Supply Constraints & a $94 Uranium Term Price Increase the Value of Stable-Jurisdiction Supply

Supply constraints and a $94 uranium term price highlight rising demand for stable-jurisdiction supply as utilities secure long-term fuel contracts.

- The long-term uranium contract price reached about $94 per pound in early 2026, an 18-year high reported by UxC and TradeTech, while the spot proxy remained near $85. The roughly $9 premium shows utilities paying for long-term delivery certainty rather than competing for limited spot supply.

- Kazakhstan cut its 2026 nominal uranium output from 32,777 to 29,697 tonnes, removing supply equal to about 5% of world primary production. It also tightened joint-venture ownership rules in favor of its state producer, reducing Western access to some of the world's lowest-cost uranium.

- Niger's nationalized SOMAIR mine produced no uranium in 2025 and remains subject to an ICSID tribunal order blocking the sale of its stockpile, keeping a source of supply previously available to Western utilities off the market.

- Four privately built reactors reached criticality by July 4, 2026, while hyperscaler-backed power agreements extended long-term uranium fuel requirements. Together, they widened a supply deficit that new mines are unlikely to close quickly.

- Utilities are paying more to secure uranium from reliable jurisdictions, supporting producers, developers, and explorers even as many uranium equities continue to trade below the signal from long-term contract prices.

Supply Concentration & Record Term Prices Lift Uranium Contract Values

Unlike copper or gold, uranium does not trade on a centralized public exchange. Instead, two pricing benchmarks define the market: the spot price reflects prompt delivery in a thin market where relatively small trades can move prices, while the term price reflects the multi-year contracts utilities use to secure future uranium supply. Because utilities procure most reactor fuel through long-term contracts rather than spot purchases, the term price provides the clearest signal of underlying uranium demand.

In the first quarter of 2026, TradeTech's long-term uranium indicator reached $93.00 per pound at the end of March, up $6.50 from December 2025 and the highest level in more than 18 years, while UxC reported a comparable price near $94 per pound. By contrast, the spot proxy remained near $85 and is published as a contract-for-difference reference rather than an exchange-cleared transaction price. A multi-decade high in term prices above the spot market shows utilities paying a premium to secure long-term uranium supply rather than relying on prompt purchases.

Term Pricing & Lagging Uranium Equities Signal a Valuation Gap

IsoEnergy, a uranium developer with assets in Canada, the United States, and Australia, sits close to this market on the contract market.

Philip Williams, Chief Executive Officer of IsoEnergy, says long-term uranium contract prices continue to signal stronger market fundamentals than uranium equity valuations currently reflect:

"Spot is $85, and it can be a bit volatile. UxC reported a $94 long-term price, which is within spitting distance of an all-time high, but equities are not trading that way. A $94 uranium price on the term basis, and knowing full well the contracts are being done higher than that, with reporting issues around it. To me, that's game on."

Supply Concentration & Geopolitical Risk Tighten Uranium Supply

Long-term uranium contract prices are rising because Kazakhstan, the world's largest uranium producer, cut its 2026 nominal output from 32,777 to 29,697 tonnes, removing supply equal to about 5% of global primary production as it prioritized higher-value sales over production growth. In December, Kazakhstan also amended its subsoil code to limit production-right transfers to ventures in which its state producer holds at least 75% ownership and exploration at producing deposits to holdings of at least 90%, reducing Western partners' access to some of the world's lowest-cost uranium. Production from the Budenovskoye joint venture is committed entirely to the Russian civil nuclear industry, limiting availability for other buyers.

Niger's nationalized SOMAIR mine, formerly operated by Orano, produced no uranium in 2025 and remains subject to a September 2025 order from the World Bank's International Centre for Settlement of Investment Disputes blocking the sale or transfer of a disputed stockpile of 1,150 to 1,500 tonnes. Together, those restrictions remove a source of uranium previously available to Western utilities, further tightening accessible supply outside Russian-aligned channels.

The Strait of Hormuz is another critical bottleneck because Kazakhstan produces most of its uranium through in-situ recovery, which relies on sulfuric acid to dissolve uranium underground. Roughly one-fifth of global sulfur shipments move through the Strait, making the route a critical supply line for the world's largest uranium producer. The renewed disruption in early July 2026 highlighted how supply interruptions in the Strait of Hormuz could restrict sulfuric acid deliveries, increasing operational risk for the world's largest and lowest-cost uranium producer.

Geopolitical Competition & Secure Uranium Supply Increase the Value of Stable Jurisdictions

Phil Hoskins, Chief Executive Officer of Atomic Eagle, says governments are competing to secure long-term uranium supply, increasing the strategic importance of projects in stable jurisdictions:

"As it relates to uranium, like a lot of other critical minerals, it's becoming a bit of a battleground from a geopolitical standpoint. The US government, producing only 2% of the uranium that they need, is obviously looking to get active; India recently signed some long-term supply deals with Kazatomprom and Cameco; and the Chinese have been super aggressive, building around 10 new reactors every year for the last four or five years. If you've got credible near-term pounds in a very stable jurisdiction like Zambia, we think it will be a very tight market."

Reactor Growth & Long-Term Fuel Demand Deepen the Uranium Deficit

Demand is also increasing as four privately built reactors reached criticality by the July 4, 2026 target set under a US executive order, converting announced nuclear projects into operating reactors that require long-term uranium fuel purchases. Utilities that deferred contracting still have uncovered fuel requirements, meaning uranium needed for future reactor operations remains uncontracted and must eventually be purchased.

Supply cannot answer quickly. New mine development is generally cited as requiring $60 to $70 per pound to justify construction, with triple-digit contract pricing viewed as the level needed to fund the next wave of capacity. At about $94, the term price is only beginning to reach that threshold, and mine restarts over the past two to three years have repeatedly fallen short of their targets.

Higher Uranium Contract Prices & Low-Cost Production Expand Cash Flow

Producers already selling under long-term utility contracts are capturing the first gains from higher uranium contract prices. Energy Fuels, a US uranium producer, operates the country's only conventional uranium mill and reports processing costs of $9 to $12 per pound and mining costs of $23 to $30 per pound at its Pinyon Plain mine, compared with a 2025 realized sales price of $74.20 per pound. enCore Energy, another US producer, increased first-quarter 2026 uranium extraction 22% year over year to 90,000 pounds while realizing an average sales price of $67.78 per pound. Together, the results show established producers converting higher contract prices into operating cash flow.

Mark Chalmers, Chief Executive Officer of Energy Fuels, says higher uranium prices are translating into stronger cash flow for low-cost producers as the supply-demand deficit widens:

"Uranium has moved forward accretively, and people expect it to take off quite soon, given the supply-demand deficit story. We're making great strides in the uranium business. It's generating cash, it's low cost, and it's truly unique."

Scale is becoming the dividing line among US producers, because larger output lowers the cost of capital and strengthens contract terms with utilities. William Sheriff, executive chairman of enCore Energy, frames the consolidation pressure inside the in-situ recovery business:

"In terms of the ISR business, you're going to have to have some producers that produce more than a million pounds a year, or you're going to be essentially running a mom-and-pop grocery store on the corner. You've got to get some size for a number of reasons. Your credit ratings go up, so your cost of capital goes down."

Higher Contract Prices & Limited Mine Supply Increase the Value of Uranium Development Projects

If higher uranium contract prices support the next wave of mine development, developers and explorers control much of the future uranium supply needed to meet that demand. IsoEnergy's Hurricane deposit in Saskatchewan contains an indicated resource of 48.6 million pounds grading 34.5% U₃O₈, one of the highest indicated grades globally, and the company holds about C$130.5 million in cash to fund studies across three jurisdictions. Atomic Eagle's Muntanga project contains a 58.8-million-pound resource grading 309 parts per million U₃O₈.

Although lower grade, its shallow geometry supports simple heap-leach mining, and the project advanced toward permitting after securing environmental and resettlement approvals in mid-2026. Resource confidence progresses from inferred to indicated to measured as drilling density increases, with each stage reducing development risk ahead of a construction decision.

Explorers represent the earliest stage of the uranium supply pipeline, offering the greatest upside if new discoveries are made but carrying the highest geological and financing risk because they have neither defined resources nor operating revenue. ATHA Energy controls more than 7 million acres across Canada's uranium basins and funded a roughly 20,000-meter drill program in 2026 with a C$63 million financing. Its radiometric readings, measured in counts per second, identify exploration targets but are not assays and do not define a mineral resource.

