IsoEnergy's Uranium Portfolio Positions for a Structural Supply Gap; But Execution Is the Real Test

IsoEnergy is advancing one of the world's highest-grade undeveloped uranium deposits at Hurricane in Canada, a near-term US mine restart at Tony M in Utah, and a pending Australian acquisition, all against a backdrop of a structural global uranium supply gap that the World Nuclear Association says will leave 54 percent of 2040 demand uncovered by known sources.

- IsoEnergy has published its February 2026 corporate presentation, outlining a diversified uranium developer with assets spanning Canada, the United States, and Australia.

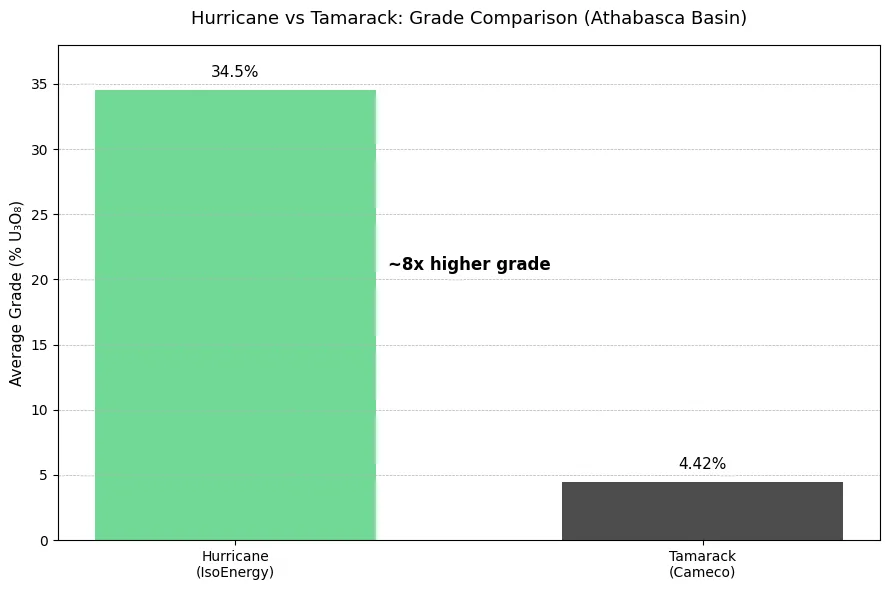

- The company's flagship Hurricane deposit in Saskatchewan, Canada holds 48.6 million pounds of uranium oxide (U3O8) at a world-leading grade of 34.5 percent, making it the highest-grade published Indicated uranium resource on the planet.

- A 2,000-tonne bulk sampling program at the Tony M mine in Utah is expected to wrap up in April 2026, with results feeding directly into a potential production restart decision.

- The pending takeover of Australian developer Toro Energy would push the combined Mineral Resource Estimate (MRE) to 133 million pounds Measured and Indicated (M&I) plus 39 million pounds Inferred under Canada's National Instrument 43-101 (NI 43-101) reporting standard.

- The company holds approximately C$156 million in cash and a further C$55 million equity portfolio, giving it a well-funded runway across all active programs.

