Q1 Uranium Recap: How Governments Are Deciding Who Secures Uranium

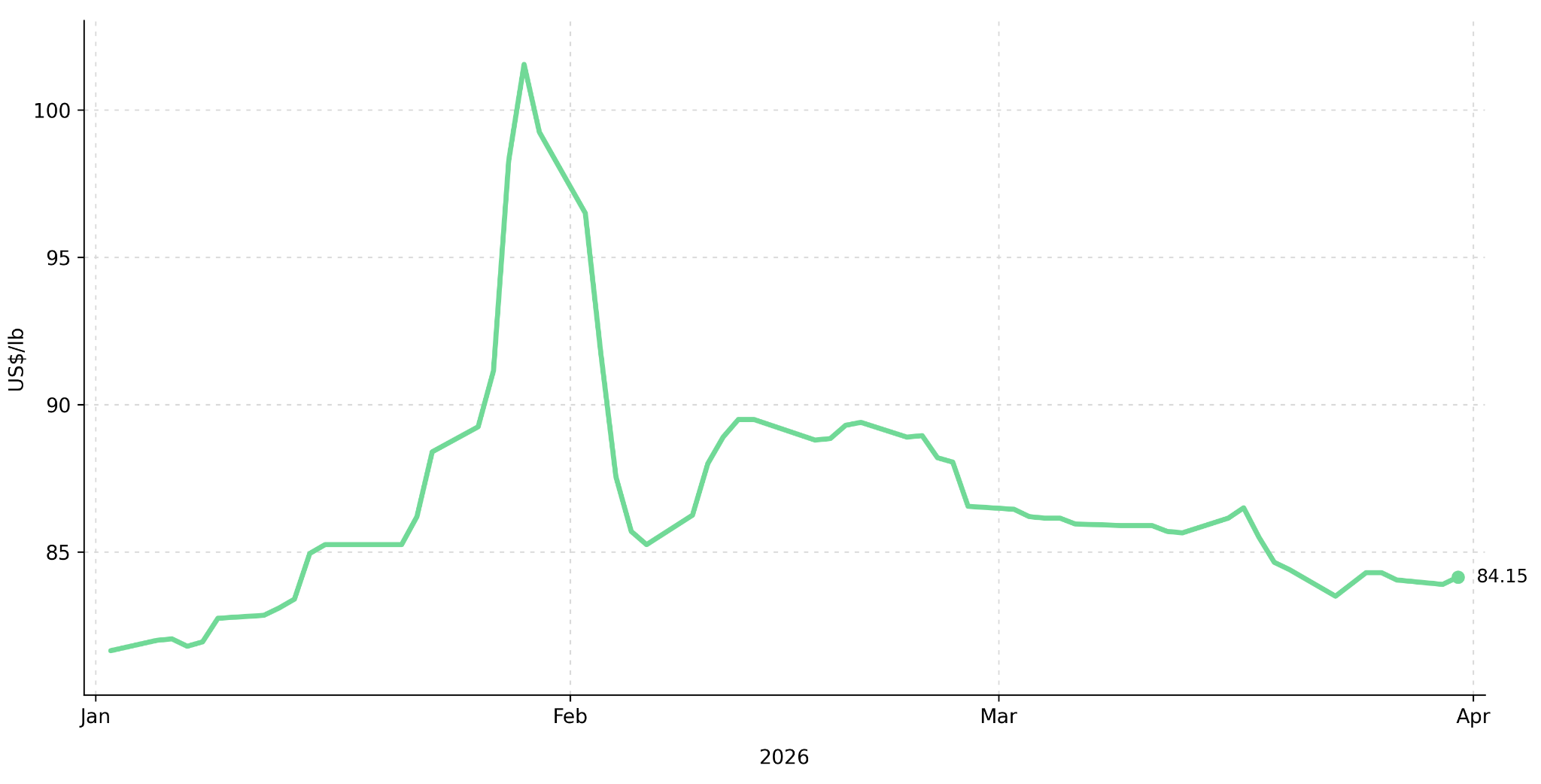

Uranium spot prices hit $94.28/lb in January 2026 as US Section 232, Kazakhstan's subsoil law changes, and Kazatomprom's India deal reshape who secures supply.

- US Section 232 policy, Kazakhstan regulatory changes, and bilateral supply agreements are collectively reducing open-market uranium liquidity and creating conditions for jurisdictional pricing premiums.

- Global utility uranium requirements stand at approximately 180 million pounds per year against a supply base constrained by geopolitical and regulatory intervention.

- Uranium spot prices reached $94.28 per pound by the end of January 2026, a two-year high, before consolidating into the mid-$80s, reflecting tightening supply fundamentals rather than speculative excess.

- Technology companies are entering nuclear energy procurement directly, introducing a capital-backed, non-cyclical demand base that extends beyond traditional utility contracting patterns.

- The Northshore Global Uranium Mining Index returned 39.49% year-to-date as of January 31, 2026, per Sprott Asset Management, illustrating the embedded leverage and corresponding risk that mining equities carry relative to the underlying commodity.

Spot Prices Hit a Two-Year High as Government Actions Tighten Supply Access

Uranium spot prices reached $94.28 per pound by the end of January 2026, a two-year high confirmed by Sprott Asset Management, before consolidating into the mid-$80s, a movement driven by US Section 232 review activity, Kazakhstan's December 2025 Subsoil Use Code amendments, and Kazatomprom's bilateral supply agreement with India removing open-market volumes.

Global utility uranium requirements of approximately 180 million pounds per year establish the scale of the procurement obligation utilities must fulfill. Contracting activity has consistently fallen short of this requirement, concentrating procurement pressure into shorter windows and creating conditions for sharp upward price adjustments when utilities re-enter the market.

The Northshore Global Uranium Mining Index's 39.49% year-to-date return as of January 31, 2026, illustrates the operational leverage mining equities carry to commodity price movements. This leverage amplifies upside during repricing events and introduces proportional downside risk during consolidation, both dynamics visible within a single quarter in early 2026.

Under-Procurement & Deferred Contracting Risk

Utility uranium procurement operates on long lead times, with fuel fabrication, conversion, and enrichment requirements dictating contracting decisions three to seven years ahead of reactor loading. When utilities systematically defer contracting below annual consumption levels, the deferred volume does not disappear; it accumulates as a future procurement obligation that must eventually be fulfilled at prevailing market prices.

This dynamic is particularly consequential in a market where new mine supply requires five to fifteen years from discovery to nameplate production, meaning no production decision taken today can address near-term supply gaps within the fuel cycle planning window that utilities currently face.

Section 232 and Kazakhstan's Amendments Are Creating a Two-Tier Uranium Market

Uranium is transitioning from a commodity governed primarily by market economics to a strategically controlled asset shaped by national security priorities. This transition has direct implications for how investors should price jurisdictional exposure, cost curves, and supply chain positioning.

The US government's Section 232 review, classifying uranium as a critical mineral, creates the legislative basis for domestic price floors, import restrictions, and preferential procurement frameworks targeting reduced dependence on Russian-origin uranium. If implemented, these measures would establish a two-tier pricing structure in which US-origin uranium trades above the spot price, the scale of which would be determined by the volume thresholds and import tariff levels specified in any resulting executive order.

Domestic Premiums & Bifurcated Pricing Risks

If domestic procurement preferences are enacted under Section 232, US utilities subject to those mandates would be required to source uranium processed through domestic facilities, a requirement that producers without US-based milling or conversion capacity cannot satisfy, regardless of mine location, concentrating eligible contracted supply among a small number of domestic operators.

Energy Fuels operates the White Mesa Mill in Utah, confirmed in the company's 2026 corporate presentation as the only operating conventional uranium mill in the United States, and is targeting 1.5 to 2.5 million pounds of uranium production in 2026.

Mark Chalmers, Chief Executive Officer of Energy Fuels, frames the company's positioning within the broader critical minerals supply chain context:

"Energy Fuels focused on building a critical mineral hub that revolves around the uranium business… Having uranium, rare earth, and heavy mineral sands, we have over 10 critical minerals, which really stands out from others."

enCore Energy's In-Situ Recovery model offers a complementary approach to domestic supply, with lower capital intensity and faster site reclamation timelines than conventional mining. William Sheriff, Executive Chairman of enCore Energy, describes the structural advantages that distinguish ISR extraction from legacy uranium operations:

"Uranium mining now, in terms of in-situ, is not your predecessor uranium. It's as different as day and night. Being so environmentally friendly and short timeline, short cost to reclaim them."

Supply Constraints Are Deepening Across Key Producing Regions

Kazakhstan's December 2025 Subsoil Use Code amendments, granting the state greater control over new discoveries and license extensions, have materially raised barriers to foreign exploration investment. Combined with a large long-term bilateral supply agreement between Kazatomprom and India, significant uranium volumes are being removed from open-market availability.

Spot price no longer reflects the effective cost of securing supply: Kazatomprom's bilateral agreement with India and Kazakhstan's restrictions on Western exploration licenses are removing low-cost volumes from open-market availability, leaving uncontracted Western buyers with a narrower, higher-cost supply pool than spot benchmarks reflect. Capital previously directed toward Kazakhstan greenfield development is being redirected toward Canada, the United States, and Africa, jurisdictions where regulatory access is not subject to state revocation, raising the global marginal cost of new supply as lower-cost Central Asian development becomes inaccessible to Western investors.

Shift Toward Western Jurisdictions

Canada, the United States, and Africa are absorbing exploration and development capital previously directed toward Central Asia. IsoEnergy is advancing the Hurricane deposit in Saskatchewan's Athabasca Basin, which holds an Indicated resource of 48.6 million pounds of U₃O₈ at an average grade of 34.5%, per the NI 43-101 technical report on the Larocque East Project filed August 4, 2022. Philip Williams, Chief Executive Officer of IsoEnergy, describes the asset's scale and the company's multi-jurisdiction risk management approach:

"Hurricane… where we've made a discovery in 2018, put a resource out in 2022, 34.5% grades, 48.6 million pounds."

Philip Williams also describes IsoEnergy's presence across the top uranium jurisdictions as a deliberate structural position:

"We're a diversified uranium developer, explorer, and near-term producer in the top jurisdictions in the world for uranium, being Canada, the US, and Australia."

ATHA Energy holds the largest uranium exploration land position in Canada at over 7 million acres across the Athabasca Basin, Nunavut, and the Central Mineral Belt. The Angilak Project's 31-kilometer mineralized trend grades up to 5.85% U₃O₈, backed by $115 million in prior investment. A 10% carried interest on lands developed by NexGen Energy and IsoEnergy provides unfunded resource upside.

Zambia's Muntanga Project: Heap Leach Economics

Atomic Eagle's Muntanga project in Zambia represents a distinct entry point into the supply pipeline in Africa. Phil Hoskins, Chief Executive Officer of Atomic Eagle, describes the project's resource base, confirmed by an ASX announcement dated March 10, 2026:

"We recently increased the resource 24% to 58.8 million pounds at 309 ppm, it has a feasibility study."

The Muntanga resource comprises a Measured and Indicated component of 40.0 million pounds at 359 ppm and an Inferred component of 18.8 million pounds at 238 ppm.

AI-Driven Energy Demand Introduces a New Buyer Base

Technology companies are entering nuclear energy procurement as direct participants. Meta announced landmark agreements for new nuclear capacity, while other technology firms are investing directly in Small Modular Reactor programs. AI-driven data centers require uninterrupted baseload power at scale, a requirement intermittent renewable sources cannot reliably fulfill.

This demand is different from traditional utility-driven procurement. Technology firms operate under long-term infrastructure investment mandates and have lower fuel-cost sensitivity than utilities, which are subject to regulated pass-through pricing. Their entry into nuclear energy contracting introduces a demand floor that is less cyclical and more durable than conventional utility demand, effectively adding a second buyer class with no historical price anchor.

This creates new contracting counterparties with institutional capital backing and multi-decade energy commitments, accelerating long-term contracting cycles and providing more bankable revenue profiles to support project financing.

The Investment Thesis for Uranium

The uranium sector in 2026 presents a convergence of structural drivers that support a disciplined long-term investment case across the production and development spectrum.

- Global utility uranium requirements of approximately 180 million pounds per year, against a supply base constrained by geopolitical intervention and jurisdictional consolidation, sustain procurement pressure that no production decision taken in 2026 resolves within the current fuel cycle planning window.

- US Section 232 policy creates the legislative basis for domestic pricing premiums that would structurally advantage producers with US-domiciled assets and integrated milling and conversion infrastructure.

- Kazakhstan's bilateral supply agreement with India are removing volumes from open-market availability, increasing price sensitivity to marginal demand shifts for uncontracted utilities.

- Technology companies entering nuclear energy procurement directly add a capital-backed, lower-price-sensitive demand base that extends beyond traditional utility contracting cycles, supporting durable, long-term contract pricing.

- Development-stage projects with published feasibility studies, confirmed resource classifications, and competitive extraction economics are positioned to capture the supply premium that jurisdictionally stable development now commands.

- Producers and developers with strong institutional balance sheets and demonstrated access to capital markets carry materially lower execution risk than peers reliant on dilutive project-level financing under tighter credit conditions.

- High-grade Athabasca Basin assets and large-scale exploration platforms offer resource expansion optionality, providing asymmetric upside relative to commodity price movements.

The spot price reached $94.28 per pound in January 2026, a two-year high, followed by mid-$80s consolidation, which reflects pricing adjustments driven by three developments absent from prior uranium cycles: US Section 232 creating a legislative basis for domestic procurement preferences, Kazakhstan's amended Subsoil Use Code restricting Western license access, and Kazatomprom's bilateral supply agreement with India removing open-market volumes.

What Q1 2026 establishes is that uranium's price is no longer set solely by the balance between mine supply and utility demand; it is now shaped by which governments control which volumes and under what terms Western buyers can access them, a condition that persists regardless of where spot prices trade in any given quarter.

TL;DR

Uranium's Q1 2026 price movement, spot reaching $94.28 per pound before consolidating into the mid-$80s, was driven by three concurrent government actions: the US Section 232 review creating a legislative basis for domestic procurement preferences, Kazakhstan's December 2025 Subsoil Use Code amendments restricting Western license access, and Kazatomprom's bilateral supply agreement with India removing open-market volumes. Against 180 million pounds per year in global utility requirements, contracting has consistently fallen short, accumulating deferred procurement obligations that no new production decision taken in 2026 resolves within the current fuel cycle planning window. Technology companies entering nuclear procurement directly, without the regulated cost constraints governing utility decisions, introduce a second buyer class that extends demand beyond traditional contracting cycles. Uranium's price is no longer governed solely by mine supply and utility demand; it is now shaped by which governments control which volumes and under what terms Western buyers can access them.

Analyst's Notes

Subscribe to Our Channel

Stay Informed