A Rare Shovel-Ready US Gold-Copper Project Advances With FS Imminent

US Gold Corp holds a fully permitted, low-capex gold-copper project in Wyoming — one of the few shovel-ready assets in North America at a time of rising metal prices.

- US Gold Corp's CK Gold Project in Wyoming is fully permitted and engineered, making it one of the few genuinely shovel-ready gold-copper assets in North America in a time when the investment community is actively seeking near-term production opportunities.

- The company is on the cusp of releasing a Feasibility Study backed by $30 million in cash, with an 18-to-24-month construction timeline targeting first production by end-2027 or 2028, producing approximately 110,000 gold-equivalent ounces annually over a 10-to-11-year mine life.

- While the prefeasibility study placed initial capital expenditure at $277 million, management notes that significant appreciation in both gold and copper prices over the same period has more than offset inflationary cost increases, keeping project economics robust.

- CEO George Bee reports strong inbound interest from potential financiers and mid-tier strategic partners at PDAC, with the company's tight share structure of approximately 16 million shares outstanding and meaningful management ownership aligning incentives closely with investors.

- Beyond CK Gold, the company holds substantial exploration upside at its 20-square-mile Keystone Project in Nevada and the Challis deposit in Idaho, providing longer-dated optionality for transformational scale.

Speaking at the Prospectors and Developers Association of Canada (PDAC) conference in Toronto, which has drawn approximately 45,000 attendees in what was described as the largest turnout in years, George Bee, President and CEO of US Gold Corp, outlined a company that has spent five years methodically de-risking its flagship CK Gold Project in Wyoming. With gold prices at historic highs, copper demand structurally supported by the energy transition, and a global shortage of near-term production assets, the timing of US Gold Corp's advance toward a Feasibility Study appears well-calibrated to current market conditions.

CK Gold Project: The Asset in Focus

The company's core value proposition rests on a combination of factors that are increasingly rare in the junior mining space: a fully permitted open-pit project, established infrastructure, a stable regulatory environment, and management with the technical credentials and financial discipline to advance it to production.

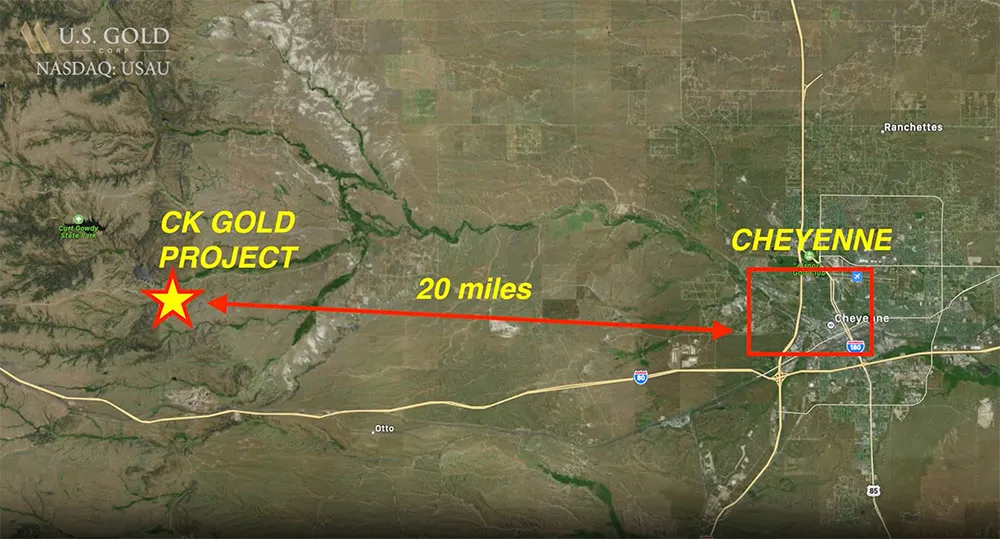

The CK Gold Project is located in Wyoming with a power substation situated approximately 16 miles from the site. This infrastructure proximity is not incidental as it is a direct driver of the project's relatively modest capital cost. The deposit contains gold and copper in a configuration amenable to a straightforward open-pit, low strip-ratio mining operation. Ore will be processed through a concentrator, with the end product being a copper-gold concentrate with a minor silver component, that Bee notes is currently in high demand among smelters facing feedstock shortages.

The 2025 PFS (prefeasibility study) placed initial capital expenditure at $277 million though management acknowledges this figure has increased due to general construction cost inflation and the complexity introduced by shifting tariff environments, particularly regarding equipment sourcing.

The project's resource and reserve base underpins a mine life of approximately 10 to 11 years, producing around 110,000 gold equivalent ounces annually. Bee clears that mineralization remains open at depth, and that a modest exploration program could potentially double the mine life adding further optionality to an already well-defined asset.

Financing and the Path to Production

US Gold Corp currently holds approximately $30 million in cash. The Feasibility Study, described by Bee as imminent, represents the key gateway document for the formal financing package required to fund construction. A 18-to-24-month build timeline from financing close puts first production at end-2027 or into 2028 aligning well with expectations for continued strength in gold and copper markets.

Bee described interest from entities in the emergent mid-tier sector companies large enough to bring meaningful capital but for whom CK Gold would represent a material addition to their portfolio. As Bee states:

"We'll spit out cash from the CK Gold project and then out of those funds we can go and pursue our ambitions. The scale of what we anticipate in Keystone could be huge, a real company maker."

The company has explicitly kept its share count tight, with approximately 16 million shares outstanding, and management holds a meaningful stake, aligning incentives with shareholders.

Jurisdiction: Wyoming as a Competitive Advantage

In the current global environment, where resource nationalism, regulatory unpredictability, and infrastructure deficits have introduced meaningful risk premiums into projects across Africa, Latin America, and parts of Asia, US Gold Corp's Wyoming address is a genuine differentiator. Bee framed this in terms of what he calls "knowing the rules of the game" where the regulatory agencies understand the mining industry, where mineral rights are secure, and where there is no risk of retroactive changes to fiscal or environmental frameworks.

Wyoming is a resource state with an established mining culture and a legal framework that provides long-term certainty for project developers and their capital providers. The project's location along a major interstate route further reduces execution risk, eliminating the infrastructure-build costs that inflate capital requirements for projects in more remote settings.

Bee also highlighted the significance of being a US-listed, NASDAQ-traded company at a time when domestic capital markets are increasingly focused on securing supply chains for critical minerals and energy-transition metals. With institutional and generalist investors now reconsidering resource exposure following years of underinvestment in the sectort, exchange-listed entity in the world's largest capital market is a material advantage.

Interview with George Bee, President & CEO of US Gold Corp.

Exploration Upside: Keystone and Beyond

While CK Gold is the near-term value driver, Bee was candid that the company's longer-term ambitions are centered on the Keystone Project in Nevada. Spanning 20 square miles and situated approximately 11 miles from Nevada Gold Mines' Cortez complex, Keystone represents the kind of blue-sky exploration target that can redefine a company's scale. The geological indicators at surface, including pathfinder elements and mineralization continuity from the Cortez system, are encouraging.

The company has recently completed geophysical surveys and soil sampling across the Keystone property, and is now applying artificial intelligence (AI) tools to integrate this dataset with geological models, with the objective of identifying the most compelling drill targets. At an estimated $500,000 per drill hole, capital allocation discipline will be essential, but the potential reward justifies the investment.

The Challis deposit in Idaho, which has a plan of operations in place for exploration, adds a third leg to the portfolio. In aggregate, US Gold Corp is positioning CK Gold as a cash-generating platform that funds exploration at assets with the potential to deliver transformational scale.

Market Context: Supply Scarcity Meets Rising Demand

The broader backdrop for US Gold Corp's advance to production is one of structural undersupply in the gold and copper markets. Years of underinvestment following the commodity cycle downturn of the mid-2010s have left the industry with a depleted pipeline of near-term projects. Permitting timelines in many jurisdictions have lengthened, exploration capital has been insufficient to replace mined reserves, and construction cost inflation has pushed the economics of greenfield development to levels that require sustained high metal prices to justify.

This is precisely the environment in which fully permitted, infrastructure-adjacent projects like CK Gold command a premium. Bee noted the irony of the current situation: after years of depressed interest from the investment community, there is now an urgent desire to produce but the supply chain and permitted project inventory is simply not there to meet that demand quickly. US Gold Corp is, by its own account, one of the few companies in a position to respond.

The Investment Thesis for US Gold Corp

- Permitted and de-risked: CK Gold holds full permits in Wyoming, eliminating one of the most time-consuming and uncertain phases of mining project development. This is a material advantage in an environment where permitting timelines have lengthened across most jurisdictions.

- Near-term production catalyst: The imminent Feasibility Study release will unlock formal project financing discussions. An 18-to-24-month construction timeline puts first production at end-2027 or 2028, delivering near-term cash flow visibility.

- Infrastructure proximity reduces capex: Proximity to I-80 corridor, a power substation 16 miles away, and established regional services keep initial capital requirements modest relative to peers with the PFS figure of $277 million, while subject to revision, remains competitive for a project of this scale.

- Metal price tailwinds: Gold at historic highs and copper supported by energy transition demand provide a favorable revenue backdrop that management believes more than compensates for cost inflation since the PFS was completed.

- Tight share structure preserves upside: With approximately 16 million shares outstanding and significant management ownership, dilution risk is low relative to peers, and per-share leverage to project value is meaningful.

- Jurisdiction premium in a risk-aware market: Wyoming's stable regulatory and legal framework eliminates the risk premium investors must price into projects in less predictable jurisdictions as increasingly valued by institutional capital providers.

- Strategic interest provides near-term optionality: Active discussions with potential strategic partners and financiers introduce the possibility of a transaction that could re-rate the stock ahead of the Feasibility Study.

- Exploration optionality adds asymmetric upside: The Keystone Project in Nevada, proximal to one of the world's great gold mining districts, provides a longer-dated but potentially transformational exploration upside not currently reflected in project-level valuations.

Macro Thematic Analysis: The Permitted Project Premium

The re-emergence of generalist investor interest in gold and base metals is not simply a function of metal price performance, though that has certainly been a catalyst. The reasons for supply constraints are well-documented: a decade of underinvestment following the 2012–2015 commodity price correction, the lengthening of permitting timelines in many jurisdictions from an average of three to five years to upwards of ten years in some cases, the depletion of reserve bases at major producers without commensurate replacement from new discoveries, and the concentration of new discoveries in increasingly remote or geopolitically sensitive locations. The result is that the pipeline of projects genuinely capable of entering production within a five-year window is remarkably thin.

This scarcity is driving a fundamental re-pricing of permitted, near-construction-ready assets. The market is beginning to differentiate between companies that are exploring for future resources and those that have already done the hard work of converting resources to reserves, obtaining permits, completing engineering studies, and positioning themselves for a financing decision.

"Now all of a sudden we want to turn on the spigot for production but there's been a dearth of interest from the investment community and as a consequence everybody's excited now. The supply chain isn't there that's why we're unique because we're one of the few permitted projects ready to get into production."

Western governments and corporations are acutely aware of the concentration of critical mineral supply chains in jurisdictions that carry political risk. This is driving active policy support for domestic mining in the United States, Canada, and Australia, and is making projects in these jurisdictions more attractive not just to financial investors but to strategic industrial buyers and offtake partners seeking supply chain security.

TL;DR

US Gold Corp enters this phase of the gold and copper cycle from a position of operational readiness that most of its peers cannot claim. With a fully permitted project, $30 million in cash, an imminent Feasibility Study, and active financing and strategic discussions underway, the company is materially closer to production than the junior mining sector average. The combination of a tight share structure, experienced management, and a genuinely infrastructure-advantaged project in one of North America's most stable mining jurisdictions creates a differentiated value proposition at a time when the investment community is beginning to price in the scarcity of near-term supply. The exploration portfolio at Keystone and Challis ensures that any re-rating driven by CK Gold's de-risking does not come at the expense of longer-term growth optionality. For investors seeking exposure to gold and copper with near-term production catalysts and a defined path to cash flow, US Gold Corp warrants close attention in the months ahead.

Frequently Asked Questions (FAQs) AI-Generated

CK Gold is fully permitted and has completed the majority of its engineering work. The company is on the verge of releasing a Feasibility Study, which will serve as the gateway document to secure construction financing. An 18-to-24-month build timeline puts first production at end-2027 or into 2028.

The prefeasibility study outlined initial capital expenditure of $277 million. Management acknowledges this figure has increased due to construction cost inflation and tariff-related equipment sourcing complexities. However, the company maintains that the significant appreciation in gold and copper prices over the same period has more than offset these higher costs, leaving the project's overall economics in a stronger position than when the PFS was completed.

Wyoming is a resource state with regulatory agencies that understand the mining industry, a stable legal framework, and no history of retroactive changes to mining fiscal terms. The project also benefits from direct access to the I-80 interstate corridor and a power substation 16 miles away — infrastructure advantages that directly reduce capital costs and execution risk compared to more remote projects globally.

Keystone is a 20-square-mile exploration property in Nevada, situated approximately 11 miles from Nevada Gold Mines' Cortez complex — one of the world's most prolific gold mining districts. Geological indicators at surface, including pathfinder elements and mineralization continuity from the Cortez system, suggest the potential for a large-scale discovery. The company is currently applying AI tools to prioritize drill targets. Management views Keystone as a potential company-defining asset, funded by cash flow from CK Gold once in production.

The company holds approximately $30 million in cash. The imminent Feasibility Study will anchor formal discussions with project financiers and strategic partners, a process already underway following strong inbound interest at PDAC. With a tight share structure of approximately 16 million shares outstanding and meaningful management ownership, the company is focused on securing financing structures that minimize unnecessary dilution to existing shareholders.

Analyst's Notes

Subscribe to Our Channel

Stay Informed