Supportive Uranium Markets & Large Land Positions Increase Exploration Value

The exploration case rests on the size of the system rather than near-term cash flow. Troy Boisjoli, Chief Executive Officer of ATHA Energy, frames the market backdrop into which that scale is being tested:

"This uranium market that we're heading into is the most constructive market I've seen in 20 years in space."

Supply Constraints & Lagging Uranium Equities Create a Valuation Gap

Taken together, the supply, demand, and pricing data point to the same conclusion. Accessible uranium supply continues to tighten, long-term contract prices remain at multi-decade highs, and uranium demand is increasing as new reactors enter service and long-term power agreements extend fuel procurement requirements. Yet many uranium equities continue to lag higher long-term contract prices, leaving a gap between improving market fundamentals and company valuations.

The thesis faces two principal risks. First, the gap between spot and term prices could narrow if utilities continue delaying contract purchases and secondary supply remains available longer than expected. Second, the Fed's policy rate of 3.50% to 3.75% can continue to pressure valuations for pre-revenue uranium companies that depend on future project cash flows. Mine restarts have also repeatedly missed production targets, showing that higher uranium prices alone do not guarantee additional supply.

Uranium equities remain volatile, while developers and explorers face dilution, permitting, and execution risks. Even if the long-term supply-demand outlook remains supportive, contract prices, project execution, and equity valuations are unlikely to move in a straight line, and individual investments can still lose capital.

The Investment Thesis for Uranium

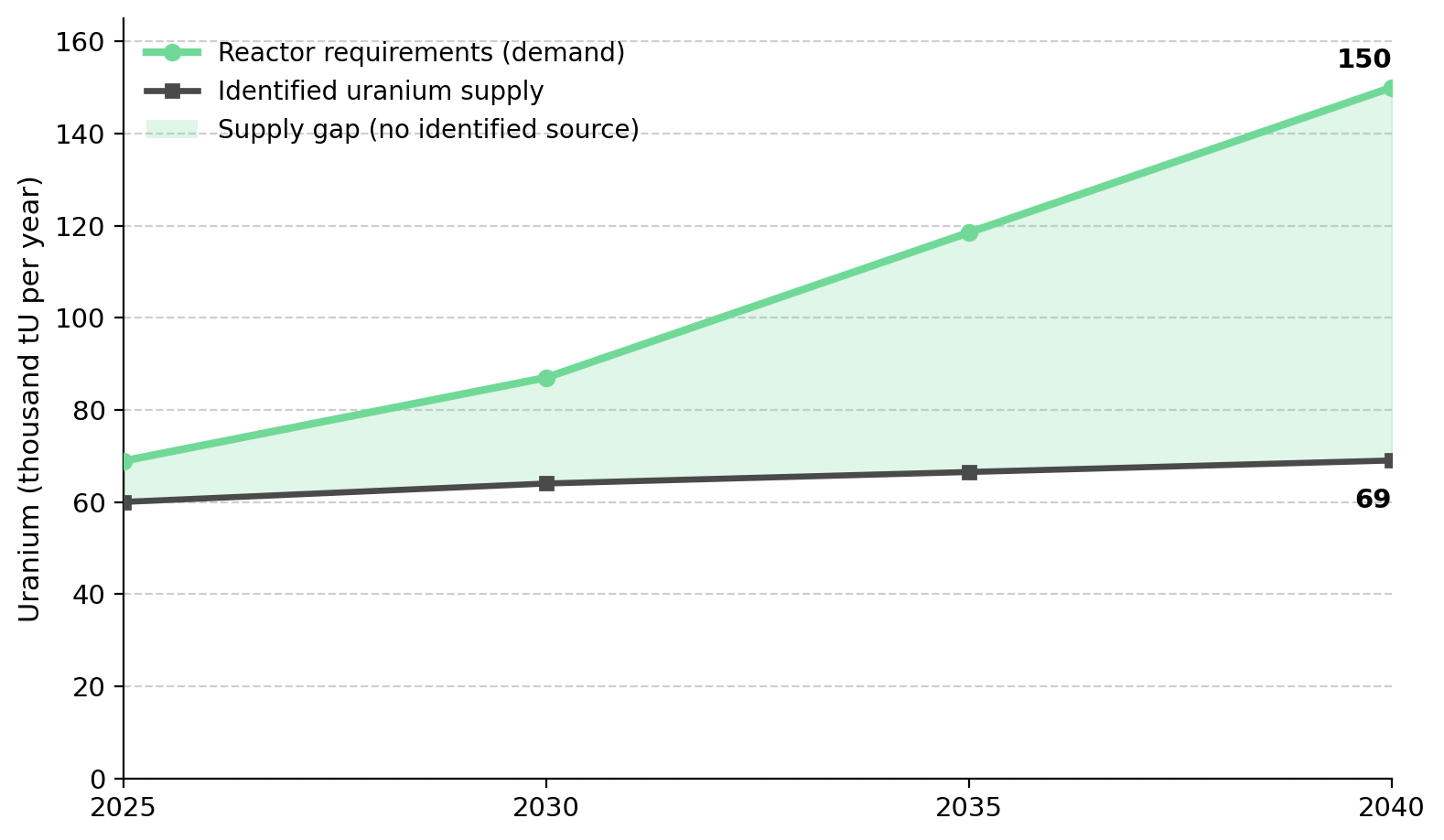

- A widening uranium supply-demand deficit as global primary production remains below reactor requirements and the shortfall expands through 2040, supporting long-term contract pricing as older mines deplete and new reactors come online.

- A long-term contract price near an 18-year high that is beginning to reach the incentive level required to fund new mine construction, which rewards supply that can be delivered from stable jurisdictions.

- Producers selling under multi-year utility contracts at costs well below realized sales prices, generating operating cash flow from higher contract prices with limited exposure to spot-market volatility.

- Developers with defined uranium resources in stable jurisdictions, positioned to advance new production into a market expected to remain in supply deficit through the end of the decade.

- Explorers with large land positions in prospective uranium districts, offering the greatest upside from new discoveries but carrying the highest geological and financing risk because they have neither defined resources nor operating revenue.

- Concentration of the world's lowest-cost uranium supply in non-Western jurisdictions, increasing the value of production from stable jurisdictions as utilities diversify away from Russian-aligned and restricted sources of supply.

- Growing uranium demand from reactor restarts, new builds, small modular reactors, and AI-driven nuclear power projects, requiring utilities to secure additional long-term fuel contracts.

An 18-year-high contract price alongside a range-bound spot price is not a contradiction. The premium reflects utilities paying more to secure uranium from accessible sources as the world's lowest-cost supply becomes increasingly concentrated behind state ownership and stranded inventories. The key market signal remains the term price, while the principal supply risk is whether disruptions to sulfuric acid supply or shipping routes constrain Kazakhstan's production. Reliable uranium supply from stable jurisdictions now commands a premium in long-term utility contracts.

Kazakhstan's production cuts and tighter joint-venture rules, Niger's stranded SOMAIR stockpile, and the dependence of Kazakhstan's in-situ recovery mines on sulfuric acid shipped through the Strait of Hormuz have reduced access to the world's lowest-cost uranium supply. The long-term contract price responded by rising to about $94 per pound, an 18-year high and roughly $9 above the $85 spot proxy, while uranium demand increased as new reactors reached criticality and AI-driven nuclear power projects expanded long-term fuel requirements. That pricing environment favors producers such as Energy Fuels and enCore Energy, developers including IsoEnergy and Atomic Eagle, and explorers such as ATHA Energy that operate in stable jurisdictions. Even so, uranium equities continue to lag higher contract prices, and the sector remains exposed to volatility, permitting risk, dilution, and potential capital loss.

TL;DR

Long-term uranium contract prices have climbed to about $94 per pound, an 18-year high, as production cuts in Kazakhstan, restricted access to low-cost supply, and geopolitical disruptions tighten the market while reactor growth and AI-driven power demand increase long-term fuel requirements. Utilities are prioritizing delivery certainty through multi-year contracts, creating a premium for producers, developers, and explorers operating in stable jurisdictions. Although uranium equities have yet to fully reflect stronger contract prices, the supply-demand outlook remains supportive, with risks including delayed utility contracting, higher interest rates, mine execution challenges, dilution, and permitting uncertainty.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed