AI Electricity Demand & Uranium Supply Deficits Drive Prices to the Highest Level Since 2008

AI-driven nuclear power demand and constrained uranium supply pushed long-term uranium prices to their highest level since 2008.

- AI hyperscalers including Meta, which has contracted up to 7.8 gigawatts of nuclear capacity, and Microsoft, which has secured more than 800 megawatts of reactor power, are entering uranium-linked nuclear procurement alongside utilities, adding a new source of long-term fuel demand outside traditional reactor replacement cycles.

- Kazatomprom, which supplies approximately 43% of global primary uranium production, is tracking 2026 output at approximately 62 million pounds, 23 million pounds below earlier projections, reducing available supply as Western sanctions redirect utilities away from Russian uranium imports.

- Long-term uranium contract prices reached $90 per pound in Q1 2026, the highest level since 2008, while spot uranium traded at $86.25 per pound, indicating utilities and institutional buyers are securing future supply at higher contracted prices.

- The January 2026 Section 232 Critical Minerals Proclamation is separating uranium pricing by origin by directing US utilities toward Western-aligned supply, increasing pricing premiums for non-Russian and non-Kazakh uranium through 2040.

- Across the uranium value chain, producers are generating strong margins at current uranium prices, development-stage companies with high-grade assets near licensed processing infrastructure offer higher sensitivity to uranium price increases, and fully funded exploration programs in secure jurisdictions provide early exposure to new supply required later this decade.

AI Electricity Demand & Rising Uranium Consumption

Historically, uranium demand has come primarily from utilities purchasing fuel for existing reactor fleets under long-term replacement contracts rather than for new capacity growth. Technology companies are now contracting nuclear power directly to secure continuous carbon-free electricity for AI infrastructure, adding a new source of uranium demand outside traditional utility procurement.

Nuclear energy provides the continuous, large-scale electricity supply AI data centers require while reducing exposure to fuel price volatility compared with natural gas generation. Renewables require battery storage or gas backup to offset intermittency, while natural gas exposes buyers to fuel-price volatility, demonstrated in 2026 when energy market disruptions pushed Brent crude above $103 per barrel.

The International Energy Agency's World Energy Outlook 2025 projects global electricity demand will increase by at least one-third by 2035, driven by AI workloads, digitalization, and industrial electrification. The report also identifies Russia, which controls approximately 40% of global uranium enrichment capacity, as a major supply-chain risk for Western utilities. Each gigawatt of nuclear capacity consumes approximately 360,000 pounds of U3O8 annually, implying Meta's 7.8 gigawatt commitment could require approximately 2.8 million pounds of uranium per year when fully operational, comparable to the annual output of major uranium-producing assets.

Uranium Supply Constraints & Delayed Mine Development

Uranium supply cannot increase fast enough to meet projected demand growth during the current investment cycle. The World Nuclear Association and International Energy Agency estimate new uranium mines require 10 to 20 years from discovery to production, meaning projects approved today are unlikely to supply material before the mid-2030s. Most uranium supply growth expected between 2026 and 2030 depends on projects already under development, limiting the market's ability to respond to new demand.

Kazatomprom Production Cuts & Tightening Uranium Supply

Kazatomprom originally projected 2026 output at approximately 85 million pounds. Following its August 2025 production downgrade from 32,777 to 29,697 metric tons and the expected use of its 20% down-flex option, Kazatomprom's 2026 output is now tracking at approximately 62 million pounds, reducing expected global uranium supply by roughly 14% versus earlier forecasts. Construction delays at the Budenovskoye joint venture reduced expected 2026 output, while Kazakhstan's December 2025 subsoil code amendment gave Kazatomprom priority rights over new uranium exploration licenses, limiting private-sector control over future supply expansion.

US Uranium Import Restrictions & Higher Western Supply Premiums

Two US policy measures are separating uranium pricing by origin: the Prohibiting Russian Uranium Imports Act, which bans Russian uranium imports through 2040, and the January 2026 Section 232 Presidential Proclamation identifying foreign uranium dependence as a national security risk. Together, these policies are redirecting Western utility contracts toward uranium sourced from allied countries including Canada, the US, Australia, and Namibia, increasing pricing premiums for Western-aligned supply.

Western Uranium Jurisdictions & Higher Asset Valuations

Uranium assets in Western-aligned jurisdictions are receiving higher market valuations and contract interest than comparable assets in Kazakhstan or Russia. Uranium produced in Saskatchewan, South Texas, or Zambia is attracting stronger Western utility demand than Kazakh supply because US import restrictions and procurement policies favor allied jurisdictions. Because the legislation remains in effect through 2040, applying a single uranium price assumption across all jurisdictions may undervalue Western-aligned uranium assets.