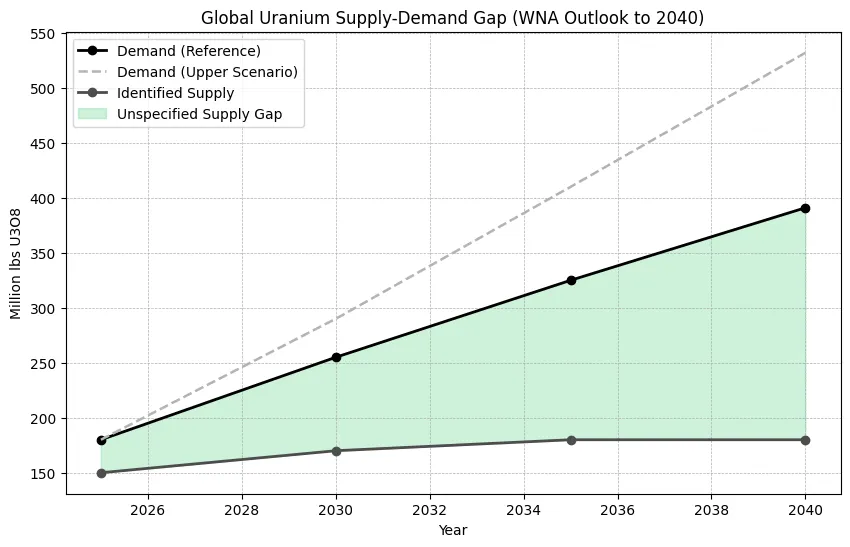

- The World Nuclear Association (WNA) projects that only 46 percent of global uranium demand in 2040 is covered by known supply sources, a gap that sits at the heart of IsoEnergy's investment case.

Opening Briefing

IsoEnergy released its February 2026 investor presentation this month, pulling together the most complete picture yet of a company that has been quietly building one of the most geographically spread uranium portfolios in the sector. The update lands as the company runs a bulk sampling program at its Tony M mine in Utah, pushes ahead with drilling at the Hurricane deposit in Canada's Athabasca Basin, and works toward completing its takeover of Australian uranium developer Toro Energy.

The backdrop could hardly be more supportive. The WNA's latest fuel report projects a widening gap between uranium supply and demand through to 2040, and IsoEnergy has deliberately built its portfolio to sit squarely in the path of that trend. The harder question, and the one investors should keep front of mind, is whether the company can move fast enough to turn its asset base into pounds in the ground and, eventually, pounds in the market.

The Global Uranium Shortfall Is Not a Future Problem: It Is Happening Now

Here is the core issue for uranium investors to understand. The WNA's 2025 World Nuclear Fuel Report puts global uranium demand at 391 million pounds U3O8 by 2040 under its central forecast, with a higher scenario reaching 532 million pounds. The problem is that mines currently operating, projects under development, and secondary supply sources together only cover around 46 percent of what will be needed. The rest sits in what the WNA calls an "unspecified gap," meaning the world does not yet know where that uranium will come from.

This gap is not driven by one factor alone. Governments are recommitting to nuclear power for energy security. Decarbonisation targets are accelerating demand. Small Modular Reactors (SMRs) are moving from concept to construction pipeline. All of these forces are pushing uranium demand higher at exactly the moment when new supply takes eight to twelve years to bring online. That long development timeline is the critical point: decisions made today about which projects to fund and advance will determine whether utilities can secure fuel a decade from now.

Chief Executive Officer and Director of IsoEnergy, Phil Williams, put it directly:

"Structural supply deficit supports a strong long-term price environment, particularly favourable for producers in Western, allied jurisdictions with established regulatory and permitting frameworks."

That framing is not marketing language. It reflects where utilities are being forced to look as the decade progresses.

Hurricane Is One of the Rarest Uranium Deposits in the World: Here Is Why That Matters

Not all uranium deposits are created equal, and Hurricane is in a category of its own. Located at IsoEnergy's Larocque East project in Saskatchewan's eastern Athabasca Basin, the deposit holds an MRE of 48.6 million pounds U3O8 Indicated at an average grade of 34.5 percent. To put that in context, the next-closest undeveloped deposit within 50 kilometres of the McClean Lake processing mill is Cameco's Tamarack deposit, which grades 4.42 percent. Hurricane is nearly eight times higher grade.

Why does grade matter so much? In simple terms, higher-grade ore means you process less rock to get the same amount of uranium. That translates directly into lower operating costs, a smaller physical footprint, and a project that can remain economical even when uranium prices pull back. Hurricane's highest-grade core of 38,200 tonnes averages 52.1 percent U3O8, which is extraordinary by any global standard. Add to that a relatively shallow depth of 325 metres, no water cover at the surface, existing road and power access, and a location just 40 kilometres from the operating McClean Lake mill, and you have a deposit with a development pathway that looks considerably cleaner than most. Reinforcing the view from outside, Cameco noted in its 2026 Annual Information Form that drilling at the adjacent Dawn Lake joint venture "continued to expand the footprint of known uranium mineralization with additional high-grade mineralized intercepts... the results to date are comparable to those of other mines."

The 2026 Drill Program Could Make Hurricane Even Bigger

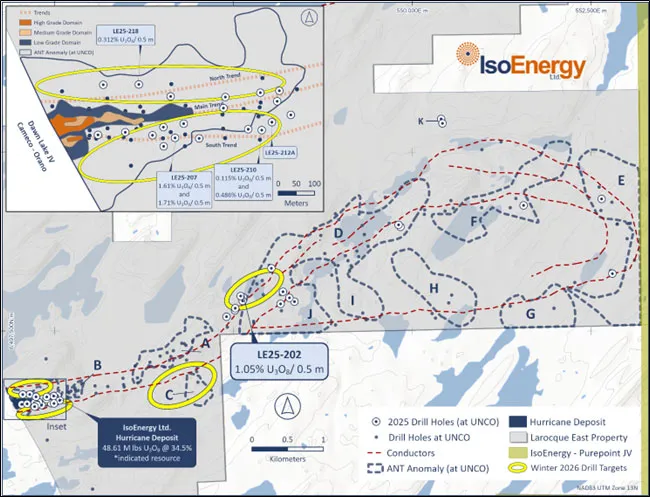

The deposit may already be growing. IsoEnergy's 2025 drilling program pushed beyond the existing MRE boundary and returned encouraging results. Drill hole LE25-202 cut 1.05 percent U3O8 over 0.5 metres in an area called Area D, which the company describes as the strongest uranium result to date outside the Hurricane deposit itself. That is significant because it suggests the mineralised system extends further than the current resource outline captures.

A winter 2026 drill program totalling approximately 5,200 metres across up to 13 holes is now underway, focused on the newly identified trends and zones where the geology has been structurally upgraded based on last year's work. Williams described the program as "positioned to build on momentum," targeting areas that the integrated summer results have flagged as high priority. For investors, the key question is simple: do these holes extend the deposit in a meaningful way? If they do, a resource update becomes possible, and with it, a potential re-rating of the asset's value. When the world's highest-grade Indicated uranium deposit gets bigger, the market tends to notice.

Tony M Bulk Sample Will Determine the Near-Term Production Timeline

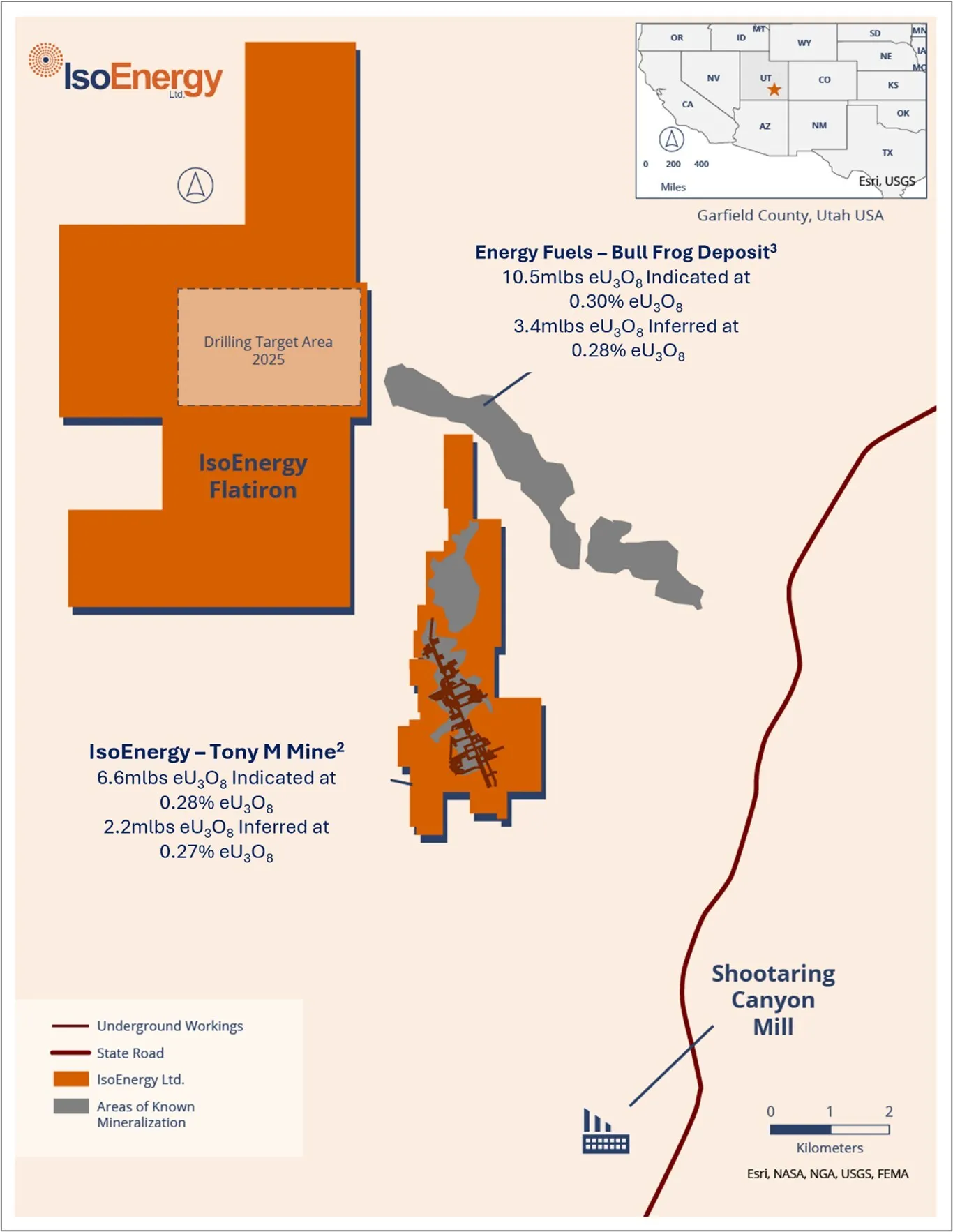

While Hurricane carries the long-term development narrative, IsoEnergy's near-term production story centres on its Henry Mountains portfolio in Utah, specifically the Tony M mine. The 2022 MRE shows 6.6 million pounds U3O8 Indicated and 2.2 million pounds Inferred at grades of 0.28 percent and 0.27 percent respectively. These grades are modest relative to Hurricane, but the strategic value here lies elsewhere: Tony M is a past-producing mine with key state and federal operating permits already in place, permits the company estimates represent three to five years of time savings and over US$1 million per mine in avoided costs. All projects in the Henry Mountains cluster are within trucking distance of Energy Fuels' White Mesa Mill in Utah, providing an existing toll milling pathway that eliminates the need for on-site processing infrastructure.

The current 2,000-tonne bulk sampling program, with completion targeted for April 2026 and processing at White Mesa Mill, is the critical near-term catalyst. Completed beneficiation test work already demonstrates greater than 90 percent uranium recovery, and a completed Enhanced Evaporation Study has confirmed that Landshark evaporators eliminate the need for pond expansion, reducing both permitting complexity and capital requirements.

Williams has been direct about the sequencing logic:

"Multiple concurrent work programs across the portfolio including drilling at Hurricane, exploration in the Athabasca Basin and Henry Mountains, and technical studies to support a Tony M production decision..."

reflect the company's deliberate build-out approach, advancing near-term and long-term assets in parallel rather than sequentially.

The Toro Acquisition Adds Scale, Geography, & an Offtake Signal

The pending acquisition of Australian developer Toro Energy, announced in October 2025, materially changes the pro forma resource picture. On a combined basis, IsoEnergy would hold 133 million pounds M&I and 39 million pounds Inferred under NI 43-101, alongside historical resources of 154 million pounds M&I and 88 million pounds Inferred. The primary Toro asset is the Wiluna Uranium Project in Western Australia, hosting 69.1 million pounds U3O8 M&I across multiple shallow, near-surface deposits suited to open-pit mining and alkaline leach processing, with a further 4.5 million pounds Inferred.

Perhaps the most telling commercial signal embedded in the Toro transaction is the existing offtake arrangement: Japan Australia Uranium and Itochu hold the right to acquire a 35 percent interest in Lake Maitland for US$39.6 million, an arrangement that pre-dates IsoEnergy's involvement and provides independent third-party validation of the project's commercial viability. Australia holds the largest share of global uranium resources and is the world's fourth-largest uranium producer, giving Wiluna a geopolitical edge in a market increasingly focused on supply chain security. The deal is not yet closed, and integration risk remains real, but the strategic logic of adding low-cost, open-pittable Australian pounds to a portfolio anchored by high-grade Canadian underground resources is difficult to argue with.

A Well-Funded Balance Sheet Backed by the Sector's Most Experienced Operators

IsoEnergy's pro forma financial position of approximately C$156 million in cash and equivalents, plus an equity portfolio valued at roughly C$55 million, provides meaningful runway across its concurrent work programs. The equity portfolio spans NexGen Energy, Atha Energy, Premier American Uranium, and several smaller uranium developers, functioning as a basket of sector call options with embedded liquidity. The company describes this as approximately C$55.8 million in value created from non-core assets, a figure that reflects disciplined capital recycling across a series of spinouts, joint venture formations, and asset sales dating back to late 2023.

The shareholder register reinforces the quality signal. NexGen Energy holds approximately 30 percent of IsoEnergy, providing both a strategic anchor and a direct connection to the team that discovered and advanced the Arrow deposit, one of the most significant uranium discoveries of the past two decades.

Williams noted that the company benefits from:

" a proven leadership team with deep uranium sector expertise, including the co-founders of NexGen Energy and former executives from Cameco and Uranium One."

At a February 2026 share price of C$14.42 against analyst consensus price targets ranging from C$18.00 to C$28.25, all carrying Buy ratings, the market appears to be pricing in meaningful uncertainty around execution timelines, a gap that the next twelve months of operational delivery will be critical in closing.

What Investors Should Be Watching Over the Next Twelve Months

Several specific catalysts will define IsoEnergy's trajectory, and readers should monitor them closely. The bulk sample processing results from Tony M, expected following White Mesa Mill processing of the April 2026 sample, will deliver the first hard economic data on what a potential restart might look like. A positive outcome could catalyse a formal production decision timeline and represent a meaningful re-rating moment for a market that has yet to fully price near-term US production optionality into the company's valuation.

At Hurricane, the winter 2026 drill results will clarify whether the mineralised trends identified outside the existing resource represent genuine deposit expansion. The Toro acquisition closing remains a near-term corporate milestone, after which the initiation of a Preliminary Economic Assessment (PEA) at Wiluna and further infill drilling at Lake Maitland become the key development markers. Longer term, the transition of Hurricane from exploration asset to formally scoped development project, through the initiation of a PEA, would signal the moment IsoEnergy crosses from developer into territory where major utility contracting conversations become realistic. In a uranium market defined by structural supply constraints and rising demand from the energy transition, that transition is the milestone worth watching most carefully.

TL;DR

IsoEnergy holds one of the highest-grade undeveloped uranium deposits in the world at Hurricane in Canada, a near-term production candidate at Tony M in Utah, and a pending Australian acquisition that together position the company to benefit from a structural global uranium supply shortfall, provided it can execute on its busy 2026 work program.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed