile unprecedented in the nuclear fuel cycle's history.

For investors, the takeaway is clear. The market's next phase will favor jurisdictional security, permitting readiness, and disciplined capital allocation. Companies positioned in Tier-1 jurisdictions with advanced-stage projects, existing infrastructure, or near-term production visibility are likely to capture premium valuations as the supply deficit widens through 2035 and beyond. The energy transition is no longer a distant driver but the foundation of uranium's sustained investment case, supported by policy frameworks prioritizing domestic fuel cycle independence and decarbonization commitments that require nuclear baseload generation at scale.

Read more:

Part 2 - Nuclear Energy Security Imperatives

TL;DR

Uranium markets face a structural supply-demand imbalance through 2040. Reactor requirements are projected to grow 5.3-7.6% annually, driven by Asian buildouts and Small Modular Reactor deployment, while existing mine production will decline from meeting 90% of current demand to just 40% by 2035. Geopolitical fragmentation following the Russia-Ukraine war and Niger's coup has disrupted traditional supply chains, creating premiums for Western jurisdictions. Rising input costs have elevated project economic thresholds from $60 to $75-$80 per pound. Companies with advanced-stage projects in Canada, the United States, and Australia, combined with near-term production visibility or existing infrastructure, are positioned to capture premium valuations as the unspecified supply gap widens toward 75,000-123,000 tonnes uranium annually by 2040.

FAQs (AI-Generated)

Existing mines face resource depletion and will decline from meeting over 90% of current demand to only 40% by 2035. New uranium projects require 10-20 years from discovery to production, creating a structural lag. Additionally, global exploration expenditure collapsed 88% between 2014-2020, leaving the development pipeline shallow relative to forecast requirements. Cost inflation has increased project economic thresholds by $15-20 per pound, further constraining economically viable supply.

The Russia-Ukraine war disrupted secondary supply from underfeeding and tails re-enrichment. Niger's 2023 coup introduced sovereign risk into 25% of EU uranium imports. US and allied nations have banned Russian enrichment imports, forcing supply chain reconfiguration. Kazatomprom has adopted OPEC-style supply discipline, prioritizing value over volume. These factors have fragmented global uranium trade and created premiums for Western jurisdictions with regulatory stability.

SMRs could contribute 35,800 tonnes uranium annually by 2040 under the Upper Scenario, with the Reference Scenario projecting 17,000 tonnes annually by decade's end. Their modular design and smaller footprint lower entry barriers for new markets beyond traditional nuclear power economies. This demand layer was not included in legacy forecast models, representing incremental growth above conventional reactor requirements and extending uranium's demand profile across diverse geographies.

Canada, the United States, and Australia are commanding jurisdictional premiums due to regulatory transparency, permitting predictability, and political stability. These regions benefit from established mining frameworks, ESG alignment, and policy support for domestic nuclear fuel cycles. Investors increasingly prioritize security of tenure and permitting certainty over pure resource scale, mirroring valuation trends observed in copper and gold markets where jurisdictional risk materially impacts project multiples.

Advanced-stage developers hold permitted or near-production assets with reduced development timelines, existing infrastructure access, and clearer paths to cash flow generation. Companies with active NRC licenses, completed feasibility studies, or restart-ready ISR operations face lower technical and regulatory risk. In a supply-constrained market where time-to-production determines market share capture, permitting readiness and operational visibility provide asymmetric upside compared to early-stage projects facing 10-20 year development horizons.

Analyst's Notes

Subscribe to Our Channel

Stay Informed