Philip Williams, Chief Executive Officer of IsoEnergy, describes the rising institutional demand for uranium companies with exposure to Western jurisdictions:

“Earlier this year, we went out to raise $50 million. There was over $300 million in demand in that book. It was a global set of institutional investors with very large appetites looking to write very large checks into our company and into the sector.”

Rising Uranium Prices & Differentiated Value Chain Exposure

Higher uranium prices and tighter supply are affecting producers, developers, and exploration companies differently across the uranium value chain. Producers are generating strong margins at current uranium prices, development-stage companies with high-grade assets near licensed processing infrastructure offer greater upside if uranium prices rise further, and fully funded exploration programs in secure jurisdictions provide exposure to future uranium discoveries.

Energy Fuels Expands Uranium Margins Through Low-Cost Production

Energy Fuels reported Q1 2026 uranium concentrate revenues of $35.7 million. Spot market sales of 100,000 pounds during the quarter achieved an average realized price of $95.88 per pound against Pinyon Plain production costs of $23 to $30 per pound. The company reduced its finished U3O8 inventory cost by 16% to approximately $36 per pound while holding 2.24 million pounds of finished and contained U3O8 inventory.

Mark Chalmers, Chief Executive Officer of Energy Fuels, describes how uranium operations are contributing to broader investor interest in the company:

“People are seeing that 2 billion is achievable by Energy Fuels to build out a world significant low cost critical mineral company, but also including uranium. I think that's a big reason why we've had the re-rate in our stock.”

enCore Energy Expands Low-Cost ISR Uranium Production

enCore Energy operates In-Situ Recovery uranium production centres in South Texas. The company returned to profitability in Q1 2026 with earnings of $0.03 per share versus a loss of $0.13 per share a year earlier, as uranium extraction increased approximately 22% year-over-year to 90,000 pounds at a cash extraction cost of $34.94 per pound. Total available liquidity reached $84.7 million as of May 8, 2026, while permit-pending projects in South Dakota and Wyoming could expand US uranium production.

William Sheriff, Executive Chairman of enCore Energy, explains why larger-scale ISR production is becoming necessary for US uranium producers:

“In the ISR business, producers will need to operate at more than one million pounds per year to remain competitive. You've got to get some size.”

IsoEnergy Advances High-Grade Uranium Development in Saskatchewan and Utah

IsoEnergy is advancing the Larocque East project in Saskatchewan's Athabasca Basin, where the Hurricane deposit hosts an indicated uranium resource grading 34.5% U3O8 containing 48.6 million pounds. Winter 2026 drilling returned hole LE26-248 at 4.21% U3O8 over 3.5 meters outside the current deposit boundary. The company also holds permitted uranium mines in Utah under a toll milling agreement with Energy Fuels.

Atomic Eagle Expands Uranium Development Scale at Muntanga

Atomic Eagle is executing a 30,000-metre drill program at its Muntanga Uranium Project in Zambia, which holds a JORC-compliant uranium resource of 58.8 million pounds U3O8. The Muntanga feasibility study estimated a net present value of $243 million at a uranium price of $90 per pound.

Phil Hoskins, Chief Executive Officer of Atomic Eagle, explains how larger uranium resources could improve project economics and financing flexibility at Muntanga:

“We think that by scaling this project up, we can get this project to the point where it demands to be financed without an increase in the uranium price.”

ATHA Energy Expands High-Grade Uranium Exploration Across the Angilak Basin

ATHA Energy controls approximately 6.8 million acres of uranium exploration ground in Canada, including the Angilak Uranium Project in southern Nunavut. The 2025 exploration program returned grades up to 8.16% U3O8 over 0.5 meters at RIB North, well above the 1% U3O8 threshold commonly used to define high-grade uranium mineralisation. The 2026 exploration program is fully funded through a CAD $63 million financing completed in February 2026.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the scale and consistency of mineralization identified across the Angilak Basin:

“We've now identified mineralization over 14 kilometers of strike length at Angilak. Every geophysical target that we have tested and drilled has been mineralized.”

The Investment Thesis for Uranium

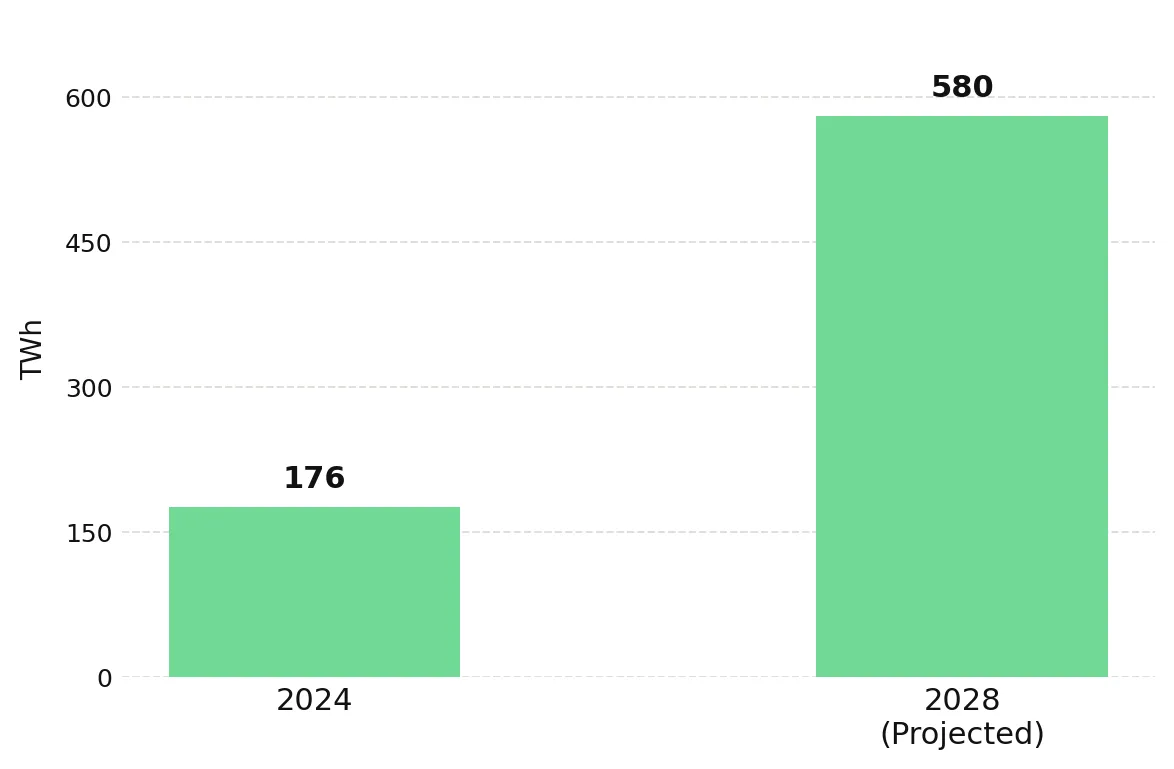

- AI data center operators are contracting nuclear power as the US Department of Energy projects domestic data center electricity demand will reach 580 TWh by 2028, adding a new source of uranium demand alongside traditional utility procurement.

- Uranium supply growth remains constrained because new mines require 10 to 20 years from discovery to production, while Kazatomprom's expected 2026 output has fallen approximately 23 million pounds below earlier projections, reducing anticipated global primary supply by roughly 14%.

- The Section 232 Critical Minerals Proclamation and the Prohibiting Russian Uranium Imports Act are directing Western utilities toward allied uranium supply through 2040, supporting higher valuations for Western-aligned uranium assets relative to Russian or Kazakh supply exposure.

- Uranium producers with low production costs and exposure to Western utility contracts are generating strong margins at spot uranium prices of $86.25 per pound and long-term contract prices of $90 per pound, the highest term price level since 2008.

- Development-stage uranium companies with high-grade deposits near existing processing infrastructure may require less capital and reach production faster than greenfield uranium projects.

- Fully funded uranium exploration programs in politically stable jurisdictions with strong drilling results provide early exposure to potential resource growth as the uranium market searches for new supply later this decade.

- Legislation restricting Russian uranium imports and Western utility procurement policies are increasing contract demand and valuations for uranium assets in allied jurisdictions.

Uranium prices are being supported by rising nuclear fuel demand and constrained long-term supply rather than short-term trading activity. AI data center electricity demand and Western legislation restricting Russian uranium imports are increasing long-term demand for uranium produced in allied jurisdictions. New uranium supply cannot be developed quickly enough to meet projected demand growth this decade. Long-term uranium contract prices reached $90 per pound, the highest level since 2008, as utilities and institutional buyers compete to secure future supply. Uranium investors are increasingly valuing producers, developers, and explorers differently based on jurisdiction, production costs, and project timelines. Producers in allied jurisdictions are benefiting from current uranium pricing, while development-stage and exploration companies offer exposure to future supply growth. AI-driven nuclear power demand is increasing uranium consumption faster than new mines can enter production.

TL;DR

AI hyperscalers including Meta and Microsoft are contracting nuclear power directly to support rising electricity demand from data centers, creating a new source of uranium demand outside traditional utility procurement. At the same time, uranium supply growth remains constrained because new mines require 10 to 20 years to reach production and Kazatomprom's expected 2026 output has fallen roughly 23 million pounds below earlier projections. US import restrictions on Russian uranium are also redirecting utility contracts toward Western-aligned suppliers through 2040. These combined forces pushed long-term uranium prices to $90 per pound in Q1 2026, the highest level since 2008, while increasing investor focus on low-cost producers, high-grade developers, and funded exploration companies.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed